- Summary

- Table Of Content

- Methodology

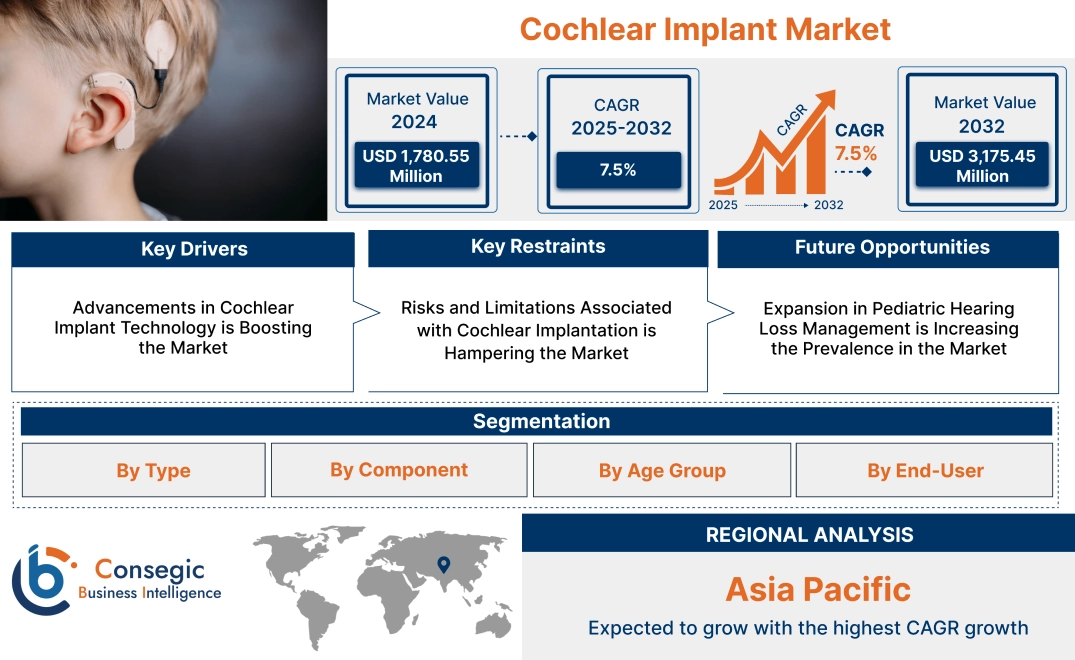

Cochlear Implant Market Size:

Cochlear Implant Market size is estimated to reach over USD 3,175.45 Million by 2032 from a value of USD 1,780.55 Million in 2024 and is projected to grow by USD 1,882.36 Million in 2025, growing at a CAGR of 7.5% from 2025 to 2032.

Cochlear Implant Market Scope & Overview:

The cochlear implants are medical devices designed to provide hearing to individuals with severe to profound sensorineural hearing loss. Cochlear implants bypass damaged parts of the inner ear by directly stimulating the auditory nerve, enabling sound perception. These devices consist of external components, such as microphones and speech processors, and surgically implanted internal components, including electrodes and a receiver-stimulator.

Key characteristics of cochlear implants include high sound clarity, the ability to adapt to various sound environments, and compatibility with advanced technologies like Bluetooth and AI for improved user experience. The benefits include enhanced hearing ability, improved speech recognition, and a significant improvement in the quality of life for users.

Applications span pediatric and adult patient populations, addressing congenital hearing loss, age-related hearing impairment, and hearing loss due to trauma or infections. End-users include hospitals, specialty ENT clinics, and audiology centers, driven by the increasing prevalence of hearing disorders, advancements in implant technology, and supportive healthcare policies and reimbursement frameworks.

Cochlear Implant Market Dynamics - (DRO) :

Key Drivers:

Advancements in Cochlear Implant Technology is Boosting the Market

Recent innovations in cochlear implant technology have significantly enhanced the quality of life for individuals with hearing impairments. Modern cochlear implants feature advanced sound processors, improved electrode arrays, and wireless connectivity options, offering clearer and more natural sound perception. These devices are now equipped with Bluetooth technology and mobile app compatibility, enabling users to connect seamlessly with smartphones and other digital devices, enhancing usability and convenience.

Trends in miniaturization and battery efficiency have further improved device comfort and durability, particularly for pediatric and elderly users. Analysis highlights that such advancements are driving wider adoption, as they align with the demand for personalized and user-friendly medical devices.

Key Restraints:

Risks and Limitations Associated with Cochlear Implantation is Hampering the Market

While cochlear implants provide life-changing benefits, the procedure involves inherent risks and limitations. Surgical complications, such as infections, device failure, or facial nerve damage, can occur, deterring some candidates from opting for the procedure. Additionally, cochlear implants may not provide the desired results for individuals with complex auditory nerve conditions or severe hearing loss.

The high cost of implantation and post-operative rehabilitation also poses a limitation, making it inaccessible to many patients in resource-constrained regions. Trends in patient education and counseling emphasize managing expectations and understanding potential risks, ensuring informed decision-making for candidates.

Future Opportunities :

Expansion in Pediatric Hearing Loss Management is Increasing the Prevalence in the Market

The growing emphasis on early intervention for congenital hearing loss presents significant cochlear implant market opportunities in the cochlear implant market. Early implantation in children has been shown to enhance language development, cognitive skills, and social integration, driving widespread adoption in pediatric care. Advances in neonatal hearing screening programs and increasing parental awareness about the benefits of early cochlear implantation are further bolstering this trend.

Trends in pediatric-focused cochlear implant designs, such as devices tailored for smaller anatomy and robust durability, align with the needs of this demographic. Analysis suggests that continued investment in pediatric care and supportive government initiatives will play a critical role in expanding the market for cochlear implants globally.

Cochlear Implant Market Segmental Analysis :

By Type:

Based on type, the market is segmented into unilateral implants and bilateral implants.

The unilateral implants segment accounted for the largest revenue in the cochlear implant market share in 2024.

- Unilateral implants are widely adopted as a cost-effective solution for individuals with profound hearing loss in one ear.

- High success rates and widespread availability of unilateral implants have contributed to their dominance in the market.

- Increasing awareness about the benefits of cochlear implants for hearing restoration is driving cochlear implant market demand for unilateral devices.

- Technological advancements in implant design, offering improved speech clarity and sound localization, have reinforced segment trends.

The bilateral implants segment is anticipated to register the fastest CAGR during the forecast period.

- Bilateral implants provide better sound localization and improved speech recognition in noisy environments, enhancing patient outcomes.

- Increasing adoption among pediatrics, where bilateral hearing is crucial for language development, is driving trends in this segment.

- Expanding insurance coverage and supportive reimbursement policies for bilateral implants in developed countries are fueling the segment's dominance.

- Rising clinical evidence supporting the cognitive and quality-of-life benefits of bilateral implantation is expected to propel cochlear implant market growth.

By Component:

Based on components, the market is segmented into external components (microphone, speech processor, transmitter) and internal components (receiver/stimulator, electrode array).

The external components segment accounted for the largest revenue in cochlear implant market share in 2024.

- External components, particularly the speech processor, play a critical role in capturing and processing sound signals, making them indispensable.

- Rising advancements in microphone and transmitter technologies have improved sound quality and patient satisfaction.

- Integration of wireless connectivity features in external components, such as Bluetooth-enabled processors, has driven trends.

- Increasing replacement rates for external components due to wear and tear have contributed to segment growth.

The internal components segment is anticipated to register the fastest CAGR during the forecast period.

- Internal components, such as the receiver/stimulator and electrode array, are essential for converting electrical signals into neural impulses.

- Advancements in electrode array technology have improved signal precision and auditory outcomes, driving demand.

- Growing adoption of minimally invasive surgical techniques has enhanced the safety and success rates of internal component implantation.

- Rising research and development investments in biocompatible materials and long-lasting internal components are expected to propel cochlear implant market growth.

By Age Group:

Based on age group, the market is segmented into adults and pediatrics.

The pediatrics segment accounted for the largest revenue share in 2024.

- Early intervention through cochlear implants in children with severe hearing loss is critical for speech and language development.

- Increasing awareness among parents and healthcare providers about the long-term benefits of pediatric implantation has driven trends.

- Government initiatives and funding programs for pediatric hearing loss management in developed and emerging economies are bolstering demand.

- Technological innovations tailored for pediatric patients, such as lightweight and child-friendly designs, have further supported this segment.

The adult segment is anticipated to register the fastest CAGR during the forecast period.

- Rising prevalence of age-related hearing loss and noise-induced hearing damage in adults is driving advancement for cochlear implants.

- Increasing adoption of advanced cochlear implant systems among the adult population, seeking enhanced hearing outcomes, is fueling trends.

- Expanding access to cochlear implant services and reimbursement support for adults in developing regions is contributing to this segment’s growth.

- Growing awareness about the cognitive benefits of hearing restoration in older adults is expected to propel demand for adult cochlear implants.

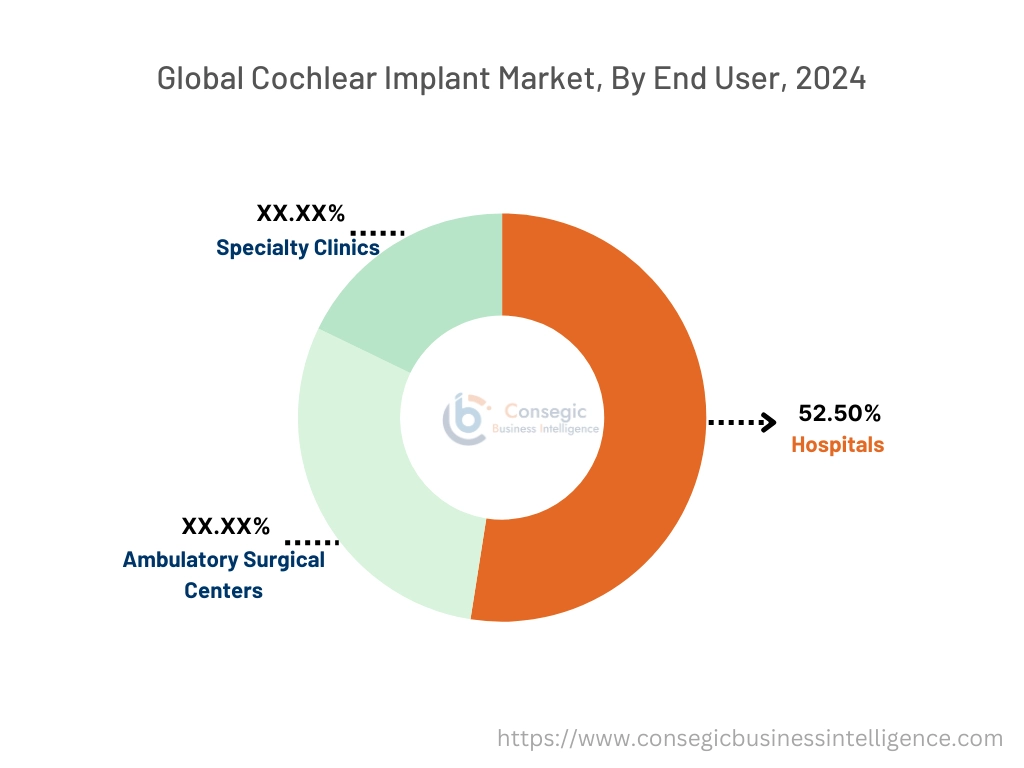

By End-User:

Based on end-users, the market is segmented into hospitals, ambulatory surgical centers, and specialty clinics.

The hospitals segment accounted for the largest revenue share of 52.50% in 2024.

- Hospitals serve as primary care centers for cochlear implantation, offering comprehensive diagnostic, surgical, and post-operative services.

- Availability of skilled professionals and advanced surgical equipment in hospitals ensures superior patient outcomes.

- Rising hospital admissions for hearing loss management, coupled with increasing healthcare infrastructure investments, are driving trends.

- Growing collaborations between hospitals and cochlear implant manufacturers for training and device procurement are further supporting this segment.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics, particularly those focused on audiology and otology, offer tailored cochlear implant services, enhancing patient satisfaction.

- Increasing preference for outpatient surgeries in specialty clinics due to shorter waiting times and cost efficiency is driving development.

- Expansion of specialty clinics in urban and semi-urban areas has improved accessibility to advanced cochlear implantation services.

- Growing partnerships between specialty clinics and device manufacturers for offering cutting-edge technology is expected to propel advancement.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

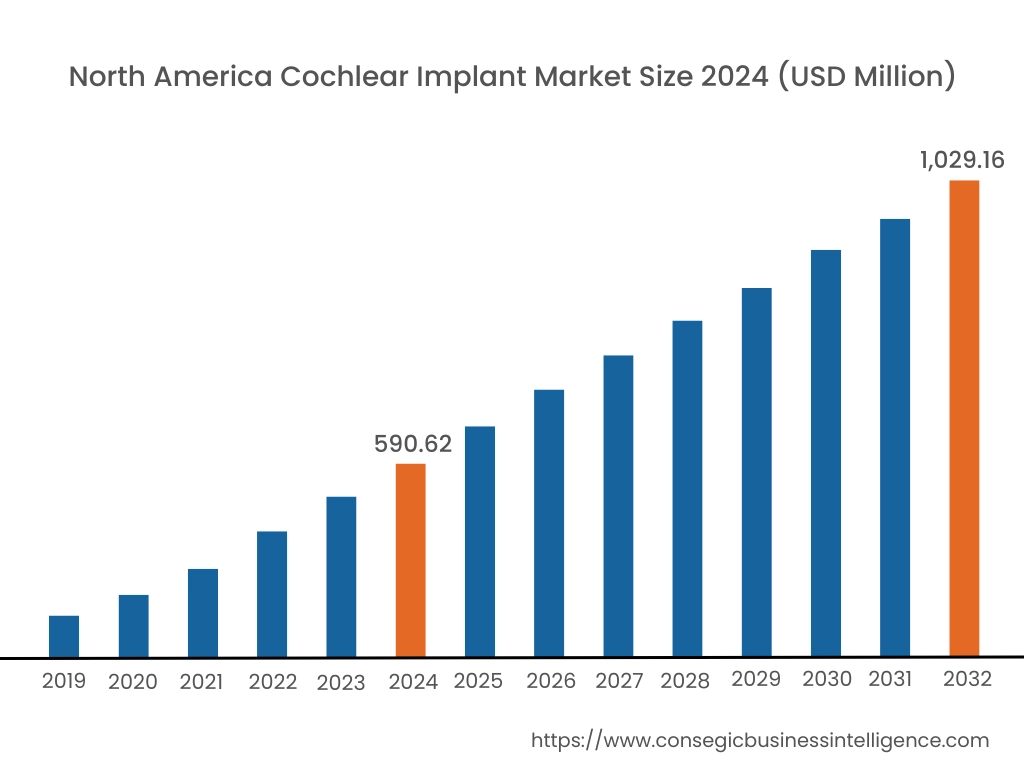

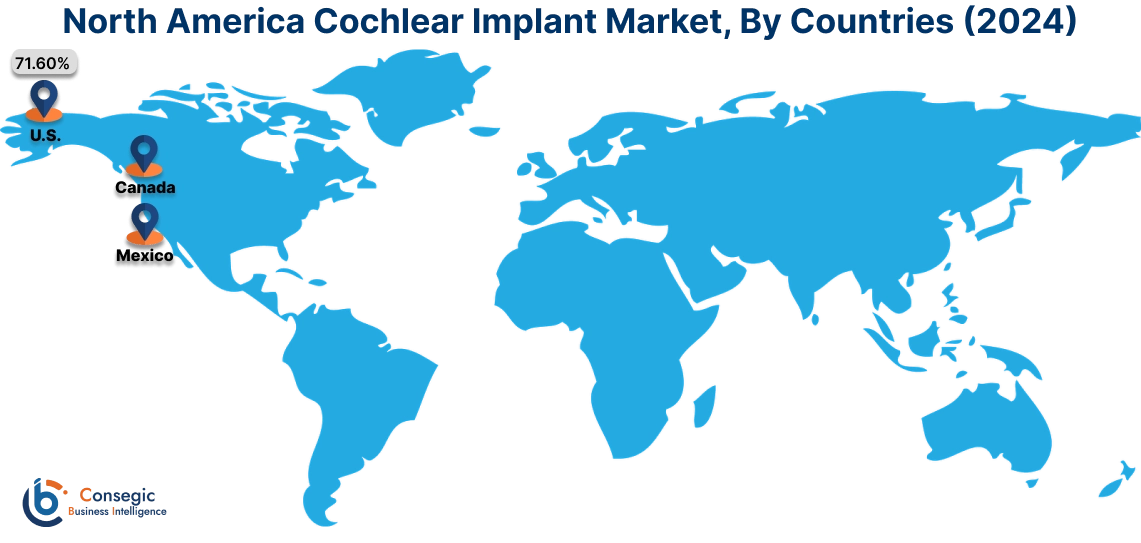

In 2024, North America was valued at USD 590.62 Million and is expected to reach USD 1,029.16 Million in 2032. In North America, the U.S. accounted for the highest share of 71.60% during the base year of 2024. North America holds a significant share of the global cochlear implant market, driven by advanced healthcare infrastructure, high adoption of hearing aid technologies, and increasing awareness about hearing loss treatments. As per the cochlear implant market analysis, the U.S. dominates the region due to robust government initiatives to support cochlear implantation, such as Medicare coverage for eligible patients, and the presence of leading cochlear implant manufacturers. Canada contributes to the rising adoption of cochlear implants in pediatric and geriatric populations, supported by improving healthcare access. However, the high cost of implantation procedures and devices may limit adoption in underserved populations.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.9% over the forecast period. The cochlear implant market analysis is fueled by rapid advancements in healthcare infrastructure, increasing prevalence of hearing disorders, and rising awareness about hearing aids in China, India, and Japan. China dominates the region with a growing demand for cochlear implants in both pediatric and adult populations, supported by government initiatives to improve access to hearing care. India’s expanding healthcare sector drives the adoption of cost-effective implant solutions, particularly in urban areas. Japan emphasizes advanced cochlear implant technologies and precision surgeries, leveraging its strong medical device industry. However, affordability challenges and limited access to specialized care in rural areas may hinder cochlear implant market expansion.

Europe is a prominent market for cochlear implants, supported by an aging population, an increasing prevalence of hearing loss, and strong government initiatives to improve access to hearing aids and implants. Countries like Germany, France, and the UK are key contributors. Germany leads with a well-established healthcare system and advanced audiology clinics, focusing on pediatric and geriatric cochlear implantation. France emphasizes public health programs and subsidies to make cochlear implants accessible to a wider population, while the UK invests in research and early intervention programs for hearing impairment. However, long waiting times for publicly funded implants may pose challenges in some areas.

The Middle East & Africa region is witnessing steady growth in the cochlear implant market, driven by increasing investments in healthcare infrastructure and rising awareness about hearing impairment. In the Middle East, countries like Saudi Arabia and the UAE are adopting advanced implant technologies and improving access to audiology care in hospitals and clinics. In Africa, South Africa is an emerging market, focusing on government initiatives and international collaborations to provide affordable cochlear implants to children and adults with hearing loss. However, limited local expertise and reliance on imports for advanced devices may restrict market development in certain parts of the region.

Latin America is an emerging market for cochlear implants, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and rising prevalence of hearing loss in both pediatric and geriatric populations drive demand for cochlear implants and audiological services. Mexico focuses on expanding access to hearing aids and cochlear implants through public healthcare programs and partnerships with international manufacturers. The region is also emphasizing early intervention and education programs to raise awareness about the benefits of cochlear implantation. However, economic instability and inconsistent healthcare infrastructure may pose challenges to market growth in smaller economies.

Top Key Players and Market Share Insights:

The cochlear implant market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the cochlear implant market. Key players in the Cochlear Implant industry include -

- Cochlear Limited (Australia)

- Sonova Holding AG (Switzerland)

- Hearing Implant Company (United States)

- William Demant Holding A/S (Denmark)

- Shanghai Lishengte Medical Technology Co., Ltd. (China)

- MED-EL (Austria)

- Advanced Bionics AG (Switzerland)

- Oticon Medical (Demant A/S) (Denmark)

- Nurotron Biotechnology Co., Ltd. (China)

- Surgical Specialties Corporation (United States)

Recent Industry Developments :

Product Launches:

- Launched in September 2024, the SONNET 3 offers exceptional sound quality and integrated wireless connectivity, enhancing user experience.

- In June 2024, MED-EL announced a partnership with Microsoft to develop accessible communication technology for individuals with hearing loss, aiming to enhance global communication solutions.

Cochlear Implant Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,175.45 Million |

| CAGR (2025-2032) | 7.5% |

| By Type |

|

| By Component |

|

| By Age Group |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Cochlear Implant Market by 2032? +

Cochlear Implant Market size is estimated to reach over USD 3,175.45 Million by 2032 from a value of USD 1,780.55 Million in 2024 and is projected to grow by USD 1,882.36 Million in 2025, growing at a CAGR of 7.5% from 2025 to 2032.

What are the key drivers for the cochlear implant market? +

Key drivers include advancements in implant technology (e.g., Bluetooth compatibility and AI integration), growing awareness about hearing loss treatments and increasing emphasis on early intervention for pediatric hearing loss.

What challenges does the market face? +

Challenges include risks associated with implantation surgery, high costs of the devices and post-operative care, and limited access to specialized treatment in resource-constrained regions.

Which type of implant dominates the market? +

Unilateral implants hold the largest market share, driven by their cost-effectiveness and high adoption rates for individuals with profound hearing loss in one ear.