- Summary

- Table Of Content

- Methodology

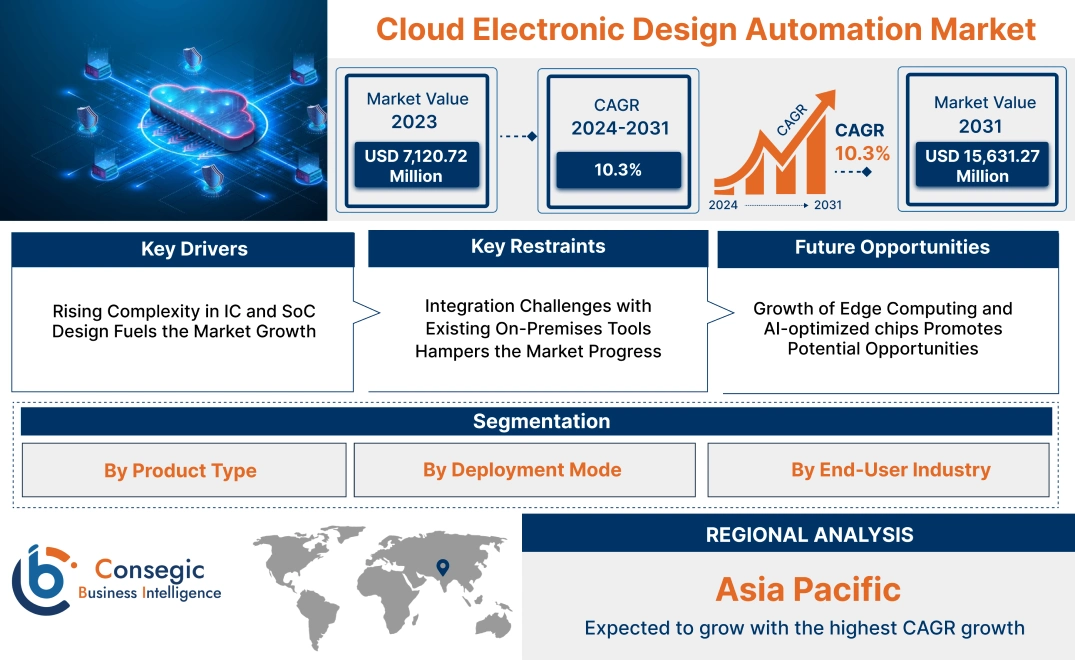

Cloud Electronic Design Automation Market Size:

Cloud Electronic Design Automation Market size is estimated to reach over USD 15,631.27 Million by 2031 from a value of USD 7,120.72 Million in 2023 and is projected to grow by USD 7,729.26 Million in 2024, growing at a CAGR of 10.3% from 2024 to 2031.

Cloud Electronic Design Automation Market Scope & Overview:

Cloud electronic design automation (EDA) refers to the use of cloud-based platforms to perform electronic design processes such as simulation, verification, and testing of electronic systems and integrated circuits. These platforms provide scalable and efficient solutions for managing the complex workflows involved in designing semiconductors and electronic devices. By leveraging cloud infrastructure, cloud EDA enables real-time collaboration, enhanced computational power, and flexibility in handling large-scale designs.

Cloud EDA tools offer features such as high-speed processing, automated design workflows, and integration with advanced analytics, allowing users to optimize performance and reduce time-to-market. These solutions are accessible across various devices, providing convenience and adaptability for design teams working in different locations. Additionally, cloud EDA platforms are equipped with robust security protocols to protect sensitive intellectual property during the design process.

End-users of cloud electronic design automation solutions include semiconductor companies, consumer electronics manufacturers, and research institutions that require advanced tools to streamline design processes and improve operational efficiency. These platforms play a crucial role in accelerating innovation and supporting the development of next-generation electronic products.

Cloud Electronic Design Automation Market Dynamics - (DRO) :

Key Drivers:

Rising Complexity in IC and SoC Design Fuels the Market Growth

The increasing demand for sophisticated integrated circuits (ICs) and system-on-chips (SoCs) in industries like automotive, telecommunications, and consumer electronics has led to more complex design requirements. Advanced features such as higher processing power, energy efficiency, and multi-functional capabilities are driving this complexity. Traditional EDA tools often struggle to meet these demands due to limited scalability and computational capacity.

Cloud-based electronic design automation (EDA) platforms provide a solution by offering high-performance computing capabilities and enabling real-time collaboration among global teams. These platforms streamline the design process, reduce time-to-market, and handle the iterative development cycles required for modern semiconductor devices. Additionally, cloud-based solutions accommodate large data volumes and complex simulations, ensuring accuracy and efficiency in the design of cutting-edge ICs and SoCs. This scalability and flexibility make cloud EDA tools indispensable for addressing the growing challenges in semiconductor design, contributing to the cloud electronic design automation market demand.

Key Restraints :

Integration Challenges with Existing On-Premises Tools Hampers the Market Progress

The transition from traditional on-premises EDA tools to cloud-based platforms poses significant integration challenges for organizations. Many companies have established workflows and infrastructure centered on legacy systems, making compatibility with cloud-based solutions a complex task. Existing on-premises tools often lack the seamless interoperability required for hybrid setups, leading to inefficiencies and disruptions during the transition phase.

Additionally, employees accustomed to traditional tools require retraining to effectively utilize the cloud-based platforms, adding to implementation costs and delays. These challenges are further compounded in industries with stringent design timelines and critical project dependencies, where even minor disruptions lead to significant setbacks. Consequently, the integration process deters companies, especially small and medium-sized enterprises, from fully embracing cloud-based EDA solutions, thereby slowing adoption rates despite the evident advantages of scalability and collaboration offered by cloud platforms. Therefore, the aforementioned factors limit the cloud electronic design automation market growth.

Future Opportunities :

Growth of Edge Computing and AI-optimized chips Promotes Potential Opportunities

The rapid expansion of edge computing and AI-enabled devices is driving demand for sophisticated semiconductor designs tailored to meet the unique requirements of these technologies. Edge computing relies on low-latency, high-performance chips to process data closer to the source, while AI applications demand chips optimized for tasks such as deep learning and real-time decision-making. Designing these advanced chips involves highly iterative and resource-intensive processes, including simulation, verification, and optimization.

Cloud-based EDA platforms provide the scalability, computational power, and collaborative tools necessary to streamline these processes. By enabling faster prototyping and reducing development time, cloud platforms foster innovation in AI and edge computing hardware. This trend is particularly relevant in industries such as automotive, healthcare, and telecommunications, where the integration of edge computing and AI is revolutionizing operations, creating cloud electronic design automation market opportunities.

Cloud Electronic Design Automation Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into Computer-Aided Engineering, Semiconductor Intellectual Property, IC Physical Design & Verification, and Printed Circuit Board and Multi-Chip Module (MCM).

The computer-aided engineering segment accounted for the largest revenue of the total cloud electronic design automation market share in 2023.

- Computer-aided engineering tools streamline complex design and simulation processes, enabling faster prototyping and product iterations.

- These tools are widely adopted in industries such as automotive and aerospace to ensure precision and adherence to stringent regulatory standards.

- The segment's dominance reflects its ability to optimize product designs through advanced simulation and analysis capabilities.

- As per market trends, the growth in adoption of CAE tools is fueled by the increasing complexity of electronic devices and the need for rapid innovation, which further drives the cloud electronic design automation market expansion.

The Semiconductor Intellectual Property segment is expected to register the fastest CAGR during the forecast period.

- Semiconductor IP solutions are essential for enhancing design efficiency and ensuring compatibility in complex chip architectures.

- The rising focus on customized chip designs for emerging applications like IoT and AI is driving the need for reusable IP cores.

- The segment benefits from advancements in process technologies and the shift toward system-on-chip (SoC) designs.

- As per cloud electronic design automation market analysis, increasing collaborations between IP vendors and semiconductor manufacturers further enhance the adoption of semiconductor IP solutions.

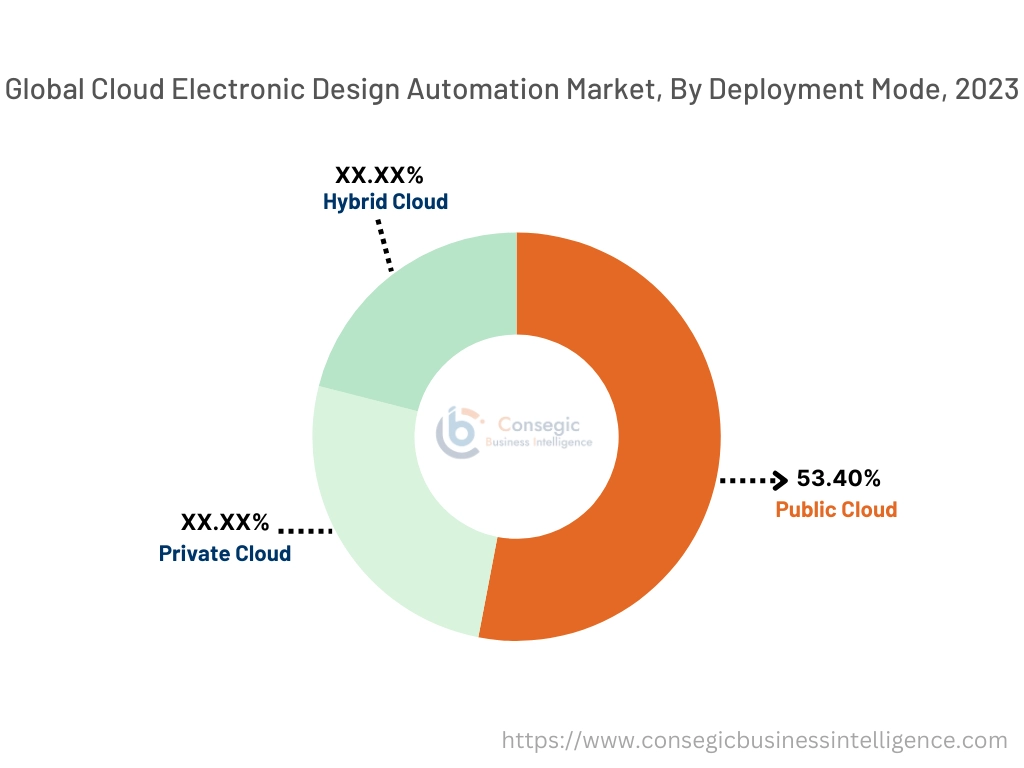

By Deployment Mode:

Based on deployment mode, the market is segmented into public cloud, private cloud, and hybrid cloud.

The Public Cloud segment held the largest revenue of 54.40% in 2023.

- Public cloud deployment offers scalability and cost-effectiveness, making it a preferred choice for small and medium enterprises (SMEs).

- The adoption of the public cloud is driven by its ability to provide on-demand access to high-performance computing resources.

- Cloud-based EDA tools enable real-time collaboration among global teams, reducing time-to-market for electronic designs.

- As per cloud electronic design automation market trends, the dominance of this segment is supported by increasing investments in cloud infrastructure and the extension of global cloud service providers.

The Hybrid Cloud segment is expected to register the fastest CAGR during the forecast period.

- Hybrid cloud deployment combines the flexibility of the public cloud with the control and security of private cloud infrastructure.

- It is increasingly adopted by large enterprises seeking to balance operational efficiency and data privacy concerns.

- Hybrid solutions support seamless integration with legacy systems, ensuring continuity in design workflows.

- As per market analysis, the rising adoption of hybrid cloud is attributed to its adaptability and ability to address diverse operational requirements, fueling the cloud electronic design automation market growth.

By End-User Industry:

Based on the end-user industry, the market is segmented into automotive, aerospace & defense, consumer electronics, healthcare, IT & telecom, and others.

The Automotive segment accounted for the largest revenue share of the total cloud electronic design automation market share in 2023.

- EDA tools play a critical role in designing advanced driver-assistance systems (ADAS) and electric vehicle (EV) components.

- The automotive sector's focus on electrification and autonomous vehicles is driving the adoption of cutting-edge design tools.

- High-performance computing and simulation capabilities enhance the efficiency of chip designs for automotive applications.

- The segment's dominance reflects the industry's growing reliance on EDA tools for innovation and compliance with safety standards, which further facilitates the cloud electronic design automation market demand.

The healthcare segment is expected to register the fastest CAGR during the forecast period.

- EDA tools are increasingly used in designing medical devices, such as wearable health monitors and diagnostic equipment.

- The rising need for precision and miniaturization in healthcare devices boosts the adoption of advanced design tools.

- Collaborations between healthcare providers and semiconductor companies are driving innovation in medical electronics.

- The rapid growth of this segment is supported by advancements in AI-enabled healthcare solutions and increasing regulatory approvals, creating significant cloud electronic design automation market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

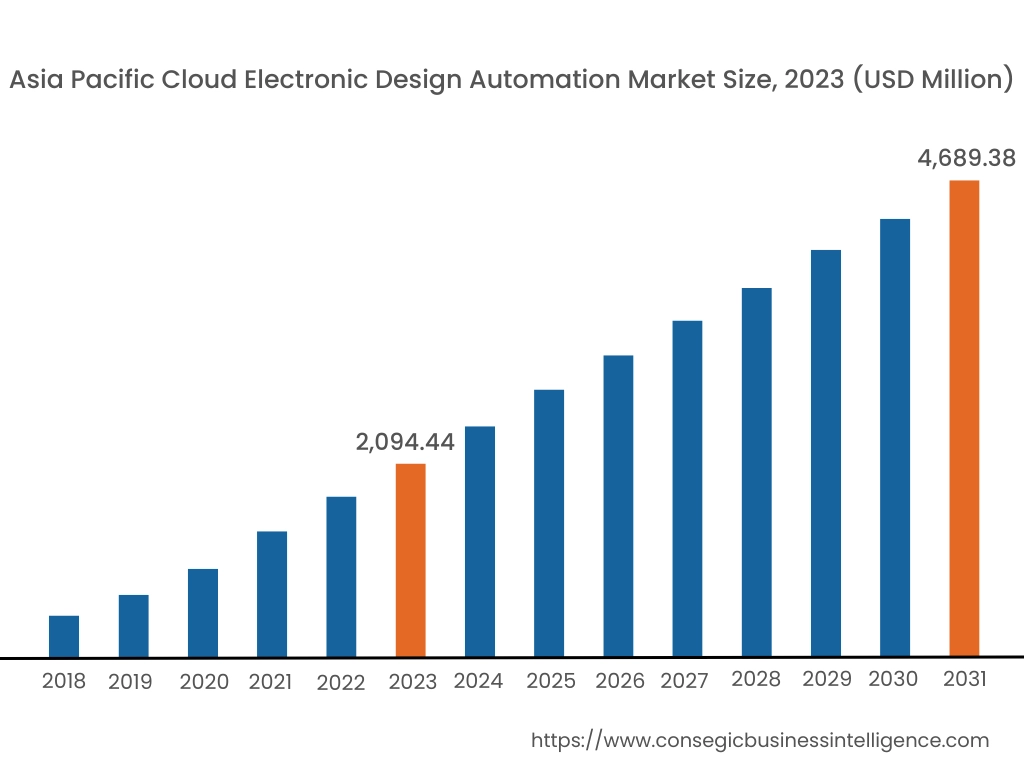

Asia Pacific region was valued at USD 2,094.44 Million in 2023. Moreover, it is projected to grow by USD 2,277.21 Million in 2024 and reach over USD 4,689.38 Million by 2031. Out of these, China accounted for the largest share of 33.7% in 2023. The Asia-Pacific region is experiencing rapid growth in the Cloud EDA market, driven by industrialization and technological advancements in countries such as China, Japan, and India. The proliferation of consumer electronics and the enlargement of the semiconductor sector has intensified the need for efficient and scalable design tools. As per the market trends, government initiatives promoting digital transformation further influence cloud electronic design automation market expansion.

North America is estimated to reach over USD 5,142.69 Million by 2031 from a value of USD 2,366.87 Million in 2023 and is projected to grow by USD 2,566.96 Million in 2024. This region holds a significant share of the Cloud EDA market, driven by the rapid adoption of advanced technologies and the presence of key industry players. The United States, in particular, has seen widespread implementation of cloud-based EDA tools across sectors such as automotive, consumer electronics, and aerospace & defense. The cloud electronic design automation market trends indicate a shift towards integrating cloud computing with EDA solutions has enabled companies to reduce time-to-market and enhance innovation while maintaining or lowering effective costs.

Europe represents a substantial portion of the global Cloud EDA market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's strong emphasis on sustainability and efficient design processes has propelled the use of cloud-based EDA solutions, particularly in the automotive and industrial sectors. Analysis indicates a growing trend towards the adoption of cloud EDA tools to streamline operations and improve product development cycles.

The Middle East & Africa region shows a growing interest in Cloud EDA solutions, particularly in the telecommunications and industrial sectors. Countries like the United Arab Emirates and South Africa are investing in advanced design technologies to support digitalization efforts. Analysis suggests an increasing trend towards adopting cloud-based EDA tools to enhance operational efficiency and support sustainable initiatives.

Latin America is an emerging market for Cloud EDA, with Brazil and Mexico being key contributors. The region's growth in the electronics manufacturing sector and initiatives to promote technological innovation have spurred the adoption of cloud-based design tools. As per cloud electronic design automation market analysis, government policies aimed at modernizing infrastructure and enhancing digital capabilities influence market trends.

Top Key Players and Market Share Insights:

The cloud electronic design automation market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global cloud electronic design automation market. Key players in the cloud electronic design automation industry include -

- Synopsys, Inc. (USA)

- Cadence Design Systems, Inc. (USA)

- Autodesk, Inc. (USA)

- National Instruments Corporation (USA)

- Dassault Systèmes SE (France)

- Siemens Digital Industries Software (Germany)

- Mentor Graphics Corporation (USA)

- Keysight Technologies, Inc. (USA)

- Ansys, Inc. (USA)

- Altium Limited (Australia)

Recent Industry Developments :

Partnerships & Collaborations:

- In December 2024, Marvell Technology expanded its strategic collaboration with Amazon Web Services (AWS) through a five-year, multi-generational agreement. This partnership includes the supply of custom AI products, optical digital signal processors, active electrical cable DSPs, PCIe retimers, data center interconnect optical modules, and Ethernet switching silicon solutions. Additionally, Marvell will utilize AWS's cloud infrastructure for electronic design automation, aiming to enhance data center computing, networking, and storage offerings.

- In July 2023, Siemens Digital Industries Software announced an expansion of its Strategic Collaboration Agreement with Amazon Web Services (AWS) to enhance the accessibility, scalability, and flexibility of Siemens' Electronic Design Automation (EDA) portfolio on AWS. This collaboration aims to help integrated circuit (IC) and electronics design customers leverage AWS's advanced cloud services to shorten design cycles, optimize engineering resources, and boost verification coverage using Siemens EDA products.

- In February 2023, Marvell Technology expanded its strategic collaboration with Amazon Web Services (AWS) to enhance its electronic design automation (EDA) processes by adopting a cloud-first approach. This partnership enables Marvell to leverage AWS's scalable compute infrastructure, allowing for rapid scaling of EDA workloads and more efficient silicon design cycles. The collaboration also includes Marvell providing AWS with data center silicon solutions tailored to support demanding, business-critical workloads.

Product Launches:

- In October 2023, Synopsys introduced the Synopsys Cloud OpenLink Program, aiming to enhance interoperability within the semiconductor design ecosystem. This initiative allows chip designers to seamlessly integrate third-party electronic design automation (EDA) tools and intellectual property (IP) into the Synopsys Cloud environment. By providing an open application programming interface (API), the program facilitates secure system-to-system interactions, enabling efficient access to a diverse range of EDA solutions, IP, and foundry technologies.

Cloud Electronic Design Automation Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 15,631.27 Million |

| CAGR (2024-2031) | 10.3% |

| By Product Type |

|

| By Deployment Mode |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Cloud Electronic Design Automation Market? +

Cloud Electronic Design Automation Market size is estimated to reach over USD 15,631.27 Million by 2031 from a value of USD 7,120.72 Million in 2023 and is projected to grow by USD 7,729.26 Million in 2024, growing at a CAGR of 10.3% from 2024 to 2031.

What are the key segments in the Cloud Electronic Design Automation Market? +

The Cloud Electronic Design Automation Market is segmented by product type (Computer Aided Engineering, Semiconductor Intellectual Property, IC Physical Design & Verification, Printed Circuit Board and Multi-Chip Module), deployment mode (Public Cloud, Private Cloud, Hybrid Cloud), end-user industry (Automotive, Aerospace & Defense, Consumer Electronics, Healthcare, IT & Telecom), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which region is expected to dominate the Cloud Electronic Design Automation Market? +

The Asia-Pacific region is expected to dominate the Cloud Electronic Design Automation Market, driven by industrialization and technological advancements in countries such as China, India, and Japan, along with government initiatives promoting digital transformation.

Who are the key players in the Cloud Electronic Design Automation Market? +

Key players in the Cloud Electronic Design Automation Market include Synopsys, Inc. (USA), Cadence Design Systems, Inc. (USA), Siemens Digital Industries Software (Germany), Mentor Graphics Corporation (USA), Keysight Technologies, Inc. (USA), Ansys, Inc. (USA), Altium Limited (Australia), Autodesk, Inc. (USA), National Instruments Corporation (USA), and Dassault Systèmes SE (France).