- Summary

- Table Of Content

- Methodology

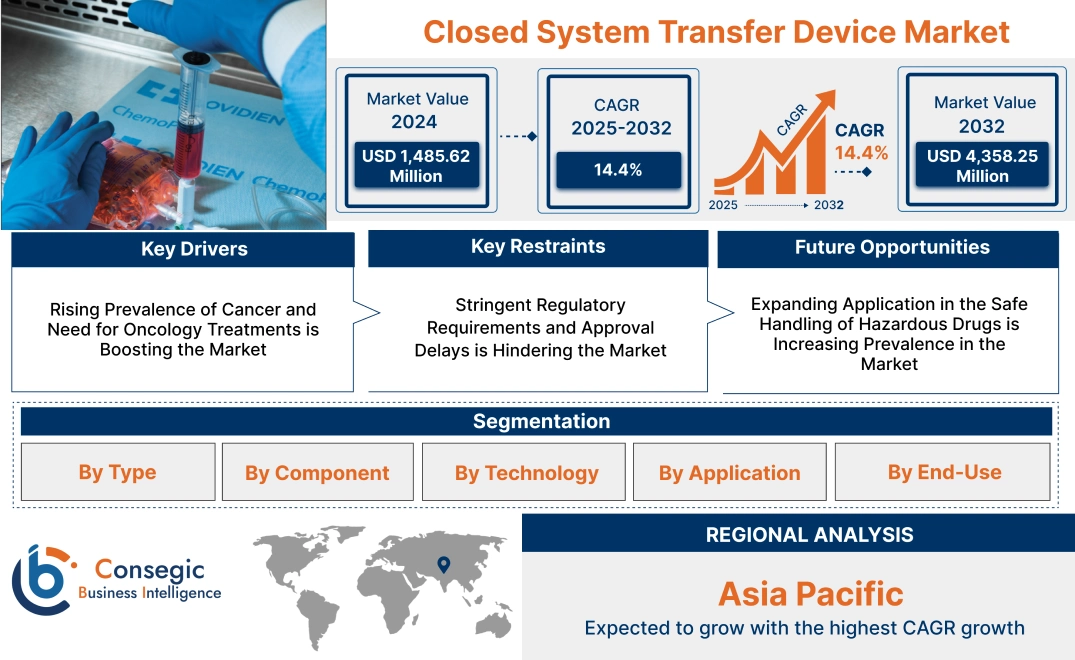

Closed System Transfer Device Market Size:

Closed System Transfer Device Market size is estimated to reach over USD 4,358.25 Million by 2032 from a value of USD 1,485.62 Million in 2024 and is projected to grow by USD 1,673.08 Million in 2025, growing at a CAGR of 14.4% from 2025 to 2032.

Closed System Transfer Device Market Scope & Overview:

The closed system transfer device (CSTD) is designed to safely transfer hazardous drugs and other compounds, preventing contamination and protecting healthcare workers from exposure. These devices use innovative technologies to create a closed environment, ensuring the safe preparation, transport, and administration of medications. Key characteristics of CSTDs include airtight and leak-proof seals, compatibility with a range of drug vials and syringes, and adherence to stringent safety standards. The benefits include enhanced occupational safety, reduced risk of drug exposure, and compliance with regulatory requirements for handling hazardous substances. Applications span oncology drug administration, compounding pharmacies, and healthcare facilities managing cytotoxic drugs. End-users include hospitals, specialty clinics, and pharmacies, driven by increasing cancer prevalence, rising awareness of occupational safety, and stringent regulatory frameworks mandating the use of safety devices in hazardous drug handling.

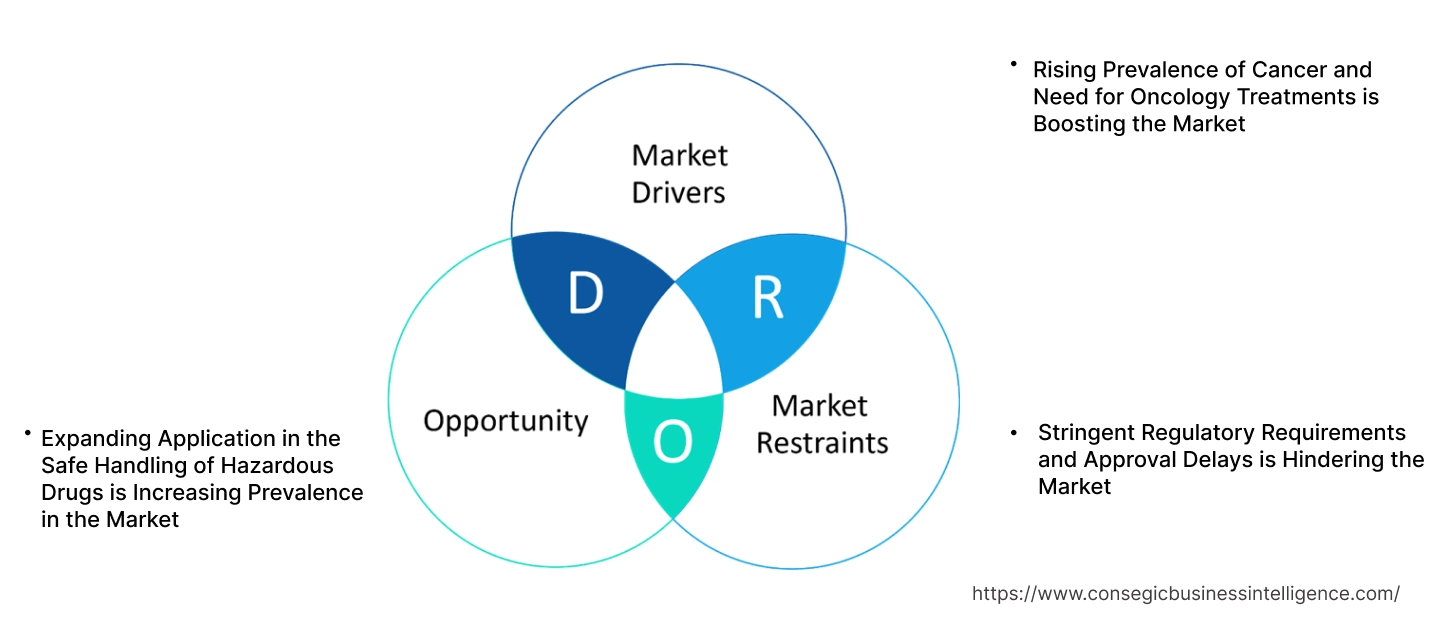

Closed System Transfer Device Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Cancer and Need for Oncology Treatments is Boosting the Market

The increasing prevalence of cancer globally has significantly elevated the use of hazardous drugs, particularly chemotherapy agents. Closed System Transfer Devices (CSTDs) play a crucial role in ensuring the safe preparation, transfer, and administration of these drugs, protecting healthcare workers and patients from exposure to harmful chemicals. With advancements in personalized cancer therapies and complex treatment regimens, the importance of precise drug handling has grown exponentially.

Trends in oncology care, including outpatient and home-based chemotherapy delivery, have highlighted the value of CSTDs in reducing contamination risks and maintaining drug integrity. The analysis underscores that the role of CSTDs in improving safety and efficiency in oncology treatment workflows makes them indispensable in modern cancer care practices.

Key Restraints:

Stringent Regulatory Requirements and Approval Delays is Hindering the Market

The development and commercialization of CSTDs are subject to rigorous regulatory guidelines and standards to ensure safety, efficacy, and compliance. Navigating these regulatory landscapes can be time-consuming and costly, particularly for smaller manufacturers or companies expanding into new markets. Delays in product approvals, along with the need for periodic updates to meet evolving standards, can hinder the availability of CSTDs in certain regions.

Trends in healthcare compliance and heightened scrutiny of hazardous drug handling protocols further emphasize the need for continuous innovation and adherence to regulatory frameworks. Analysis suggests that streamlining approval processes and aligning with global standards can help overcome these challenges while ensuring consistent product availability.

Future Opportunities :

Expanding Application in the Safe Handling of Hazardous Drugs is Increasing Prevalence in the Market

CSTDs are increasingly being adopted for the safe handling of hazardous drugs beyond oncology, including immunosuppressants, antiviral medications, and other high-risk pharmaceuticals. These devices provide a closed environment that prevents contamination and exposure, making them vital in protecting healthcare workers across various specialties. Their ability to ensure safety during drug preparation and administration aligns with global trends in enhancing occupational health standards.

The analysis highlights that the adoption of CSTDs in broader applications, such as clinical trials and pharmaceutical compounding, presents significant closed system transfer device market opportunities for closed system transfer device market expansion. As healthcare facilities continue to prioritize safety and efficiency in hazardous drug handling, CSTDs are positioned as a critical solution to address these evolving needs.

Closed System Transfer Device Market Segmental Analysis :

By Type:

Based on type, the (CSTD) market is segmented into membrane-to-membrane systems and needleless systems.

The membrane-to-membrane systems segment accounted for the largest revenue in the closed system transfer device market share in 2024.

- Membrane-to-membrane systems are extensively used due to their superior capability to prevent hazardous drug leakage and ensure airtight sealing.

- These systems employ dual-membrane barriers that create a secure transfer environment, minimizing contamination risks during drug preparation and administration.

- Membrane-to-membrane systems are particularly suitable for handling cytotoxic drugs used in chemotherapy treatments, ensuring safety for healthcare professionals and patients.

- The increasing prevalence of cancer, which has heightened the demand for chemotherapy drugs, has significantly contributed to the adoption of membrane-to-membrane systems.

- Additionally, the growing focus on workplace safety in healthcare institutions and adherence to stringent regulatory guidelines have further bolstered the demand for these systems globally.

The needleless systems segment is anticipated to register the fastest CAGR during the forecast period.

- Needleless systems are rapidly gaining traction as a safer alternative to traditional systems.

- These systems eliminate the risk of needle-stick injuries, a common hazard for healthcare workers handling hazardous drugs.

- Needleless CSTDs are designed to simplify workflows, reduce handling time, and improve overall safety during drug transfer.

- The rising adoption of needleless technology in oncology clinics, pharmacies, and ambulatory surgical centers is driving segment closed system transfer device market growth.

- Furthermore, the ongoing advancements in needleless designs to enhance compatibility with existing medical equipment are expected to boost their adoption.

By Component:

Based on components, the (CSTD) market is segmented into vial access devices, syringe safety devices, bag/line access devices, and accessories.

The vial access devices segment accounted for the largest revenue in the closed system transfer device market share in 2024.

- Vial access devices are crucial for safely accessing and transferring drugs from vials to syringes or infusion bags.

- These devices form an airtight seal to prevent contamination and protect against hazardous drug exposure.

- Vial access devices are widely used in hospitals and pharmacies, where large volumes of drug compounding and preparation occur.

- The increasing demand for chemotherapy drug preparation and the growing use of hazardous drugs in treating chronic diseases have reinforced the trends for vial access devices in the market.

The syringe safety devices segment is anticipated to register the fastest CAGR during the forecast period.

- Syringe safety devices are designed to ensure the secure handling of hazardous drugs during preparation and administration.

- These devices help prevent spills, leaks, and accidental exposure to toxic substances.

- Their application is expanding across oncology clinics and ambulatory surgical centers, where high volumes of drug administration occur.

- The growing focus on protecting healthcare workers from occupational hazards, combined with advancements in syringe safety technology, is expected to drive significant growth in this segment.

By Technology:

The diaphragm-based systems segment accounted for the largest revenue share in 2024.

- Diaphragm-based systems are widely adopted due to their reliable sealing mechanism, preventing drug aerosolization and contamination.

- These systems use a flexible diaphragm to create a physical barrier, ensuring sterility and safety during drug transfer.

- Their extensive use in chemotherapy drug preparation and hazardous drug handling has made them a critical component in hospital pharmacies and oncology clinics.

- The increasing prevalence of cancer and the rising adoption of diaphragm-based CSTDs in healthcare facilities have strengthened their market position.

The air cleaning/filtration systems segment is anticipated to register the fastest CAGR during the forecast period.

- Air cleaning/filtration systems capture airborne contaminants, providing an additional safety layer during hazardous drug handling.

- These systems are essential in compounding and administration processes, where the prevention of toxic particle release is critical.

- Rising awareness of healthcare worker safety and compliance with regulatory standards are driving their adoption in hospitals and specialized clinics.

- Growing investments in advanced air filtration technologies are further supporting the rapid expansion of this segment.

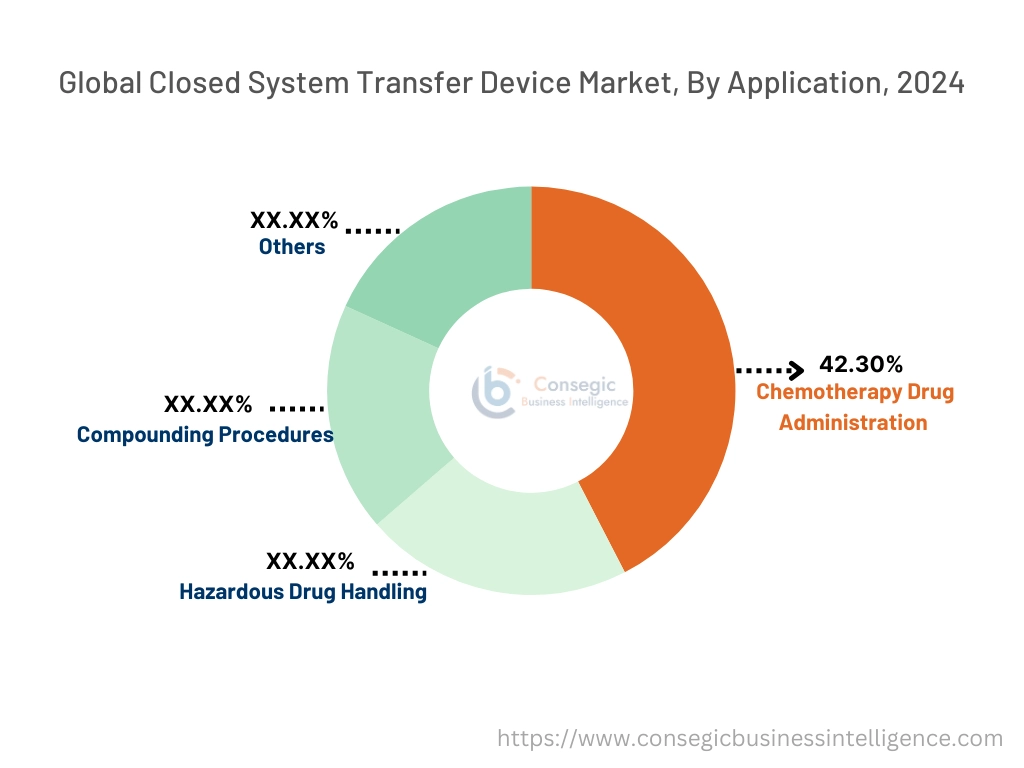

By Application:

The chemotherapy drug administration segment accounted for the largest revenue of 42.30% share in 2024.

- CSTDs are indispensable for minimizing exposure to toxic substances during chemotherapy drug administration.

- These devices ensure a contamination-free transfer process, protecting both healthcare workers and patients.

- The rising global prevalence of cancer and increasing use of cytotoxic drugs in oncology treatments are driving closed system transfer device market demand for CSTDs in this segment.

- Regulatory mandates requiring the use of CSTDs in chemotherapy drug handling have further solidified this segment’s trends.

The hazardous drug handling segment is anticipated to register the fastest CAGR during the forecast period.

- CSTDs are critical in mitigating exposure risks during hazardous drug compounding, preparation, and administration.

- These devices ensure compliance with occupational safety guidelines and regulatory standards, such as OSHA and NIOSH.

- Growing adoption in pharmacies, oncology clinics, and ambulatory surgical centers highlights their importance in healthcare settings.

- Increasing focus on workplace safety and advancements in drug handling technologies are expected to drive growth in this segment.

By End-Use:

Based on end-use, the (CSTD) market is segmented into hospitals, oncology clinics, ambulatory surgical centers, and others.

The hospitals segment accounted for the largest revenue share in 2024.

- Hospitals are major end-users of CSTDs due to the high volume of chemotherapy treatments and hazardous drug-handling procedures, especially in oncology departments and pharmacies.

- CSTDs are essential for ensuring healthcare worker safety by minimizing exposure to cytotoxic drugs and enhancing compliance with regulatory standards such as OSHA and NIOSH guidelines.

- Rising cancer prevalence and growing investments in oncology care infrastructure have led hospitals to adopt advanced CSTD technologies to meet increasing demand.

- Hospitals also focus on improving operational efficiency, reducing drug wastage, and maintaining sterility, which further drives the adoption of CSTDs across these facilities.

The oncology clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Oncology clinics are rapidly adopting CSTDs to safely handle and administer chemotherapy drugs for outpatient cancer treatments, where safety and efficiency are critical.

- The expansion of oncology clinics globally, driven by rising cancer incidences and the preference for cost-effective outpatient care trends, has increased the use of CSTDs.

- Technological advancements, such as needleless systems and compact CSTD designs, have made these devices more accessible and easier to integrate into clinical workflows.

- Growing awareness of regulatory compliance and the benefits of CSTDs for protecting staff and patients from hazardous drug exposure is accelerating their adoption in oncology clinics.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

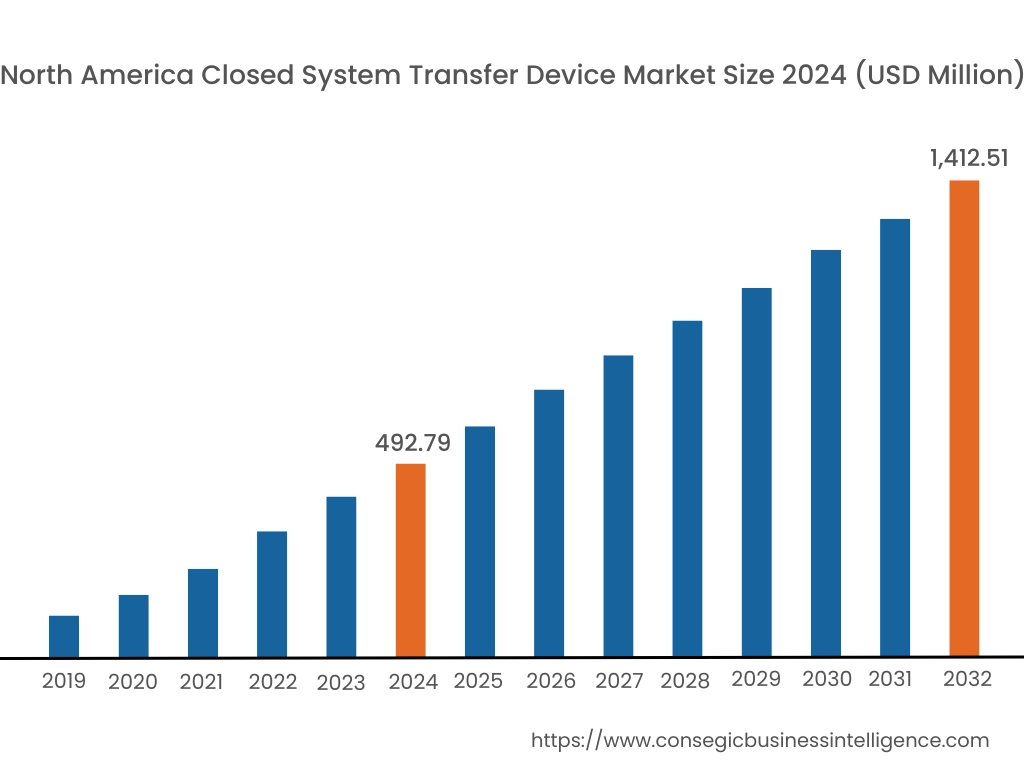

In 2024, North was valued at USD 492.79 Million and is expected to reach USD 1,412.51 million in 2032. In North America, the U.S. accounted for the highest share of 72.80% during the base year of 2024. North America holds a significant stake in the closed system transfer device market, driven by stringent regulations for hazardous drug handling and a well-established healthcare infrastructure. The U.S. dominates the region due to the increasing adoption of CSTDs in oncology and chemotherapy drug administration to protect healthcare workers from exposure to cytotoxic drugs. Canada contributes to growing awareness of workplace safety in healthcare settings and rising investments in advanced medical technologies. However, the high cost of CSTD systems may limit adoption in smaller healthcare facilities.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 14.9% over the forecast period. The closed system transfer device market analysis shows, that it is fueled by rapid advancements in healthcare infrastructure and increasing awareness about occupational safety in China, India, and Japan. China dominates the region with rising demand for CSTDs in oncology departments to handle hazardous drugs safely. India’s growing healthcare sector, driven by government initiatives and increasing cancer prevalence, supports the adoption of CSTDs in hospitals and specialty clinics. Japan focuses on high-precision CSTDs to enhance patient and healthcare worker safety in advanced medical settings. However, limited awareness and high costs may hinder adoption in smaller healthcare facilities in emerging economies.

Europe is a prominent market for closed system transfer devices, supported by strict workplace safety regulations and increasing cancer treatment cases. As per the closed system transfer device market analysis countries like Germany, France, and the UK are key contributors. Germany leads with significant adoption of CSTDs in hospitals and oncology centers to ensure compliance with EU safety standards. France focuses on integrating CSTDs in chemotherapy and other hazardous drug preparation processes, while the UK emphasizes worker safety through the mandatory use of advanced drug transfer systems in healthcare settings. However, budget constraints in some healthcare systems may restrict adoption in smaller hospitals and clinics.

The Middle East & Africa region is witnessing steady growth in the closed system transfer device market trends, driven by increasing investments in healthcare infrastructure and rising cancer treatment cases. As per the analysis countries like Saudi Arabia and the UAE are adopting CSTDs in hospitals and oncology centers to enhance workplace safety and meet international healthcare standards. In Africa, South Africa is emerging as a market with growing awareness of occupational hazards in healthcare and increasing use of CSTDs in specialized medical facilities. However, limited local availability and affordability challenges may restrict broader adoption across the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s expanding healthcare sector and an increasing number of oncology centers drive closed system transfer device market demand for CSTDs to ensure the safe handling of hazardous drugs. Mexico emphasizes the use of CSTDs in hospitals and cancer treatment facilities to protect healthcare workers from exposure risks. The region’s focus on improving healthcare infrastructure and aligning with global safety standards supports closed system transfer device market growth. However, economic instability and inconsistent regulatory frameworks may pose challenges to closed system transfer device market trends in some parts of the region.

Top Key Players and Market Share Insights:

The closed system transfer device market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the closed system transfer device market. Key players in the closed system transfer device industry include -

- Becton, Dickinson and Company (BD) (USA)

- ICU Medical, Inc. (USA)

- Yukon Medical, LLC (USA)

- Caragen Ltd. (Ireland)

- JMS North America Corporation (USA)

- Braun Melsungen AG (Germany)

- Baxter International Inc. (USA)

- Equashield LLC (USA)

- Simplivia Healthcare (Israel)

- Corvida Medical (USA)

Recent Industry Developments :

Research and Trials:

- In February 2024, NIOSH is developing a unified test protocol applicable to both air-cleaning and physical barrier types of CSTDs. This initiative aims to establish standardized performance criteria, ensuring that CSTDs effectively contain hazardous drugs and prevent environmental contamination.

Closed System Transfer Device Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4,358.25 Million |

| CAGR (2025-2032) | 14.4% |

| By Type |

|

| By Component |

|

| By Technology |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Closed System Transfer Device Market by 2032? +

Closed System Transfer Device Market size is estimated to reach over USD 4,358.25 Million by 2032 from a value of USD 1,485.62 Million in 2024 and is projected to grow by USD 1,673.08 Million in 2025, growing at a CAGR of 14.4% from 2025 to 2032.

What factors are driving the growth of the CSTD market? +

The increasing prevalence of cancer and the associated rise in chemotherapy treatments are key drivers. Additionally, stringent regulatory frameworks emphasizing workplace safety, coupled with advancements in CSTD technologies, are fueling market growth.

What challenges does the CSTD market face? +

Stringent regulatory requirements and delays in product approvals are major challenges. Additionally, the high cost of CSTDs may limit their adoption, especially in smaller healthcare facilities and emerging markets.