- Summary

- Table Of Content

- Methodology

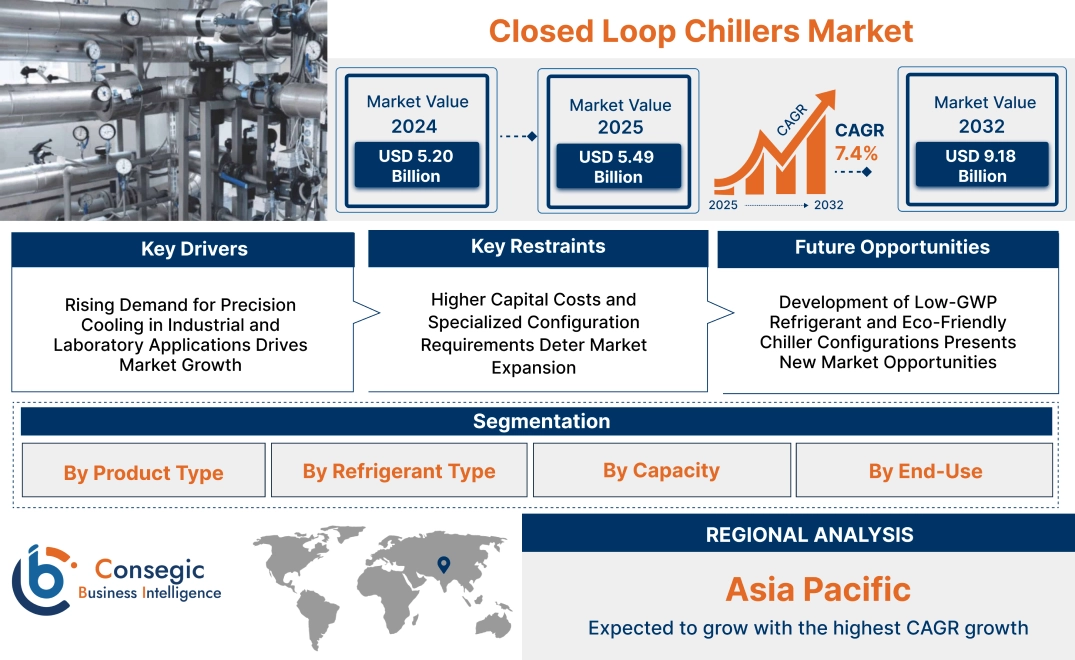

Closed Loop Chillers Market Size:

Closed Loop Chillers Market size is estimated to reach over USD 9.18 Billion by 2032 from a value of USD 5.20 Billion in 2024 and is projected to grow by USD 5.49 Billion in 2025, growing at a CAGR of 7.4% from 2025 to 2032.

Closed Loop Chillers Market Scope & Overview:

Closed loop chillers are temperature regulation systems designed to transfer coolant around an independent closed circuit, excluding process fluid from ambient contaminants and guaranteeing thermal stability. These systems find regular use in industrial processes, labs, medical instrumentation, and precise manufacturing facilities where continuous cooling is a priority.

The key components of these systems are built-in refrigeration hardware, insulated reservoirs, recirculating pumps, and temperature control assemblies. Sealed-loop construction reduces fluid evaporation, contamination, and maintenance requirements. The chillers provide reliable operation under diverse load conditions and enable clean, efficient cooling of critical systems.

They provide accurate temperature control, enhanced system reliability, and efficient energy consumption. They allow multiple configurations to offer flexibility of installation and interfacing with advanced thermal systems. With their potential for safeguarding equipment and guaranteeing continuous output, they form an essential solution for operations with a need for precise, undisturbed cooling performance in controlled environments.

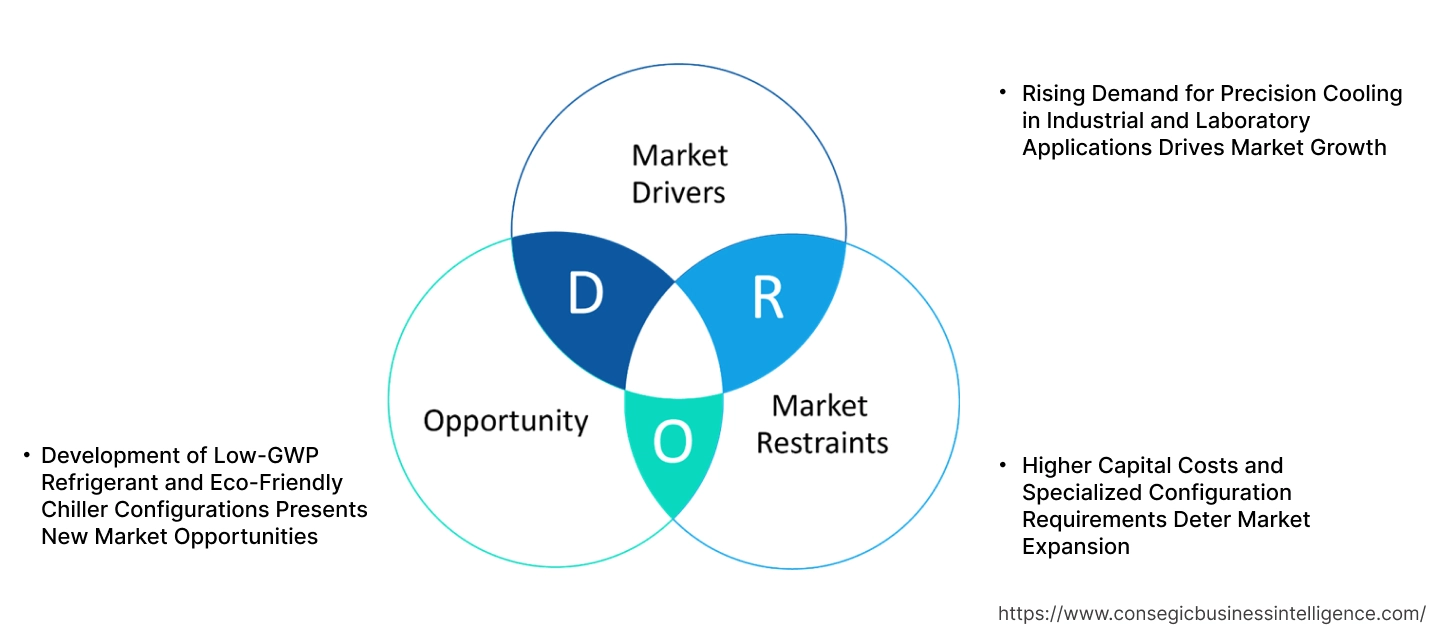

Closed Loop Chillers Market Dynamics - (DRO):

Key Drivers:

Rising Demand for Precision Cooling in Industrial and Laboratory Applications Drives Market Growth

Closed-loop chillers are commonly used in applications that require accurate temperature control and equipment protection from surrounding contaminants. Analytical instruments, medical diagnostics, and laser processing depend on thermal stability to preserve equipment accuracy and avoid performance drift. They keep a constant coolant temperature using sealed recirculation loops, decoupling process fluids from outside water sources and reducing corrosion or mineral deposition. Laboratory settings appreciate lower thermal fluctuation, essential for sample preservation and measurement accuracy. In manufacturing, their application in processes like 3D printing, CNC machining, and semiconductor testing improves process reliability and equipment longevity. The widening range of temperature-sensitive processes is driving the need for dependable and isolated thermal control systems. As industries embrace more high-performance technologies demanding thermal accuracy, the position of engineered cooling systems is increasingly pivotal—fueling closed loop chillers market expansion.

Key Restraints:

Higher Capital Costs and Specialized Configuration Requirements Deter Market Expansion

Closed-loop chillers typically entail higher up-front investment than traditional open-loop or ambient-cooled systems. Corrosion-resistant materials, sealed loops of circulation, and built-in controls contribute to higher unit cost. System design also has to be tailored by fluid chemistry, flow rate, pressure drop, and heat load, necessitating engineering time and expert participation. For those buildings with typical cooling needs, such complexity is hard to justify. In less capital-intensive laboratory environments or in low-cost-of-capital production settings, customers often use less sophisticated options that have lower precision but reduced capital costs. The lack of off-the-shelf or modular solutions also increases procurement time and implementation risk. These economic and technical challenges reduce adoption across applications outside of high-precision or mission-critical environments. Therefore, even with growing demand for next-generation cooling, cost and customization continue to be ongoing hurdles to closed loop chillers market growth.

Future Opportunities:

Development of Low-GWP Refrigerant and Eco-Friendly Chiller Configurations Presents New Market Opportunities

Environmental regulations are leading chiller makers towards embracing low-global warming potential (GWP) refrigerants like R-513A, R-1234yf, and natural substitutes like CO₂. Closed loop chillers that accommodate these eco-friendly refrigerants are finding increased favor in applications wherein environmental regulation compliance and carbon reduction are the thrust. The design that incorporates variable-speed compressors, energy conserving controls, and low charge systems of refrigerants is enhancing both ecological and energy-saving capabilities. These innovations resonate with industries focused on ESG goals and green building standards. Climate-responsible industrial facilities are in increasing demand for pharmaceuticals, electronics, and food manufacturing, particularly where F-gas phase-down regulations are in effect. Chillers that combine thermal accuracy with regulatory compliance are increasingly becoming strategic assets for visionary facilities.

- For instance, in June 2024, Laird Thermal Systems unveiled the new eco-friendly EFC Chiller with natural refrigerant R-290. This high-performing product range provides zero ozone depletion potential (ODP) and low global warming potential (GWP) operation. With a cooling capacity of 2350 watts, the chillers contain a user-friendly touch screen for easy operation. Charged with less than 100 g of refrigerant, these chillers are suitable for air freight.

These innovations are unleashing differentiated value propositions, underpinning closed loop chillers market opportunities fueled by necessity and growth in sustainable cooling technologies.

Closed Loop Chillers Market Segmental Analysis :

By Product Type:

Based on product type, the closed loop chillers market is segmented into air-cooled, water-cooled, and evaporative cooled closed loop chillers.

The air-cooled segment held the largest revenue share in 2024.

- Air-cooled chillers offer simplified installation and lower maintenance due to the absence of cooling towers, making them favorable in commercial and light industrial settings.

- These chillers are ideal for facilities with space constraints or where water availability is limited, thus supporting their widespread adoption.

- Increasing need for compact and modular cooling systems across data centers and manufacturing plants has driven segment expansion.

- For instance, in September 2024, Daikin launched a new glycol-free option for air-cooled free cooling chillers. The absence of glycol results in significant cost savings, making maintenance easier and improving its efficiency. Moreover, it minimizes contamination risks in industrial processes.

- According to closed loop chillers market analysis, their energy efficiency and cost-effective performance further bolster usage in long-term industrial operations.

The evaporative cooled segment is projected to witness the fastest CAGR over the forecast period.

- Evaporative chillers operate with higher thermal efficiency by utilizing both air and water, reducing energy consumption in high-capacity installations.

- Growing focus on sustainable solutions has increased the adoption of hybrid and evaporative systems across large-scale manufacturing plants.

- These systems support stable temperature regulation in varying environmental conditions, making them suitable for high-load operations.

- As per closed loop chillers market trends, rising need for eco-efficient systems with reduced water and power usage is accelerating this segment's growth.

By Refrigerant Type:

Based on refrigerant type, the market is categorized into R-134a, R-410A, R-407C, R-404A, natural refrigerants (e.g., ammonia, CO₂), and others.

The R-134a refrigerant segment accounted for the largest closed loop chillers market share in 2024.

- R-134a is widely used in closed loop chillers due to its high thermal stability, non-flammability, and suitability across diverse climates.

- Its proven compatibility with various compressor types supports its integration in commercial, pharmaceutical, and industrial chillers.

- The ease of retrofit and availability of system components further encourage its deployment in legacy and new systems alike.

- Thus, R-134a continues to be a reliable choice for medium and high-temperature cooling systems due to its desirable attributes, driving closed loop chillers market growth.

The natural refrigerants segment is expected to grow at the fastest CAGR.

- Growing regulatory restrictions on synthetic refrigerants have fueled interest in natural refrigerants like ammonia and CO₂, which have lower global warming potential (GWP).

- Advancements in compressor design and corrosion-resistant materials have improved system safety and efficiency when using natural refrigerants.

- Industries such as food processing and pharmaceuticals are increasingly adopting these eco-friendly refrigerants to meet ESG targets.

- This aligns with closed loop chillers market trends emphasizing green technology adoption and compliance with evolving international climate regulations.

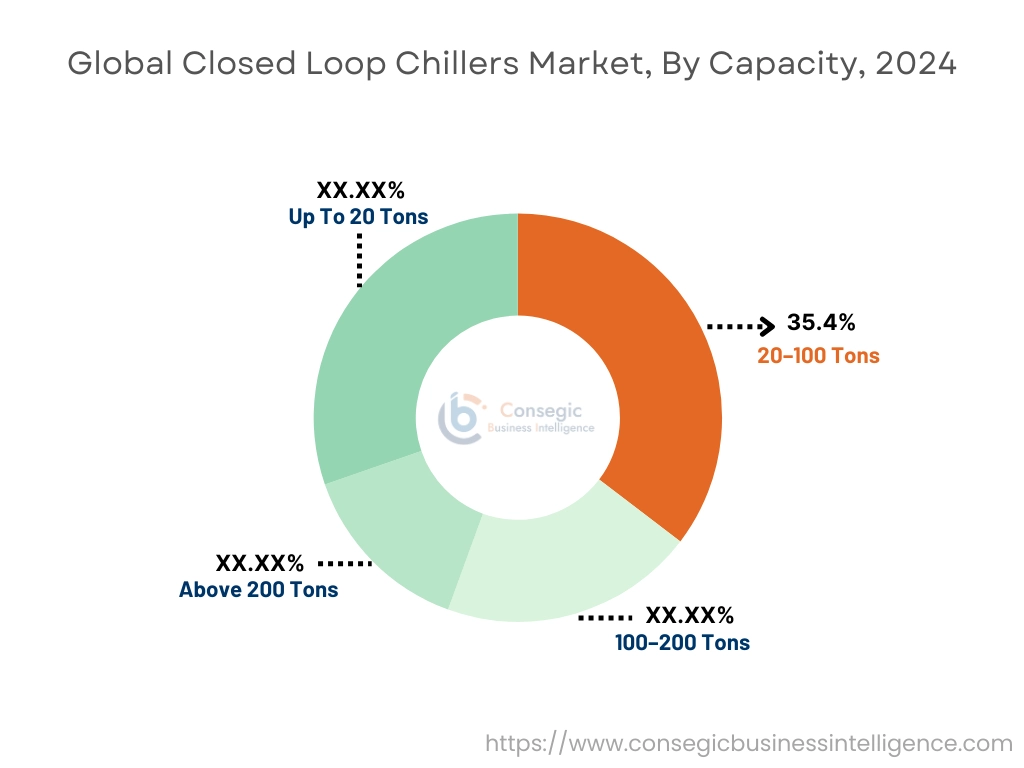

By Capacity:

Based on capacity, the market is segmented into up to 20 tons, 20–100 tons, 100–200 tons, and above 200 tons.

The 20–100 tons segment dominated with a market share of 35.4% in 2024.

- This capacity range is widely suited for mid-size facilities like commercial buildings, research laboratories, and healthcare centers.

- These systems offer balanced performance between energy efficiency and output capacity, aligning with operational budgets.

- Their adaptability to scalable designs and modular configurations increases their appeal for retrofits and system upgrades.

- According to closed loop chillers market analysis, mid-capacity systems remain a strong choice for versatile and cost-effective cooling.

The above 200 tons segment is projected to register the fastest CAGR.

- This category serves heavy-duty industrial facilities, data centers, and utility plants requiring high-capacity, 24/7 cooling.

- Rising infrastructure development in emerging markets and industrial zones boosts demand for centralized large-scale chillers.

- These systems are often integrated with advanced controls and variable-speed drives, enabling efficient operation in energy-intensive environments.

- The closed loop chillers market demand is driven by investments in high-throughput manufacturing and power-intensive operations.

By End Use:

Based on end-use, the market is segmented into industrial manufacturing, food & beverage, pharmaceuticals & biotechnology, chemicals, plastics & rubber, energy & power, metal processing, aerospace & defense, data centers, and others.

The industrial manufacturing segment held the largest closed loop chillers market share in 2024.

- Continuous production lines in metal fabrication, plastic molding, and electronics require reliable and efficient cooling to maintain process integrity.

- They are preferred due to their consistent performance and minimal water consumption compared to open-loop systems.

- The need for automation and precision in industrial operations has further increased reliance on stable thermal management systems.

- Industrial manufacturers prioritizing durability, control, and low operating costs have bolstered the closed loop chillers market expansion.

The data centers segment is expected to witness the fastest CAGR.

- Growing global demand for cloud storage, AI computing, and 5G infrastructure has significantly increased thermal loads in server rooms.

- Models with redundant configurations ensure uninterrupted cooling in high-density server environments.

- Their capacity for integration with smart controls and remote monitoring platforms makes them ideal for modern IT infrastructure.

- For instance, in August 2024, Microsoft launched a next-generation datacenter design that optimizes AI workloads and consumes zero water for cooling. This closed loop recycling system circulates water between the servers and chillers, eliminating the need for a freshwater supply. The design utilizes chip-level cooling solutions to optimize temperature control without relying on water evaporation.

- Energy-efficient cooling to lower data center operating costs and carbon footprint is driving the closed loop chillers market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

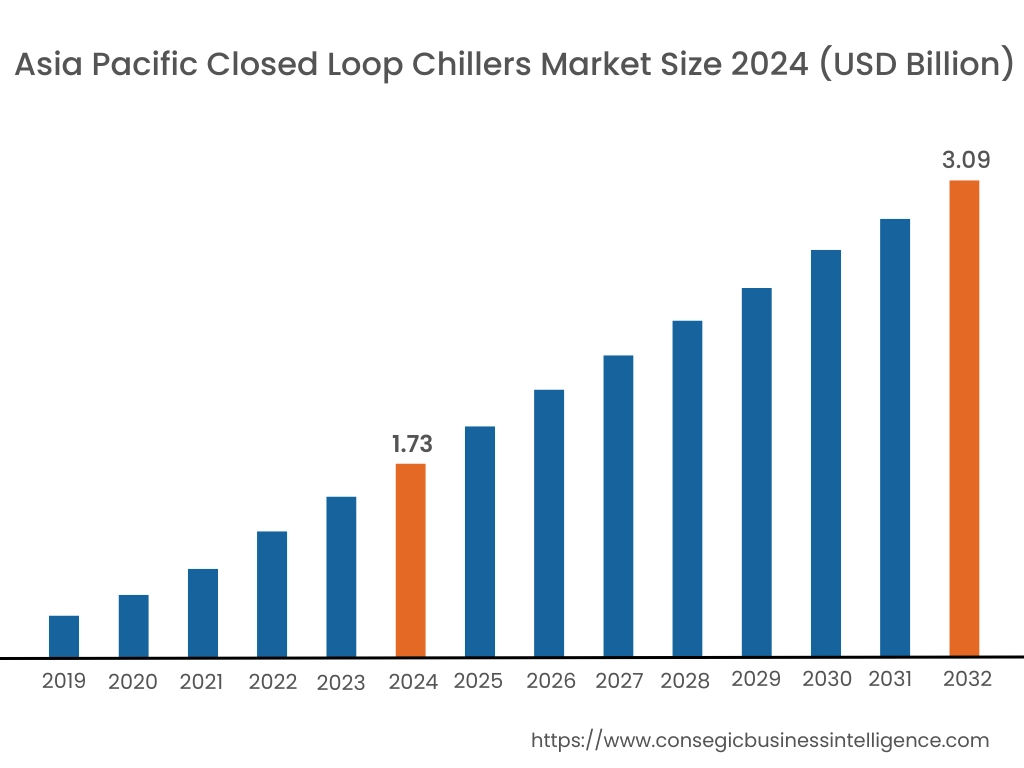

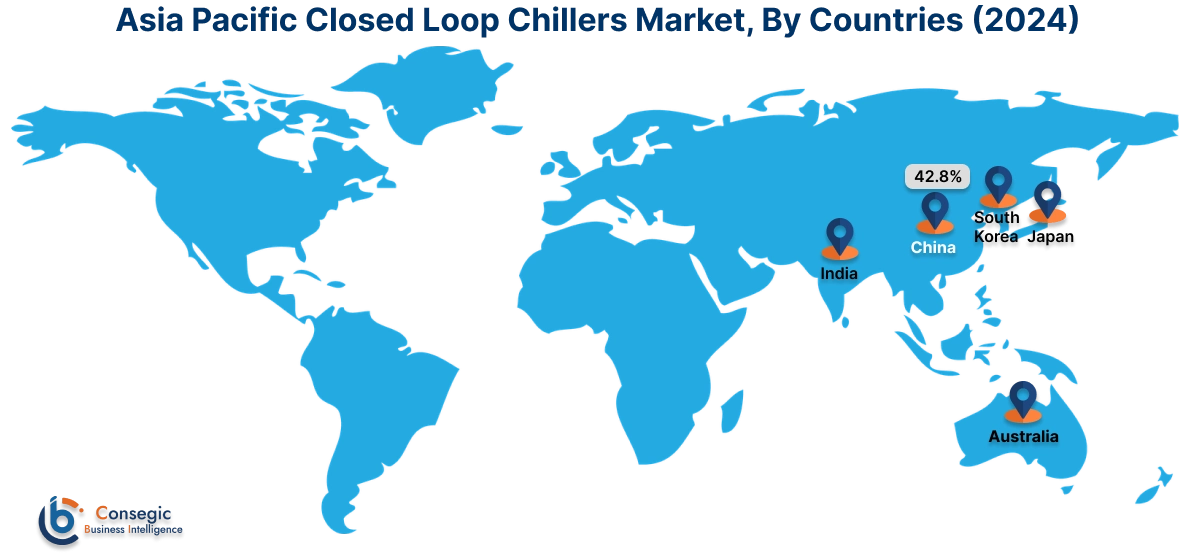

Asia Pacific region was valued at USD 1.73 Billion in 2024. Moreover, it is projected to grow by USD 1.83 Billion in 2025 and reach over USD 3.09 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. Asia-Pacific is witnessing rapid expansion in the closed loop chillers industry due to aggressive industrial growth, infrastructure upgradation, and increasing sensitivity towards operational effectiveness. In nations like China, India, South Korea, and Japan, demand is growing in electronics manufacturing, plastic molding, and food processing industries where reliability and temperature control are critical. Regional analysis shows that cost competitiveness and energy consumption regulations are driving companies to implement compact, high-efficiency closed loop systems. Besides, government-backed industrial modernizations and smart factory programs are helping drive the deployment of digitally equipped and remote-monitoring chillers, which are providing positive preconditions for sustained growth.

North America is estimated to reach over USD 2.71 Billion by 2032 from a value of USD 1.53 Billion in 2024 and is projected to grow by USD 1.61 Billion in 2025. The region boasts a well-placed market, with extensive use of closed loop chillers in manufacturing, food processing, and laboratory applications. The United States and Canada increasingly favor energy-efficient, low-maintenance systems with accurate temperature control. Market research indicates that the drive towards decarbonization and sustainability in industrial processes is leading to the replacement of conventional open-loop systems with more environmentally controlled systems. Adoption of closed loop systems is especially high in sectors that need to maintain contamination-free operations, like pharmaceuticals and semiconductor manufacturing. Furthermore, intelligent integration with building automation and prognostics-based maintenance platforms is becoming a key differentiator in the region.

Europe has a highly sophisticated and environmentally-conscious market for closed loop cooling systems. Germany, Italy, and France are incorporating closed loop chillers in energy-consuming industries like chemical production, printing, and data center operations. In-depth analysis indicates that EU water conservation and industrial emissions directives are key drivers of higher water-saving and self-contained cooling technology adoption. In addition, the shift towards industrial electrification and climate-neutral manufacturing processes has facilitated the move towards closed systems that minimize waste and enhance energy efficiency. Technological advancement and modularity of systems are also promoting wider use in smaller industrial establishments.

Latin America is evidencing slow but steady adoption, with market pickup in Brazil, Mexico, and Chile. It is witnessing accelerated installation of closed loop chillers in beverage manufacturing, pharmaceutical, and agriculture processing plants. Analysis indicates that even though conventional cooling systems remain popular, interest is increasingly shifting toward self-contained equipment that uses minimal water and reduces operating costs. The trend towards local production, combined with reducing equipment downtime, is driving increasing interest in more efficient cooling facilities. The closed loop chillers market opportunity in this area lies in replacing old systems with retrofitting and educating end-users about lifecycle efficiency advantages.

In the Middle East and African region, there is increasing demand for closed loop chillers in response to diversification in the industrial sector as well as infrastructural development across countries like the UAE, Saudi Arabia, and South Africa. Increasing ambient temperatures and the need for reliable cooling systems in oil & gas, desalination, and data management are propelling adoption. Based on regional analysis, focus on water saving and sustainability is slowly changing preferences in favor of closed loop designs. But adoption continues to remain small in certain regions due to increased initial investment and low awareness. Opening local service networks and proving long-term cost savings in operation are essential in order to expand penetration within this market.

Top Key Players & Market Share Insights:

The closed loop chillers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global closed loop chillers market. Key players in the closed loop chillers industry include –

- Daikin Industries Ltd. (Japan)

- Trane Technologies plc (Ireland)

- Gree Electric Appliances Inc. (China)

- Midea Group Co., Ltd. (China)

- LG Electronics Inc. (South Korea)

- Mitsubishi Electric Corporation (Japan)

- Johnson Controls International plc (Ireland)

- Smardt Chiller Group Inc. (Canada)

- Dimplex Thermal Solutions (Germany)

- Thermax Limited (India)

Recent Industry Developments :

Acquisitions:

- In May 2023, Trane Technologies acquired MTA, an Italian-based manufacturer and distributor of sustainable solutions in industrial process cooling. This move enabled Trane to expand its product portfolio with chillers purpose-built for industrial process cooling, offering different cooling capacities that meet the specialized needs of pharmaceutical, food and beverage, automotive and general manufacturers.

Closed Loop Chillers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 9.18 Billion |

| CAGR (2025-2032) | 7.4% |

| By Product Type |

|

| By Refrigerant Type |

|

| By Capacity |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Closed Loop Chillers Market? +

Closed Loop Chillers Market size is estimated to reach over USD 9.18 Billion by 2032 from a value of USD 5.20 Billion in 2024 and is projected to grow by USD 5.49 Billion in 2025, growing at a CAGR of 7.4% from 2025 to 2032.

What specific segmentation details are covered in the Closed Loop Chillers Market report? +

The Closed Loop Chillers market report includes specific segmentation details for product type, refrigerant type, capacity and end-use.

What are the end-use of the Closed Loop Chillers Market? +

The end-use of the Closed Loop Chillers Market are industrial manufacturing, food & beverage, pharmaceuticals & biotechnology, chemicals, plastics & rubber, energy & power, metal processing, aerospace & defense, data centers and others (printing, textile, etc.).

Who are the major players in the Closed Loop Chillers Market? +

The key participants in the Closed Loop Chillers market are Daikin Industries Ltd. (Japan), Trane Technologies plc (Ireland), Mitsubishi Electric Corporation (Japan), Johnson Controls International plc (Ireland), Smardt Chiller Group Inc. (Canada), Dimplex Thermal Solutions (Germany), Thermax Limited (India), Gree Electric Appliances Inc. (China), Midea Group Co., Ltd. (China), LG Electronics Inc. (South Korea).