- Summary

- Table Of Content

- Methodology

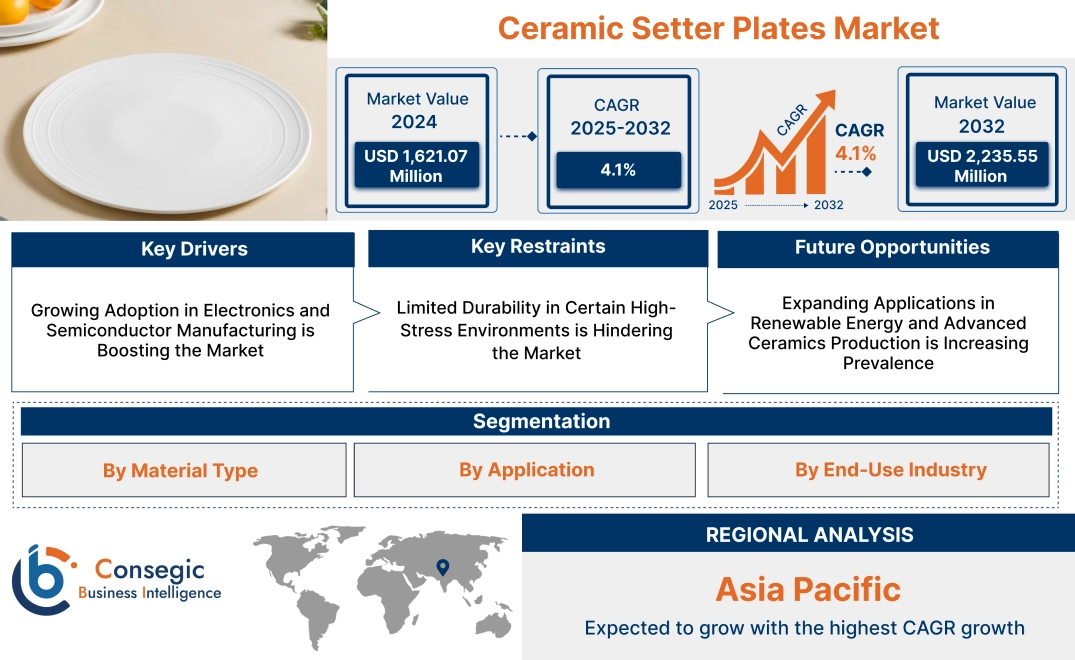

Ceramic Setter Plates Market Size:

Ceramic Setter Plates Market size is estimated to reach over USD 2,235.55 Million by 2032 from a value of USD 1,621.07 Million in 2024 and is projected to grow by USD 1,658.65 Million in 2025, growing at a CAGR of 4.1% from 2025 to 2032.

Ceramic Setter Plates Market Scope & Overview:

The ceramic setter plates are materials used as supports or bases during the high-temperature processing of ceramics and other materials. Setter plates are engineered for applications in kilns and furnaces, where they provide stability, uniform heat distribution, and resistance to thermal shock. These plates are integral in manufacturing technical ceramics, tiles, and electronic components, ensuring dimensional accuracy and product quality. Key characteristics of ceramic setter plates include high mechanical strength, thermal stability, and resistance to wear and chemical corrosion. The benefits include improved product consistency, extended service life of kiln furniture, and reduced energy consumption in high-temperature operations. Applications span ceramics production, metallurgy, and electronics manufacturing, where precision and durability are essential. End-users include ceramics manufacturers, electronic component producers, and metal processing industries, driven by increasing demand for advanced ceramics, growth in electronics manufacturing, and advancements in thermal processing technologies.

Ceramic Setter Plates Market Dynamics - (DRO) :

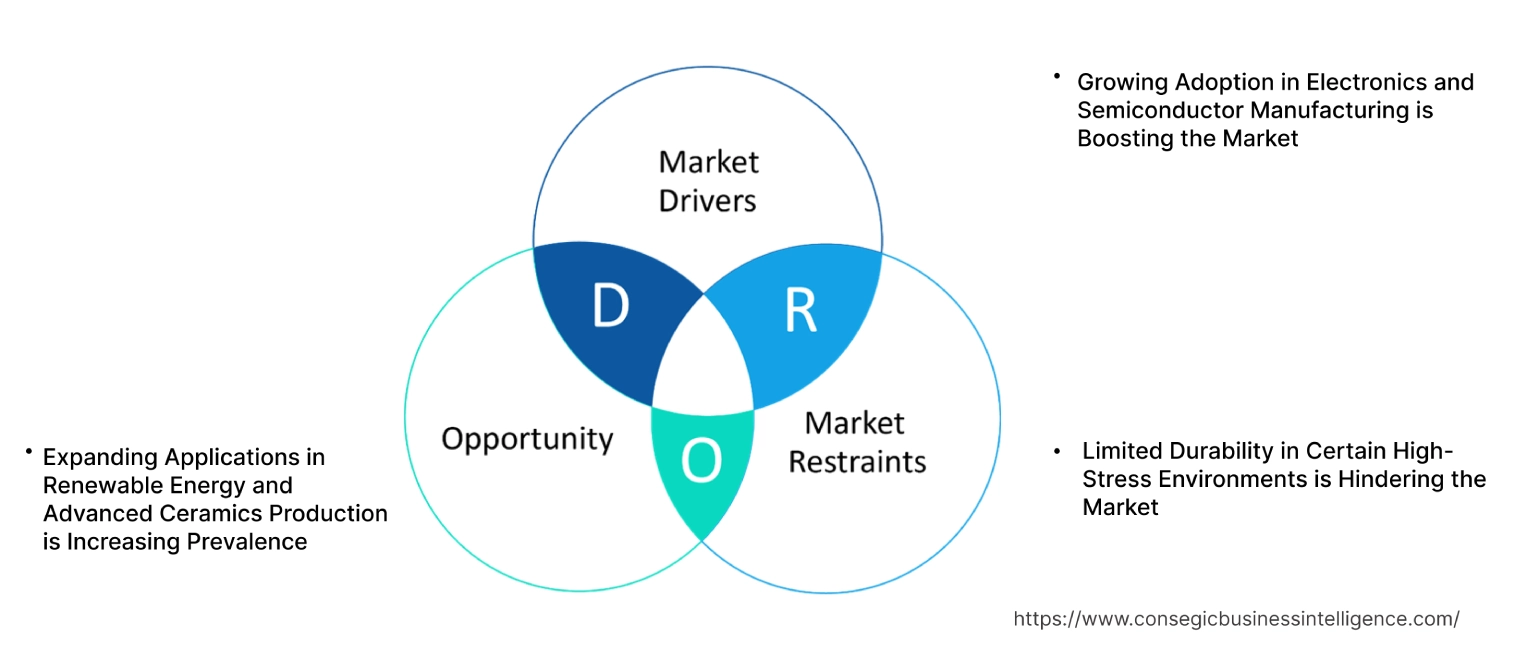

Key Drivers:

Growing Adoption in Electronics and Semiconductor Manufacturing is Boosting the Market

Ceramic setter plates have become essential in the electronics and semiconductor industries, where precise thermal management and stability are critical for high-temperature processes. These plates provide consistent support during the sintering and firing of materials, ensuring that components like semiconductors, capacitors, and microchips meet the stringent performance and quality standards required by modern electronics. Their superior thermal stability and chemical resistance make them indispensable in processes that involve high heat and aggressive chemical environments.

Trends in semiconductor miniaturization and advanced electronic device manufacturing are driving the integration of ceramic setter plates into production lines. As industries strive for precision and reliability, ceramic setter plates offer a solution that enhances the consistency and efficiency of production processes. Analysis highlights their role in supporting cutting-edge technologies in consumer electronics, telecommunications, and industrial automation.

Key Restraints:

Limited Durability in Certain High-Stress Environments is Hindering the Market

While ceramic setter plates excel in thermal and chemical resistance, their performance can be compromised in high-stress applications involving rapid thermal cycling, mechanical impacts, or prolonged exposure to extreme conditions. Such environments can lead to micro-cracking, wear, or degradation of the plates, reducing their operational lifespan and necessitating frequent replacements.

This limitation poses challenges for industries that require long-term durability and consistent performance under intense operational conditions, such as aerospace or heavy industrial applications. Trends in developing advanced materials with enhanced durability are essential to address these challenges and expand the usability of ceramic setter plates across diverse sectors.

Future Opportunities :

Expanding Applications in Renewable Energy and Advanced Ceramics Production is Increasing Prevalence

The renewable energy sector is increasingly incorporating ceramic setter plates into the production of advanced ceramics used in solar panels, fuel cells, and energy storage systems. These plates ensure precision and stability during the manufacturing of ceramic components that play a vital role in clean energy technologies. Their ability to withstand high temperatures and harsh conditions makes them ideal for enabling efficient production processes in this growing industry.

Trends in clean energy adoption and advanced ceramics innovation present significant adaption for the ceramic setter plates market opportunities. Analysis suggests that the development of customized plates for specific renewable energy applications, such as solar cell substrates or electrolytic cell components, can drive further drives ceramic setter plates market expansion. Manufacturers focusing on sustainability and performance optimization are well-positioned to capitalize on these emerging opportunities.

Ceramic Setter Plates Market Segmental Analysis :

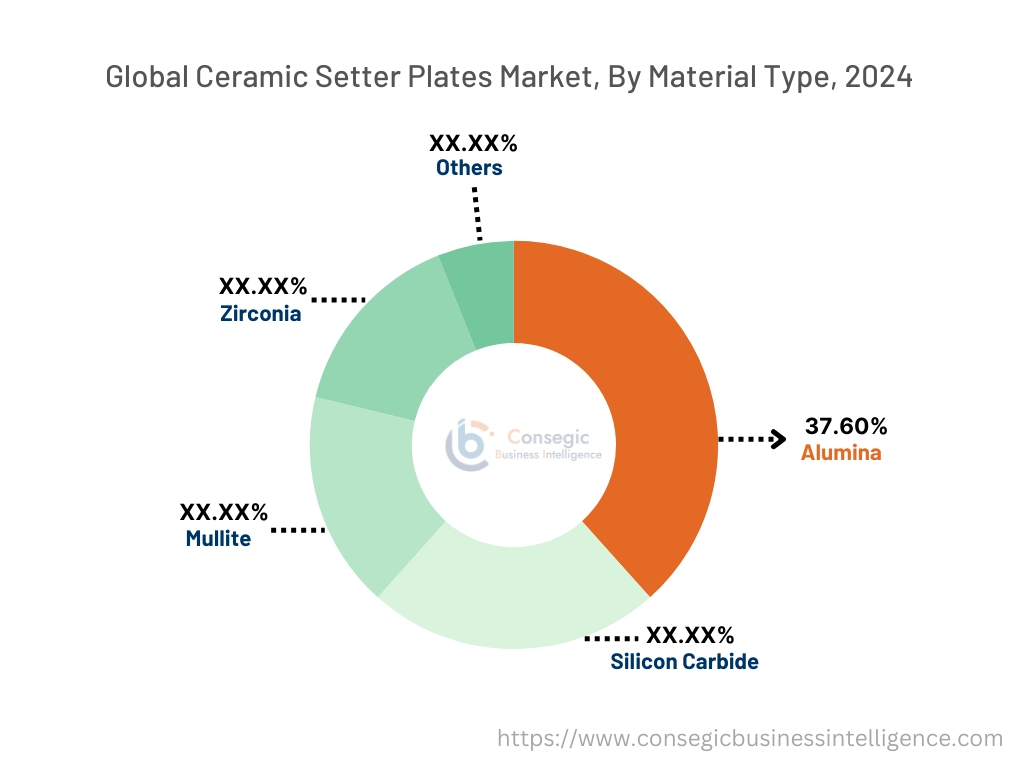

By Material Type:

Based on material type, the refractory setter plates market is segmented into alumina, silicon carbide, mullite, zirconia, and others.

The alumina segment accounted for the largest revenue of 37.60% of ceramic setter plates market share in 2024.

- Alumina-based refractory setter plates are widely used due to their high thermal stability, mechanical strength, and resistance to corrosion.

- These plates are extensively applied in heat treatment processes, kiln furniture, and firing ceramic components in industries such as electronics and automotive.

- Their ability to withstand extreme temperatures and harsh environments makes alumina plates a preferred choice for high-performance applications. T

- The increasing ceramic setter plates market trends for alumina plates in industrial manufacturing and sintering processes, coupled with advancements in material technology, have driven the dominance of this segment.

The silicon carbide segment is anticipated to register the fastest CAGR during the forecast period.

- Silicon carbide setter plates are gaining traction due to their exceptional thermal conductivity, low thermal expansion, and superior wear resistance.

- These properties make them ideal for applications in high-temperature sintering, heat treatment, and firing processes.

- The growing trends for lightweight and durable materials in aerospace and automotive industries have boosted the adoption of silicon carbide setter plates.

- Additionally, advancements in manufacturing techniques for silicon carbide plates are expected to propel the segment’s growth further.

By Application:

Based on application, the refractory setter plates market is segmented into firing of ceramic components, heat treatment processes, sintering of powdered metals, kiln furniture, and others.

The firing of ceramic components segment accounted for the largest revenue of ceramic setter plates market share in 2024.

- Refractory setter plates are critical in firing ceramic components, ensuring uniform heating and structural integrity.

- These plates are extensively used in the production of advanced ceramics for electronics, automotive, and aerospace applications.

- The increasing trends for ceramic components in semiconductors, insulators, and wear-resistant parts have driven the adoption of setter plates in this application.

- Furthermore, the focus on improving the quality and efficiency of ceramic production processes has bolstered the growth of this segment.

The sintering of the powdered metals segment is anticipated to register the fastest CAGR during the forecast period.

- Setter plates are essential in sintering processes for powdered metals, providing stability and consistency during high-temperature operations.

- These plates are widely used in the production of metal components for industrial machinery, automotive, and aerospace applications.

- The growing adoption of sintered metals in lightweight and high-strength components, coupled with the ceramic setter plates market expansion of additive manufacturing (3D printing), is driving the trends for setter plates in this segment.

- Additionally, advancements in sintering technologies and materials are expected to further accelerate development.

By End-User Industry:

Based on the end-use industry, the refractory setter plates market is segmented into electronics, automotive, aerospace, industrial manufacturing, healthcare, and others.

The electronics segment accounted for the largest revenue share in 2024.

- The electronics sector is a major consumer of refractory setter plates, driven by the ceramic setter plates market trends for advanced ceramics and components used in semiconductors, sensors, and insulators.

- Setter plates play a crucial role in the production of high-performance electronic components, ensuring precision and quality during firing and sintering processes.

- The increasing adoption of electronics in consumer devices, automotive applications, and industrial systems has fueled the demand for setter plates in this segment.

- Additionally, advancements in ceramic materials and microelectronics are further driving growth in the electronics sector.

The aerospace segment is anticipated to register the fastest CAGR during the forecast period.

- Refractory setter plates are extensively used in the aerospace sectors for the production of lightweight and high-temperature-resistant components.

- These plates are critical in sintering processes for advanced ceramics and powdered metals, which are used in turbine blades, engine components, and structural parts.

- The growing focus on fuel efficiency, weight reduction, and material durability in aerospace applications is driving the adoption of setter plates.

- Additionally, increased investments in aerospace manufacturing and the rising production of commercial and defense aircraft are expected to propel the segment’s growth significantly.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

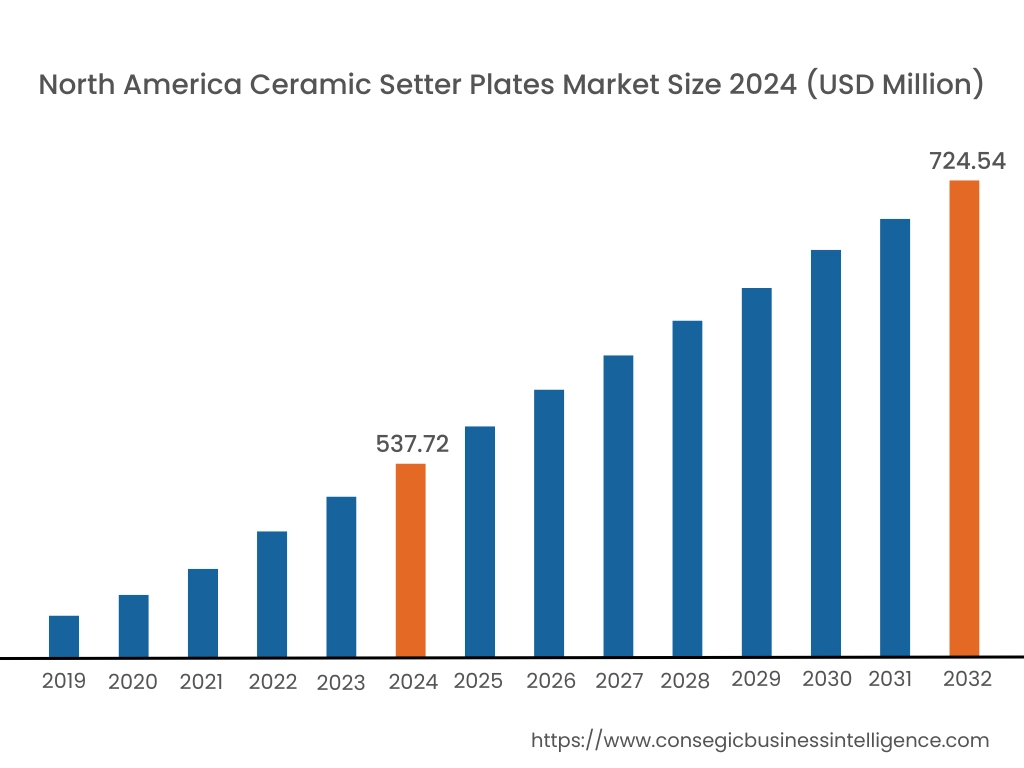

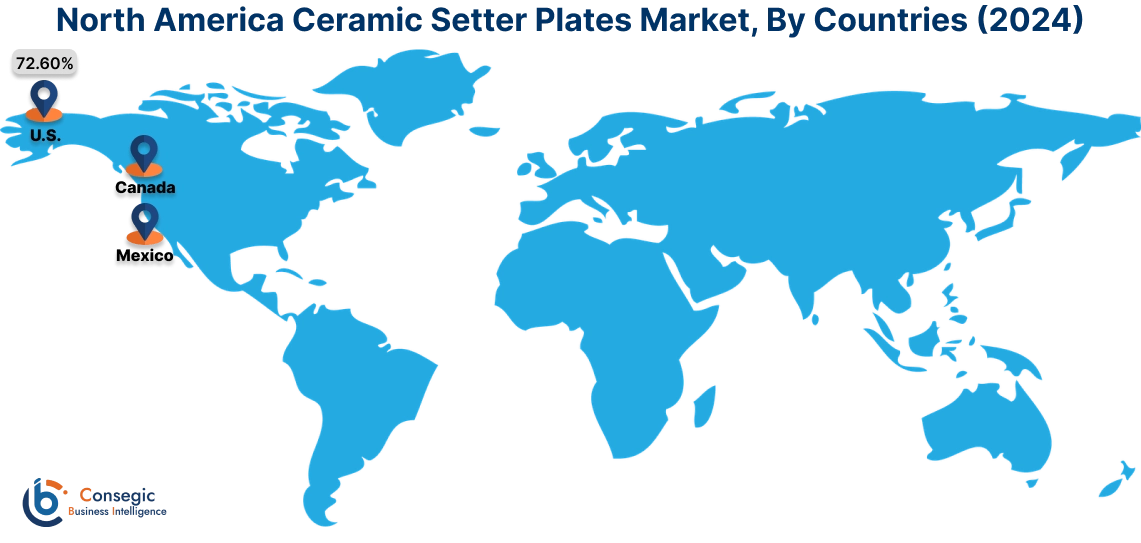

In 2024, North America was valued at USD 537.72 Million and is expected to reach USD 724.54 Million in 2032. In North America, the U.S. accounted for the highest share of 72.60% during the base year of 2024. North America holds a significant share in the ceramic setter plates market analysis, driven by advancements in the aerospace, electronics, and industrial manufacturing sectors. The U.S. leads the region, with strong demand for ceramic plates in high-temperature applications such as sintering and firing processes in electronics and aerospace component manufacturing. The growing adoption of additive manufacturing technologies also supports the use of setter plates for precise and high-quality ceramic parts. Canada contributes with increasing utilization in metalworking and advanced ceramics production. However, the high cost of advanced ceramic materials may pose challenges to widespread adoption.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.5% over the forecast period. In the ceramic setter plates market analysis, fueled by rapid industrialization, urbanization, and increasing demand for high-performance ceramics in China, India, and Japan. China dominates the market with extensive use of setter plates in advanced ceramics production for electronics, automotive, and industrial applications. India’s growing infrastructure and industrial sectors support the adoption of setter plates in metalworking and refractory applications. Japan emphasizes high-precision applications in electronics and healthcare, leveraging setter plates for consistent quality in ceramic components. However, fluctuating raw material prices and limited domestic production capabilities in emerging markets may hinder ceramic setter plate market opportunities.

Europe is a prominent market for ceramic setter plates, supported by its advanced industrial base and focus on high-performance materials. As per the analysis, countries like Germany, France, and the UK are key contributors. Germany’s strong ceramics and automotive industries drive the adoption of setter plates in sintering processes for high-performance components. France emphasizes their use in aerospace applications, particularly for high-temperature-resistant materials, while the UK focuses on precision ceramics for medical and electronic components. However, stringent EU regulations on material safety and recycling may create challenges for manufacturers.

The Middle East & Africa region is witnessing steady growth in the ceramic setter plates market, driven by increasing investments in industrial manufacturing and energy sectors. Countries like Saudi Arabia and the UAE are adopting setter plates for use in high-temperature applications such as ceramics manufacturing and petrochemical industries. In Africa, South Africa analysis is portraying it as an emerging market, utilizing ceramic setter plates in mining and industrial processes where durability and heat resistance are critical. However, limited local production capabilities and reliance on imports may restrict broader market development in the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s growing industrial base, particularly in ceramics and metalworking, drives ceramic setter plates market demand for setter plates in sintering and high-temperature firing applications. The regional analysis of Mexico focuses on their use in electronics manufacturing and automotive component production to enhance quality and efficiency. The region is also exploring the use of advanced ceramics in energy and infrastructure projects. However, economic instability and lack of advanced manufacturing infrastructure may pose challenges to market expansion in smaller economies.

Top Key Players and Market Share Insights:

The ceramic setter plates market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the ceramic setter plates market. Key players in the ceramic setter plates industry include -

- Kerafol (Germany)

- CeramTec (Germany)

- Bailey Ceramic (USA)

- Saint-Gobain (France)

- KYOCERA Corporation (Japan)

- Applied Ceramics (USA)

- Anderman Industrial Ceramics (UK)

- IPS Ceramics (UK)

- Tuckers Pottery (USA)

- Unipretec (China)

Recent Industry Developments :

Product Launches:

- In October 2024, CeramTec GmbH, based in Marktredwitz, Germany, developed advanced Al₂O₃ (alumina) and AlN (aluminum nitride) setter plates and sintering trays designed to enhance the sintering process for Ceramic Injection Moulded (CIM) and Metal Injection Moulded (MIM) components. The advanced ceramic materials prevent reactions with metals, removing the need for release agents or protective coatings, thereby streamlining the production process and reducing contamination risks.

Ceramic Setter Plates Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,235.55 Million |

| CAGR (2025-2032) | 4.1% |

| By Material Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size for Ceramic Setter Plates by 2032? +

Ceramic Setter Plates Market size is estimated to reach over USD 2,235.55 Million by 2032 from a value of USD 1,621.07 Million in 2024 and is projected to grow by USD 1,658.65 Million in 2025, growing at a CAGR of 4.1% from 2025 to 2032.

What are the key drivers for the Ceramic Setter Plates Market? +

The increasing demand for advanced ceramics in industrial manufacturing, electronics, and automotive applications, along with rising adoption in the aerospace and healthcare sectors, are key drivers for the market.

What challenges are impacting the market growth? +

High production costs and the complexity of manufacturing processes for advanced ceramic materials pose challenges to market growth.

What opportunities are shaping the future of this market? +

The development of lightweight, high-strength ceramics for aerospace and renewable energy applications presents significant growth opportunities for market players.