- Summary

- Table Of Content

- Methodology

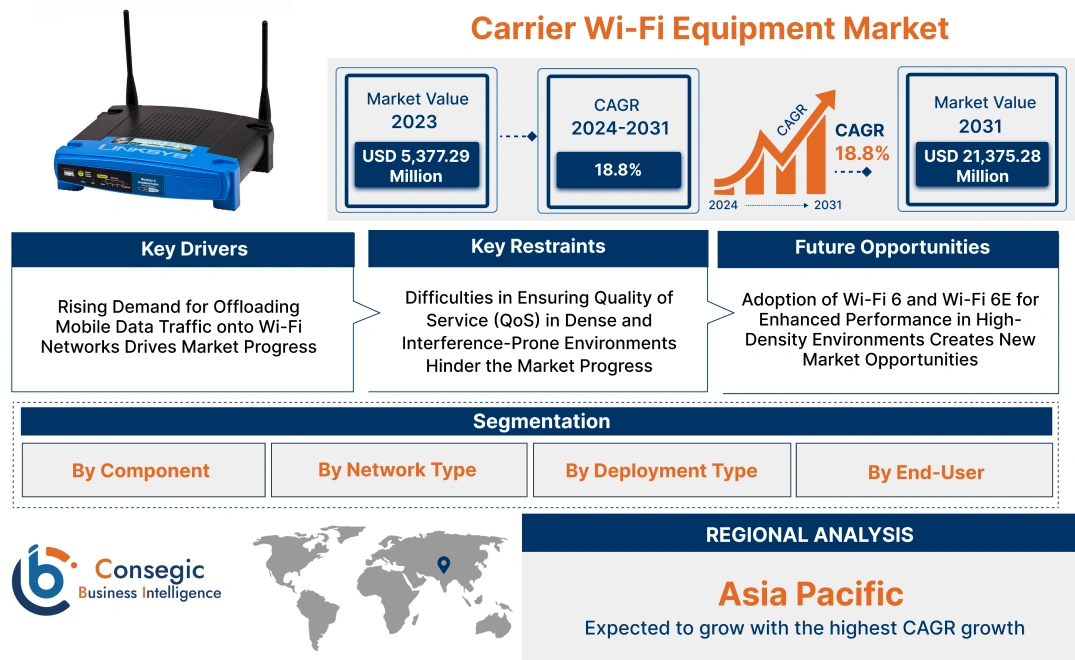

Carrier Wi-Fi Equipment Market Size:

Carrier Wi-Fi Equipment Market size is estimated to reach over USD 21,375.28 Million by 2031 from a value of USD 5,377.29 Million in 2023 and is projected to grow by USD 6,293.90 Million in 2024, growing at a CAGR of 18.8% from 2024 to 2031.

Carrier Wi-Fi Equipment Market Scope & Overview:

Carrier Wi-Fi equipment refers to the network infrastructure used by telecommunications service providers to deliver high-speed, reliable wireless internet access to end-users. This equipment includes access points, wireless controllers, gateways, and network management tools specifically designed for large-scale deployments, ensuring robust connectivity and seamless user experiences. Carrier Wi-Fi solutions are typically integrated with mobile networks to offload traffic, enhance network capacity, and provide efficient data services in high-density environments like public venues, transportation hubs, and urban areas. Key end-users of Carrier Wi-Fi equipment include telecommunications operators, internet service providers (ISPs), enterprises, and public sector organizations.

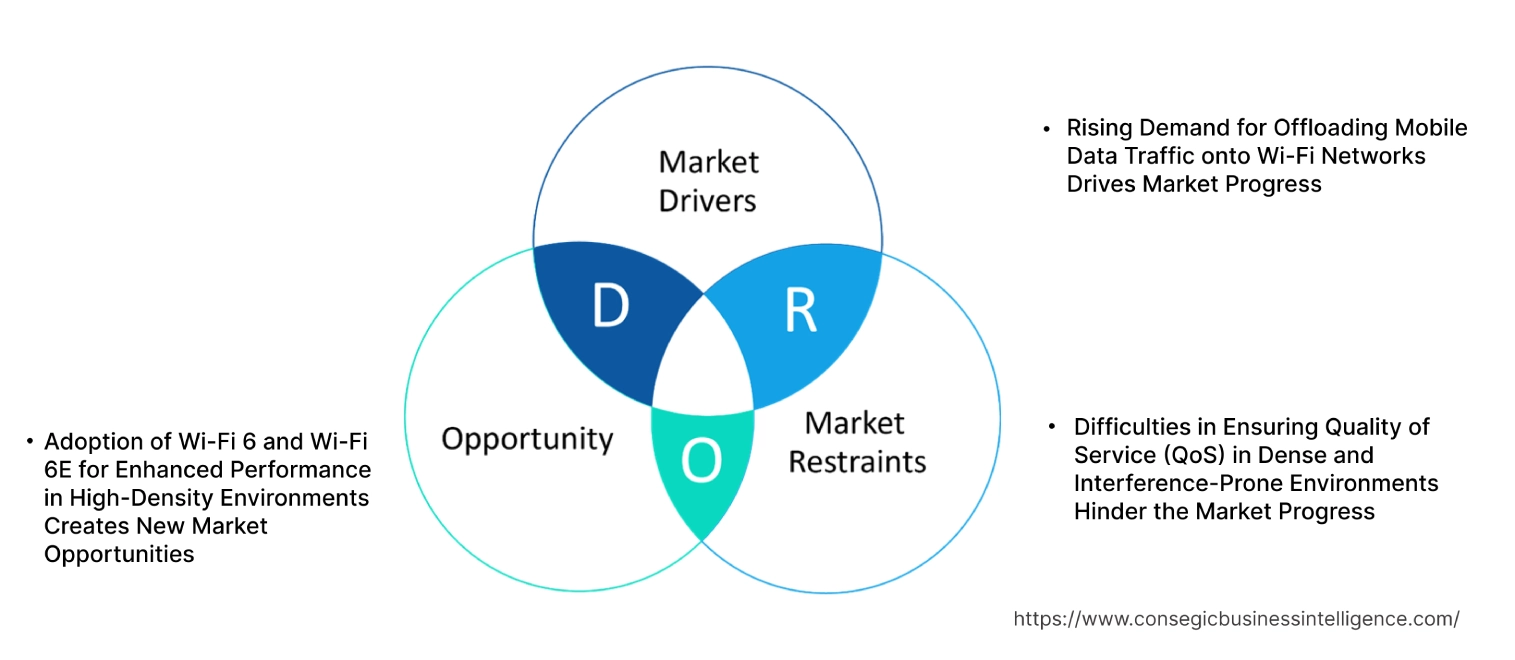

Carrier Wi-Fi Equipment Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Offloading Mobile Data Traffic onto Wi-Fi Networks Drives Market Progress

The increasing need for mobile data offloading is a significant driver of the carrier Wi-Fi equipment market. With the exponential gain in mobile data traffic, driven by the proliferation of video streaming, social media, and cloud-based applications, mobile network operators (MNOs) face challenges in managing network congestion. Carrier Wi-Fi offers a robust solution by enabling MNOs to offload excess data traffic from cellular networks onto Wi-Fi networks, thereby improving network efficiency and enhancing user experiences. Unlike traditional Wi-Fi, carrier-grade Wi-Fi provides seamless integration with cellular networks, supporting features like SIM-based authentication and quality of service (QoS) management. This capability allows operators to maintain high service quality even during peak usage times, making carrier Wi-Fi a critical component in network capacity planning, particularly in urban areas and high-density environments. Therefore, the surge in offloading onto Wi-Fi networks boosts the carrier wi-fi equipment market demand.

Key Restraints :

Difficulties in Ensuring Quality of Service (QoS) in Dense and Interference-Prone Environments Hinder the Market Progress

Ensuring a consistent Quality of Service (QoS) in dense, interference-prone environments is a significant constraint for the carrier Wi-Fi equipment market. Public Wi-Fi deployments often occur in areas with high user density, such as stadiums, shopping malls, and transportation hubs, where the risk of signal interference is elevated due to the presence of numerous overlapping Wi-Fi networks and other wireless signals. Maintaining a stable, high-quality connection in these scenarios requires advanced interference management techniques, such as dynamic channel selection and spectrum analysis, which is difficult and costly to implement effectively. Additionally, managing congestion and bandwidth allocation among a large number of simultaneous users without compromising service quality is a complex task. The inability to guarantee a high level of QoS in congested areas leads to poor user experiences, negatively impacting the reputation of service providers and limiting the adoption of carrier-grade Wi-Fi solutions. The aforementioned factors hampers the carrier wi-fi equipment market growth.

Future Opportunities :

Adoption of Wi-Fi 6 and Wi-Fi 6E for Enhanced Performance in High-Density Environments Creates New Market Opportunities

The adoption of Wi-Fi 6 and Wi-Fi 6E technologies presents a significant growth opportunity for the carrier Wi-Fi equipment market. Wi-Fi 6 introduces several enhancements, including higher data rates, improved efficiency, and better performance in congested environments, making it ideal for high-density applications like stadiums, convention centers, and urban hotspots. Wi-Fi 6E extends these capabilities into the 6 GHz spectrum, providing additional channels that offer lower interference and greater capacity. These advancements are particularly beneficial for service providers aiming to deliver superior quality of service (QoS) and seamless connectivity in locations with high user densities. By deploying Wi-Fi 6 and Wi-Fi 6E equipment, carriers will offer faster, more reliable connections and support new use cases, such as augmented reality (AR) and virtual reality (VR) applications, which require low-latency, high-bandwidth networks. The shift towards these next-generation Wi-Fi standards is expected to drive substantial investment in carrier-grade Wi-Fi infrastructure further creating carrier wi-fi equipment market opportunities.

Carrier Wi-Fi Equipment Market Segmental Analysis :

By Component:

Based on component, the Carrier Wi-Fi Equipment market is segmented into access points, controllers, gateways, software, and others.

The access points segment accounted for the largest revenue of the total carrier wi-fi equipment market share in 2023.

- Access points are critical components of carrier Wi-Fi networks, providing connectivity to end-user devices and enabling seamless wireless access.

- The rising requirement for high-speed, reliable Wi-Fi coverage in public and private networks drives the widespread adoption of advanced access points.

- The growing trend of Wi-Fi 6 and Wi-Fi 6E access points, with enhanced capabilities such as improved throughput and reduced latency, is contributing to this segment's dominance.

- Access points offer scalability and flexibility, making them suitable for various environments, from dense urban areas to rural deployments.

- The access points segment leads the market due to the increasing deployment of high-performance Wi-Fi solutions in both consumer and enterprise applications.

- As per carrier wi-fi equipment market analysis, the access points segment boosts the market progress.

The software segment is anticipated to register the fastest CAGR during the forecast period.

-

- Software solutions play a crucial role in managing and optimizing carrier Wi-Fi networks, offering capabilities such as network analytics, traffic management, and user authentication.

- The shift towards cloud-based network management and the integration of AI-driven analytics tools are driving the development of the software segment.

- Advanced software platforms enable service providers to monitor network performance in real-time, ensuring optimal user experience and efficient resource allocation.

- The increasing adoption of software-defined networking (SDN) and network functions virtualization (NFV) is further enhancing the capabilities of Wi-Fi management software.

- The software segment is expected to grow rapidly, driven by the rising need for intelligent, cloud-based network management solutions.

- As per carrier wi-fi equipment market trends, the software segment boosts the market progress.

By Network Type:

Based on network type, the market is segmented into 3G & 4G LTE, 5G, public Wi-Fi, and private Wi-Fi.

The public Wi-Fi segment accounted for the largest revenue share in 2023.

- Public Wi-Fi networks are widely deployed in high-traffic areas such as airports, shopping malls, stadiums, and city centers, providing internet access to large numbers of users.

- The increasing consumer need for free, high-speed internet access in public spaces is driving the expansion of public Wi-Fi networks by telecom operators and ISPs.

- The rise of smart city initiatives and the growing need for urban connectivity are further propelling the deployment of public Wi-Fi networks.

- Public Wi-Fi networks offer benefits such as enhanced customer engagement and the ability to gather valuable user data, supporting the strong growth of this segment.

- The public Wi-Fi segment leads the market due to its extensive deployment in high-traffic locations and the increasing focus on providing reliable, high-speed internet access in public areas.

- Therefore, as per segmental trends analysis, public Wi-Fi segment drives the carrier wi-fi equipment market expansion.

The 5G segment is anticipated to register the fastest CAGR during the forecast period.

- The integration of 5G with Wi-Fi networks is transforming the capabilities of carrier Wi-Fi equipment, enabling faster speeds, lower latency, and enhanced user experiences.

- The roll-out of 5G networks by telecom operators is driving the adoption of advanced Wi-Fi solutions that complement 5G services, particularly in urban and dense environments.

- 5G-enabled Wi-Fi offers seamless connectivity for applications like video streaming, online gaming, and virtual reality (VR), meeting the requirement for high-performance wireless networks.

- The increasing adoption of Wi-Fi 6 and Wi-Fi 6E technologies, designed to work efficiently with 5G networks, is further boosting progress in this segment.

- The 5G segment is expected to grow rapidly due to the ongoing roll-out of 5G infrastructure and the demand for integrated, high-performance wireless solutions.

- As per segmental trends analysis, the 5G segment boosts the market development.

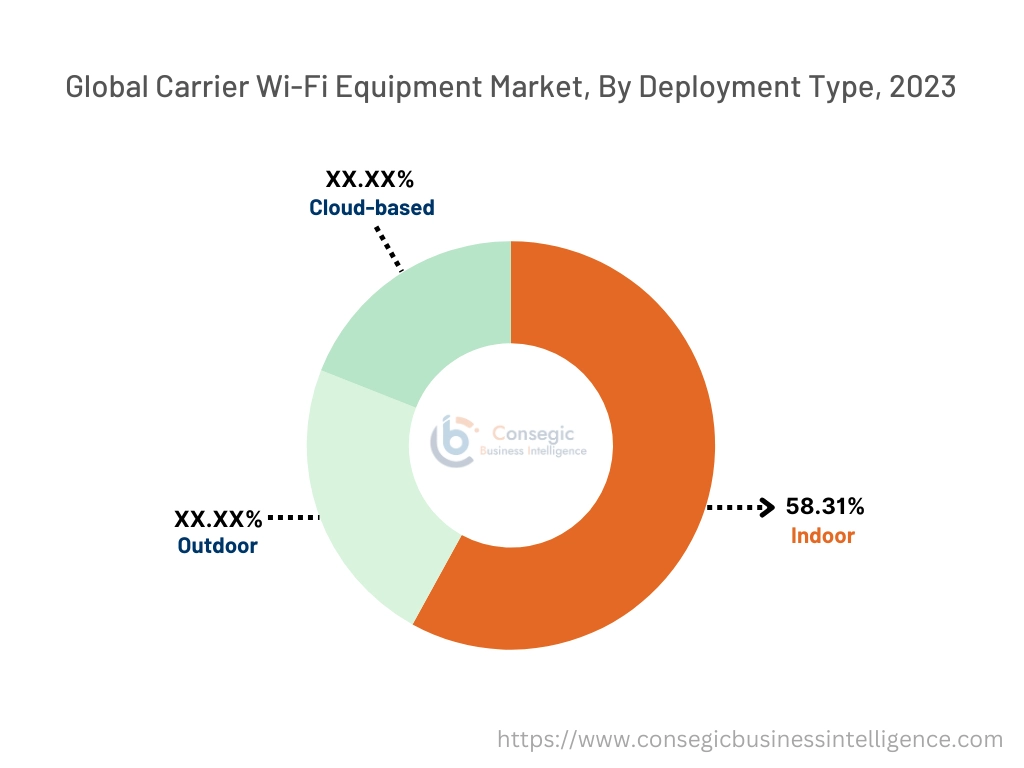

By Deployment Type:

Based on deployment type, the market is segmented into indoor, outdoor, and cloud-based deployments.

The indoor deployment segment accounted for the largest revenue share of 58.31% in 2023.

- Indoor Wi-Fi deployments are prevalent in environments such as offices, retail stores, educational institutions, and healthcare facilities, where reliable, high-speed connectivity is essential.

- The demand for seamless Wi-Fi coverage inside buildings, combined with the need for network security and user authentication, is driving the progress of indoor Wi-Fi equipment.

- Indoor access points and controllers offer features such as beamforming and MU-MIMO (multi-user, multiple-input, multiple-output), enhancing coverage and user experience.

- The increasing adoption of smart building technologies and the rise of enterprise digital transformation initiatives are further boosting the demand for indoor Wi-Fi solutions.

- Indoor deployments lead the market due to their widespread use in commercial, enterprise, and institutional settings, where consistent, high-quality connectivity is critical.

- As per segmental trends analysis, the indoor deployment segment boosts the market development.

The cloud-based deployment segment is anticipated to register the fastest CAGR during the forecast period.

- Cloud-based deployments offer scalability, flexibility, and ease of management, making them attractive for telecom operators and enterprises looking to streamline network operations.

- The growing trend of network virtualization and the adoption of software-defined networking (SDN) are driving the need for cloud-based Wi-Fi solutions.

- Cloud-based Wi-Fi management platforms provide real-time analytics, centralized control, and automated updates, enhancing network performance and user experience.

- The shift towards remote work and the increasing demand for flexible, scalable network solutions are contributing to the rapid development of cloud-based deployments.

- Cloud-based deployments are expected to grow rapidly, driven by the need for scalable, efficient, and easily manageable Wi-Fi solutions across various industries.

- As per segmental trends analysis, the cloud-based deployment segment boosts the market progress.

By End-User:

Based on end-user, the market is segmented into telecom operators, internet service providers (ISPs), enterprises, and government & public sector.

The telecom operators segment accounted for the largest revenue share in 2023.

- Telecom operators are the primary deployers of carrier Wi-Fi equipment, leveraging these solutions to offload mobile data traffic and enhance network capacity.

- The growing demand for high-speed mobile data, driven by increased smartphone usage and the expansion of 5G networks, is boosting the adoption of Wi-Fi solutions by telecom operators.

- Carrier Wi-Fi equipment enables telecom operators to provide seamless, high-performance connectivity, enhancing customer experience and reducing network congestion.

- Major telecom operators are investing heavily in advanced Wi-Fi technologies, including Wi-Fi 6, to deliver faster speeds and better coverage to their subscribers.

- Telecom operators lead the market due to their extensive infrastructure and strong focus on enhancing network capacity and user experience.

- Thus, due to the aforementioned factors the Telecom operators segment fuels the market development.

The enterprise segment is anticipated to register the fastest CAGR during the forecast period.

- Enterprises across various industries, including retail, healthcare, and manufacturing, are increasingly adopting carrier Wi-Fi equipment to provide reliable connectivity for employees, customers, and IoT devices.

- The shift towards digital transformation and the growing need for secure, high-performance wireless networks in business environments are driving demand in the enterprise segment.

- Enterprise Wi-Fi solutions offer features like enhanced security, network segmentation, and real-time analytics, supporting the complex connectivity needs of modern businesses.

- The adoption of hybrid work models and the increasing reliance on cloud-based applications are further propelling the development of enterprise Wi-Fi deployments.

- The enterprise segment is expected to grow rapidly, driven by the increasing need for scalable, secure, and high-performance Wi-Fi solutions in business environments.

- Thus, due to the aforementioned factors the enterprise segment fuels the market progress.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

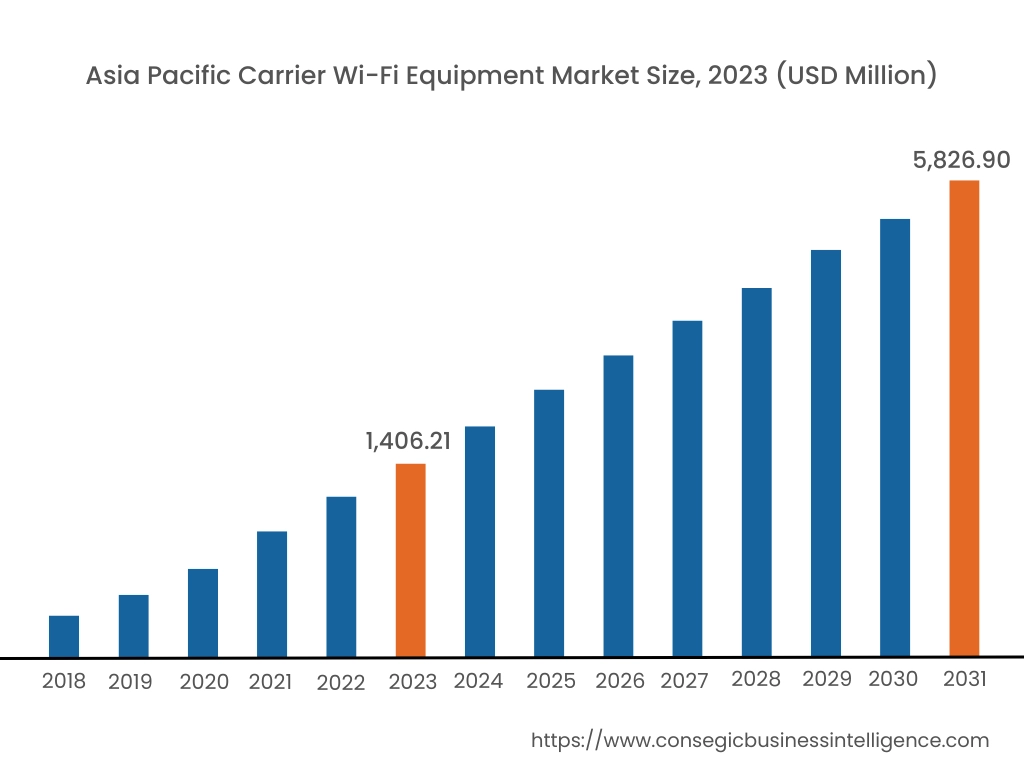

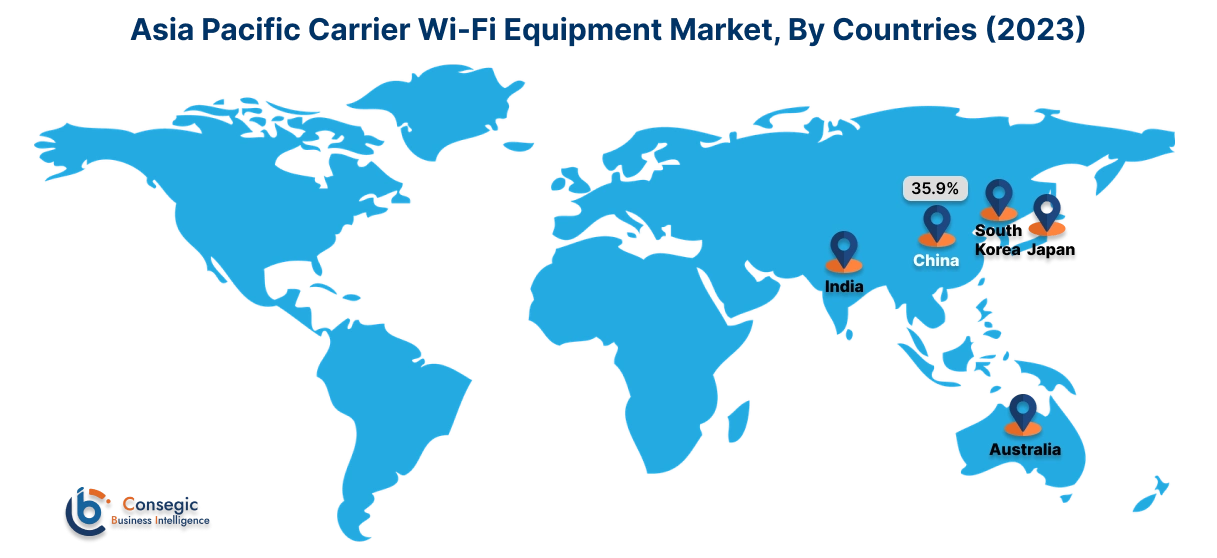

Asia Pacific region was valued at USD 1,406.21 Million in 2023. Moreover, it is projected to grow by USD 1,651.73 Million in 2024 and reach over USD 5,826.90 Million by 2031. Out of these, China accounted for the largest share of 35.9% in 2023. Asia-Pacific is witnessing the fastest progress in the carrier Wi-Fi equipment market, driven by increasing internet penetration, rapid urbanization, and the extension of the telecommunications industry in countries like China, Japan, and India. The region has become a global hub for electronics manufacturing, with a strong supply chain and cost advantages. The growing market need for mobile data services and the need to alleviate network congestion contribute to market progression.

North America is estimated to reach over USD 6,669.09 Million by 2031 from a value of USD 1,668.84 Million in 2023 and is projected to grow by USD 1,954.18 Million in 2024. This region holds a substantial share of the carrier Wi-Fi equipment market, primarily due to a well-established telecommunications infrastructure and early adoption of advanced technologies. The United States, in particular, has a significant market presence, with major telecom operators investing heavily in Wi-Fi solutions to offload mobile data traffic and improve indoor coverage. The need for seamless connectivity in public venues, enterprises, and residential areas propels market progress.

Europe represents a significant portion of the global carrier Wi-Fi equipment market, with countries like Germany, the UK, and France leading in terms of adoption and innovation. The region benefits from strong government support for digital initiatives and a robust industrial base. The focus on smart city projects and the integration of Wi-Fi networks with cellular networks further accelerates the adoption of carrier Wi-Fi solutions.

Asia-Pacific is witnessing the fastest growth in the carrier Wi-Fi equipment market, driven by increasing internet penetration, rapid urbanization, and the extension of the telecommunications sector in countries like China, Japan, and India. The region has become a global hub for electronics manufacturing, with a strong supply chain and cost advantages. The growing market need for mobile data services and the need to alleviate network congestion contribute to market progression.

The Middle East & Africa region shows promising potential in the carrier Wi-Fi equipment market, particularly in countries like the UAE, Saudi Arabia, and South Africa. Increasing investments in infrastructure, a growing consumer electronics market, and government initiatives to promote digital transformation drive the need for carrier Wi-Fi solutions. The expanding tourism industry and the adoption of smart technologies further support market growth.

Latin America is an emerging market for carrier Wi-Fi equipment, with Brazil and Mexico being the primary growth drivers. The rising adoption of smartphones, improving internet connectivity, and increasing focus on enhancing network capacity contribute to the market's development. Government initiatives aimed at modernizing telecommunications infrastructure and promoting foreign investments support market growth.

Top Key Players & Market Share Insights:

The Carrier Wi-Fi Equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Carrier Wi-Fi Equipment market. Key players in the Carrier Wi-Fi Equipment industry include –

- Cisco Systems, Inc. (USA)

- Aruba Networks (a Hewlett Packard Enterprise company) (USA)

- Ruckus Networks (a CommScope company) (USA)

- Extreme Networks, Inc. (USA)

- Ubiquiti Inc. (USA)

- Cambium Networks (USA)

- NETGEAR, Inc. (USA)

- Huawei Technologies Co., Ltd. (China)

- ZTE Corporation (China)

- Nokia Corporation (Finland)

Recent Industry Developments :

Product Launches:

- In October 2023, Nokia introduced the industry's first carrier-grade Wi-Fi 7 product portfolio, designed to offer high-speed and low-latency connectivity for homes and businesses. The portfolio includes advanced access points and beacons to deliver superior network performance, supporting growing bandwidth demands from applications like virtual reality and 8K video streaming. The Wi-Fi 7 products will be available in the first half of 2024, reinforcing Nokia's commitment to next-gen connectivity.

- In May 2023, CommScope introduced its new HomeVantage Fiber Gateways and ONUs (Optical Network Units) at the 2023 ANGA COM event. These advanced devices are designed to offer enhanced fiber connectivity, bringing faster and more reliable internet to homes. The products focus on delivering improved performance for service providers, supporting higher speeds and next-gen services, and ensuring efficient network operations for a better user experience.

Carrier Wi-Fi Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 21,375.28 Million |

| CAGR (2024-2031) | 18.8% |

| By Component |

|

| By Network Type |

|

| By Deployment Type |

|

| By End-user |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Carrier Wi-Fi Equipment market? +

Carrier Wi-Fi Equipment Market size is estimated to reach over USD 21,375.28 Million by 2031 from a value of USD 5,377.29 Million in 2023 and is projected to grow by USD 6,293.90 Million in 2024, growing at a CAGR of 18.8% from 2024 to 2031.

What specific segmentation details are covered in the Carrier Wi-Fi Equipment Market report? +

The Carrier Wi-Fi Equipment market report includes segmentation details for component, network type, deployment type, end-user and region.

What are the emerging opportunities in the Carrier Wi-Fi Equipment Market? +

Emerging opportunities in the Carrier Wi-Fi Equipment market include the growing demand for Wi-Fi 6 and Wi-Fi 6E technologies, the rise of public and private sector investments in smart city infrastructure, and the increasing adoption of IoT devices.

Who are the major players in the Carrier Wi-Fi Equipment Market? +

The key players in the Carrier Wi-Fi Equipment market include Cisco Systems, Inc. (USA), Aruba Networks (a Hewlett Packard Enterprise company) (USA), Ruckus Networks (a CommScope company) (USA), Extreme Networks, Inc. (USA), Ubiquiti Inc. (USA), Cambium Networks (USA), NETGEAR, Inc. (USA), Huawei Technologies Co., Ltd. (China), ZTE Corporation (China), and Nokia Corporation (Finland).