- Summary

- Table Of Content

- Methodology

Cargo Handling Equipment Market Size:

Cargo Handling Equipment Market size is estimated to reach over USD 33.23 Billion by 2032 from a value of USD 24.66 Billion in 2024 and is projected to grow by USD 25.16 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

Cargo Handling Equipment Market Scope & Overview:

The cargo handling equipment industry focuses on machinery and vehicles designed for the efficient movement, loading, unloading, and storage of goods in ports, airports, warehouses, and logistics hubs. These include forklifts, cranes, straddle carriers, reach stackers, and automated guided vehicles (AGVs), which enhance operational efficiency and streamline supply chain processes. Equipment is available in diesel, electric, and hybrid variants to meet environmental regulations and operational requirements.

Key characteristics of cargo handling equipment include high load-bearing capacity, durability, automation capabilities, and compliance with safety standards. The benefits include increased productivity, reduced manual labor, improved cargo management, and lower operational costs.

Applications span seaports, airports, manufacturing plants, and distribution centers, where efficient handling of containers, bulk cargo, and palletized goods is essential. End-users include port authorities, logistics companies, airport ground handlers, and warehouse operators, driven by increasing global trade volumes, advancements in automation and electrification, and growing investments in port and logistics infrastructure.

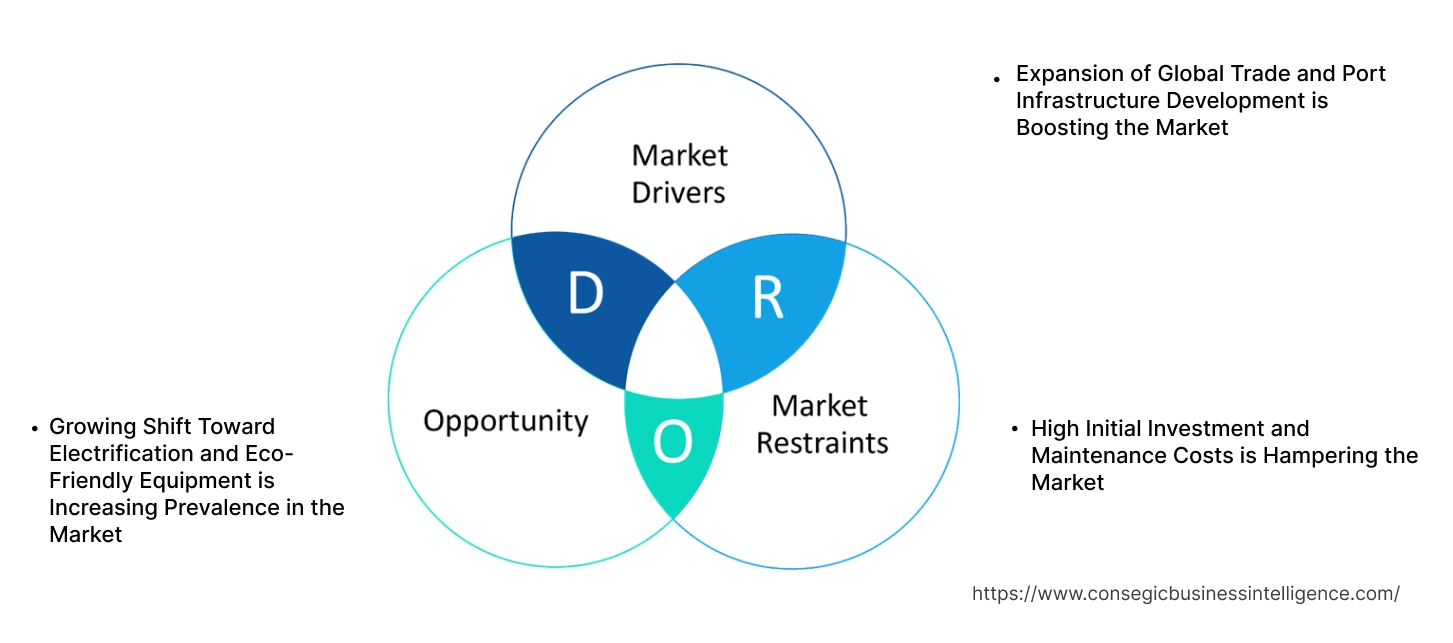

Cargo Handling Equipment Market Dynamics - (DRO) :

Key Drivers:

Expansion of Global Trade and Port Infrastructure Development is Boosting the Market

The rapid surge of global trade and increasing investments in port infrastructure development are significant drivers of the cargo handling equipment market. With rising international shipping activities, there is an increasing need for efficient equipment such as cranes, forklifts, straddle carriers, and reach stackers to facilitate cargo movement in ports, terminals, and warehouses. Governments and private entities are investing in modernizing ports and logistics hubs to improve operational efficiency and accommodate larger container ships. Additionally, automation trends such as AI-driven equipment and remote-controlled cargo handlers are reshaping cargo movement, enhancing speed, and reducing human error.

Key Restraints:

High Initial Investment and Maintenance Costs is Hampering the Market

A major challenge in the cargo handling equipment market is the high initial investment required for advanced machinery, coupled with ongoing maintenance and operational expenses. Heavy-duty cargo handling machinery involves significant capital expenditure, making it difficult for small and mid-sized logistics operators to adopt high-end solutions. Additionally, frequent servicing and part replacements, especially in fuel-powered equipment, contribute to long-term ownership costs. In regions with budget constraints, these financial challenges limit the adoption of technologically advanced cargo handling solutions, slowing modernization efforts in certain markets.

Future Opportunities :

Growing Shift Toward Electrification and Eco-Friendly Equipment is Increasing Prevalence in the Market

The increasing emphasis on sustainability and emissions reduction in port and warehouse operations presents a major opportunity for the cargo handling equipment market growth. Governments worldwide are implementing strict environmental regulations, prompting a shift toward electrification and hybrid cargo movers. Electric cranes, battery-powered forklifts, and hydrogen fuel cell cargo handlers are emerging as viable alternatives to traditional diesel-powered machinery. These innovations not only reduce carbon emissions but also lower long-term operational expenses. Additionally, cargo handling equipment market trends in IoT integration and real-time monitoring solutions are improving fleet management, predictive maintenance, and overall equipment efficiency, further accelerating market adoption.

These market dynamics highlight the increasing cargo handling equipment market opportunities for efficient and sustainable cargo handling equipment as trade volumes rise. While demand remains strong, high costs pose a challenge, making affordability and efficiency key priorities. However, the growing trends for electrification, smart automation, and eco-friendly solutions presents substantial opportunities for industry growth. As trends in automation and sustainability continue to shape the sector, the adoption of innovative technologies is expected to drive further rising trends across global cargo handling operations.

Cargo Handling Equipment Market Segmental Analysis :

By Equipment Type:

Based on equipment type, the market is segmented into cranes, forklifts, straddle carriers, reach stackers, terminal tractors, automated guided vehicles (AGVs), conveyor systems, and others.

The cranes segment accounted for the largest revenue of cargo handling equipment market share in 2024.

- Cranes play a crucial role in large-scale cargo movement at ports and terminals, ensuring efficiency in containerized shipping.

- Increasing investments in port infrastructure and automation enhance the adoption of advanced cranes.

- Technological advancements, such as remote-controlled and AI-assisted cranes, improve operational accuracy and safety.

- Surge in world trade and containerized cargo transportation further solidifies cranes as a primary cargo handling solution.

The automated guided vehicles (AGVs) segment is anticipated to register the fastest CAGR during the forecast period.

- AGVs are increasingly deployed in warehouses, ports, and distribution centers to optimize cargo movement with minimal human intervention.

- Rising interest in automation to improve efficiency and reduce operational costs supports the growing use of AGVs.

- Advancements in AI, IoT, and robotics enhance the functionality and precision of AGVs, making them integral to future cargo operations.

- Growth of smart warehouses and autonomous logistics operations fuels the segment’s advancement.

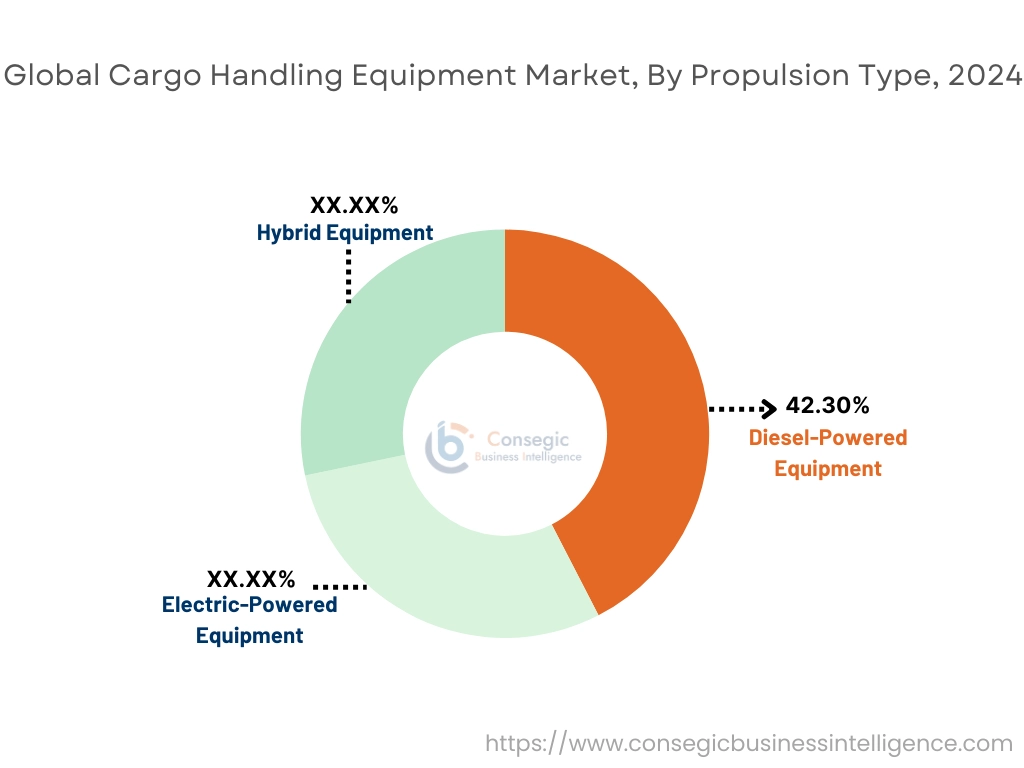

By Propulsion Type:

Based on propulsion type, the market is segmented into diesel-powered equipment, electric-powered equipment, and hybrid equipment.

The diesel-powered equipment segment accounted for the largest revenue share of 42.30% in 2024.

- Diesel-powered cargo handling equipment remains widely used due to its high power output and ability to handle heavy loads efficiently.

- Despite increasing environmental concerns, diesel-powered equipment continues to be essential in high-capacity operations.

- Advances in cleaner diesel technologies and fuel efficiency improvements help sustain the segment’s relevance.

- As per the analysis the ongoing infrastructure projects in developing economies contribute to continued reliance on diesel-powered handling equipment.

The electric-powered equipment segment is expected to register the fastest CAGR during the forecast period.

- The shift toward sustainability and emission reduction regulations accelerates growth in the adoption of electric cargo handling solutions.

- Increasing advancements in battery technology, including higher capacity and faster charging, enhance the feasibility of electric equipment.

- Ports, warehouses, and distribution centers are prioritizing electrification to reduce carbon footprints and operational costs.

- The rise of renewable energy integration into logistics facilities further promotes the adoption of electric-powered cargo handling equipment.

By Application:

Based on application, the market is segmented into port handling, rail cargo handling, air cargo handling, warehouse handling, and industrial material handling.

The port handling segment accounted for the largest revenue of cargo handling equipment market share in 2024.

- Ports serve as primary hubs for world trade, requiring high-capacity cargo handling equipment to manage containerized goods efficiently.

- Increasing investments in smart port technologies and automation enhance cargo handling efficiency and throughput.

- The rise of global shipping networks and rising container volumes strengthen the need for advanced port handling solutions.

- Adoption of AI-powered cargo tracking and management systems further optimizes port operations.

The warehouse handling segment is anticipated to register the fastest CAGR during the forecast period.

- Growth in e-commerce and logistics industries is driving the cargo handling equipment market expansion of warehouses and distribution centers.

- The rising trend of automated warehouses fuels the demand for advanced cargo handling solutions, including conveyor systems and AGVs.

- Increasing cargo handling equipment market trends for AI-driven inventory management systems enhance the efficiency of warehouse operations.

- The growing use of cold storage facilities and specialized warehousing solutions further boosts cargo handling equipment market demand for advanced handling equipment.

By End-User:

Based on end-user, the market is segmented into ports & terminals, airports, rail yards, warehouses & distribution centers, manufacturing facilities, and logistics & freight forwarding companies.

The ports & terminals segment accounted for the largest revenue share in 2024.

- Ports serve as key transportation hubs for international trade, requiring high-capacity equipment to manage increasing cargo volumes.

- Investments in port expansion projects and automation technologies drive the need for efficient cargo movement solutions.

- Adoption of smart port systems and AI-driven logistics solutions enhances operational efficiency and throughput.

- Rising focus on sustainability and emission reduction initiatives further promotes the adoption of energy-efficient handling equipment.

The warehouses & distribution centers segment is anticipated to register the fastest CAGR during the forecast period.

- The rapid surge of e-commerce and allover supply chain networks increases the need for automated and high-performance handling systems.

- Integration of AI, robotics, and IoT in warehouse operations enhances efficiency and reduces manual labor dependency.

- Growing consumer preference for same-day and express delivery services drives the need for faster cargo handling solutions.

- Development of multi-modal logistics hubs and automated storage facilities fuels the market for warehouse handling equipment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

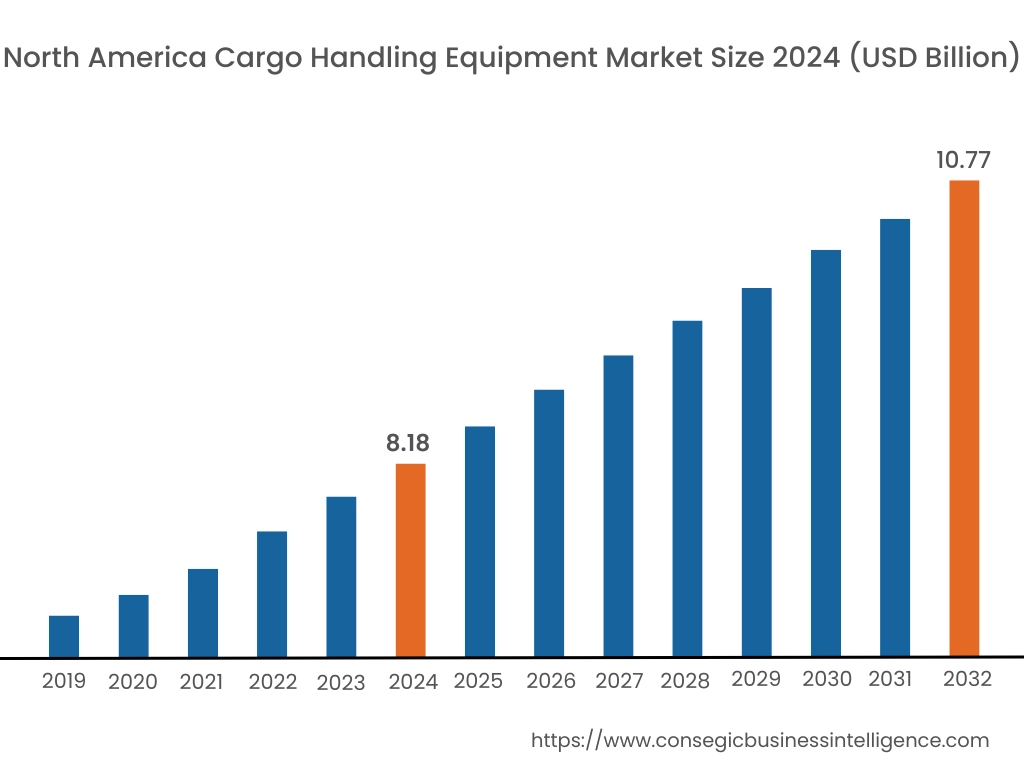

In 2024, North America was valued at USD 8.18 Billion and is expected to reach USD 10.77 Billion in 2032. In North America, the U.S. accounted for the highest share of 71.30% during the base year of 2024. North America holds a significant share of the cargo handling equipment market, driven by the growth of seaports, airports, and logistics hubs across the region. The U.S. leads in adoption due to rising trade volumes, increasing automation in cargo terminals, and government investments in port infrastructure. Canada supports cargo handling equipment market expansion with modernization initiatives at major ports and increased demand for electric and hybrid cargo handling equipment to reduce emissions. The analysis highlights that stringent environmental regulations are encouraging the transition toward sustainable equipment solutions in this region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.2% over the forecast period. The cargo handling equipment market is fueled by rapid trade enlargement, growing seaport capacities, and increasing investments in infrastructure in China, India, and Japan. China dominates with large-scale port enlargement and high demand for automated handling equipment to manage bulk cargo operations. India’s market is growing due to increased container traffic, government-backed logistics development projects, and the integration of smart handling systems. Japan focuses on advanced cargo handling solutions with a strong emphasis on sustainability and automation in port and airport operations. Analysis indicates that government-led infrastructure investments are a major driving force for market in this region.

Europe is a key market for cargo handling equipment, supported by stringent emission norms, automation in port terminals, and rising e-commerce-driven logistics operations. Countries like Germany, the UK, and France are major contributors. Germany emphasizes efficiency improvements in cargo terminals with the integration of smart cargo handling technologies. The UK focuses on port electrification and the use of hybrid cargo handling equipment to meet its sustainability goals, while France is investing in upgrading its airport cargo handling infrastructure. Analysis suggests that the adoption of advanced fleet management systems and automation is a key factor influencing market dynamics.

The Middle East & Africa region is witnessing steady market surge, driven by increasing investments in logistics infrastructure, expanding trade routes, and port modernization projects. Countries like Saudi Arabia and the UAE are enhancing their cargo handling capabilities through automation and electrification initiatives in seaports and airports. In Africa, South Africa is emerging as a key market, focusing on upgrading its cargo handling systems to support growing trade activities. Regional cargo handling equipment market analysis highlights that reliance on imported cargo handling equipment poses cost challenges, affecting procurement strategies in some countries.

Latin America is an emerging market for cargo handling equipment, with Brazil and Mexico leading the region. Brazil’s growing seaport and airport cargo operations drive demand for efficient and cost-effective handling solutions. Mexico focuses on enhancing logistics operations in industrial zones, leading to increased adoption of container handling and forklift equipment. The cargo handling equipment market analysis shows that partnerships between local and international equipment manufacturers are improving technology adoption and accessibility in the region. However, economic fluctuations and infrastructure limitations may restrict broader cargo handling equipment market growth.

Top Key Players & Market Share Insights:

The cargo handling equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global cargo handling equipment market. Key players in the cargo handling equipment industry include -

- Konecranes PLC (Finland)

- Cargotec Corporation (MacGregor) (Finland)

- SANY Group (China)

- ACE (Action Construction Equipment) (India)

- Jungheinrich AG (Germany)

- Liebherr Group (Germany)

- Toyota Industries Corporation (Japan)

- Kalmar (Finland)

- Hyster-Yale Materials Handling, Inc. (USA)

- TIL Limited (India)

Recent Industry Developments :

Innovations:

- In April 2024, Alstef Group made a strategic move to expand its footprint in India with the opening of an innovation center, which focuses on enhancing baggage and cargo handling systems at airports. This expansion includes introducing cutting-edge automation and robotics to streamline cargo handling, improving efficiency and safety. The integration of these advanced technologies aims to support the growing cargo handling equipment market demand for more efficient and faster cargo handling in India’s rapidly expanding logistics and aviation sectors. This development is expected to significantly impact the cargo handling equipment market, particularly in the automation of loading and unloading processes in airports.

- In May 2024, Dnata unveiled its strategic plan to integrate digital and autonomous innovations in its cargo handling operations, marking a significant shift towards a more data-driven supply chain. The company is deploying new technologies at its global facilities, including 48 warehouses across 13 countries, aiming to enhance operational efficiency and customer experience. This includes automated check-ins, traffic management systems, and digital cargo tracking, all designed to streamline the cargo journey. This development positions Dnata at the forefront of digital transformation in the air cargo sector, driving innovation in cargo handling equipment.

Cargo Handling Equipment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 33.23 Billion |

| CAGR (2025-2032) | 3.8% |

| By Equipment Type |

|

| By Propulsion Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the current and projected size of the Cargo Handling Equipment Market? +

Cargo Handling Equipment Market size is estimated to reach over USD 33.23 Billion by 2032 from a value of USD 24.66 Billion in 2024 and is projected to grow by USD 25.16 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

What are the key types of cargo handling equipment used in the market? +

The market is segmented into cranes, forklifts, straddle carriers, reach stackers, terminal tractors, automated guided vehicles (AGVs), conveyor systems, and others. Cranes held the largest market share in 2024 due to their critical role in port operations, while AGVs are experiencing rapid growth driven by automation in logistics.

Which propulsion type dominates the Cargo Handling Equipment Market? +

Diesel-powered equipment accounted for the largest revenue share in 2024 due to its high power output and reliability for heavy-load applications. However, electric-powered equipment is expected to witness the fastest growth due to increasing regulations on emissions and the rising adoption of sustainable cargo handling solutions.

What factors are driving the growth of the Cargo Handling Equipment Market? +

Growth is driven by increasing global trade volumes, rising port infrastructure development, growing automation in cargo operations, and the shift toward sustainable and electrified handling solutions.