- Summary

- Table Of Content

- Methodology

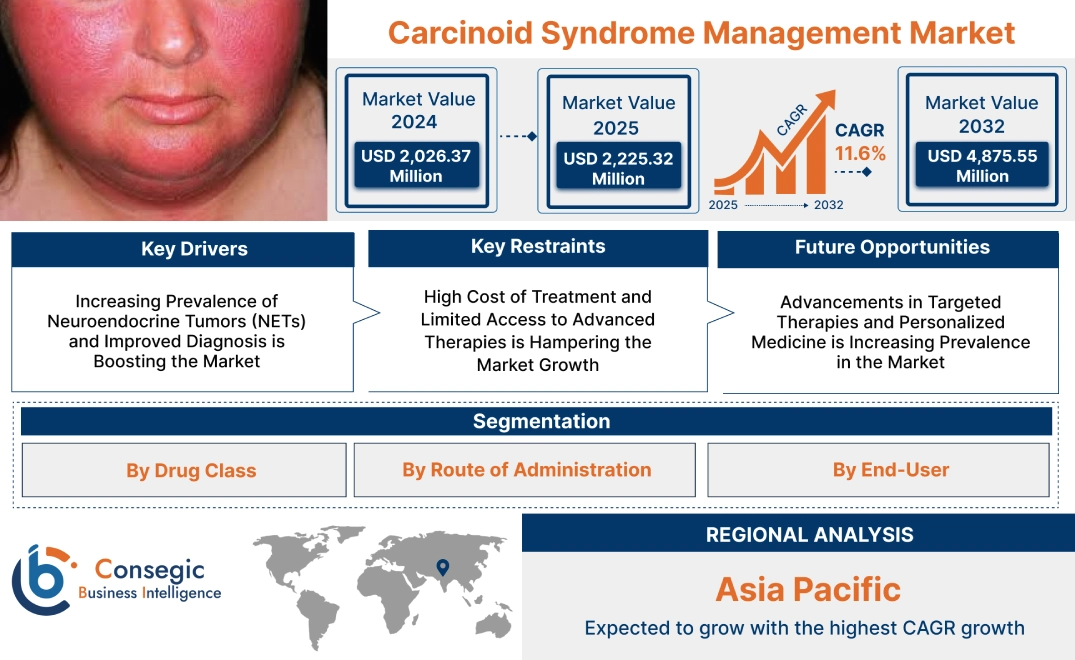

Carcinoid Syndrome Management Market Size:

The Carcinoid Syndrome Management Market size is estimated to reach over USD 4,875.55 Million by 2032 from a value of USD 2,026.37 Million in 2024 and is projected to grow by USD 2,225.32 Million in 2025, growing at a CAGR of 11.6% from 2025 to 2032.

Carcinoid Syndrome Management Market Scope & Overview:

The carcinoid syndrome management industry focuses on the diagnosis, treatment, and long-term care of patients affected by carcinoid syndrome, a condition caused by neuroendocrine tumors (NETs) that release excessive serotonin and other hormones. Management strategies include pharmaceutical therapies such as somatostatin analogs (SSAs), serotonin synthesis inhibitors, targeted therapies, and peptide receptor radionuclide therapy (PRRT). In addition, dietary modifications and symptomatic treatments are often integrated into patient care.

Key characteristics of carcinoid syndrome management include early symptom control, long-term tumor stabilization, and improved patient quality of life. The benefits include reduced flushing and diarrhea episodes, minimized hormone-related complications, and enhanced treatment efficacy through combination therapies.

Applications span oncology treatment centers, hospitals, and specialty clinics, where patients receive tailored therapies for symptom management and tumor progression control. End-users include oncologists, gastroenterologists, and healthcare providers, driven by increasing incidence of neuroendocrine tumors, advancements in targeted therapies, and growing awareness of early diagnosis and effective symptom management strategies.

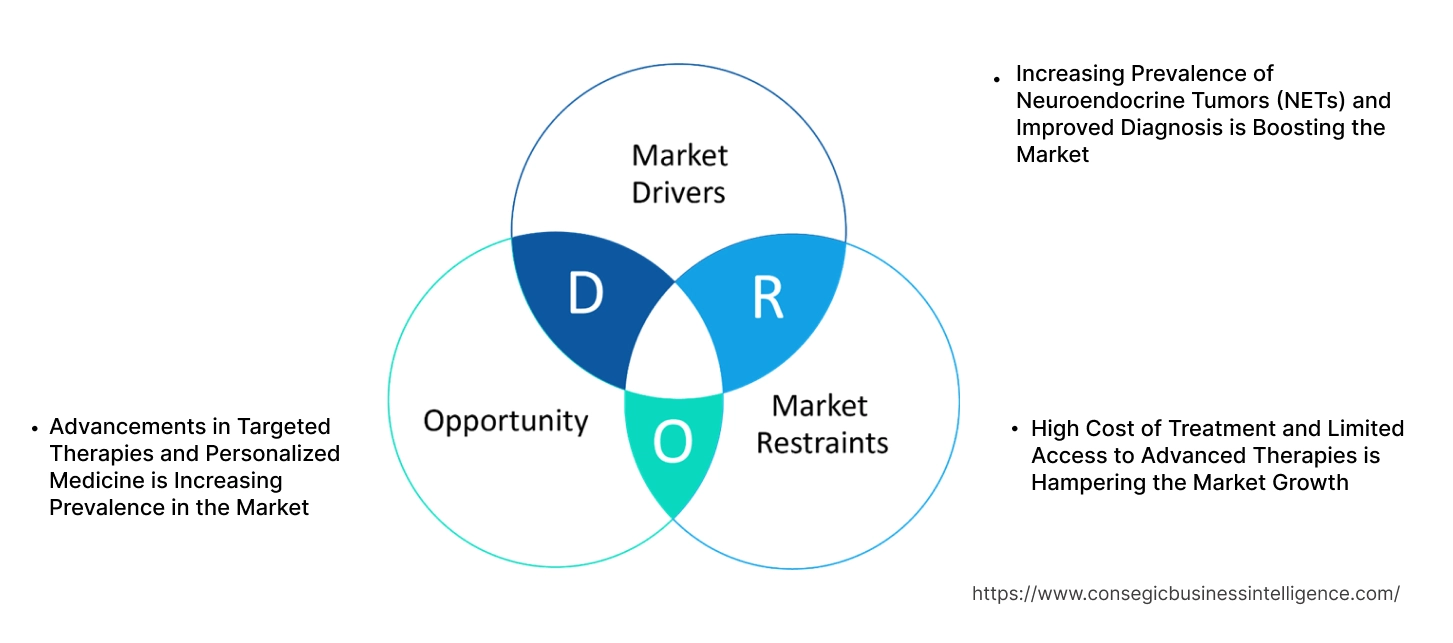

Carcinoid Syndrome Management Market Dynamics - (DRO) :

Key Drivers:

Increasing Prevalence of Neuroendocrine Tumors (NETs) and Improved Diagnosis is Boosting the Market

The rising incidence of neuroendocrine tumors (NETs), which are the primary cause of carcinoid syndrome, is a major driver for the market. With advancements in diagnostic imaging and biomarker testing, early detection rates have improved, leading to a greater number of patients requiring long-term management. Additionally, increased awareness among healthcare professionals about the symptoms of carcinoid syndrome, such as flushing, diarrhea, and wheezing, has contributed to a demand for effective treatment options. The availability of targeted therapies, somatostatin analogs (SSAs), and newer biologic treatments has further expanded the market by improving symptom control and patient quality of life.

Key Restraints:

High Cost of Treatment and Limited Access to Advanced Therapies is Hampering the Market Growth

A significant barrier in the market is the high cost of treatment, particularly for advanced therapies such as somatostatin analogs, targeted drug therapies, and peptide receptor radionuclide therapy (PRRT). These treatments are often expensive and require continuous administration, leading to substantial long-term healthcare expenses. Additionally, access to specialized treatment centers and expert oncologists is limited in many emerging markets, restricting the availability of demanded therapies. Variability in insurance coverage and reimbursement policies further complicates access to optimal treatment, limiting carcinoid syndrome management market growth in regions with healthcare affordability challenges.

Future Opportunities :

Advancements in Targeted Therapies and Personalized Medicine is Increasing Prevalence in the Market

The development of targeted therapies and personalized treatment approaches presents a significant opportunity for the market. Research in biomarker-driven therapies and novel drug formulations is enabling more effective and individualized treatment plans, reducing symptom severity and improving patient outcomes. Additionally, trends in combination therapies—such as somatostatin analogs used alongside mTOR inhibitors or PRRT—are showing promise in enhancing disease control. Companies investing in genomic research and precision medicine are well-positioned to capitalize on these advancements, expanding the market by offering tailored treatment solutions.

These market dynamics highlight the increasing demand for effective carcinoid syndrome management driven by improved diagnostics and novel treatment options. While cost barriers and access limitations remain challenges, innovations in targeted therapies and trends in personalized medicine are creating new trends in carcinoid syndrome management market opportunities for pharmaceutical companies and healthcare providers in this space.

Carcinoid Syndrome Management Market Segmental Analysis :

By Drug Class:

Based on drug class, the market is segmented into somatostatin analogs (SSAs), serotonin synthesis inhibitors, targeted therapies, chemotherapy agents, and others.

The somatostatin analogs (SSAs) segment accounted for the largest revenue of carcinoid syndrome management market share in 2024.

- SSAs, such as octreotide and lanreotide, are widely used as first-line therapies for controlling hormone secretion and reducing symptoms of carcinoid syndrome.

- Increasing preference for long-acting SSA formulations enhances patient compliance and treatment outcomes.

- Growing awareness and availability of SSAs in both developed and emerging markets drive their adoption.

- Advancements in sustained-release and depot injection formulations further support this segment’s trends.

The targeted therapies segment is anticipated to register the fastest CAGR during the forecast period.

- Targeted therapies, including tyrosine kinase inhibitors (TKIs) and peptide receptor radionuclide therapy (PRRT), are gaining traction for their efficacy in advanced carcinoid tumors.

- Increasing R&D investments in personalized medicine and molecular-targeted treatments support this segment’s rapid growth.

- Expanding approvals for novel targeted agents, such as everolimus and lutetium-177 PRRT, enhance treatment options.

- Growing focus on precision oncology and biomarker-driven treatment strategies contributes to market advancement.

By Route of Administration:

Based on route of administration, the market is segmented into oral and injectable.

The injectable segment accounted for the largest revenue of carcinoid syndrome management market share in 2024.

- Injectable therapies, particularly SSAs and PRRT, are the standard treatments for managing carcinoid syndrome symptoms and tumor growth.

- Increasing adoption of long-acting injectables (LAIs) enhances treatment adherence and reduces hospital visits.

- Advancements in subcutaneous and intramuscular formulations improve patient comfort and administration efficiency.

- Expanding availability of biologic therapies and novel injectable formulations strengthens market trends.

The oral segment is anticipated to register the fastest CAGR during the forecast period.

- Oral therapies, including serotonin synthesis inhibitors and targeted agents, are gaining traction due to their convenience and ease of administration.

- Increasing development of small-molecule inhibitors and oral targeted therapies improves treatment accessibility.

- Growing patient preference for non-invasive treatment options supports the adoption of oral medications.

- Ongoing research into novel oral formulations, including sustained-release and combination therapies, drives segment expansion.

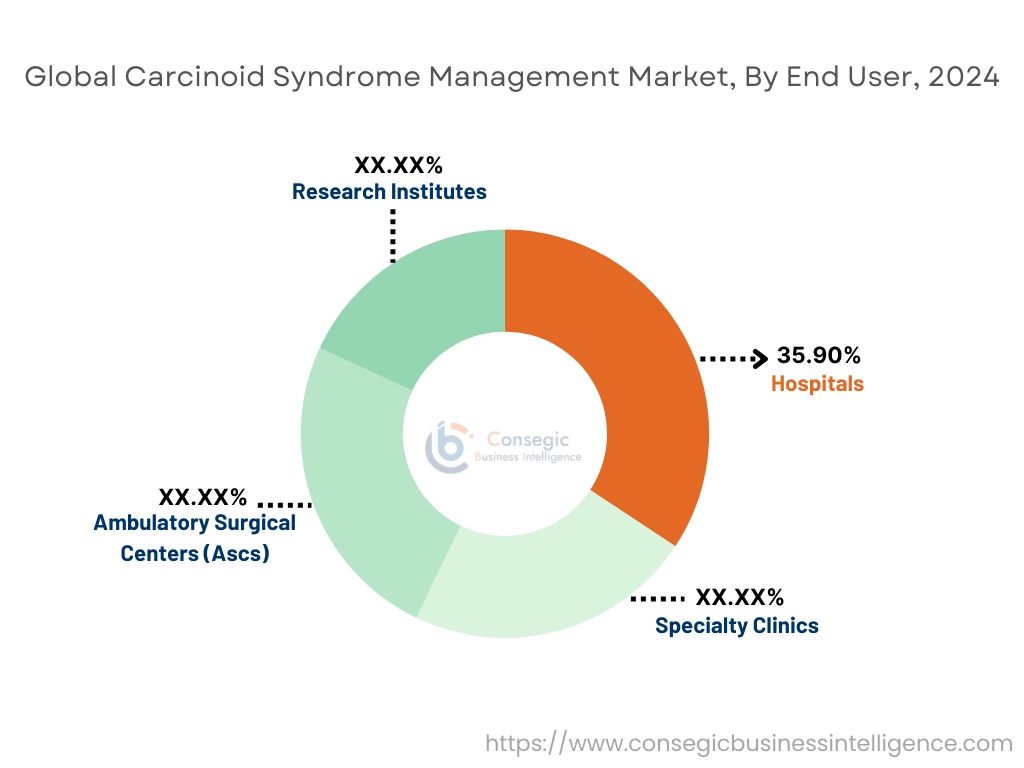

By End-User:

Based on end-user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers (ASCs), and research institutes.

The hospitals segment accounted for the largest revenue share of 35.90% in 2024.

- Hospitals serve as primary treatment centers for carcinoid syndrome patients requiring specialized care and advanced therapies.

- Increasing hospital-based administration of PRRT and injectable SSAs supports carcinoid syndrome management market trends.

- Availability of multidisciplinary teams, including oncologists and endocrinologists, enhances treatment outcomes in hospital settings.

- Expanding healthcare infrastructure and investments in cancer care centers further drive carcinoid syndrome management market demand in this segment analysis.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics offer focused care for neuroendocrine tumors (NETs) and carcinoid syndrome, improving patient management.

- Rising preference for outpatient treatment options, including long-acting SSA injections, supports this segment’s carcinoid syndrome management market trends.

- Increasing collaborations between specialty clinics and pharmaceutical companies enhance access to innovative therapies.

- Growing awareness and diagnosis of carcinoid syndrome in specialty healthcare settings contribute to carcinoid syndrome management market expansion.

Regional Analysis:

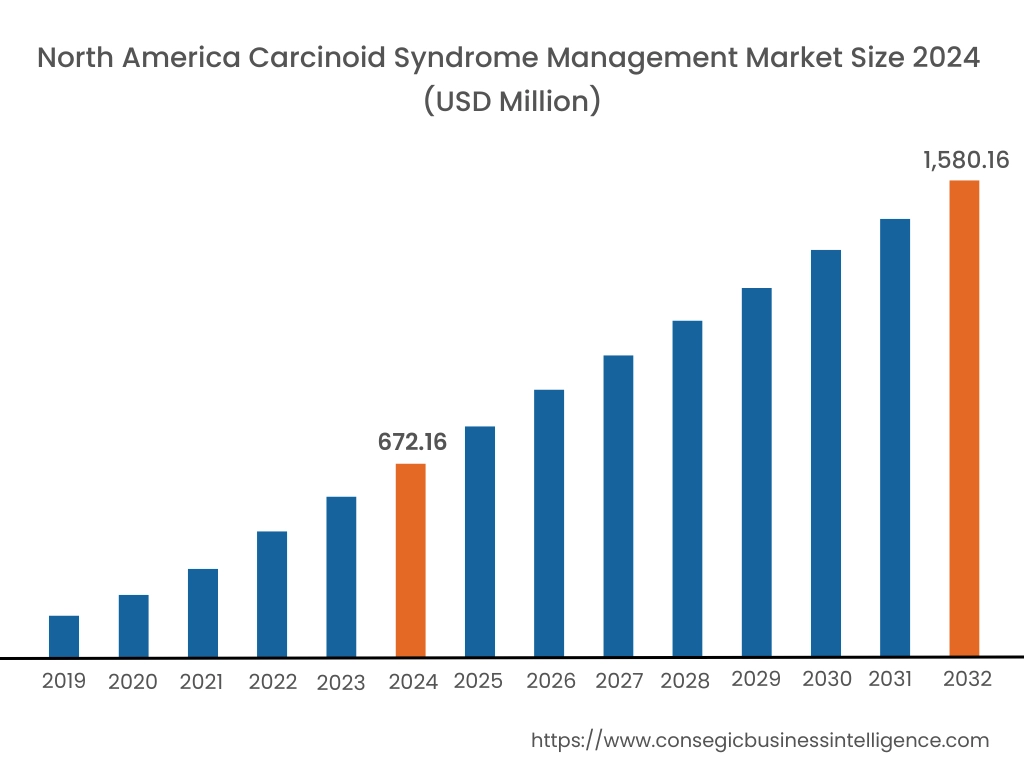

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2024, North America was valued at USD 672.16 Million and is expected to reach USD 1,580.16 Million in 2032. In North America, the U.S. accounted for the highest share of 72.60% during the base year of 2024. North America holds a significant share in the global carcinoid syndrome management market, driven by high awareness, advanced healthcare infrastructure, and strong investment in oncology research. The U.S. leads the region with increasing cases of neuroendocrine tumors (NETs) and a well-established pharmaceutical sector focusing on targeted therapies. The availability of somatostatin analogs and novel drug developments support treatment advancements. Canada contributes through government-funded healthcare programs that improve patient access to specialized treatments. Analysis indicates that ongoing clinical trials and FDA approvals for new therapies are key factors influencing market expansion in this region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 12.1%over the forecast period. The syndrome management market is fueled by improving healthcare infrastructure, rising incidence of neuroendocrine tumors, and increasing government investments in oncology care in China, India, and Japan. China dominates the regional trends due to its expanding access to cancer diagnostics and ongoing research into targeted therapies. India’s carcinoid syndrome management market growth is driven by increasing awareness of carcinoid syndrome and the development of cost-effective treatment options. Japan focuses on advanced drug formulations and precision oncology, leveraging its strong R&D capabilities. Analysis suggests that the rising availability of specialty healthcare centers and clinical trials for novel therapeutics is driving carcinoid syndrome management market expansion.

Europe is a key market for carcinoid syndrome management, supported by a rising prevalence of NETs, well-developed healthcare policies, and increasing adoption of precision medicine. Countries like Germany, the UK, and France are major contributors. Germany leads with extensive research on neuroendocrine tumors and access to advanced therapies. The UK focuses on patient support programs and improved diagnostics, while France emphasizes early detection and pharmaceutical collaborations for novel drug development. Analysis highlights that the European Medicines Agency's (EMA) approval of new treatment options is shaping the regional market, alongside increasing efforts to enhance early diagnosis rates.

The Middle East & Africa region is witnessing steady growth in the carcinoid syndrome management market, driven by increasing investments in cancer care infrastructure and improving access to specialized treatments. Countries like Saudi Arabia and the UAE are adopting advanced therapeutic options, supported by healthcare modernization initiatives. In Africa, South Africa is emerging as a key market, with efforts to improve diagnostic capabilities and expand access to oncology treatments. Regional carcinoid syndrome management market analysis points to challenges such as limited specialized treatment centers and high costs associated with targeted therapies, which may affect market accessibility in certain areas.

Latin America is an emerging market for carcinoid syndrome management, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and increasing incidence of neuroendocrine tumors drive carcinoid syndrome management market demand for advanced treatment options. Mexico focuses on expanding oncology care facilities and improving patient access to somatostatin analogs and targeted therapies. The carcinoid syndrome management market analysis highlights that partnerships with global pharmaceutical companies and local healthcare initiatives are enhancing treatment availability, despite economic challenges that may impact affordability in some countries.

Top Key Players & Market Share Insights:

The carcinoid syndrome management market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global carcinoid syndrome management market. Key players in the carcinoid syndrome management industry include -

- Ipsen Pharma (France)

- Novartis International AG (Switzerland)

- Exelixis, Inc. (USA)

- MediGene AG (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Ferring Pharmaceuticals (Switzerland)

- Horizon Therapeutics (Ireland)

- Pfizer Inc. (USA)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lexicon Pharmaceuticals (USA)

Carcinoid Syndrome Management Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4,875.55 Million |

| CAGR (2025-2032) | 11.6% |

| By Drug Class |

|

| By Route of Administration |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the current and projected size of the Carcinoid Syndrome Management Market? +

The Carcinoid Syndrome Management Market size is estimated to reach over USD 4,875.55 Million by 2032 from a value of USD 2,026.37 Million in 2024 and is projected to grow by USD 2,225.32 Million in 2025, growing at a CAGR of 11.6% from 2025 to 2032.

What are the key drug classes used in the management of carcinoid syndrome? +

The market is segmented into somatostatin analogs (SSAs), serotonin synthesis inhibitors, targeted therapies, chemotherapy agents, and others. Somatostatin analogs (SSAs) held the largest market share in 2024 due to their efficacy in controlling hormone secretion and symptoms, while targeted therapies are expected to grow at the fastest CAGR due to advancements in precision medicine and biomarker-driven treatments.

Which route of administration dominates the Carcinoid Syndrome Management Market? +

Injectable therapies accounted for the largest revenue share in 2024, primarily due to the widespread use of long-acting somatostatin analogs and peptide receptor radionuclide therapy (PRRT). The oral segment is expected to register the fastest CAGR, driven by increasing adoption of serotonin synthesis inhibitors and targeted therapies offering convenience and improved patient compliance.

What factors are driving the growth of the Carcinoid Syndrome Management Market? +

Growth is driven by the increasing prevalence of neuroendocrine tumors (NETs), improvements in diagnostic imaging and biomarker testing, and advancements in targeted therapies. The growing awareness of carcinoid syndrome symptoms among healthcare professionals has led to earlier detection and better patient outcomes, further supporting market expansion.