- Summary

- Table Of Content

- Methodology

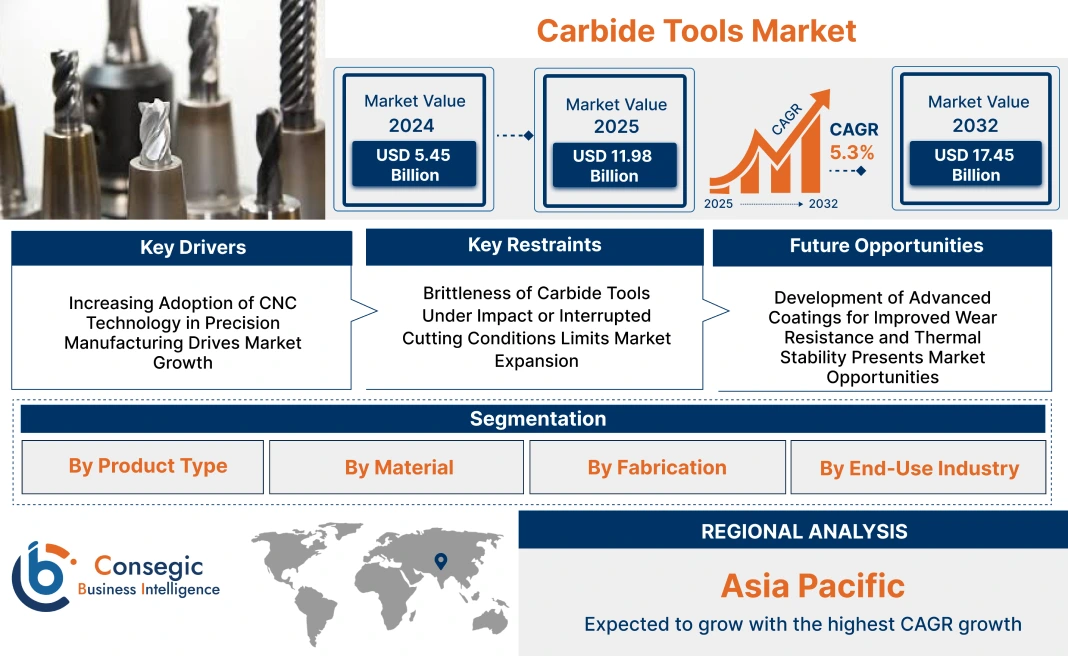

Carbide Tools Market Size:

Carbide Tools Market size is estimated to reach over USD 17.45 Billion by 2032 from a value of USD 11.58 Billion in 2024 and is projected to grow by USD 11.98 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

Carbide Tools Market Scope & Overview:

Carbide tools are precision-cutting instruments manufactured from carbide compounds, primarily tungsten carbide, known for their exceptional hardness and wear resistance. These tools are widely used in machining operations across automotive, aerospace, metal fabrication, and general manufacturing sectors.

Typical product categories include end mills, inserts, drills, reamers, and taps, designed for high-speed, high-precision cutting applications. Their ability to maintain sharp edges and structural stability under high temperatures ensures extended tool life and reduced downtime.

The key benefits of carbide tools are enhanced dimensional accuracy, resistance to deformation, and compatibility with both ferrous and non-ferrous materials. Furthermore, they support increased cutting speeds and feed rates, improving productivity and surface finish in complex manufacturing processes. Additionally, from heavy-duty milling to fine-detail turning, these tools remain indispensable for operations demanding reliability, consistency, and long-term performance in both manual and automated machining environments.

Carbide Tools Market Dynamics - (DRO) :

Key Drivers:

Increasing Adoption of CNC Technology in Precision Manufacturing Drives Market Growth

The growing reliance on computer numerical control (CNC) machines across industrial manufacturing is significantly accelerating the use of carbide tools. CNC technology enables automated, repeatable machining with extreme accuracy, making it essential for sectors like aerospace, automotive, medical devices, die and mold manufacturing, and general engineering. They are favored in these environments due to their ability to maintain structural rigidity and sharpness at high spindle speeds, feed rates, and under elevated temperatures. As manufacturing becomes more complex and precision-driven, the need for tools that offer dimensional stability, minimal vibration, and extended tool life continues to rise. Additionally, automated production lines using multi-axis CNC systems benefit from carbide tooling’s ability to withstand continuous use without compromising on tolerances or surface finish.

- For instance, in September 2024, Star Cutter launched the Advanced FLX Machine, powered by NUM FlexiumPro CNC Control System and the NUMROTO software to enhance automation and productivity for high-volume tool manufacturers. The machine has achieved a 30 % reduction in wheel change time, due to a redesigned wheel magazine area and increased system processing power. It also contains integrated robotics to handle both wheel and tool changes, offering up to 15 wheel pack locations and 1200 tools, extending automated production runs and ensuring faster manufacturing of tools.

In both high-volume and small-batch production settings, manufacturers are shifting toward advanced tool materials to reduce downtime and scrap. This shift is driving consistent demand, resulting in long-term carbide tools market expansion.

Key Restraints:

Brittleness of Carbide Tools Under Impact or Interrupted Cutting Conditions Limits Market Expansion

Despite offering superior hardness and thermal resistance, carbide tools face a critical drawback—their inherent brittleness under mechanical shock or inconsistent loading. In interrupted cutting operations, such as slotting, roughing of castings, or facing components with hard spots or inclusions, they are prone to edge chipping or sudden fracture. This vulnerability reduces reliability in applications where machine stability, workpiece uniformity, or fixturing rigidity cannot be assured. Operators working with older or less robust CNC machinery may hesitate to adopt them due to the increased risk of tool failure. Furthermore, in industries where mixed-material machining is common, such as aerospace and heavy machinery, tool breakage can lead to production delays and increased tooling costs. These risks deter adoption, especially among small and medium manufacturers. Although demand for high-performance tools continues to grow, this material limitation restrains the carbide tools market growth in scenarios requiring high toughness and impact tolerance.

Future Opportunities :

Development of Advanced Coatings for Improved Wear Resistance and Thermal Stability Presents Market Opportunities

Ongoing innovation in tool coating technologies is unlocking new possibilities for carbide tool performance across challenging machining environments. Advanced coatings such as titanium aluminum nitride (TiAlN), aluminum chromium nitride (AlCrN), and diamond-like carbon (DLC) are improving surface hardness, reducing friction, and enhancing resistance to oxidation at high cutting speeds. These coatings allow carbide tools to operate in dry machining conditions, resist built-up edge formation, and extend tool life significantly, especially when machining hard alloys, abrasive composites, or hardened steels. Additionally, multilayer nano-coatings are being developed to optimize adhesion, heat dissipation, and anti-corrosive performance. These innovations are expanding their applicability into aerospace engine part production, hardened mold manufacturing, and energy component fabrication. As demand grows for faster throughput and higher tolerance machining across diverse sectors, manufacturers are increasingly opting for coated carbide solutions.

- For instance, in August 2024, YG-1 introduced the Solid Carbide Dream Drill X with advanced RCH-Coating technology. The coating combines features of TiAlN and AlCrN into a new ‘Nano Layered Multilayer’ coating, which offers benefits like wear resistance, high heat endurance, chipping protection and increased shelf-life. Additionally, the drill includes a universal point grinding, radius thinning and tailored flute design for an elevated performance.

This technological advancement is opening lucrative carbide tools market opportunities driven by material-specific growth and performance optimization.

Carbide Tools Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into cutting tools, drills, end mills, inserts, reamers, taps, and others.

The cutting tools segment accounted for the largest carbide tools market share in 2024.

- Carbide cutting tools, including turning tools, milling cutters, and saw blades, are widely used in metalworking for their durability and high precision.

- These tools offer superior performance in high-speed cutting applications, which is essential for industries like automotive and aerospace.

- The increasing requirement for high-quality finishes and tight tolerances is pushing adoption in sectors where precision is critical.

- As per the carbide tools market analysis, cutting tools maintain their leadership due to their broad applicability and robust performance across multiple industries.

The end mills segment is projected to witness the fastest CAGR during the forecast period.

- End mills are used in machining and shaping operations for various materials, including metals, plastics, and composites.

- These tools are favored in industries like automotive, aerospace, and industrial manufacturing, where complex geometries are required.

- New developments in carbide coatings and designs to enhance tool life and performance under extreme cutting conditions are driving segment growth.

- For instance, in October 2024, Kennametal launched new products, HARVI™ II TE 5-flute solid end mills and the GOmill™ PRO metric 4-flute solid carbide end mills. They offer better productivity and longer shelf life, as well as better vibration control and smoother cutting.

- According to the carbide tools market trends, the need for end mills in precision milling operations is increasing, leading to rapid growth in this subsegment.

By Material:

Based on material, the carbide tools market is segmented into solid carbide, carbide-tipped, carbide-coated, and others.

The solid carbide segment held the largest revenue share in 2024.

- Solid ones are known for their hardness, wear resistance, and superior performance in high-temperature applications, making them ideal for industries like automotive and aerospace.

- These tools are typically used for machining hardened metals, high-strength alloys, and other challenging materials.

- Solid tools have a longer lifespan and maintain sharpness under extreme conditions, which is why they remain in high demand for precision applications.

- As per the carbide tools market analysis, solid carbide continues to dominate due to its unparalleled cutting capabilities and long-lasting durability.

The carbide-tipped segment is expected to experience the fastest CAGR during the forecast period.

- Carbide-tipped tools combine the strength of steel with the hardness of carbide, making them ideal for machining tough materials at lower costs compared to solid carbide tools.

- These tools are widely used in the woodworking and general manufacturing industries due to their versatility and cost-efficiency.

- For instance, in September 2020, Drillco launched carbide-tipped annular cutters that offer users extended shelf life, faster operation speeds and a universal shank to fit most magnetic drilling machines.

- Furthermore, their popularity in low-to-medium intensity machining operations ensures continued carbide tools market growth in regions requiring both performance and affordability.

By Fabrication:

Based on fabrication, the market is divided into coated and uncoated.

The coated segment accounted for the largest carbide tools market share in 2024.

- Coated tools are extensively used for high-performance machining applications due to the enhanced surface properties of the coatings, which reduce wear and increase heat resistance.

- Coatings like TiN, TiAlN, and diamond are commonly applied to improve tool life and cutting efficiency, especially in heavy-duty industries like automotive and aerospace.

- The adoption of coated tools is expanding due to their ability to handle aggressive cutting speeds and prolonged operational hours.

- Thus, the increasing focus on improving productivity and tool longevity drives this segment’s growth and the carbide tools market demand.

The uncoated segment is expected to grow steadily, with applications in low-intensity operations.

- Uncoated tools are widely used in applications that involve lower speeds and non-abrasive materials, such as general-purpose milling, turning, and drilling.

- They are less expensive than coated tools, making them a preferred option in industries where cost is a significant factor.

- While they are less durable than their coated counterparts, their price-to-performance ratio drives steady need in specific applications.

- As per carbide tools market trends, the uncoated segment remains relevant in cost-sensitive markets while maintaining stable requirement.

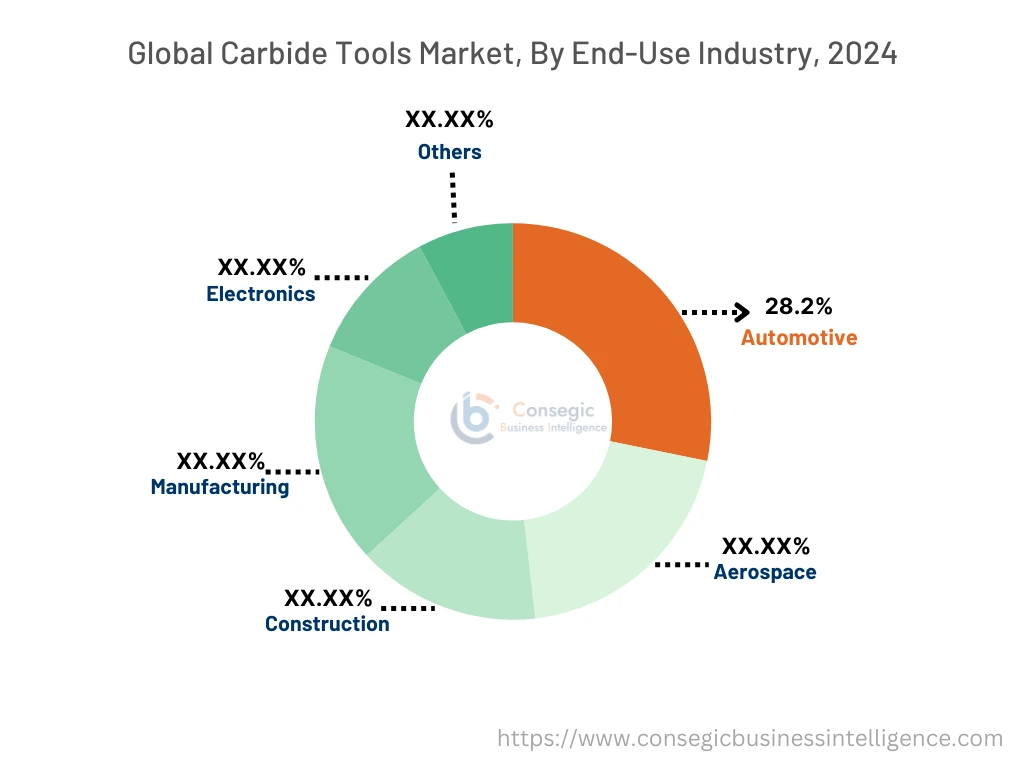

By End-Use Industry:

Based on end-use industry, the carbide tools market is segmented into automotive, aerospace, construction, manufacturing, electronics, and others.

The automotive segment held the largest revenue share of 28.2% in 2024.

- They play a crucial role in automotive manufacturing, particularly in engine component machining, transmission parts, and braking systems, where precision is paramount.

- The shift toward lightweight, high-performance materials in modern vehicles is increasing the need for high-quality tools that can work with tough alloys.

- As the automotive industry increasingly adopts automation and robotics, its requirement in mass production lines is expected to rise.

- Hence, the automotive sector remains the dominant force due to the constant need for high-precision, durable components, driving the carbide tools market expansion.

The aerospace segment is projected to grow at the fastest CAGR during the forecast period.

- Aerospace manufacturing requires high-precision machining of tough alloys like titanium and nickel-based superalloys, where carbide tools excel.

- The growth of the aerospace sector, driven by advancements in aircraft design and increasing air travel, fuels the need for specialized cutting tools.

- The need for more efficient fuel systems, lightweight structures, and advanced composites in aerospace applications contributes to its increasing use in this sector.

- Thus, aerospace applications are seeing rapid adoption due to their reliability in the most severe production environments, boosting the carbide tools market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

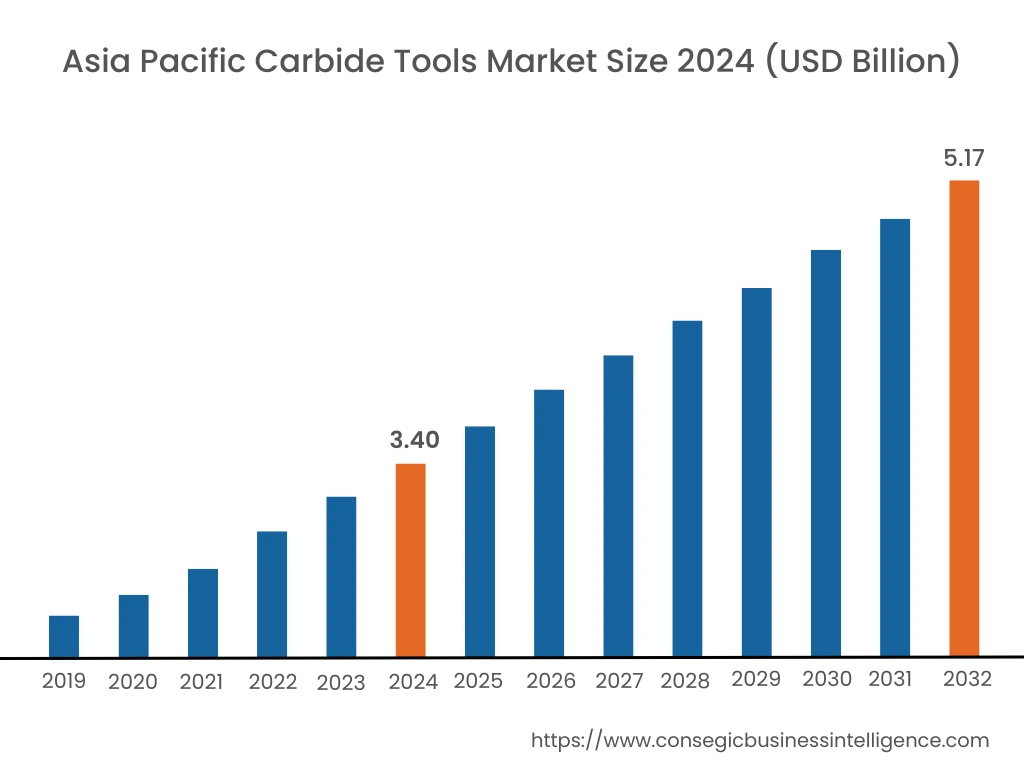

Asia Pacific region was valued at USD 3.40 Billion in 2024. Moreover, it is projected to grow by USD 3.52 Billion in 2025 and reach over USD 5.17 Billion by 2032. Out of this, China accounted for the maximum revenue share of 38.7%. Asia-Pacific is undergoing rapid growth in the carbide tools industry, with an exponential increase in industrial manufacturing, infrastructure, and export-oriented production. In China, Japan, South Korea, and India, their adoption is accelerating due to strong activity in the electronics, automotive, and heavy machinery sectors. Market analysis reveals that regional manufacturers are investing in domestic tooling innovation, including multi-layer coated carbide solutions and high-speed milling systems designed for mass production. Growth is fueled by rising CNC machine penetration, automation in metalworking operations, and the increasing presence of global and regional tool makers offering cost-effective precision tools. Government support for manufacturing upgrades and increasing export competitiveness further strengthens the region’s role in the global market.

North America is estimated to reach over USD 4.74 Billion by 2032 from a value of USD 3.13 Billion in 2024 and is projected to grow by USD 3.24 Billion in 2025. In North America, demand for carbide cutting tools remains strong, particularly in the United States and Canada, where aerospace, automotive, and general engineering sectors require high-precision machining. Market analysis shows that manufacturers are shifting toward coated carbide inserts and end mills with extended tool life and improved heat resistance. The region also emphasizes CNC-integrated tooling systems, driven by advanced manufacturing practices and reshoring efforts in key industrial sectors. Growth in North America is reinforced by ongoing investments in additive-subtractive hybrid machining technologies and government-led initiatives to revitalize domestic production capabilities.

Europe is a well-established and technologically mature market with significant use of carbide-based tooling across aerospace, automotive, defense, and mold-making industries. Countries such as Germany, Italy, France, and the UK are adopting next-generation tools engineered for high-speed machining, micro-milling, and complex geometries. Market analysis indicates growing need for application-specific tools that reduce cycle times and material waste, especially in precision component manufacturing. The carbide tools market opportunity in Europe is closely tied to digital manufacturing trends, environmental compliance in production lines, and the expansion of Industry 4.0 frameworks that support process optimization through advanced tooling integration.

Latin America is gradually expanding its use of advanced cutting tools, with activity centered in Brazil, Mexico, and Argentina. The automotive and oil & gas industries remain the primary consumers, while secondary need is emerging from aerospace parts suppliers and infrastructure-related fabrication. Market analysis highlights that although high-end carbide tools are less widespread, increasing awareness of their durability and efficiency is shifting buyer preferences away from traditional HSS tools. Furthermore, improving access to quality tools, expanding local technical support, and addressing skill gaps through training programs and partnerships with global tooling manufacturers are key avenues for development in this region.

The Middle East and Africa present a developing landscape for carbide tool usage, driven by industrial diversification, infrastructure development, and growing requirements for precision components. In the UAE, Saudi Arabia, and South Africa, carbide tool deployment is gaining traction in metal fabrication, energy infrastructure, and equipment maintenance sectors. Market analysis indicates a gradual move toward modern machining practices in workshops and mid-sized manufacturing facilities. Though market penetration is still low in many parts of the region, growth is expected through increased localization of manufacturing, rising investment in vocational training, and support for non-oil industrial growth strategies.

Top Key Players and Market Share Insights:

The carbide tools market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global carbide tools market. Key players in the carbide tools industry include -

- Sandvik AB (Sweden)

- ISCAR Ltd. (Israel)

- Kennametal Inc. (USA)

- Mitsubishi Materials Corporation (Japan)

- Sumitomo Electric Industries, Ltd. (Japan)

- Guhring GmbH (Germany)

- Zhuzhou Cemented Carbide Cutting Tools Co., Ltd. (ZCCCT) (China)

- YG-1 Co., Ltd. (South Korea)

- Walter AG (Germany)

- CeramTec GmbH (Germany)

Recent Industry Developments :

Acquisitions:

- In December 2021, GWS Tool Group acquired Carbide Tools Mfg. Inc. This acquisition increases the capability and capacity for GWS in custom tools and expands its manufacturing footprint in the upper Midwest region of the United States. This decision also increases customer exposure and fuels future growth.

Carbide Tools Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 17.45 Billion |

| CAGR (2025-2032) | 5.3% |

| By Product Type |

|

| By Material |

|

| By Fabrication |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Carbide Tools Market? +

Carbide Tools Market size is estimated to reach over USD 17.45 Billion by 2032 from a value of USD 11.58 Billion in 2024 and is projected to grow by USD 11.98 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

What specific segmentation details are covered in the Carbide Tools Market report? +

The Carbide Tools market report includes specific segmentation details for product type, material, fabrication and end-use industry.

What are the end-use industries of the Carbide Tools Market? +

The end-use industries of the Carbide Tools Market are automotive, aerospace, construction, manufacturing, electronics, and others.

Who are the major players in the Carbide Tools Market? +

The key participants in the Carbide Tools market are Sandvik AB (Sweden), ISCAR Ltd. (Israel), Kennametal Inc. (USA), Mitsubishi Materials Corporation (Japan), Sumitomo Electric Industries, Ltd. (Japan), Guhring GmbH (Germany), Zhuzhou Cemented Carbide Cutting Tools Co., Ltd. (ZCCCT) (China), YG-1 Co., Ltd. (South Korea), Walter AG (Germany) and CeramTec GmbH (Germany).