- Summary

- Table Of Content

- Methodology

Bulk Chemical Market Size:

Bulk Chemical Market size is estimated to reach over USD 802.30 Billion by 2032 from a value of USD 619.48 Billion in 2024 and is projected to grow by USD 629.06 Billion in 2025, growing at a CAGR of 3.4% from 2025 to 2032.

Bulk Chemical Market Scope & Overview:

Bulk chemical refers to large-volume industrial chemicals used as raw materials in manufacturing, processing and numerous industrial applications. These chemicals serve as essential components in producing plastics, pharmaceuticals, agrochemicals, textiles, and construction materials. They are categorized into organic and inorganic compounds, each offering distinct properties for different production requirements.

Key features include high purity, standardized formulations and large-scale availability to meet industrial requirements. These chemicals facilitate efficient manufacturing processes, enhance product performance, and support large-scale production across multiple sectors. Their compatibility with automated handling and transportation systems ensures seamless integration into supply chains.

Sectors such as automotive, electronics, and packaging utilize these chemicals for coatings, adhesives, and specialized formulations. Advances in chemical processing and distribution technologies continue to enhance efficiency, ensuring consistent quality and reliability in large-scale applications.

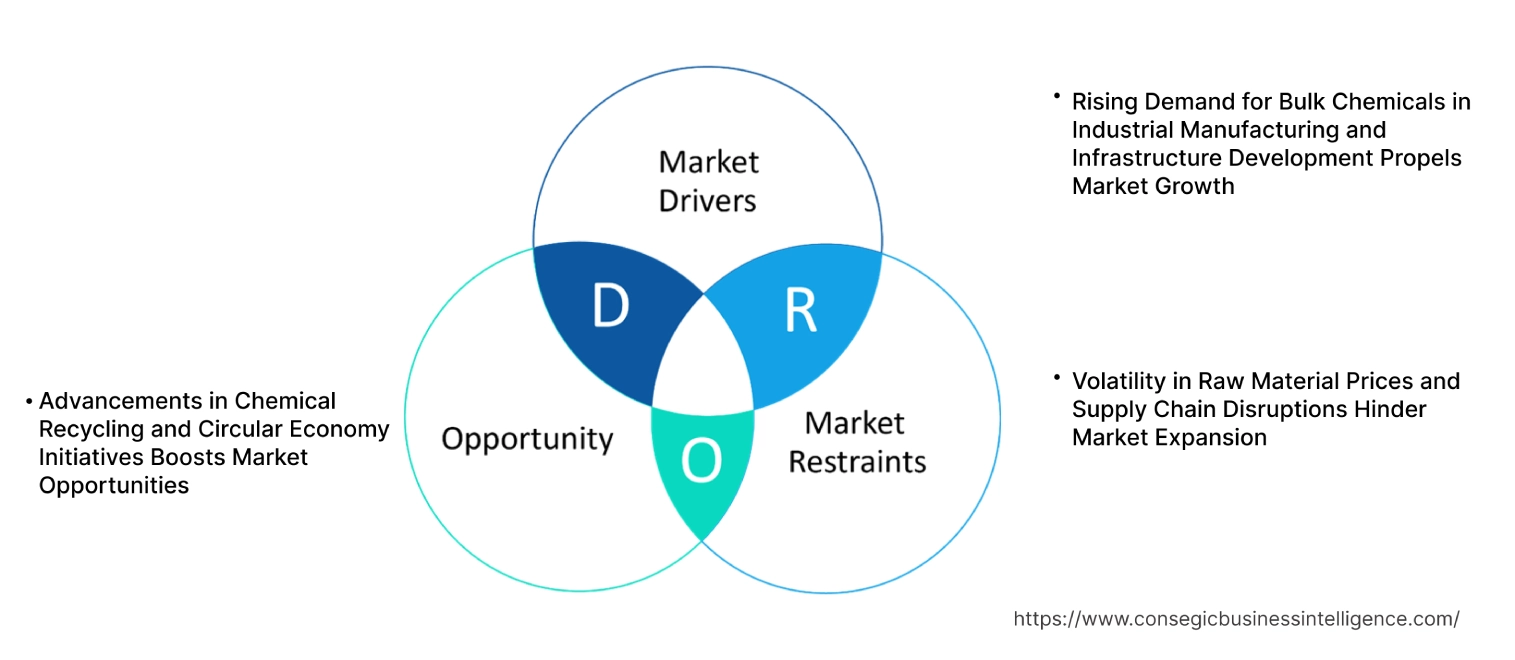

Bulk Chemical Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Bulk Chemicals in Industrial Manufacturing and Infrastructure Development Propels Market Growth

Bulk chemicals serve as essential raw materials in industries such as construction, automotive, packaging and textiles, playing a crucial role in coatings, adhesives, plastics, and synthetic fibers. Rapid urbanization, industrialization, and government investments in large-scale infrastructure projects are further fueling the use of bulk chemicals. The construction sector utilizes cement additives, waterproofing agents, and insulation materials, while the automotive field requires high-performance coatings, lubricants, and polymers. Additionally, the increasing production of electronics, pharmaceuticals, and agrochemicals drives consistent chemical demand. As industries seek cost-effective, high-volume chemical solutions, manufacturers are expanding production capacities to meet market needs.

- For instance, according to the Council of Scientific & Industrial Research (CSIR), India, the Indian chemical sector is one of the strategic industrial sectors in the country, contributing nearly 2.51% of the GDP and 15.95% of the country’s manufacturing sector GDP. With the Indian manufacturing sector is poised to reach US$ 1 trillion by 2025-26, the demand for chemicals also increases, resulting in higher international trade.

With ongoing technological advancements, sustainable production methods, and global trade expansion, the sector is expected to witness significant bulk chemical market expansion, reinforcing its critical role in modern industrial supply chains.

Key Restraints:

Volatility in Raw Material Prices and Supply Chain Disruptions Hinder Market Expansion

The demand for cost-effective and high-volume chemicals is increasing, but reliance on crude oil, natural gas, and mined minerals makes production vulnerable to price volatility and geopolitical risks. Changes in global oil prices, trade restrictions, and transportation disruptions directly impact manufacturing costs, leading to profit margin fluctuations for producers. Additionally, supply chain disruptions caused by logistics bottlenecks, labor shortages, and regulatory changes are delaying production timelines and increasing operational expenses. Many chemical manufacturers are investing in alternative sourcing strategies, process optimization, and digital supply chain management to mitigate these risks. However, the unpredictability of market conditions and raw material availability remains a key restraint. Addressing these challenges through strategic partnerships, localized production, and inventory management solutions will be essential for ensuring bulk chemical market growth in the long run.

Future Opportunities :

Advancements in Chemical Recycling and Circular Economy Initiatives Boosts Market Opportunities

As industries focus on reducing waste, improving energy efficiency, and lowering carbon emissions, chemical manufacturers are developing innovative recycling technologies to recover valuable raw materials from plastic waste, industrial byproducts, and chemical residues. The growth of circular economy practices is leading to increased investment in closed-loop production systems, bio-based feedstocks, and advanced purification methods to enhance chemical reusability. Governments and regulatory bodies are also promoting eco-friendly manufacturing processes, extended producer responsibility programs, and waste reduction mandates, creating new opportunities for sustainable chemical solutions. Additionally, partnerships between chemical producers, waste management firms, and end-user industries are accelerating the adoption of recyclable and biodegradable chemical alternatives.

- For instance, the European Commission’s Circular Economy Action Plan (CEAP), adopted in March 2020, outlines Europe’s agenda for sustainable growth. The chemical industry contributes to this by focusing on recycling and reuse of resources through the use of alternative feedstock as well as by putting circularity as a criterion when designing chemicals and materials for a wide variety of applications.

These innovations are expected to unlock significant bulk chemical market opportunities, supporting the transition toward a more sustainable and environmentally responsible industry.

Bulk Chemical Market Segmental Analysis :

By Product Type:

By product type, the market is segmented into organic and inorganic chemicals.

The organic chemicals segment held the largest bulk chemical market share in 2024.

- Organic chemicals include alcohols, aldehydes, ketones, acids and hydrocarbons. They play a crucial role in multiple industrial processes, specifically in pharmaceuticals, food processing, and automotive applications.

- The need for bio-based and sustainable organic chemicals is increasing due to environmental regulations and consumer preferences for eco-friendly solutions.

- Segmental analysis suggests that advancements in green chemistry are altering its production, improving efficiency and reducing waste.

- Bulk chemical market trends indicate that manufacturers are increasing their product portfolios, to cater to the expanding needs of sectors such as healthcare and agriculture.

The inorganic chemicals segment is anticipated to experience the fastest CAGR during the forecast period.

- Inorganic chemicals refer to acids, bases, salts and metals. They are widely used in water treatment, metallurgy and construction industries, making them essential for large-scale industrial applications.

- The need for high-purity chemicals is rising, particularly in semiconductors, mining, and infrastructure development.

- Market trends suggest that increased investments in industrial expansion and resource processing are fueling the growth of inorganic chemical consumption.

- With innovations in chemical processing and recycling technologies, this segment is contributing to bulk chemical market growth.

By End-Use Industry:

By end-use industry, the market is segmented into pharmaceuticals & healthcare, agriculture & fertilizers, construction & infrastructure, automotive & transportation, food & beverage processing, textiles & dyes, oil & gas, electronics & semiconductors, mining & metallurgy, and water treatment.

The pharmaceuticals & healthcare segment held the largest share in 2024.

- They are extensively used in drug formulation, medical devices, and laboratory research, making them integral to the healthcare sector.

- The need for high-purity chemicals is increasing as pharmaceutical companies focus on stringent quality standards and regulatory compliance.

- Bulk chemical market analysis highlights the growing role of specialty chemicals in biopharmaceuticals, diagnostics and medical formulations.

- For instance, the Indian pharmaceuticals sector is expected to reach US$ 65 billion by 2024, US$ 130 billion by 2030 and US$ 450 billion market by 2047 according to IBEF. This increase is anticipated to drive the bulk chemical market as well.

- Segmental trends indicate that the rising need for active pharmaceutical ingredients (APIs) and excipients is driving growth in the pharmaceutical sector.

The construction & infrastructure segment is expected to have the fastest CAGR during the forecast period.

- Chemicals such as cement additives, sealants, adhesives, and coatings play an important role in modern construction materials.

- The need for high-performance chemicals in infrastructure development is rising, particularly in emerging economies investing in urbanization and industrial projects.

- Market trends highlight the increasing use of advanced chemical formulations, improving building durability and energy efficiency.

- With infrastructure expansion continuing worldwide, this segment is a key contributor to bulk chemical market expansion.

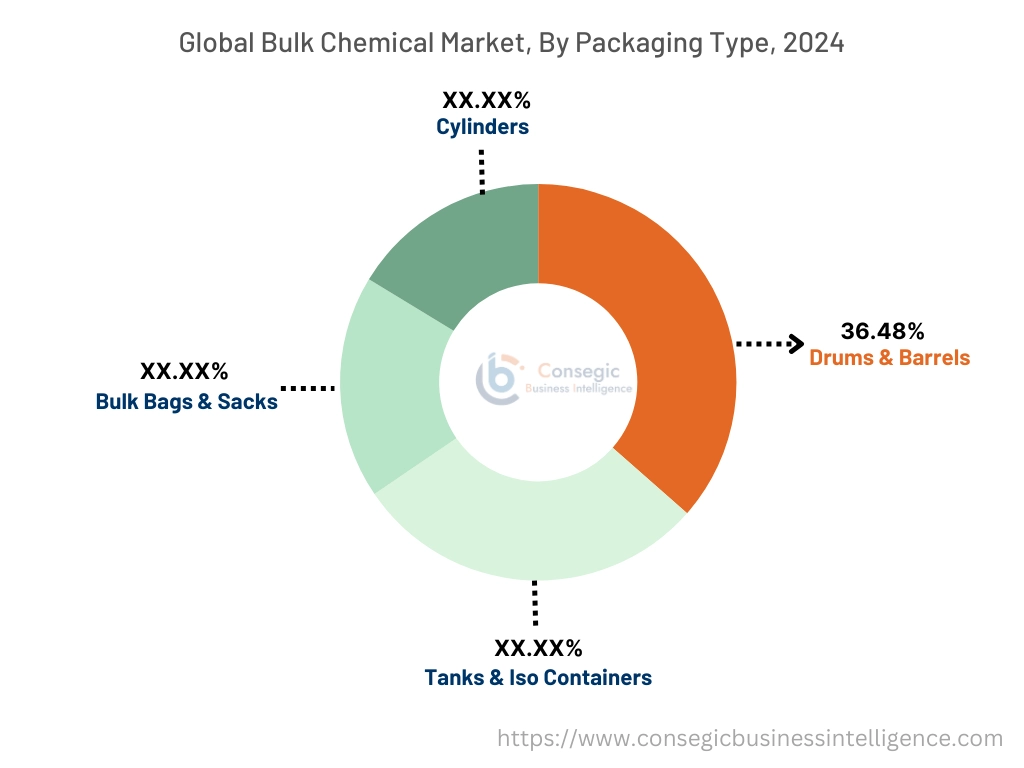

By Packaging Type:

Based on packaging type, the market is segmented into drums & barrels, tanks & iso containers, bulk bags & sacks, and cylinders.

The drums & barrels segment held the largest bulk chemical market share of 36.48% in 2024.

- Drums and barrels are the most commonly used packaging solutions for transporting bulk chemicals, ensuring safe storage and handling.

- The need for reliable, spill-resistant chemical storage solutions is increasing in industrial manufacturing and logistics.

- Bulk chemical market analysis suggests that improved barrel materials and coatings are enhancing chemical stability and extending shelf life.

- Segmental trends indicate that regulatory mandates on hazardous chemical transportation drive innovations in safety features.

The tanks & ISO containers segment is expected to experience the fastest CAGR during the forecast period.

- ISO containers and bulk tanks are increasingly being used for large-scale international chemical shipments as they provide secure and cost-efficient transportation.

- The need for flexible and reusable chemical storage solutions is rising, particularly in oil & gas, petrochemicals and high-volume chemical industries.

- Bulk chemical market trends suggest that advanced container tracking and automation technologies are improving the logistics efficiency of bulk chemical distribution.

- With rising global trade in chemicals, this segment is expected to contribute significantly to market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

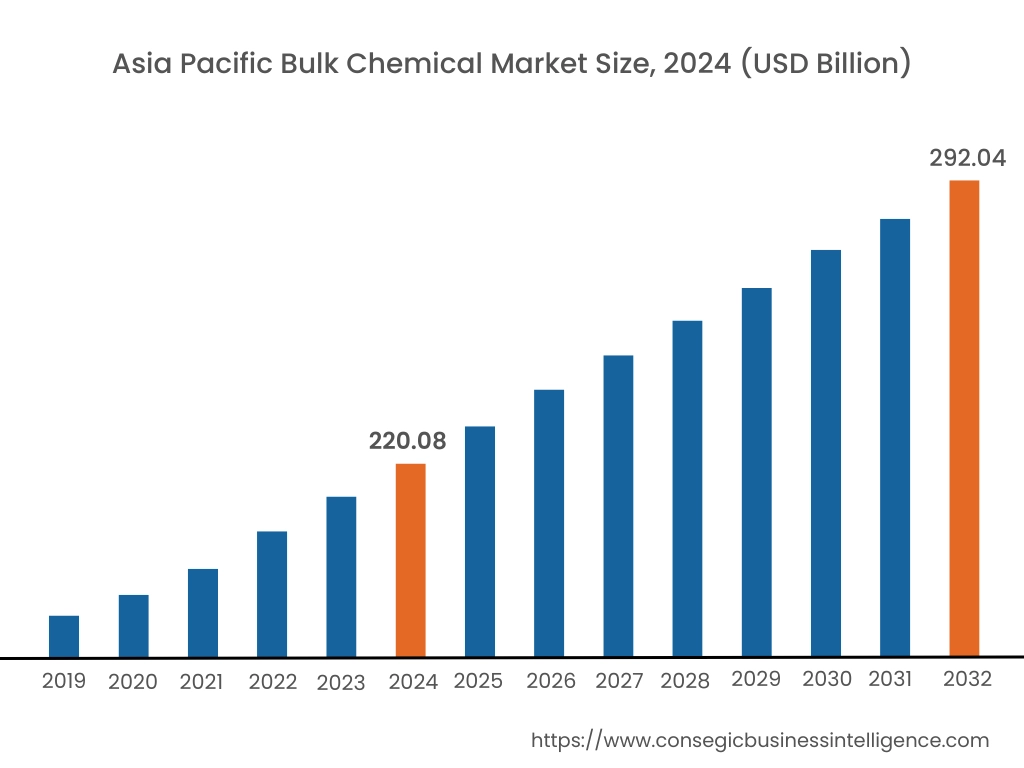

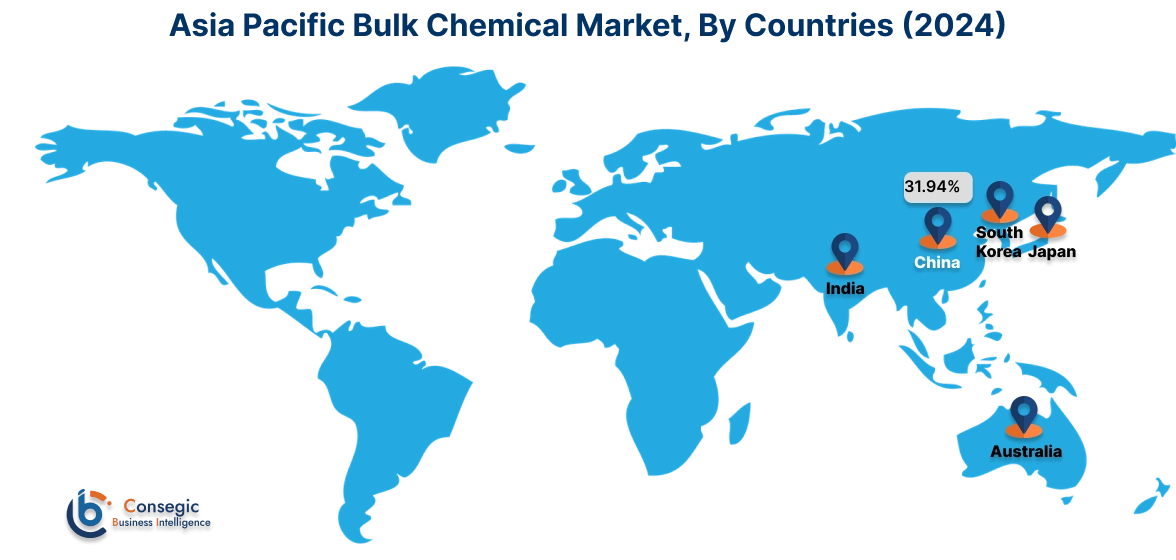

Asia Pacific region was valued at USD 220.08 Billion in 2024. Moreover, it is projected to grow by USD 223.94 Billion in 2025 and reach over USD 292.04 Billion by 2032. Out of this, China accounted for the maximum revenue share of 31.94%. Asia-Pacific stands as a dominant force in the bulk chemical market, primarily due to rapid industrialization and expanding manufacturing sectors in countries like China, India, and Japan. China, in particular, has significantly increased its production capacity, leading to a global oversupply and impacting profit margins. This expansion presents a substantial bulk chemical market opportunity for companies aiming to capitalize on the region's demand.

North America is estimated to reach over USD 214.70 Billion by 2032 from a value of USD 167.91 Billion in 2024 and is projected to grow by USD 170.32 Billion in 2025. In North America, the market is bolstered by robust industrial infrastructure and technological advancements in chemical manufacturing. The United States, especially, benefits from an abundant supply of domestic feedstocks derived from natural gas liquids, providing a competitive edge in production costs. The region's focus on innovation and sustainability further amplifies the bulk chemical market demand, particularly in sectors like pharmaceuticals and agriculture.

Europe exhibits a mature bulk chemical market, supported by a well-established industrial base and stringent environmental regulations. However, the region faces challenges due to high energy costs and increased competition from Asia-Pacific producers. This has led to consolidation efforts and a shift towards sustainable and specialized chemical production to maintain competitiveness. The emphasis on green technologies and circular economy initiatives presents opportunities for innovation within the market.

Latin America's bulk chemical market is gradually gaining traction, influenced by economic development and growth in the agriculture and construction sectors. Countries like Brazil and Mexico are investing in expanding their chemical production capacities to meet domestic demand and explore export opportunities. The region's abundant natural resources provide a favorable environment for the bulk chemical industry, with potential for expansion as infrastructure and industrial activities continue to develop.

The Middle East and Africa are emerging markets for bulk chemicals, with growth potential linked to the development of oil and gas industries and increasing industrialization. The Middle East, in particular, has seen investments in petrochemical facilities to leverage its hydrocarbon resources. However, the region faces challenges such as geopolitical tensions and fluctuating oil prices, which can impact market stability. Despite these challenges, the focus on diversifying economies and developing downstream industries offers prospects for market expansion.

Top Key Players and Market Share Insights:

The bulk chemical market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global bulk chemical market. Key players in the bulk chemical industry include -

- BASF SE (Germany)

- Sinopec (China)

- Saudi Basic Industries Corporation (SABIC) (Saudi Arabia)

- INEOS Group Ltd. (UK)

- Formosa Plastics Corporation (Taiwan)

- Linde plc (Ireland/UK)

- LG Chem Ltd. (South Korea)

- Mitsubishi Chemical Corporation (Japan)

- Grupa Azoty (Poland)

- Brenntag SE (Germany)

Recent Industry Developments :

Partnerships:

- In February 2025, SABIC collaborated with Branch Technology to develop lightweight panels to restore the exterior of the Pathfinder, an early test article for the National Aeronautics & Space Administration (NASA) space shuttle orbiter.

Bulk Chemical Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 802.30 Billion |

| CAGR (2025-2032) | 3.4% |

| By Product Type |

|

| By End-Use Industry |

|

| By Packaging Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Bulk Chemical Market? +

Bulk Chemical Market size is estimated to reach over USD 802.30 Billion by 2032 from a value of USD 619.48 Billion in 2024 and is projected to grow by USD 629.06 Billion in 2025, growing at a CAGR of 3.4% from 2025 to 2032.

What specific segmentation details are covered in the Bulk Chemical Market report? +

The Bulk Chemical market report includes specific segmentation details for product type, packaging type and end-use industry.

What are the end-use industries in the Bulk Chemical Market? +

The end-use industries in the Bulk Chemical market are pharmaceuticals & healthcare, agriculture & fertilizers, construction & infrastructure, automotive & transportation, food & beverage processing, textiles & dyes, oil & gas, electronics & semiconductors, mining & metallurgy and water treatment.

Who are the major players in the Bulk Chemical Market? +

The key participants in the Bulk Chemical market are BASF SE (Germany), Sinopec (China), Saudi Basic Industries Corporation (SABIC) (Saudi Arabia), INEOS Group Ltd. (UK), Formosa Plastics Corporation (Taiwan), Linde plc (Ireland/UK), LG Chem Ltd. (South Korea), Mitsubishi Chemical Corporation (Japan), Grupa Azoty (Poland) and Brenntag SE (Germany).