- Summary

- Table Of Content

- Methodology

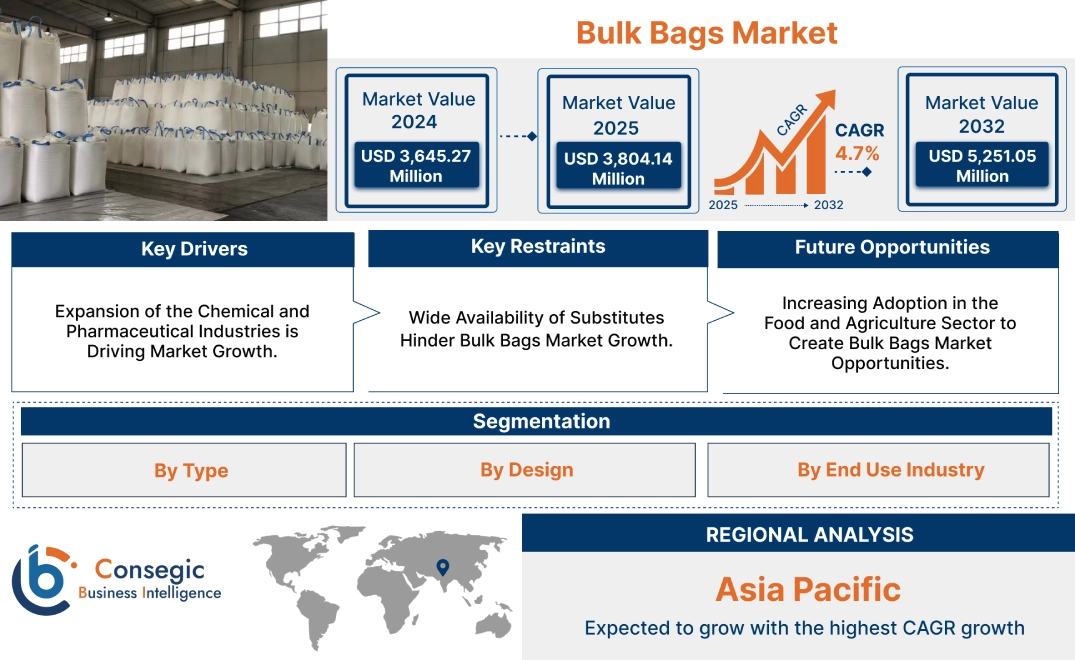

Bulk Bags Market Size:

The Bulk Bags Market size is growing with a CAGR of 4.7% during the forecast period (2025-2032), and the market is projected to be valued at USD 5,251.05 Million by 2032 from USD 3,645.27 Million in 2024. Additionally, the market value for 2025 attributes to USD 3,804.14 Million.

Bulk Bags Market Scope & Overview:

Bulk bags are also known as flexible intermediate bulk containers (FIBCs). They are large, flexible containers designed for efficient storage and transportation amongst others. These bags are made of made in different designs. A few of these designs include u-panel bags, four-side panel bags, baffle bags, and others. These bags are also capable of holding substantial quantities from hundreds of kilograms to several tons. They are commonly used in agriculture for grains and fertilizers, construction for materials like sand and cement, chemicals, food products like sugar and flour, and mining for ores amongst others. Bulk bags offer a cost-effective and easily handled packaging solution.

Bulk Bags Market Dynamics - (DRO) :

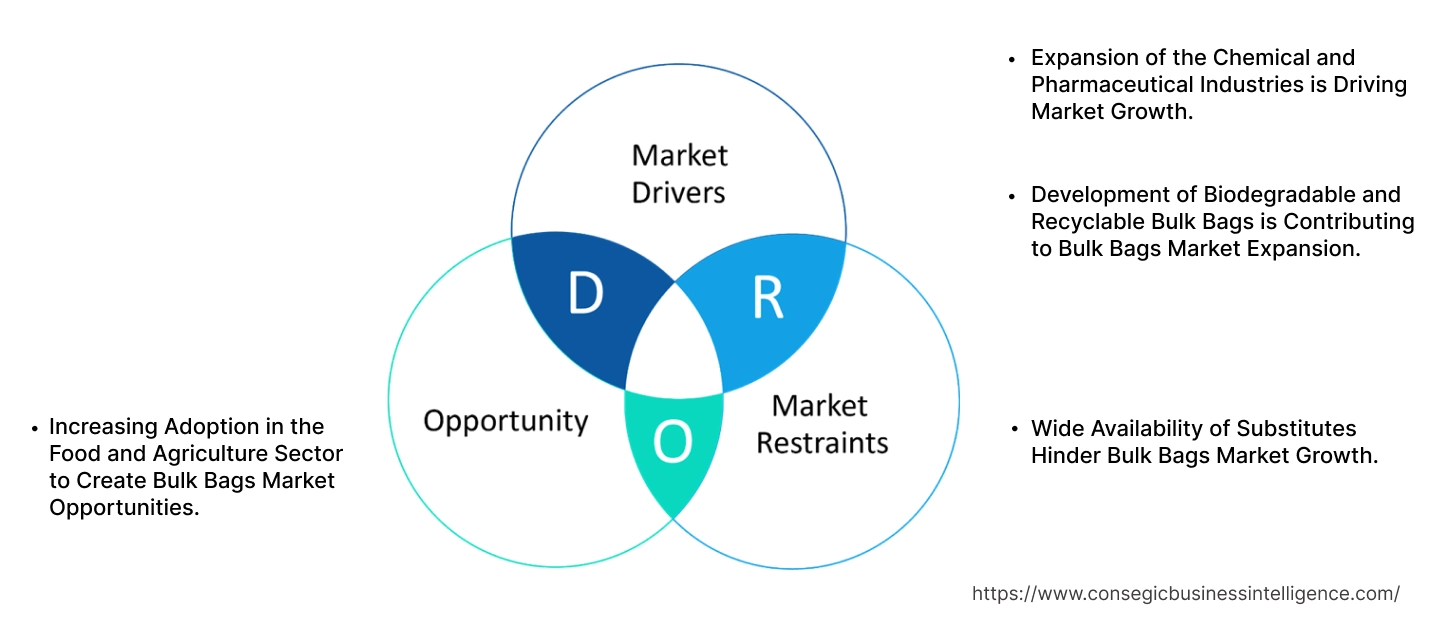

Key Drivers:

Expansion of the Chemical and Pharmaceutical Industries is Driving Market Growth.

Chemical and pharmaceutical sectors depend on bulk bags for the efficient and compliant handling of raw materials. Raw materials include powders or granules, used in manufacturing. Furthermore, many finished or semi-finished chemical and pharmaceutical products are packaged and shipped in these bags.

- For instance, according to American Chemical Chemistry Council (ACC), the demand of chemicals has grown by 3.4% in 2024 compared to the prior year.

Moreover, to meet the stringent regulations, bulk bags are customized by including features such as liners as they provide safety and compliance. The cost-effectiveness nature of these bags compared to other packaging options make them a preferred choice. Thus, the growing requirement for these bags in storing and transporting chemicals and pharmaceuticals products is contributing to the bulk bags market demand.

Development of Biodegradable and Recyclable Bulk Bags is Contributing to Bulk Bags Market Expansion.

The need for biodegradable and recyclable bulk bags is driven by growing environmental awareness among consumers and businesses. In addition to this, there has been an increase in stringent regulations regarding plastic waste leading to the need for eco-friendly packaging solutions. Technological advancements in materials science have enabled the creation of durable, biodegradable, and recyclable polymers suitable for manufacturing of these bags.

- For instance, in 2023, FlexSack introduced FlexSack-eco. It is an ecofriendly bulk bag that is produced from polypropylene. It contains 30% of recycled polypropylene.

In addition to this the rise in the willingness of consumers to pay a premium for sustainably packaged goods is contributing to market. Thus, as the focus on sustainability increases the need for eco-friendly bulk bags is also increasing.

Key Restraints:

Wide Availability of Substitutes Hinder Bulk Bags Market Growth.

The wide availability of alternative packaging and material handling solutions such as woven sacks and paper bags, amongst others are restraining market. They create direct competition leading to a change in preference of consumers based on factors such as cost and material compatibility. Additionally, price sensitivity is also a major factor contributing to the hinderance of market trajectory, especially in developing economies as some alternatives offering lower costs. Furthermore, certain materials or applications have better usage by substitutes, and existing infrastructure designed for other packaging types creates a barrier to bulk bag adoption. Hence, the aforementioned factors are restraining bulk bags market growth.

Future Opportunities :

Increasing Adoption in the Food and Agriculture Sector to Create Bulk Bags Market Opportunities.

The increase in adoption of bulk bags within the food and agriculture sector as they offer a efficient method for handling large quantities of agricultural products is contributing to market trajectory. A few of these agricultural products include grains, seeds, fertilizers, and animal feed and these bags offer storage, transport amongst others.

- For instance, according to the Union Budget 2024-2025 of India, an investment of roughly USD 18 Billion is made for agriculture and allied areas including the focus on manufacturing of bilk bags in this sector.

Moreover, their ease of use in loading, unloading, and transport, often with forklifts, streamline operations and reduces labor costs. Hence, the above-mentioned factors together contribute to creating lucrative bulk bags market opportunities over the forecast period.

Bulk Bags Market Segmental Analysis :

By Type:

Based on Type, the market is categorized into type A, type B, type C and type D

Trends in Type:

- Type A bags are preferred due to their cost-effective nature along with their wide usage for material of non-hazardous nature.

- The properties of Type C bags such as superior static dissipative are contributing to their popularity.

The Type A segment accounted for the largest bulk bags market share in 2024.

- Type A bulk bags represent the most basic form of FIBCs, constructed from woven polypropylene without any inherent static dissipative properties.

- These bags are widely used for packaging and transporting non-hazardous materials where the buildup and discharge of static electricity poses no risk.

- For instance, in 2024, the amount of non-hazardous waste generated by Roche attributed to 29,179 tons. Type A bags are incorporated by Roche for packaging and transporting purposes of these waste

- They are cost-effective in nature, making them an economical choice for applications where static control is not a critical concern.

- Stricter safety regulations and a growing awareness associated with static electricity are contributing to the segment trajectory.

- As a result, based on the bulk bags market analysis, the type A of segment is dominating the bulk bags market demand.

The Type C segment is expected to be the fastest growing segment over the forecast period.

- The Type C segment of the bulk bags offer superior static dissipation, important for preventing ignition and explosions when handling flammable materials.

- This makes them a suitable option for sectors dealing with combustible dust or explosive atmospheres.

- In addition to this, the increase in stringent safety regulations across various sectors is making mandatory use of such protective measures, further driving adoption.

- Technological advancements in fabric and manufacturing processes are contributing to further usage in sectors such as chemicals and pharmaceuticals.

- Therefore, as per bulk bags market analysis and trends, the type C segment is expected to be lucrative over the forecast period.

By Design:

The Design segment is categorized into u-panel bags, four-side panel bag, baffle bags, and others

Trends in Design:

- U-panel bags are a popular choice due to their simplicity and cost-effectiveness.

- Baffle bags are experiencing popularity due to their superior shape retention and efficient space utilization.

The U-panel segments accounted for the largest market share in 2024.

- U-panel bags contribute to the largest share due to their suitability for a broad variety of materials, from agricultural goods to construction supplies and chemicals, which makes them a popular choice.

- For instance, in India, the export for Agri & allied product experienced a growth of 4% during 2022-2023 compared to previous year. Bulks bags were observed to be one of the most widely used packaging options for these exports.

- The U-panel design contributes to lower manufacturing costs, making them an attractive option for high-volume users.

- Furthermore, established manufacturing and supply chains ensure readily available supply and competitive pricing for these bags.

- Thus, as per the market analysis, due to the above-mentioned factors, the U-panel segment is dominating the bulk bags market trends.

The Baffle Bags segment is expected to be the fastest growing segment over the forecast period.

- The baffle bag consisting of fabric panels sewn across the bag's corners, allows for superior shape retention when filled. This helps in maximizing storage space.

- Baffle bags also offer enhanced stability during handling, minimizing the risk of tipping and product damage. They are well-suited for fine powders.

- With businesses increasingly focusing on efficient logistics, the requirement for space-saving and stable packaging like baffle bags is increasing.

- These combined benefits are together contributing to the segmental growth of the baffle bag segment.

- Therefore, as per analysis and trends, the baffle bags segment is expected to be lucrative over the forecast period.

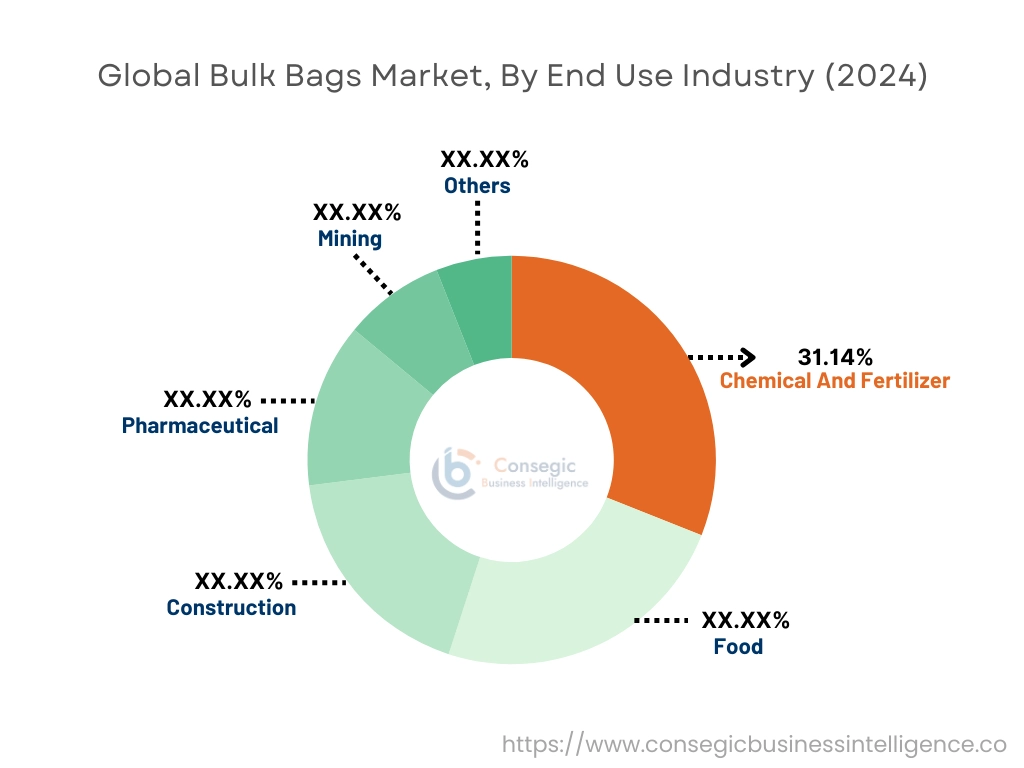

By End Use Industry:

The End Use Industry segment is categorized into chemical and fertilizer, food, construction, pharmaceutical, mining, and others

Trends in the End Use Industry:

- The focus toward specialized bags with features like static control for hazardous chemicals and moisture barriers for sensitive fertilizers is increasing.

- The focus of key manufacturers on hygiene and food safety are leading to a requirement for bags with food-grade liners and certifications.

The Chemical and Fertilizer segments accounted for the largest market share of 31.14% in 2024.

- The chemical and fertilizer sectors handle vast quantities of materials, many well-suited for bulk bag packaging. This has led to an increase in need for these bags.

- They are utilized across their supply chains, from raw material transport to finished product packaging.

- The chemical sector’s need for specialized bags, particularly for hazardous materials requiring features like static control, makes these bags essential.

- For instance, in 2023, according to HWH Environmental, more than 350 million tons of waste of hazardous nature was generated across the globe.

- Thus, as per the market analysis, due to the above-mentioned factors, the chemical and fertilizer segment is dominating the bulk bags market trends.

The Food segment is expected to be the fastest growing segment over the forecast period.

- The rise in global demand for processed and packaged foods requires a need for efficient packaging solutions like bulk bags.

- The food sector’s stringent hygiene and safety standards are readily met by bulk bags manufactured with food-grade liners and certifications contributing to market growth

- Moreover, the increasing use of these bags for transporting and storing food ingredients positively impacts the food processing sector.

- In addition to this, the growing sustainability concerns within the food sector are driving demand for recyclable and biodegradable bulk bag options.

- Therefore, as per trends, the food segment is expected to be lucrative over the forecast period.

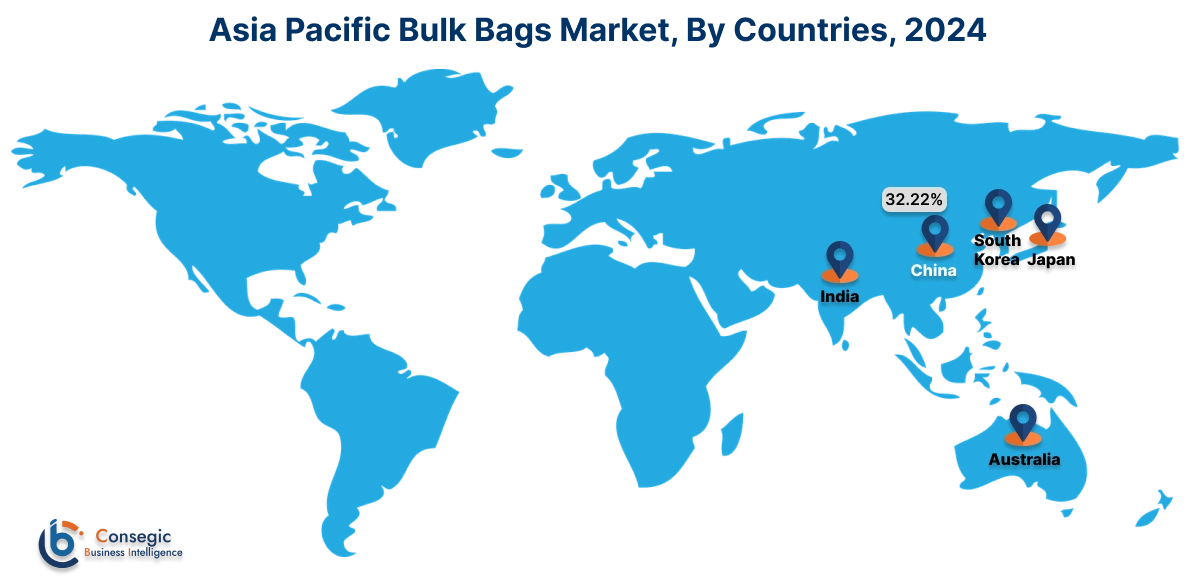

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

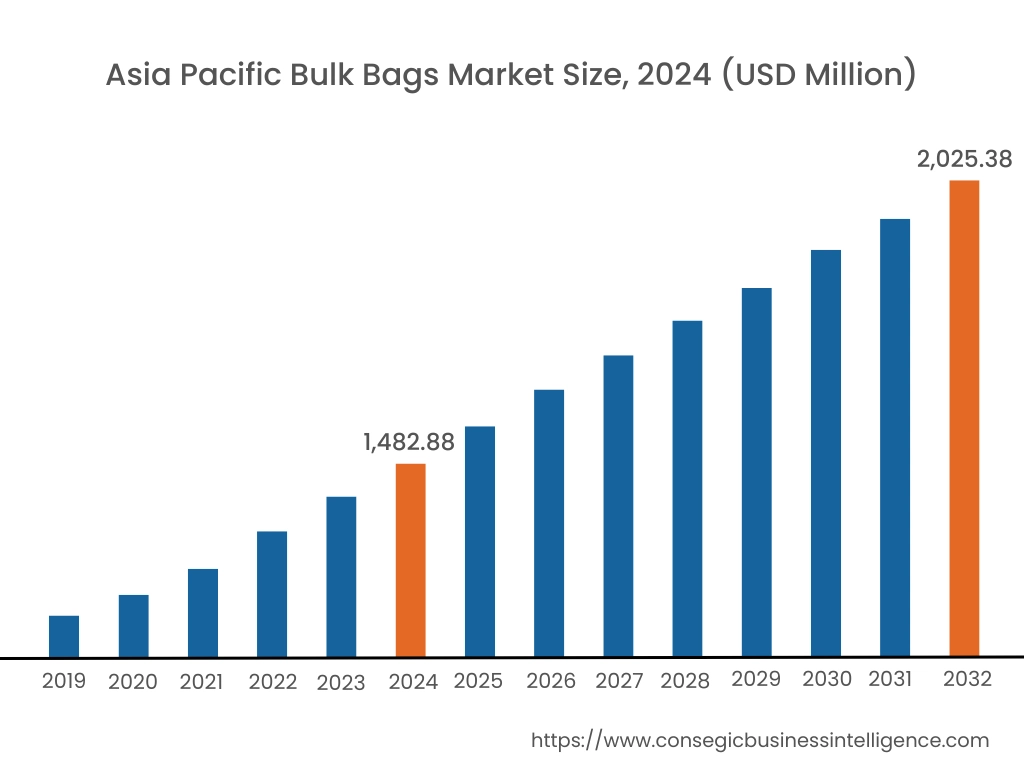

In 2024, Asia Pacific accounted for the highest bulk bags market share of 40.68% and was valued at USD 1,482.88 Million and is expected to reach USD 2,025.38 Million in 2032. In Asia Pacific, China accounted for the market share of 32.22% during the base year of 2024.

The Asia Pacific region contributes to significant manufacturing across the globe particularly in chemical and fertilizer sectors. This has led to an increase in demand for bulk bags as a packaging solution. Major players like China, India, Japan, and South Korea, with their large chemical and pharmaceutical sectors, rely heavily on these bags for handling raw materials, intermediate products, and finished goods.

- For instance, according to a chemical industry journal, Asia Pacific contributes to more than 40% towards the global chemical sector’s economic value.

Furthermore, the region's role as a major exporter of these products requires bulk bags for safe and efficient international transport. Thus, as per the market analysis, due to these factors, the requirement for bulk bags is the largest in Asia Pacific.

In Europe, the bulk bags industry is experiencing the fastest growth with a CAGR of 6.1% over the forecast period. The increasing adoption of bulk bags in the European food and agriculture sector as they offer a cost-effective solution for managing large volumes of produce and ingredients is contributing to market trajectory in the region. In addition to this, stringent European food safety and hygiene regulations are readily addressed by bulk bags manufactured with food-grade liners and certifications, promoting their use in the food sector. Moreover, the growing consumer preference for organic and sustainably produced goods aligns with the availability of recyclable and biodegradable bulk bag options. These combined benefits are creating lucrative opportunities over the forecast period.

In North America, the development of biodegradable and recyclable bulk bags is a significant factor impacting the market trajectory as well as showcasing a focus toward sustainability. Increased environmental awareness among both consumers and businesses leads to the risen demand for alternatives to traditional plastic packaging. Increasingly stringent regulations regarding waste and non-recyclable plastics further mandate manufacturers and end-users to adopt eco-friendly solutions like biodegradable and recyclable bulk bags. Technological advancements in materials science are enabling the creation of durable bulk bags from new polymers. These factors combined are driving the market trajectory in the North American region

In the Latin American bulk bags market expansion, price sensitivity is a major factor, as many businesses in the region operate with tight margins and prioritize affordability in purchasing decisions. Bulk bags offer an economic advantage compared to alternatives. Increasing competition further requires a cost reduction across operations, including packaging and material handling. This leads to making bulk bags an attractive option. Finally, the prominent agriculture and mining sectors, handling large material quantities, benefit significantly from the cost-effective packaging and transport offered by bulk bags. These combined factors contribute to the market growth in the region

In the Middle East and Africa (MEA) region flexible packaging is more focused on as it often presents a more economical option than rigid alternatives. This is especially for large-volume applications. The adaptability and customization offered by flexible packaging, allowing for tailored solutions to meet diverse product needs is increasing. Increasing exports of commodities like oil and minerals further require flexible and easily transportable packaging such as bulk bags. Consumer preferences in some areas also contribute, with a growing appreciation for the convenience and portability of flexible packaging. These combined factors are driving the growing adoption of flexible packaging, including bulk bags, across the MEA region.

Top Key Players and Market Share Insights:

The Global Bulk Bags Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Bulk Bags market. Key players in the Bulk Bags industry include-

- Berry Global Group, Inc. (U.S.)

- BAG Corp (U.S.)

- AmeriGlobe LLC (U.S.)

- Greif, Inc. (U.S.)

- Conitex Sonoco (U.S.)

- Mondi Group (UK)

- LC Packaging International BV (Netherlands)

- MiniBulk Inc. (U.S.)

- RDA Bulk Packaging Ltd. (U.S.)

- Big Bags International Pvt. Ltd. (India)

Recent Industry Developments :

Product Launch:

- In 2023, FlexSack introduced FlexSack-eco. It is an ecofriendly bulk bag that is produced from polypropylene and contains 30% of recycled polypropylene.

Bulk Bags Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,251.05 Million |

| CAGR (2025-2032) | 4.7% |

| By Type |

|

| By Design |

|

| By End Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Bulk Bags market? +

In 2024, the Bulk Bags market is USD 3,645.27 Million.

Which is the fastest-growing region in the Bulk Bags market? +

Europe is the fastest-growing region in the Bulk Bags market.

What specific segmentation details are covered in the Bulk Bags market? +

By Type, Design and End Use Industry segmentation details are covered in the Bulk Bags market.

Who are the major players in the Bulk Bags market? +

Berry Global Group, Inc. (U.S.), BAG Corp (U.S.), Mondi Group (UK), LC Packaging International BV (Netherlands), MiniBulk Inc. (U.S.), RDA Bulk Packaging Ltd. (U.S.) are some of the major players in the market.