- Summary

- Table Of Content

- Methodology

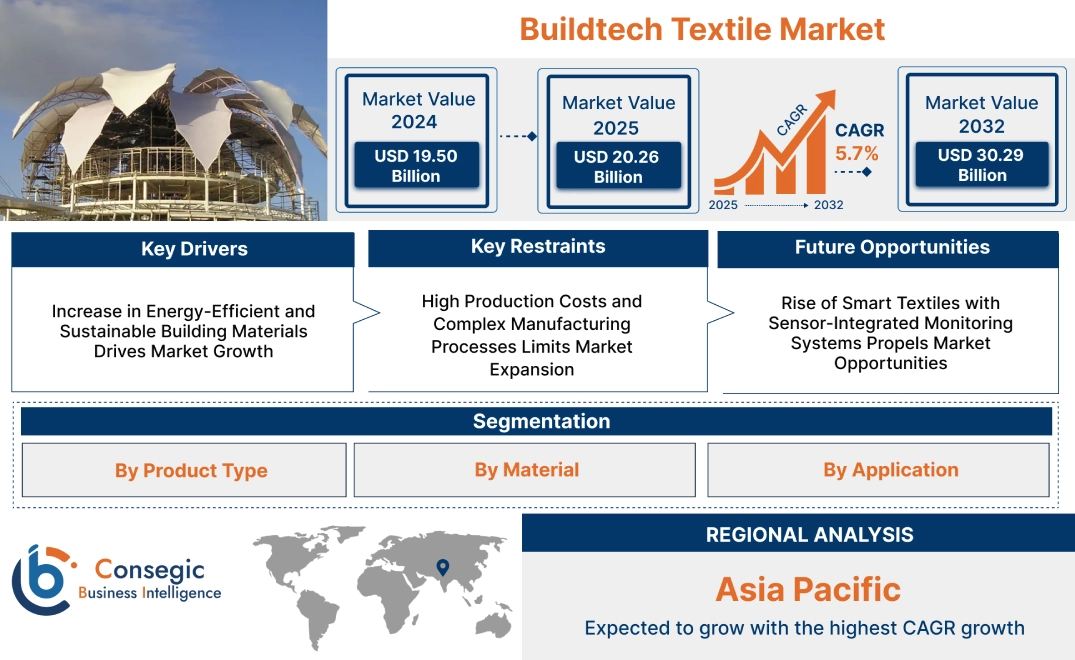

Buildtech Textile Market Size:

Buildtech Textile Market size is estimated to reach over USD 30.29 Billion by 2032 from a value of USD 19.50 Billion in 2024 and is projected to grow by USD 20.26 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Buildtech Textile Market Scope & Overview:

Buildtech textile refers to specialized technical textiles used in construction and architectural applications to enhance durability, functionality, and structural integrity. These textiles are designed for reinforcement, insulation, filtration, and protection, contributing to efficient building solutions. They are commonly utilized in roofing, scaffolding nets, geotextiles, and wall reinforcements, ensuring long-term performance in various environmental conditions.

Its key characteristics include high tensile strength, weather resistance, and flame retardancy. These materials offer improved load-bearing capacity, moisture control, and energy efficiency, making them essential in modern infrastructure projects. Their lightweight nature simplifies installation while maintaining structural stability and flexibility in design.

Construction, civil engineering, and urban development sectors integrate them to enhance sustainability and safety in building processes. Innovations in material science continue to refine their properties, ensuring superior durability, cost-effectiveness, and adaptability for diverse architectural and industrial applications.

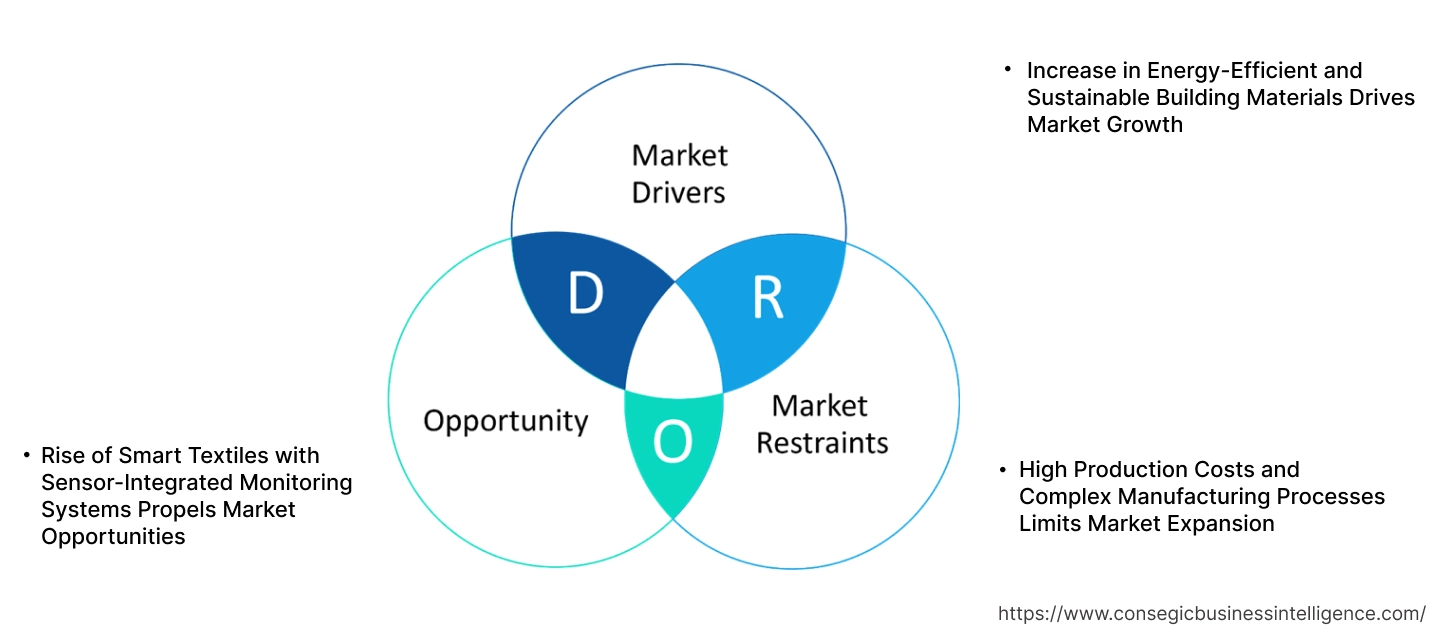

Buildtech Textile Market Dynamics - (DRO):

Key Drivers:

Increase in Energy-Efficient and Sustainable Building Materials Drives Market Growth

As governments and private developers focus on reducing carbon footprints and enhancing energy conservation, the use of high-performance, insulation, and weather-resistant textiles in modern structures is expanding. These textiles contribute to thermal insulation, moisture control, and fire resistance, making them essential for green buildings and LEED-certified construction projects. The adoption of solar-integrated fabric structures, eco-friendly roofing membranes, and biodegradable geotextiles is further strengthening market potential. Additionally, regulatory mandates promoting low-energy and resource-efficient buildings are pushing architects and engineers toward durable and lightweight textile-based solutions.

- For instance, in November 2024, Serge Ferrari Group launched Soltis Liris, a fabric with a variable openness factor that controls how much light and heat passes through, providing sustainable buildings with a new approach to thermal and visual comfort.

As the industry continues to evolve, these factors are expected to play a crucial role in buildtech textile market expansion, positioning sustainable textiles as a key component of next-generation infrastructure.

Key Restraints:

High Production Costs and Complex Manufacturing Processes Limits Market Expansion

Advanced textile solutions require specialized raw materials, multi-layer coating applications, and intensive fabrication techniques to achieve desired properties such as fire resistance, UV protection, and high tensile strength. The use of advanced weaving, lamination, and nanotechnology-based treatments adds to manufacturing complexity, leading to higher operational expenses. Additionally, the cost of research and development for next-generation textile solutions limits market accessibility, particularly for small and mid-sized construction firms looking for cost-effective alternatives. Logistics and transportation costs further contribute to pricing challenges, as certain specialized textiles require controlled storage and handling. To achieve broader adoption, manufacturers must focus on scaling production efficiency and optimizing material sourcing. Overcoming these barriers is critical for ensuring buildtech textile market growth and making these materials more accessible for large-scale infrastructure projects.

Future Opportunities:

Rise of Smart Textiles with Sensor-Integrated Monitoring Systems Propels Market Opportunities

Advanced textiles feature embedded IoT sensors, conductive fibers, and self-regulating thermal properties, that enable them to detect stress, moisture levels, and temperature fluctuations in buildings and infrastructure. The growth of digital construction and smart cities has led to increased adoption of sensor-enabled geotextiles, adaptive roofing membranes, and fiber-reinforced composites that enhance safety and efficiency in architectural designs. Additionally, these textiles are being integrated into bridge reinforcements, tunnel linings, and earthquake-resistant structures to improve long-term durability and structural resilience. As industries continue to explore the potential of AI-powered diagnostics and autonomous repair systems, these advancements will drive new buildtech textile market opportunities, establishing sensor-integrated materials as a crucial innovation in modern construction.

Buildtech Textile Market Segmental Analysis :

By Product Type:

By product type, the market is segmented into woven, non-woven, and knitted.

The woven segment held the largest buildtech textile market share in 2024.

- Woven textiles are commonly used in concrete reinforcement, scaffolding nets, and geotextile applications, offering high strength and durability in construction projects.

- The demand for heavy-duty construction textiles is increasing, particularly in road infrastructure and civil engineering projects.

- Segmental analysis highlights that woven fabrics provide superior load-bearing capacity, making them a preferred choice for reinforcement applications.

- For instance, Mermet offers Acoustis® 50, the first patented solution based on exclusively weaving coated fiberglass with a special weave and a controlled diameter.

- Thus, as per buildtech textile market trends, advancements in weaving technology are enhancing fabric flexibility and longevity, driving adoption across various construction sectors.

The non-woven segment is expected to have the fastest CAGR during the forecast period.

- Non-woven textiles offer cost-effective and lightweight alternatives, making them ideal for roofing insulation, waterproof membranes, and tarpaulins.

- The need for easy-to-install, weather-resistant construction materials is fueling the adoption of non-woven textiles.

- Market trends indicate that non-woven fabrics are gaining popularity in the waterproofing and industrial packaging sectors, improving efficiency and sustainability.

- Therefore, with the increasing investment in smart construction materials, non-woven textiles are contributing to buildtech textile market growth.

By Material:

By material, the market is segmented into natural fibers and synthetic fibers.

The synthetic fibers segment held the largest market share in 2024.

- Synthetic fibers such as polypropylene, polyester, and nylon are widely used in buildtech textiles, offering high tensile strength and resistance to environmental conditions.

- The need for chemically resistant and long-lasting construction fabrics is rising in industrial and large-scale infrastructure projects.

- Buildtech textile market analysis highlights that synthetic fibers provide superior flexibility and durability, making them suitable for roofing, insulation, and geotextile applications.

- Thus, as per segmental trends, manufacturers are developing eco-friendly synthetic alternatives, improving recyclability and reducing environmental impact.

The natural fibers segment is anticipated to experience the fastest CAGR during the forecast period.

- Natural fibers such as jute, hemp, and cotton are gaining popularity as sustainable alternatives, particularly in temporary scaffolding and eco-friendly construction solutions.

- The demand for biodegradable and renewable construction textiles is growing, driving interest in organic reinforcement materials.

- Segmental trends indicate that advancements in natural fiber treatments are enhancing moisture resistance and fire retardancy, expanding their usability.

- For instance, the Indian government has invested in projects developing cotton-based canvas tarpaulins, floor and wall coverings and canopies.

- Therefore, with the increasing emphasis on green construction materials, the natural fibers segment is contributing to buildtech textile market expansion.

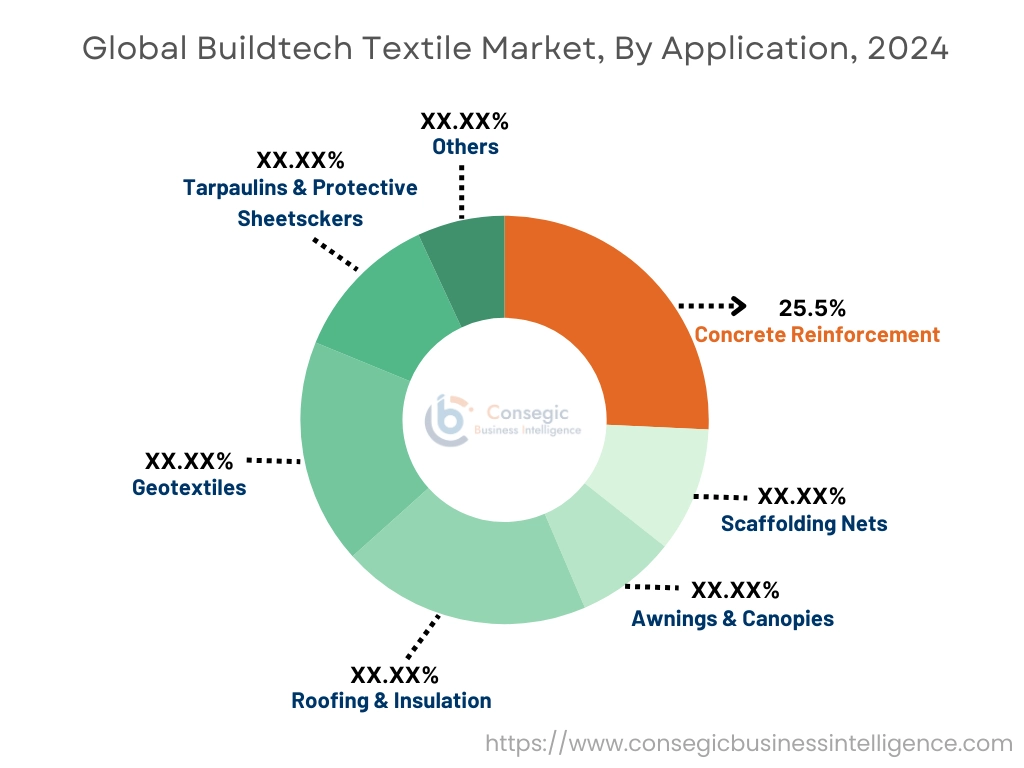

By Application:

By application, the market is segmented into concrete reinforcement, scaffolding nets, awnings & canopies, roofing & insulation, geotextiles, tarpaulins & protective sheets, and others.

The concrete reinforcement segment held the largest buildtech textile market share of 25.5% in 2024.

- They play a crucial role in strengthening concrete structures, ensuring enhanced crack resistance and load distribution.

- The need for advanced reinforcement materials is increasing as governments invest in infrastructure modernization and road development projects.

- Buildtech textile market analysis suggests that textile-reinforced concrete (TRC) is becoming a viable alternative to traditional steel reinforcement, reducing material costs and carbon footprint.

- Thus, as per market trends, a shift toward high-performance fabrics to improve the strength and longevity of reinforced structures.

The roofing & insulation segment is expected to achieve the fastest CAGR during the forecast period.

- Buildtech textiles are widely used in thermal and sound insulation solutions, improving energy efficiency and building performance.

- The demand for lightweight, breathable insulation fabrics is rising in residential and commercial construction.

- Buildtech textile market trends highlight innovations in reflective and fire-resistant insulation materials, enhancing structural safety.

- Therefore, as the construction sector moves toward sustainable and energy-efficient buildings, this segment is driving market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

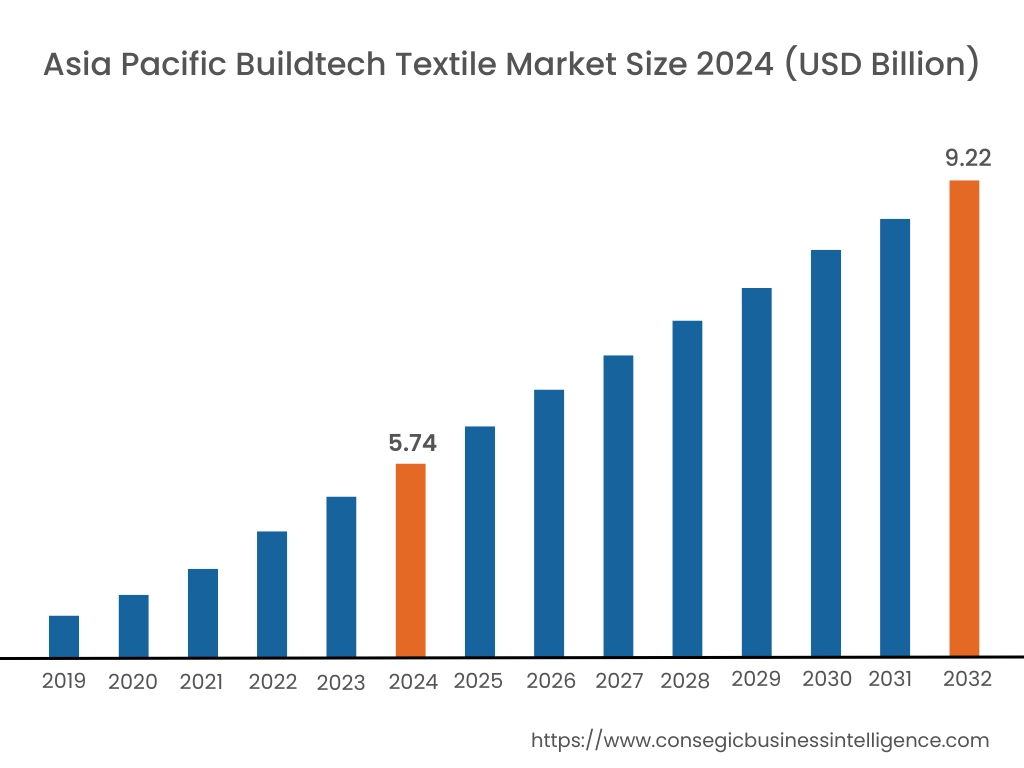

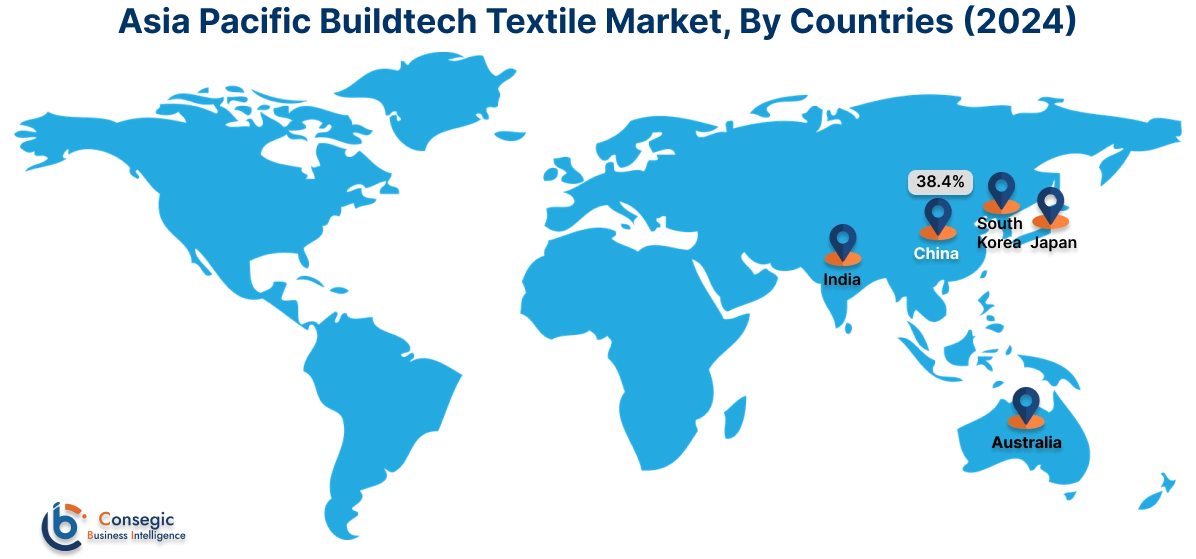

Asia Pacific region was valued at USD 5.74 Billion in 2024. Moreover, it is projected to grow by USD 5.98 Billion in 2025 and reach over USD 9.22 Billion by 2032. Out of this, China accounted for the maximum revenue share of 38.4%. The Asia Pacific region is experiencing rapid growth in the buildtech textile industry, primarily due to infrastructure development and an increasing emphasis on sustainable construction practices in developing economies. The region's strong economic growth, coupled with investments in transportation, energy, and environmental protection projects, contributes to the market expansion.

North America is estimated to reach over USD 9.82 Billion by 2032 from a value of USD 6.47 Billion in 2024 and is projected to grow by USD 6.71 Billion in 2025. In North America, the market is expanding due to increasing investments in civil engineering structures and a growing awareness of sustainable construction. Their demand is propelled by their applications in concrete reinforcement, roofing materials, and insulation. The region's focus on resilient infrastructure presents a substantial buildtech textile market opportunity for manufacturers specializing in advanced textile solutions.

Europe exhibits substantial buildtech textile market demand, with countries like Germany, France, and the UK leading in adoption. The region's stringent building regulations and commitment to energy-efficient structures drive the demand for high-performance textiles. Applications in noise prevention, air conditioning, and interior construction are particularly prominent, reflecting the market's alignment with sustainable and innovative building solutions.

Latin America's buildtech textile market is gradually gaining traction, influenced by urbanization and infrastructure development. Countries like Brazil and Mexico are investing in civil engineering projects, leading to increased need for textiles used in concrete reinforcement and roofing materials. The region's focus on modernizing infrastructure offers growth prospects for companies providing innovative textile solutions tailored to local needs.

The buildtech textile market demand in the Middle East and Africa is emerging, with growth potential linked to ambitious construction projects and urban development plans. It is driven by the need for durable and climate-resilient building materials suitable for harsh environmental conditions. As these regions continue to invest in infrastructure, opportunities arise for the adoption of advanced textile materials that enhance building performance and sustainability.

Top Key Players & Market Share Insights:

The buildtech textile market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global buildtech textile market. Key players in the buildtech textile industry include -

- Serge Ferrari Group (France)

- Mehler Texnologies GmbH (Germany)

- Toray Industries, Inc. (Japan)

- SRF Limited (India)

- Officine Maccaferri SpA (Italy)

- Verseidag-Indutex GmbH (Germany)

- Low & Bonar PLC (UK)

- DuPont (USA)

- Ahlstrom-Munksjö (Finland)

- SKAPS Industries (USA)

Recent Industry Developments :

Product Launches:

- In October 2023, Serge Ferrari Group launched the Flexlight Shield 800, a fabric made with PVC flexible composite membrane with woven fiberglass reinforcement for modular structures. This non-combustible meshing holds the structure in place and protects the inside of the building by blocking fire residue, embers and other fire debris projected onto the roof or walls.

Acquisitions:

- In May 2020, Freudenberg acquired all shares in Low & Bonar PLC, expanding its broad product range and offering customers more flexibility and individually tailored products.

Buildtech Textile Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 30.29 Billion |

| CAGR (2025-2032) | 5.7% |

| By Product Type |

|

| By Material |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Buildtech Textile Market? +

Buildtech Textile Market size is estimated to reach over USD 30.29 Billion by 2032 from a value of USD 19.50 Billion in 2024 and is projected to grow by USD 20.26 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

What specific segmentation details are covered in the Buildtech Textile Market report? +

The Buildtech Textile market report includes specific segmentation details for product type, material and applications.

Which is the fastest-growing region in the Buildtech Textile Market? +

Asia Pacific is the fastest-growing region in the Buildtech Textile market. These trends are encouraged by infrastructure development and increasing emphasis on sustainable construction practices in developing economies.

Who are the major players in the Buildtech Textile Market? +

The key participants in the Buildtech Textile market are Serge Ferrari Group (France), Mehler Texnologies GmbH (Germany), Verseidag-Indutex GmbH (Germany), Low & Bonar PLC (UK), DuPont (USA), Ahlstrom-Munksjö (Finland), SKAPS Industries (USA), Toray Industries, Inc. (Japan), SRF Limited (India) and Officine Maccaferri SpA (Italy).