- Summary

- Table Of Content

- Methodology

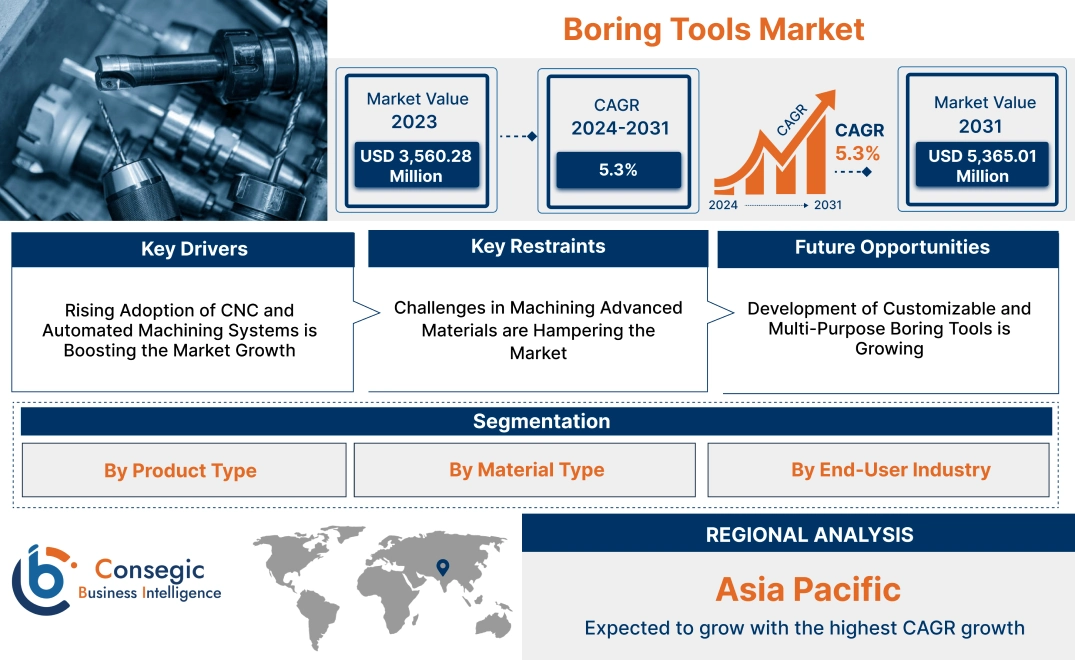

Boring Tools Market Size:

Boring Tools Market size is estimated to reach over USD 5,365.01 Million by 2031 from a value of USD 3,560.28 Million in 2023 and is projected to grow by USD 3,684.11 Million in 2024, growing at a CAGR of 5.3% from 2024 to 2031.

Boring Tools Market Scope & Overview:

The boring tools are designed to enlarge or finish pre-existing holes in materials with high precision and accuracy, catering to industries that demand exact specifications and smooth finishes. These tools are widely used in applications such as drilling, reaming, and boring in the manufacturing, automotive, aerospace, and construction sectors. Key characteristics of boring tools include their high durability, resistance to wear, and compatibility with various materials such as metals, plastics, and composites. The benefits include enhanced precision, improved productivity, and extended tool life, ensuring efficient material processing. Applications span machining centers, lathes, and automated systems for producing components like engine blocks, hydraulic cylinders, and industrial equipment. End-users include automotive manufacturers, aerospace companies, and industrial machinery producers, driven by advancements in manufacturing technologies, increasing opportunities for the implementation of high-performance machinery, and the growing adoption of automation in industrial processes.

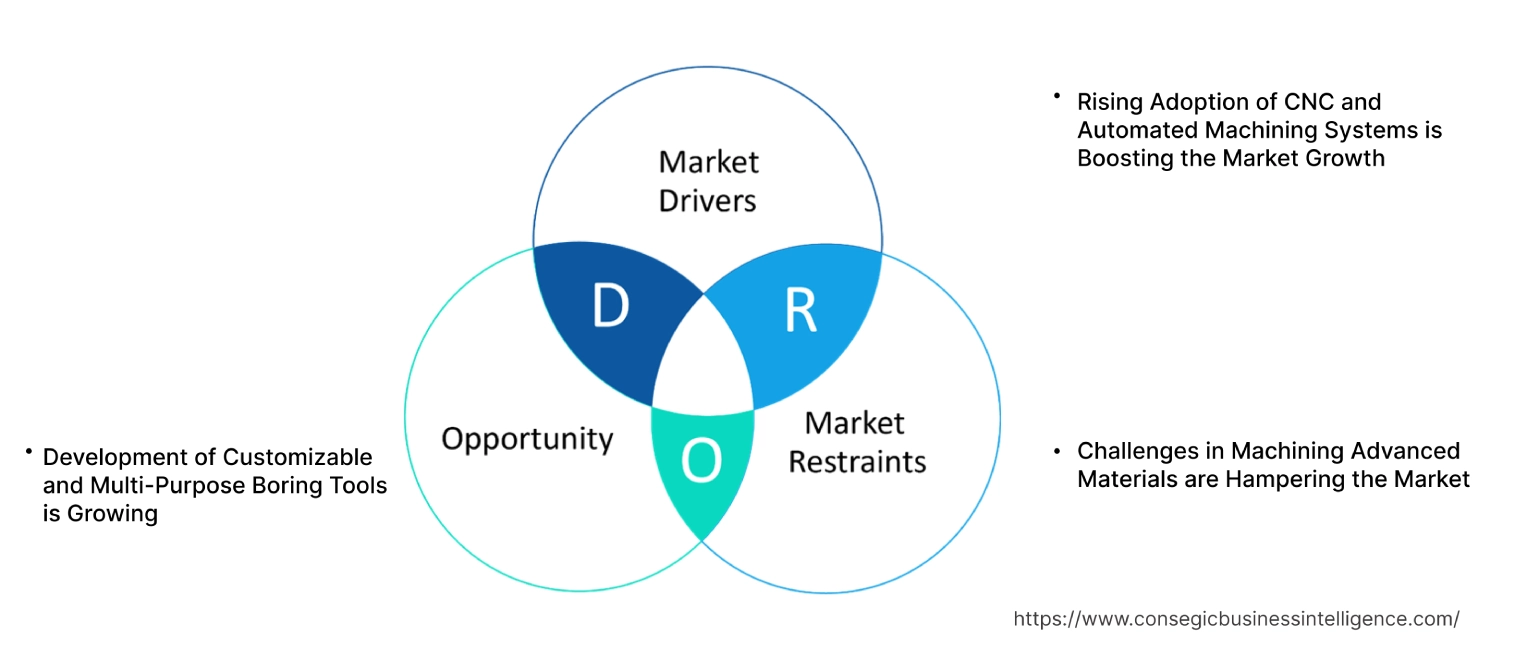

Boring Tools Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of CNC and Automated Machining Systems is Boosting the Market Growth

The integration of boring tools with CNC (Computer Numerical Control) and automated machining systems has revolutionized manufacturing by enhancing precision, consistency, and efficiency. Automated systems enable seamless execution of complex machining processes, reducing human error and operational downtime. Boring tools tailored for CNC machines play a critical role in achieving accurate internal diameters and superior surface finishes in components for industries such as aerospace, automotive, and energy.

Trends in smart manufacturing and industrial automation are driving the incorporation of CNC systems in production workflows. These systems allow manufacturers to handle high volumes while maintaining quality standards, particularly in applications requiring tight tolerances. The analysis highlights that the synergy between advanced boring tools and automation technologies is transforming traditional machining processes, paving the way for more streamlined and scalable manufacturing operations.

Key Restraints:

Challenges in Machining Advanced Materials are Hampering the Market

The rising use of advanced materials such as composites, titanium alloys, and high-strength steel presents significant challenges for boring operations. These materials, while offering superior performance, are difficult to machine due to their hardness, thermal resistance, and tendency to cause rapid tool wear. Boring tools must be designed with specialized coatings and geometries to withstand the stress associated with machining these materials.

In addition, the thermal and mechanical demands of processing advanced materials can compromise the accuracy and longevity of conventional boring tools. This challenge necessitates ongoing innovation in tool materials and designs to meet the unique requirements of high-performance industries. The boring tools market trends in material science and engineering are driving the expansion of cutting-edge solutions that address these limitations while maintaining cost efficiency.

Future Opportunities :

Development of Customizable and Multi-Purpose Boring Tools is Growing

The evolving needs of industries have created opportunities for the development of customizable and multi-purpose boring tools. These tools are designed to handle a wide range of applications, from machining lightweight materials in aerospace to high-strength components in automotive. Modular tool designs, which allow for interchangeable components, offer flexibility and reduce the need for maintaining extensive tool inventories.

Trends in adaptive manufacturing and precision engineering have also led to innovations in tool customization, enabling manufacturers to meet specific industry requirements more efficiently. By offering tools capable of addressing multiple machining challenges in a single setup, companies can enhance productivity and minimize operational complexity. Analysis indicates that these advancements will play a critical role in optimizing manufacturing processes across various sectors, aligning with the broader goals of efficiency and sustainability.

Boring Tools Market Segmental Analysis :

By Product Type:

Based on product type, the boring tools market is segmented into rough boring and fine boring.

The rough boring segment accounted for the largest revenue in the boring tools market share in 2023.

- Rough boring tools are primarily used for enlarging pre-drilled holes and removing large amounts of material efficiently.

- These tools are widely adopted in industries such as automotive, construction, and manufacturing, where speed and productivity are crucial.

- Their robust design and ability to handle high cutting speeds and feed rates make them ideal for applications requiring quick material removal.

- The trends for rough boring tools are driven by the growing need for high-performance machining solutions in heavy industries, where precision is secondary to productivity.

- Additionally, advancements in tool materials and coatings have improved the durability and performance of rough boring tools, further driving their market dominance.

The fine boring segment is anticipated to register the fastest CAGR during the forecast period.

- Fine boring tools are designed for precision machining, ensuring tight tolerances and high-quality surface finishes.

- These tools are extensively used in industries like aerospace and automotive, where accuracy and superior finishes are critical.

- Fine boring tools are particularly valued for their ability to meet the stringent requirements of components such as engine cylinders, gearboxes, and hydraulic systems.

- The growing trends for high-precision manufacturing, fueled by advancements in automation and CNC technology, are expected to drive significant boring tools market growth in the fine boring segment.

- Furthermore, their increasing boring tools market opportunities in producing high-value components make this segment a focal point of innovation and investment.

By Material Type:

Based on material type, the boring tools market is segmented into high-speed steel (HSS), carbide, diamond, cermet, ceramics, and others.

The carbide segment accounted for the largest revenue in the boring tools market share in 2023.

- Carbide boring tools are widely preferred for their exceptional hardness, wear resistance, and ability to maintain cutting-edge integrity under high temperatures.

- These tools are ideal for high-speed and high-precision machining applications, making them indispensable in industries such as automotive, aerospace, and general manufacturing.

- The durability and versatility of carbide tools enable their use across a wide range of materials, including steels, cast iron, and non-ferrous alloys.

- The rising boring tools market demand for cost-effective tools that enhance productivity and minimize downtime has established carbide as the dominant material type in the boring tools market.

The diamond segment is anticipated to register the fastest CAGR during the forecast period.

- Diamond boring tools are renowned for their unparalleled hardness and wear resistance, making them suitable for machining hard-to-cut materials like composites, ceramics, and advanced alloys.

- These tools are extensively used in high-precision applications within the aerospace and electronics industries, where superior surface finish and dimensional accuracy are critical.

- The increasing adoption of lightweight and advanced materials in manufacturing, coupled with growing investments in high-performance machining solutions, is driving the rapid growth of the diamond segment.

- Additionally, advancements in synthetic diamond technologies are expected to make these tools more accessible, further boosting their market penetration.

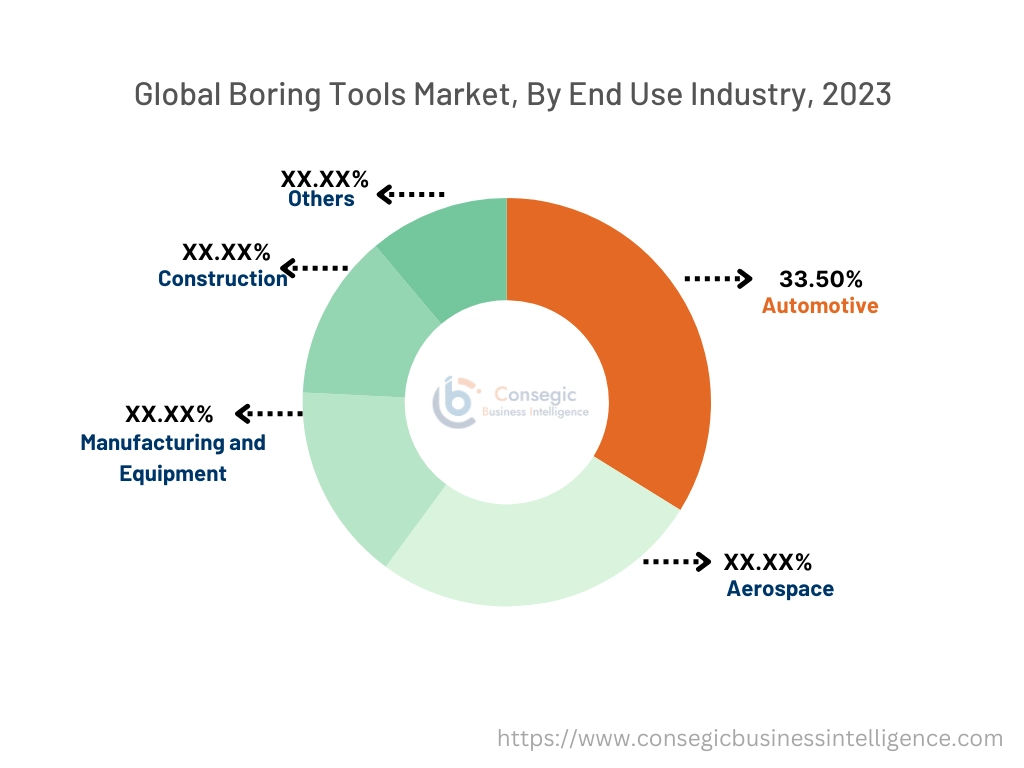

By End-Use Industry:

Based on end-use, the boring tools market is segmented into automotive, aerospace, manufacturing and equipment, construction, and others.

The automotive segment accounted for the largest revenue of 33.50% share in 2023.

- The automotive sector relies heavily on boring tools for precision machining of critical components such as engine blocks, crankshafts, and transmission parts.

- The boring tools market trends for boring tools in this sector are driven by the increasing production of vehicles and the need for efficient manufacturing processes.

- The growing adoption of electric vehicles (EVs) has further boosted the boring tools market demand for high-precision boring tools, as these vehicles require lightweight and complex components with tight tolerances.

- Additionally, advancements in boring technologies that enhance productivity and reduce machining time have solidified the dominance of the automotive segment in the market.

The aerospace segment is anticipated to register the fastest CAGR during the forecast period.

- The aerospace sector demands high-precision machining tools to manufacture critical components such as turbine blades, fuselage parts, and landing gear.

- Boring tools play a vital role in achieving the stringent tolerances and surface finishes required in aerospace manufacturing.

- The increasing use of advanced materials such as titanium alloys and composites in aircraft manufacturing has fueled the trends for specialized boring tools.

- Furthermore, the growing global boring tools market for commercial and defense aircraft, coupled with advancements in CNC and automated machining technologies, is expected to drive significant growth in the aerospace segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

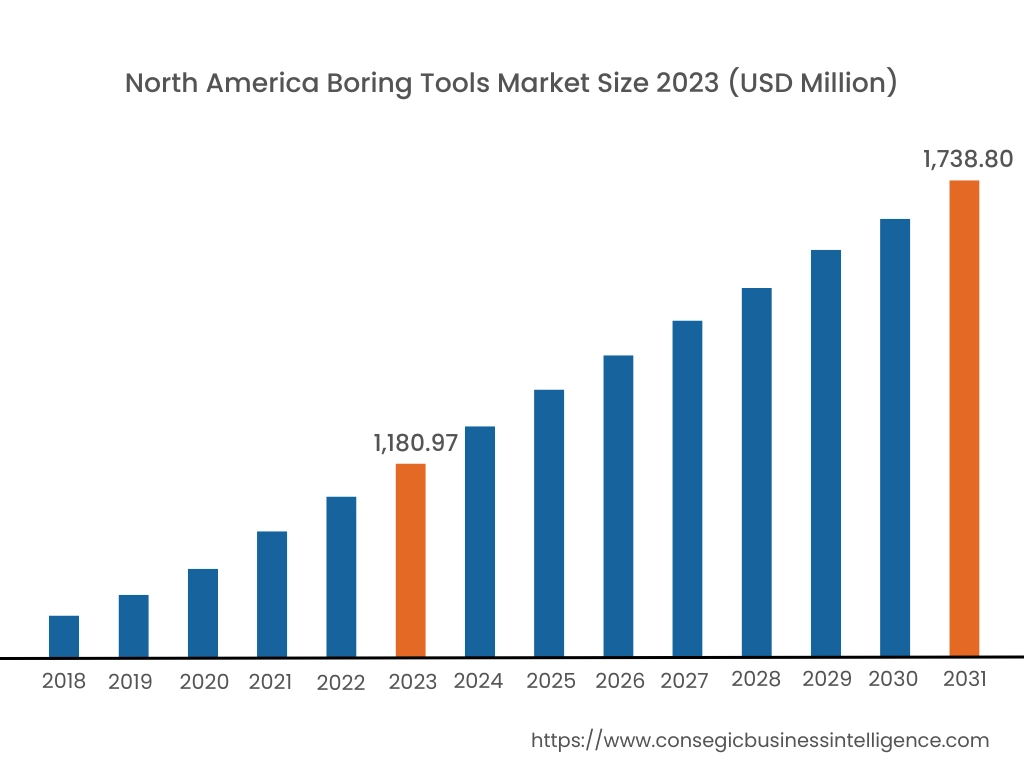

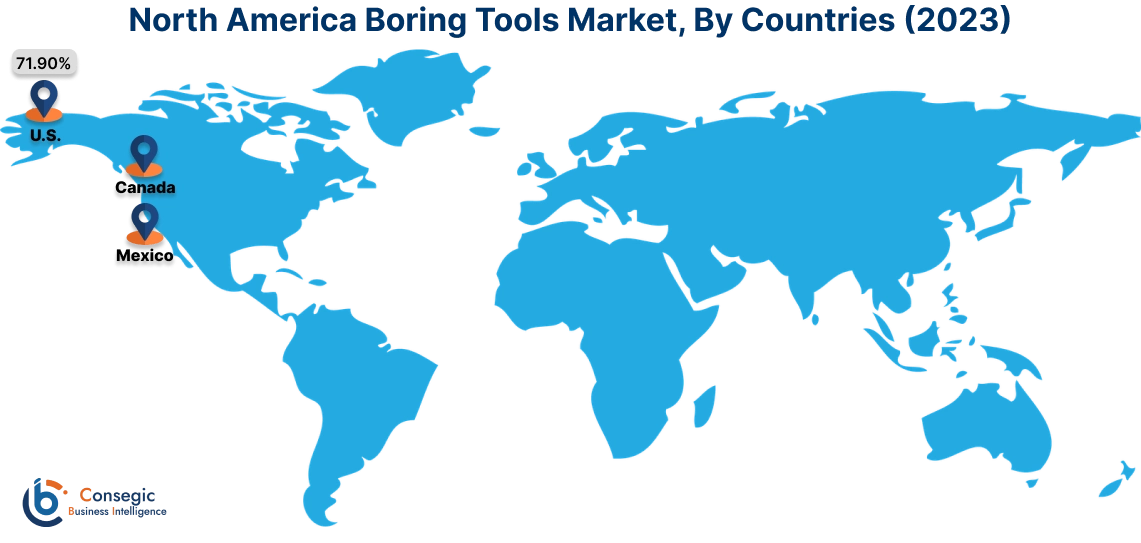

In 2023, North America was valued at USD 1,180.97 Million and is expected to reach USD 1,738.80 Million in 2031. In North America, the U.S. accounted for the highest share of 71.90% during the base year of 2023. North America holds a significant share in the boring tools market analysis, driven by its advanced manufacturing sectors such as aerospace, automotive, and oil and gas. The U.S. leads the region with a strong trend for high-precision boring tools used in machining components for aerospace and defense applications. The automotive sector further supports the adoption of advanced boring tools for engine and transmission manufacturing. Canada contributes with increasing investments in industrial machinery and equipment, particularly in the oil and gas sector. However, the high costs of advanced boring tools and increasing competition from global players may pose challenges in this region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.7% over the forecast period. Asia-Pacific is the fastest-growing region in the boring tools market analysis, fueled by rapid industrialization, urbanization, and increasing trends from the automotive and construction sectors in China, India, and Japan. China dominates the market with its expansive manufacturing sector, using boring tools in automotive production, machinery, and infrastructure projects. India’s growing industrial and automotive base supports the rising adoption of boring tools for machining and precision engineering. Japan focuses on high-quality boring tools for advanced applications in the automotive, electronics, and aerospace industries. However, price sensitivity in emerging markets and reliance on imported advanced tools in some countries may hinder broader market adoption.

Europe is a prominent market for boring tools, supported by its well-established automotive, aerospace, and industrial machinery industries. As per the Countries analysis Germany, France, and Italy are key contributors. Germany leads with extensive use of boring tools in automotive production for high-precision engine and gear manufacturing. France emphasizes their application in aerospace manufacturing, particularly for machining high-performance components. Italy, known for its strong industrial manufacturing base, utilizes boring tools in machinery and heavy equipment production. However, the region faces challenges related to increasing labor costs and stringent EU regulations on industrial machinery and tool manufacturing.

The Middle East & Africa region is witnessing steady growth in the boring tools market, driven by increasing investments in oil and gas, construction, and infrastructure expansion. Countries like Saudi Arabia and the UAE are adopting boring tools for applications in drilling equipment and industrial machinery to support their growing energy and industrial sectors. In Africa, South Africa is an emerging market, leveraging boring tools in mining and heavy machinery industries. However, limited local manufacturing capabilities and reliance on imports for high-precision tools may restrict the boring tools market growth in this region.

Latin America is an emerging market for boring tools as the analysis depicts, with Brazil and Mexico leading the region. Brazil’s expanding automotive and aerospace industries drive the growth of boring tools in precision machining and manufacturing. Mexico’s growing industrial base, particularly in automotive and electronics production, supports the adoption of boring tools to meet international manufacturing standards. The region is also exploring advancements in tooling technologies to enhance production efficiency. However, economic instability and inconsistent regulatory frameworks in some countries may pose challenges to boring tools market expansion.

Top Key Players and Market Share Insights:

The Boring Tools market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global boring tools market. Key players in the boring tools industry include -

- Allied Machine & Engineering Corp. (U.S.)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Kyocera Corporation (Japan)

- CeramTec GmbH (Germany)

- Becker Diamantwerkzeuge GmbH (Germany)

- BIG KAISER Precision Tooling Inc. (U.S.)

- Kennametal Inc. (U.S.)

- NACHI-FUJIKOSHI Corp. (Japan)

- OSG Corporation (Japan)

- Sandvik AB (Sweden)

Recent Industry Developments :

Product Launches:

- In September 2024, Sandvik Coromant engineered the world's largest boring bar, measuring nearly 11 meters in length and 600 millimeters in diameter, to meet the specific machining requirements of Finland's Häkkinen Group Jyväskylä unit. This tool is designed for precision manufacturing of large components across sectors such as offshore oil and gas, power transmission, and renewable energy. Incorporating advanced vibration-damping technology, the boring bar ensures stable and controlled cutting conditions, leading to enhanced productivity, extended tool life, and superior surface finishes. This development underscores Sandvik Coromant's commitment to innovation and precision in machining applications.

Boring Tools Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 5,365.01 Million |

| CAGR (2024-2031) | 5.3% |

| By Product Type |

|

| By Material Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Boring Tools Market by 2031? +

Boring Tools Market size is estimated to reach over USD 5,365.01 Million by 2031 from a value of USD 3,560.28 Million in 2023 and is projected to grow by USD 3,684.11 Million in 2024, growing at a CAGR of 5.3% from 2024 to 2031.

What are the key factors driving the growth of the Boring Tools Market? +

Key drivers include the rising adoption of CNC and automated machining systems, advancements in manufacturing technologies, and the growing demand for precision and efficiency in industries like automotive, aerospace, and manufacturing.

What challenges does the market face? +

Challenges include difficulties in machining advanced materials such as composites and titanium alloys, which can cause rapid tool wear and require specialized boring tools. High initial costs and the need for advanced tooling solutions also pose challenges.

What opportunities exist in the market? +

Opportunities lie in the development of customizable and multi-purpose boring tools, which address diverse machining requirements and enhance operational flexibility. Advancements in tool materials, coatings, and modular designs are further creating significant opportunities.