- Summary

- Table Of Content

- Methodology

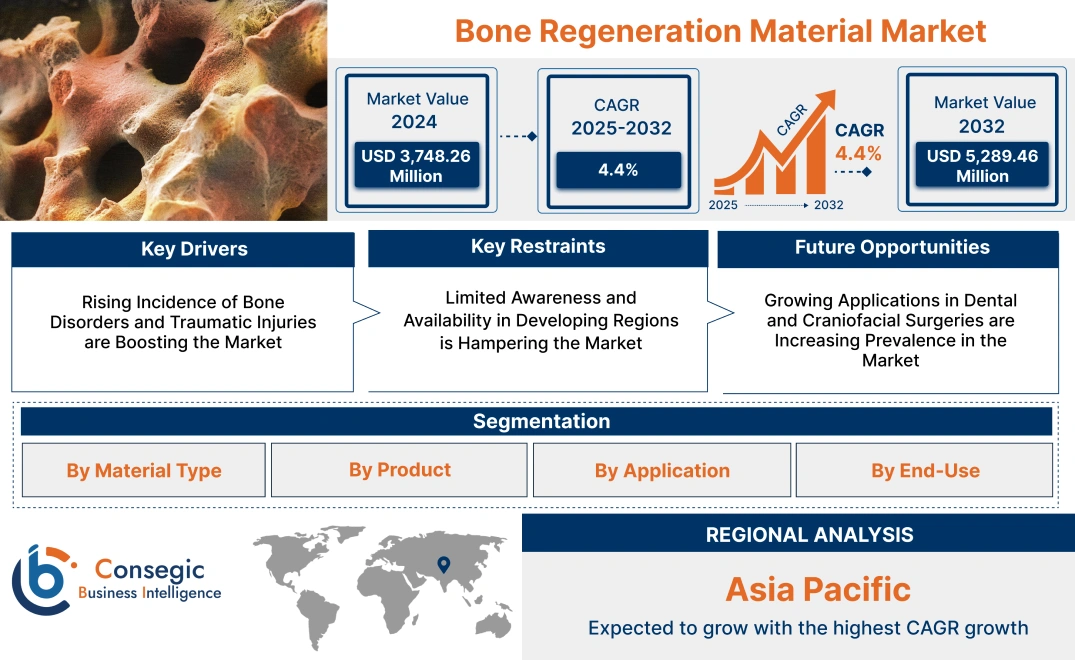

Bone Regeneration Material Market Size:

Bone Regeneration Material Market size is estimated to reach over USD 5,289.46 Million by 2032 from a value of USD 3,748.26 Million in 2024 and is projected to grow by USD 3,846.40 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

Bone Regeneration Material Market Scope & Overview:

The bone regeneration technology is designed to facilitate the repair, replacement, and regeneration of bone tissues in medical and dental applications. These materials, including synthetic grafts, bioactive ceramics, demineralized bone matrices, and collagen-based products, play a critical role in enhancing bone healing and regeneration. Key characteristics of bone regeneration materials include biocompatibility, osteoconductivity, and mechanical stability, ensuring successful integration with natural bone tissue. The benefits include reduced healing times, improved surgical outcomes, and the ability to address complex bone defects. Applications span orthopedic surgeries, dental implants, spinal fusion, and trauma recovery, where effective bone regeneration is critical. End-users include hospitals, specialty clinics, and research institutions, driven by the increasing prevalence of bone-related disorders, advancements in biomaterials technology, and rising trends for minimally invasive surgical procedures.

Bone Regeneration Material Market Dynamics - (DRO) :

Key Drivers:

Rising Incidence of Bone Disorders and Traumatic Injuries are Boosting the Market

The increasing prevalence of bone-related conditions such as osteoporosis, osteoarthritis, and traumatic injuries is significantly driving the adoption of bone regeneration materials in medical practices. These disorders often lead to compromised bone integrity and fractures, necessitating effective solutions for bone repair and reconstruction. Bone regeneration, including allografts, synthetic scaffolds, and bioactive compounds, enhances the healing process by promoting osteogenesis and providing structural support to damaged areas.

Trends in orthopedic surgeries and regenerative medicine are further amplifying the utilization of these materials, particularly in procedures requiring minimally invasive techniques. Analysis indicates that the rising number of surgeries addressing degenerative bone diseases and trauma cases highlights the critical role of bone regeneration in improving patient outcomes and recovery rates.

Key Restraints:

Limited Awareness and Availability in Developing Regions is Hampering the Market

In developing regions, limited awareness of advanced bone regeneration and its benefits poses a significant challenge to bone regeneration material market expansion. Many healthcare providers in these areas rely on traditional methods for bone repair, often due to a lack of knowledge about modern regenerative technologies. Additionally, inadequate medical infrastructure and limited availability of these materials restrict their adoption, especially in rural and underserved areas.

The lack of trained professionals and the high costs associated with advanced bone regeneration solutions further exacerbate this challenge. Addressing these gaps requires focused efforts on awareness campaigns, medical training, and collaborations with local healthcare providers to introduce cost-effective and accessible solutions. Trends in healthcare modernization and investment in emerging markets offer potential pathways to overcome these barriers.

Future Opportunities :

Growing Applications in Dental and Craniofacial Surgeries are Increasing Prevalence in the Market

Bone regeneration materials are increasingly being used in dental and craniofacial surgeries to address challenges such as bone loss, structural deformities, and implant support. These materials are vital in procedures like dental implants, maxillofacial reconstruction, and periodontal treatments, where they enhance bone integration, promote faster healing, and improve structural stability.

Trends in dental aesthetics, tourism, and reconstructive surgeries are driving the adoption of advanced regenerative materials tailored to these specialized needs. The analysis highlights that the growing focus on minimally invasive and precision-driven dental procedures presents significant opportunities for manufacturers to expand their offerings. By developing innovative and patient-specific solutions, companies can cater to the increasing sophistication and customization required in dental and craniofacial applications.

Bone Regeneration Material Market Segmental Analysis :

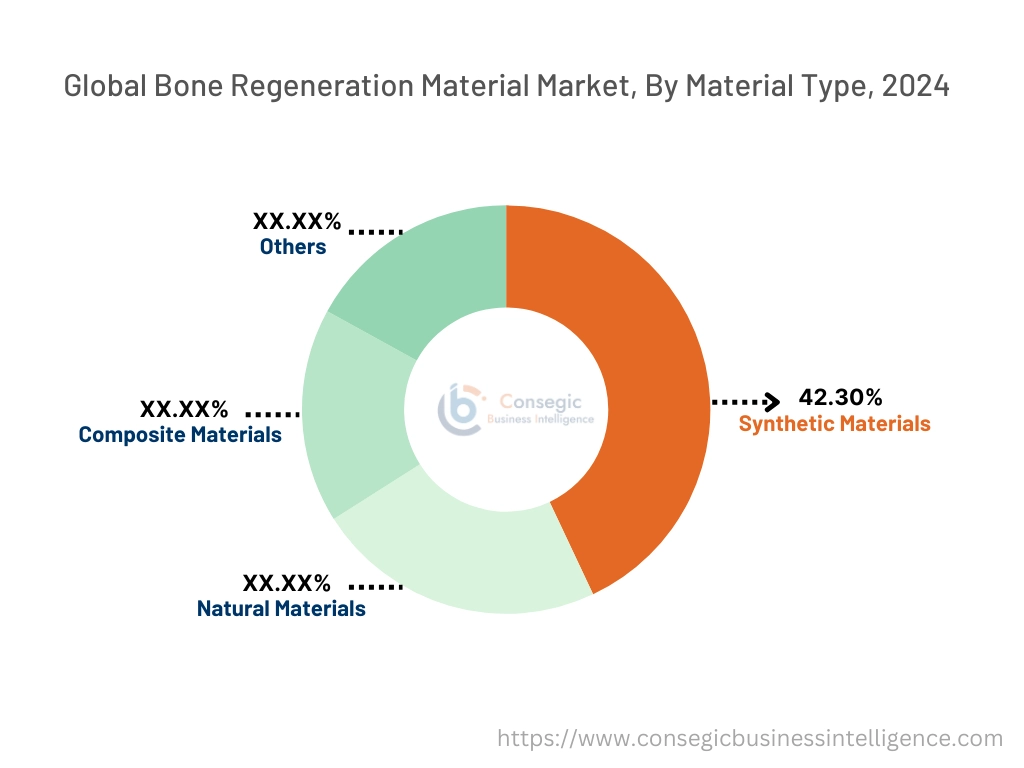

By Material Type:

Based on material type, the bone graft substitutes market is segmented into synthetic materials, natural materials, composite materials, and others. The synthetic materials segment is further divided into calcium phosphate, hydroxyapatite, tricalcium phosphate, and bioactive glass, while natural materials are subcategorized into collagen, demineralized bone matrix (DBM), and bone morphogenetic proteins (BMP).

The synthetic materials segment accounted for the largest revenue of 42.30% in bone regeneration material share in 2024.

- Synthetic materials dominate the bone graft substitutes market due to their consistent availability, cost-effectiveness, and ability to closely mimic the structure and function of natural bone.

- Calcium phosphate and hydroxyapatite are widely used for their excellent osteoconductive properties and ability to support bone regeneration.

- Tricalcium phosphate, another synthetic material, is often used in combination with other materials to enhance mechanical stability.

- Bioactive glass is gaining popularity for its osteostimulative properties, promoting faster bone formation.

- The bone regeneration material market trends for synthetic materials are particularly high in procedures requiring large graft volumes, such as spinal fusion and joint reconstruction.

The composite materials segment is anticipated to register the fastest CAGR during the forecast period.

- Composite materials combine synthetic and natural components, offering enhanced mechanical strength and biological performance.

- These materials address the limitations of individual components by providing a balance of osteoconductive and osteoinductive properties.

- Their increasing bone regeneration material market opportunities in craniomaxillofacial surgeries and complex orthopedic procedures highlight their growing relevance.

- Advancements in composite materials, including the integration of rising factors and nanotechnology, are expanding their applications, making them a key focus area for innovation in the bone graft substitutes market.

By Product:

Based on product, the bone graft and substitutes market is segmented into demineralized bone matrix (DBM), xenograft, autografts, synthetic bone graft, bone morphogenetic protein (BMP), non-invasive electrical bone growth stimulators, and invasive electrical bone growth stimulators.

The demineralized bone matrix (DBM) segment accounted for the largest revenue share in 2024.

- Demineralized bone matrix (DBM) is extensively utilized in orthopedic and spinal surgeries due to its osteoconductive and osteoinductive properties, which promote bone healing and regeneration.

- DBM is derived from allograft bone and processed to remove minerals, leaving behind growth factors that stimulate new bone formation.

- It is widely adopted for its ease of use, availability in various forms such as putty and gel, and lower risk of complications compared to autografts.

- The increasing prevalence of bone-related disorders and the rising bone regeneration material market trends for minimally invasive procedures have driven the dominance of DBM in the market.

The synthetic bone graft segment is anticipated to register the fastest CAGR during the forecast period.

- Synthetic bone grafts are gaining traction due to their biocompatibility, availability, and ability to mimic natural bone structure.

- These grafts, composed of materials such as calcium phosphate, hydroxyapatite, and bioactive glass, are increasingly used in spinal fusion, joint reconstruction, and dental implants.

- Their controlled composition reduces the risk of disease transmission and immune rejection, making them a preferred choice in complex procedures.

- Innovations in synthetic graft materials analysis, including the development of bioactive and biodegradable options, are expected to propel their rapid adoption in the coming years.

By Application:

Based on application, the bone graft substitutes market is segmented into spinal fusion, dental implants, joint reconstruction, craniomaxillofacial surgery, trauma repair, and others.

The spinal fusion segment accounted for the largest revenue of bone regeneration material share in 2024.

- Spinal fusion is a leading application for bone graft substitutes, driven by the rising prevalence of degenerative spine conditions, injuries, and deformities.

- Bone graft substitutes play a crucial role in achieving successful fusion by facilitating bone growth between vertebrae and enhancing stability.

- The widespread adoption of minimally invasive spinal fusion techniques has increased the demand for high-quality substitutes, including DBM and BMP, which enhance osteoinductivity and improve outcomes.

- Additionally, the increasing number of spinal surgeries performed globally, particularly in geriatric and obese populations, has solidified the segment’s dominance.

The dental implants segment is anticipated to register the fastest CAGR during the forecast period.

- Dental implants rely heavily on bone graft substitutes to restore the alveolar bone structure, ensuring proper implant integration and long-term stability.

- The use of synthetic materials like hydroxyapatite and bioactive glass in dental grafting procedures has gained significant traction due to their biocompatibility and ability to support osseointegration.

- The rising demand for dental restorations and cosmetic procedures, coupled with growing awareness of advanced dental care solutions, is driving the adoption of bone graft substitutes in this segment.

- Innovations such as injectable graft materials and guided bone regeneration techniques are further enhancing developmental prospects.

By End-User Industry:

Based on end-use, the bone graft substitutes market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and research institutes.

The hospitals segment accounted for the largest revenue share in 2024.

- Hospitals remain the largest end-users of bone graft substitutes, driven by the high volume of complex orthopedic, spinal, and trauma procedures performed in these facilities.

- Hospitals are equipped with advanced technologies and multidisciplinary expertise, enabling successful surgical outcomes for challenging cases.

- The availability of inpatient care and advanced imaging systems supports the effective use of bone graft substitutes in hospitals.

- Additionally, the growing number of hospital-based orthopedic and dental centers, especially in developed regions, has reinforced their leading position in the market.

The specialty clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialty clinics focusing on orthopedics and dental care are becoming prominent consumers of bone graft substitutes due to their tailored services and outpatient capabilities.

- These clinics provide a cost-effective and patient-centric approach, enabling minimally invasive procedures with faster recovery times.

- The rise in dental tourism, especially in emerging economies, is driving trends for high-quality substitutes in dental procedures.

- Similarly, orthopedic specialty clinics are increasingly adopting advanced materials like BMP and composite grafts to enhance surgical precision and patient outcomes, contributing to the segment's rapid expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

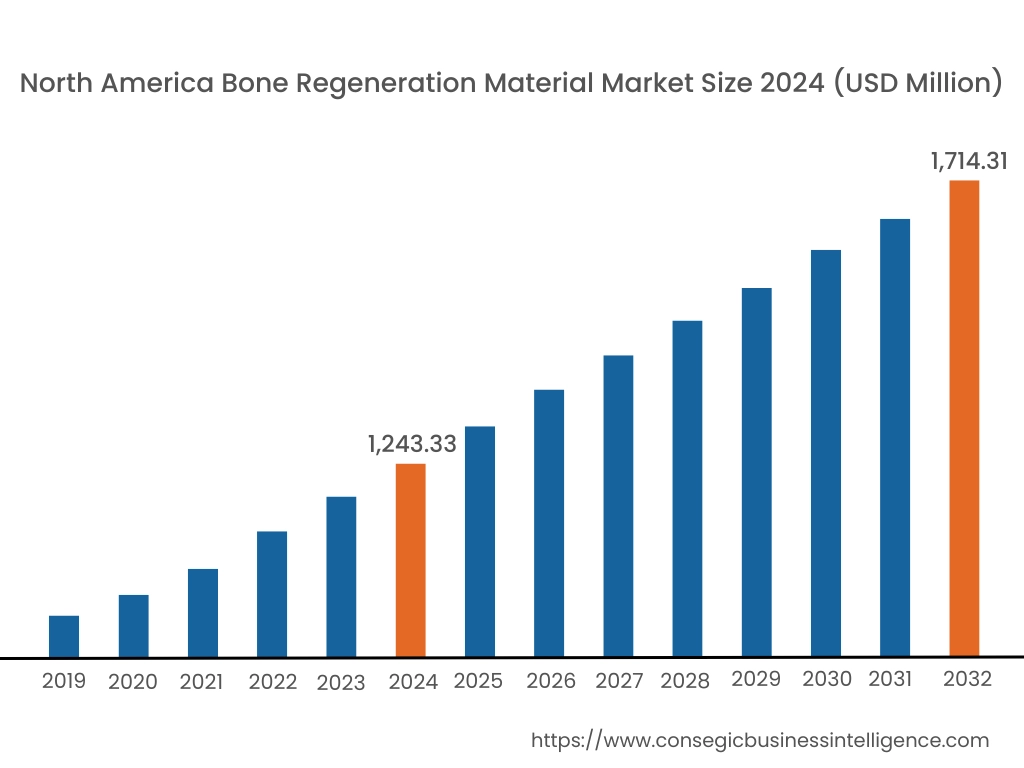

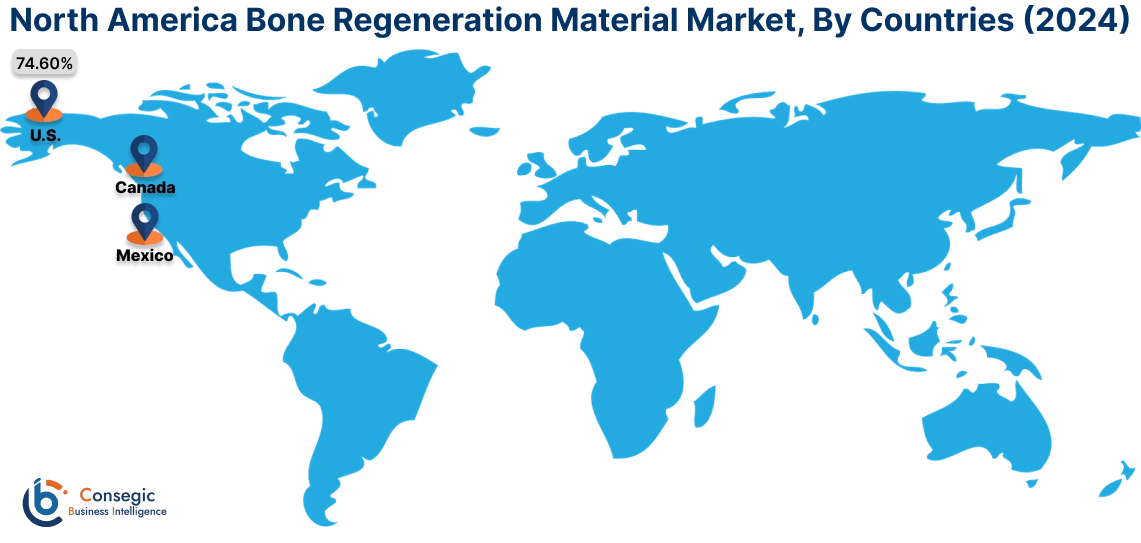

In 2024, North America was valued at USD 1,243.33 Million and is expected to reach USD 1,714.31 Million in 2032. In North America, the U.S. accounted for the highest share of 74.60% during the base year of 2024. North America holds a significant stake in the bone regeneration material market analysis, driven by advancements in healthcare infrastructure and the increasing prevalence of orthopedic conditions such as osteoporosis and bone fractures. The U.S. leads the region due to a high volume of orthopedic and dental surgeries, along with the growing adoption of advanced materials like synthetic grafts and bioactive ceramics. The region benefits from robust R&D investments in regenerative medicine and high patient awareness. Canada contributes to the market with increasing dental implant procedures and demand for bone graft substitutes. However, the high costs of advanced materials and procedures may limit broader accessibility.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.8% over the forecast period. In the bone regeneration material market analysis, fueled by rapid urbanization, increasing healthcare investments, and a growing prevalence of bone-related disorders in China, India, and Japan. China dominates the market with rising trends for bone graft substitutes due to its aging population and increasing number of orthopedic procedures. India’s expanding healthcare infrastructure supports the adoption of cost-effective bone regeneration materials, particularly in trauma and dental surgeries. Japan emphasizes advanced biomaterials and stem-cell-based solutions for bone regeneration, leveraging its strong research capabilities. However, limited patient awareness and affordability issues in rural areas may hinder bone regeneration material market expansion in some parts of the region.

Europe is a prominent market analysis of bone regeneration, supported by its aging population, advanced medical technologies, and increasing cases of bone disorders. Countries like Germany, France, and the UK are key contributors. Germany drives bone regeneration material market demand through its well-established orthopedic and dental sectors, focusing on synthetic and natural graft materials for reconstructive surgeries. France emphasizes the use of bioactive materials in dental and maxillofacial procedures, while the UK sees a growing adoption of regenerative solutions in trauma and spinal surgeries. However, strict regulatory frameworks and high approval costs for new materials may pose challenges to manufacturers.

The Middle East & Africa region is witnessing steady growth in the bone regeneration material market, driven by increasing healthcare investments and rising cases of trauma and bone diseases. In the Middle East, countries like Saudi Arabia and the UAE are adopting advanced bone graft materials for orthopedic and dental procedures, supported by growing medical tourism and healthcare infrastructure. In Africa, South Africa is emerging as a market, focusing on affordable solutions for trauma care and reconstructive surgeries. However, limited access to advanced medical facilities and reliance on imports for high-quality materials may restrict broader market development.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s growing healthcare sector and an increasing number of orthopedic surgeries drive bone regeneration material market demand for bone graft substitutes and bioactive materials. Mexico emphasizes the use of these materials in dental implants and trauma care, supported by a growing middle-class population seeking advanced healthcare solutions. However, economic instability and inconsistent healthcare infrastructure in some countries may pose challenges to bone regeneration material market expansion.

Top Key Players and Market Share Insights:

The bone regeneration material market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the bone regeneration material market. Key players in the bone regeneration material industry include -

- Johnson & Johnson (USA)

- Medtronic PLC (Ireland)

- Stryker Corporation (USA)

- Smith & Nephew plc (UK)

- Zimmer Biomet (USA)

- Integra Lifesciences Holdings Corporation (USA)

- Geistlich Pharma AG (Switzerland)

- NovaBone (USA)

- Citagenix (Canada)

- Sigma Graft (USA)

Bone Regeneration Material Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 31,616.84 Million |

| CAGR (2025-2032) | 12.1% |

| By Material Type |

|

| By Product |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Bone Regeneration Material Market by 2032? +

Bone Regeneration Material Market size is estimated to reach over USD 5,289.46 Million by 2032 from a value of USD 3,748.26 Million in 2024 and is projected to grow by USD 3,846.40 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

What are the primary applications of bone regeneration materials? +

Applications include spinal fusion, dental implants, joint reconstruction, craniomaxillofacial surgery, trauma repair, and others requiring effective bone healing and regeneration.

What factors are driving the growth of the bone regeneration material market? +

The rising incidence of bone-related disorders, advancements in biomaterials technology, and increasing adoption of minimally invasive surgical procedures are key growth drivers.