- Summary

- Table Of Content

- Methodology

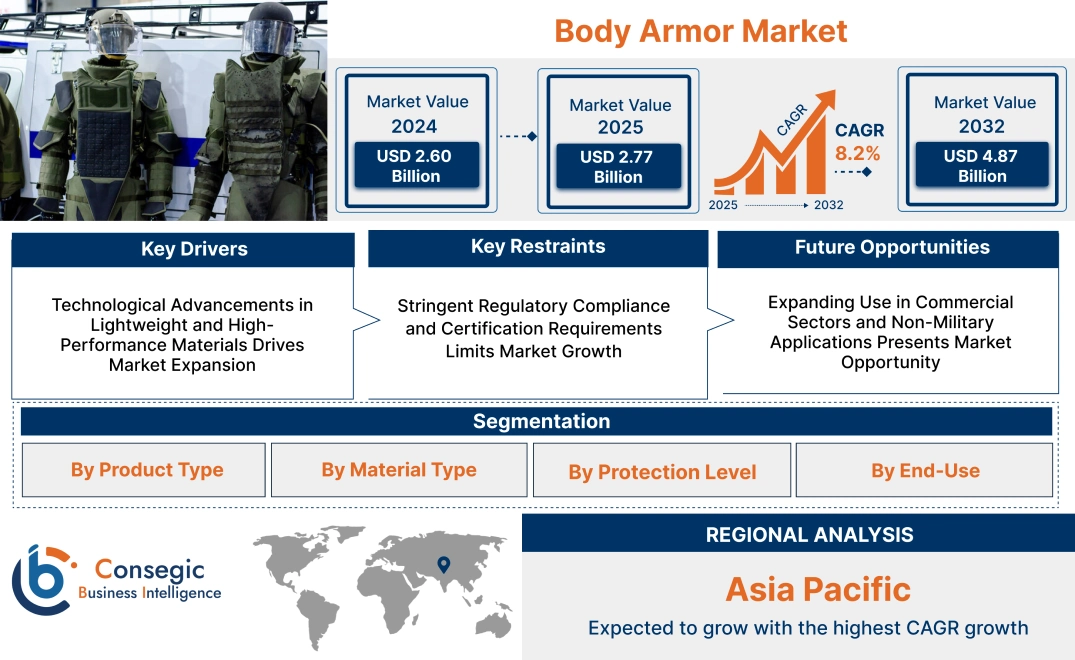

Body Armor Market Size:

The global body armor market size is estimated to reach over USD 4.87 Billion by 2032 from a value of USD 2.60 Billion in 2024 and is projected to grow by USD 2.77 Billion in 2025, growing at a CAGR of 8.2% from 2025 to 2032.

Body Armor Market Scope & Overview:

Body armor is a protective system designed to safeguard individuals from ballistic, stab and impact threats. They are widely used by military forces, law enforcement agencies, and security personnel. It is manufactured using advanced materials such as aramid fibers, ultra-high-molecular-weight polyethylene (UHMWPE), ceramics, and composite fabrics, offering a balance between durability, flexibility, and weight reduction. Different protection levels are available, ranging from soft armor designed for lower-caliber threats to hard armor capable of stopping high-velocity projectiles.

Key features include lightweight construction, modular attachments, multi-threat resistance, and customizable fit for enhanced mobility. Modern designs incorporate trauma-reducing technology, moisture-wicking fabrics, and ventilation systems to improve comfort during extended use. Some variants also offer compatibility with tactical gear, communication systems, and additional protective accessories.

Furthermore, it ensures operational safety without compromising agility. Ongoing advancements in material technology and ballistic resistance continue to improve its effectiveness, making it a crucial component in personal defense and tactical applications.

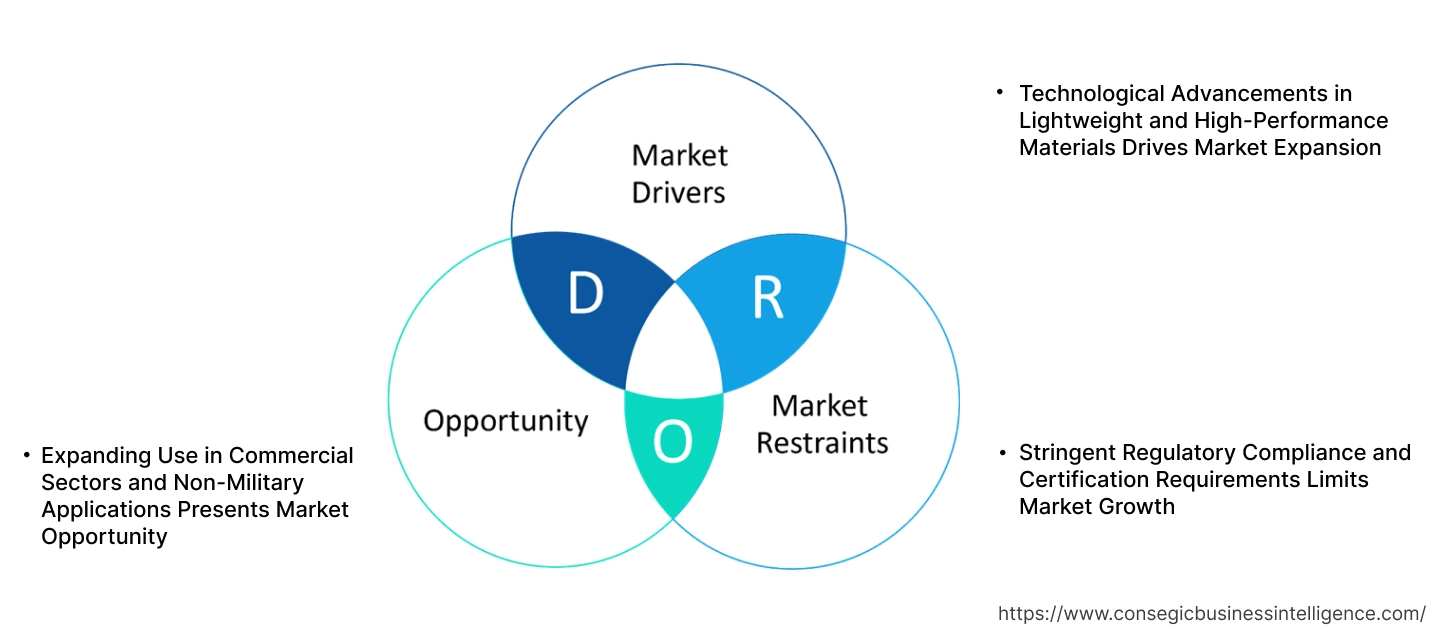

Body Armor Market Dynamics - (DRO):

Key Drivers:

Technological Advancements in Lightweight and High-Performance Materials Drives Market Expansion

Traditional body armor relied on bulky and rigid materials, which limited flexibility and prolonged wearability. Innovations in aramid fibers, ultra-high-molecular-weight polyethylene (UHMWPE), graphene composites, and liquid armor technologies are now enabling the manufacture of better quality products. These materials offer superior ballistic resistance while significantly reducing weight, improving user comfort and operational efficiency in high-risk environments. The demand for advanced, multi-threat protection solutions is increasing as security forces require gear that provides defense against multiple different impact threats without compromising agility. Additionally, modular armor systems with customizable protection levels are gaining traction. As material science continues to evolve, these technological advancements are expected to drive body armor market growth, ensuring broader adoption across multiple industries.

Key Restraints:

Stringent Regulatory Compliance and Certification Requirements Limits Market Growth

Safety standards such as NIJ (National Institute of Justice) ballistic ratings, ISO certifications, and military-grade specifications mandate rigorous testing, material validation, and quality control procedures before products are approved for deployment. These processes increase production costs, development timelines, and compliance expenses, making it difficult for new entrants to compete with established manufacturers. The demand for advanced protective solutions is rising across military, law enforcement, and private security sectors, but varying regulations across different regions create additional barriers to global distribution. Frequent updates to safety protocols require continuous material research, re-certification, and performance enhancements, further adding to operational complexity. Companies must invest heavily in R&D, testing infrastructure, and third-party validation to meet evolving standards, impacting scalability. Overcoming these compliance hurdles is essential for body armor market expansion, ensuring broader accessibility without compromising safety.

Future Opportunities:

Expanding Use in Commercial Sectors and Non-Military Applications Presents Market Opportunity

Sectors such as construction, mining, manufacturing, and hazardous material handling are increasingly integrating lightweight impact-resistant protective gear to enhance worker safety. Additionally, the sports, adventure, and motorcycling industries are witnessing a surge in demand for protective clothing embedded with high-performance ballistic and stab-resistant materials to prevent injuries. With rising concerns about workplace accidents and occupational hazards, businesses are adopting advanced protective equipment that offers both, flexibility and durability. Furthermore, the rise in private security services, personal protection solutions, and high-risk civilian professions is driving the adoption of discreet, concealable armor solutions. The growth of urban safety initiatives, along with stricter workplace safety regulations, is further fueling demand for these solutions. Increasing commercial adoption is expected to boost body armor market opportunities, ensuring broader accessibility and application diversity.

Body Armor Market Segmental Analysis :

By Product Type:

Based on product type, the body armor market is divided into soft, hard, and composite types.

The hard body armor formed the largest segment in 2024.

- Hard body armor is widely used in military and defense applications, providing high ballistic resistance and enhanced durability.

- The demand for advanced, lightweight hard armor plates is increasing due to the growing need for soldier protection in active combat zones.

- The development of multi-hit ceramic and UHMWPE-based plates is improving operational effectiveness and reducing mobility constraints.

- Segmental analysis indicates that innovations in material technology and modular armor systems are driving market trends toward more adaptable solutions.

The composite body armor segment is expected to experience the fastest CAGR during the forecast period.

- Composite armor offers an optimal balance between protection and weight, making it ideal for special operations forces and law enforcement agencies.

- Body armor market growth is influenced by the rising adoption of hybrid armor solutions, which incorporate ceramic, polymer, and fiber-based composites.

- The need for ergonomic, high-mobility armor is accelerating the development of next-generation composite protective gear.

- The body armor market trends indicate that the growth of hybrid armor systems in tactical operations will continue in the upcoming years.

By Material Type:

By material type, the market is segmented into aramid, ultra-high-molecular-weight polyethylene (UHMWPE), ceramic, steel, and others.

The aramid segment held the largest revenue of the body armor market share in 2024.

- Aramid fibers, such as Kevlar, are widely used in soft body armor and tactical vests, offering high tensile strength and lightweight protection.

- Law enforcement and security personnel rely heavily on aramid-based armor due to its flexibility and ability to stop handgun rounds effectively.

- The need for lightweight, breathable solutions is driving the continued adoption of aramid-based protective gear.

- In April 2023, DuPont launched Kevlar® EXO™, a next-generation aramid fiber that offers unmatched protection, lightness and flexibility. It offers the highest ballistics performance among the current aramid fibers without compromising on weight, peak flexibility and durability with flame- and temperature-resistance.

- Body armor market analysis indicates that aramid fibers will remain dominant, particularly in covert and high-mobility applications.

The UHMWPE segment is anticipated to have the fastest CAGR during the forecast period.

- UHMWPE is gaining traction due to its high strength-to-weight ratio, making it an ideal material for both soft and hard armor applications.

- The increasing UHMWPE adoption is fueled by next-generation lightweight ballistic protection requirements in military and special forces units.

- Advances in fiber weaving technology and impact-resistant polymer composites are enhancing UHMWPE’s protective capabilities.

- Market trends suggest that the transition from traditional materials to UHMWPE-based solutions will accelerate due to weight reduction initiatives in defense and law enforcement sectors.

By Protection Level:

Based on protection level, the body armor market is categorized into Level I, Level II, Level IIIA, Level III, and Level IV.

The Level III segment held the largest revenue share in 2024.

- Level III armor protects against rifle rounds, making it the standard for military and law enforcement tactical operations.

- The need for high-performance products capable of stopping multiple ballistic threats is driving Level III armor adoption.

- Military modernization programs across North America, Europe, and Asia-Pacific are leading to increased procurement of Level III body armor solutions.

- Market analysis highlights the rise of modular armor plates, allowing for customizable protection levels based on mission requirements.

The Level IV share is anticipated to experience the fastest CAGR during the forecast period.

- Level IV type offers the highest level of ballistic protection, designed to withstand armor-piercing rounds.

- The body armor market demand for advanced personal protective equipment in high-risk combat zones is fueling the adoption of Level IV solutions.

- The increasing investment in next-generation military gear and reinforced plates is driving the market toward higher protection standards.

- Segmental trends analysis suggests that Level IV armor will continue expanding, particularly among special forces and defense contractors seeking enhanced protective capabilities.

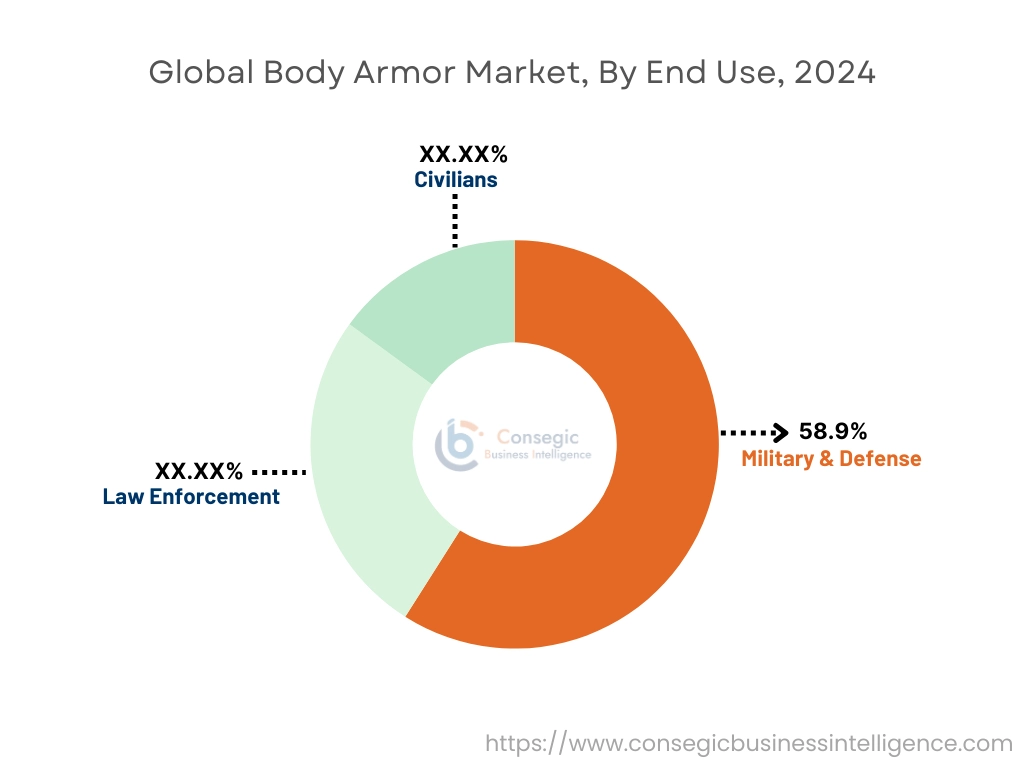

By End-Use:

By end-use, the market is divided into military & defense and civilians.

The military & defense segment held the largest revenue of body armor market share by 58.9% in 2024.

- Military forces worldwide rely on advanced body armor for protection against ballistic threats, shrapnel, and explosive impacts.

- Government initiatives focusing on troop safety, tactical gear modernization, and next-generation combat wearables are fueling requirements.

- Body armor market trends highlight the increasing role of AI-driven sensor integration in modern military armor systems.

- Market analysis suggests that continuous innovation in armor materials, including graphene-reinforced composites, will enhance future protective gear.

The civilian segment is expected to have the fastest CAGR during the forecast period.

- The rising demand for personal protective equipment among private security personnel, journalists, and law-abiding civilians is boosting body armor market expansion.

- Market trends indicate a growing preference for discreet, lightweight armor solutions, particularly in urban security environments.

- The need for flexible, concealed armor vests is increasing as civilians seek added protection in high-risk zones.

- Body armor market analysis shows a rising number of civilian purchases, driven by safety concerns and regulatory shifts allowing civilian access to ballistic protection.

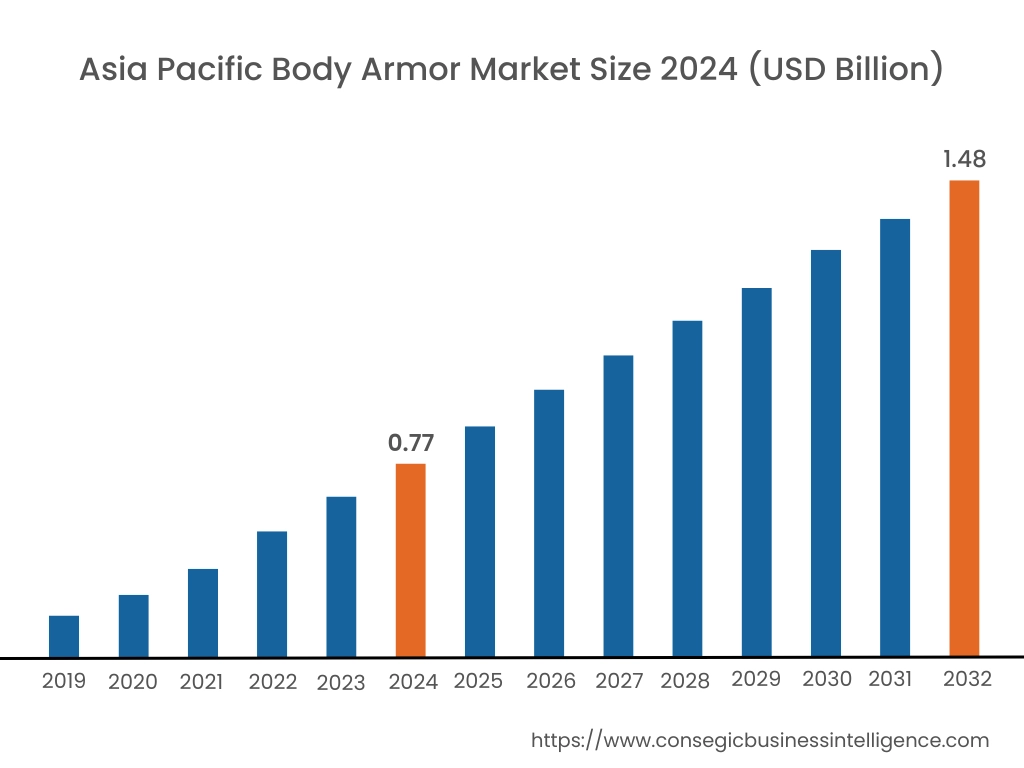

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

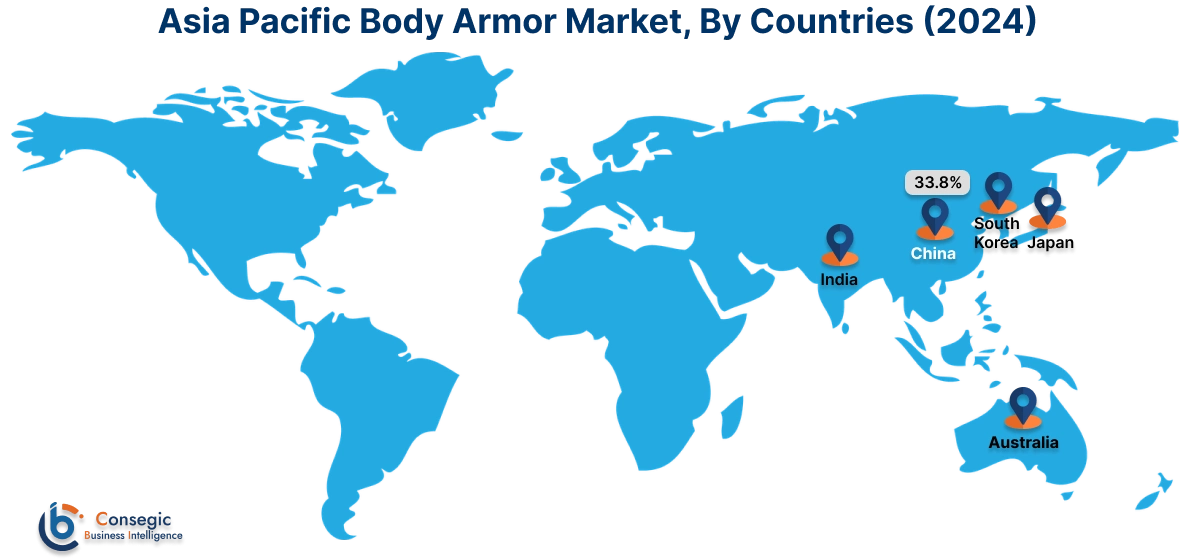

Asia Pacific region was valued at USD 0.77 Billion in 2024. Moreover, it is projected to grow by USD 0.82 Billion in 2025 and reach over USD 1.48 Billion by 2032. Out of this, China accounted for the maximum revenue share of 33.8%. The Asia-Pacific region is witnessing the fastest growth in the market, fueled by increasing defense expenditures, law enforcement modernization, and a rise in cross-border tensions. China and India are dominating with large-scale procurement programs aimed at equipping military personnel with advanced protective gear. India’s Make in India initiative has encouraged domestic product manufacturing, reducing reliance on imports while fostering innovation in bulletproof and shrapnel-resistant gear. Meanwhile, Japan and South Korea are incorporating lightweight, high-durability materials in military armor to improve mobility in combat scenarios. Another notable trend in the region is the requirement for cost-effective armor solutions tailored for paramilitary forces and private security firms. Additionally, rising security concerns in Southeast Asia have led to greater adoption of tactical vests and ballistic shields among law enforcement agencies. The body armor market opportunity in Asia-Pacific is vast, particularly in emerging economies where modernization efforts and national security threats continue to shape procurement priorities.

North America is estimated to reach over USD 1.58 Billion by 2032 from a value of USD 0.86 Billion in 2024 and is projected to grow by USD 0.92 Billion in 2025.

North America leads the body armor market demand, driven by extensive defense budgets, high procurement rates, and technological innovation. The United States plays a crucial role, with the Department of Defense (DoD) and Department of Homeland Security (DHS) investing in next generation solutions to provide military personnel and law enforcement officers with superior protection. Bulletproof vests, tactical gear, and stab-resistant armor are highly sought after, particularly in urban policing and counterterrorism operations. Lightweight, flexible armor with enhanced ballistic resistance is a key focus area for research and development. Additionally, Canadian law enforcement agencies are modernizing their protective equipment, contributing to the region’s steady growth. The presence of industry leaders engaged in manufacturing and research, combined with strong regulatory safety mandates, further consolidates North America's position as a global leader in the market.

In Europe, the market is shaped by regulatory-driven advancements, military procurement programs, and increasing security threats. Countries such as Germany, the United Kingdom, and France are investing in product development that aligns with NATO standards and EU safety directives. The heightened risk of terrorist activities, urban crime, and border security challenges has increased the adoption of protective gear among law enforcement agencies. A growing trend is the integration of smart materials, including nanotechnology-based fabrics that enhance flexibility without compromising protection. Additionally, the rise of peacekeeping missions and military deployments in international conflict zones has driven the need for modular and adaptive armor systems. European manufacturers are focusing on sustainable, high-performance materials, aligning with the region’s stringent environmental regulations. The growth of this sector in Europe is also supported by public-private collaborations that facilitate innovation in ballistic-resistant clothing and stab-proof tactical vests.

The Middle East & Africa region is characterized by high military spending, ongoing geopolitical conflicts, and growing concerns about insurgency threats. Countries such as Saudi Arabia, the UAE, and Israel are investing heavily in advanced armor technologies, including ceramic and composite-based body armor designed for extreme conditions. Law enforcement agencies across the Middle East are strengthening their tactical capabilities, leading to increased procurement of lightweight and modular armor systems. In Africa, rising concerns over organized crime, terrorism, and internal conflicts have prompted governments to equip military and police forces with enhanced protective gear. However, logistical challenges and budgetary constraints in some African nations hinder widespread adoption. Despite these limitations, opportunities exist for international manufacturers to introduce affordable, durable, and climate-resistant solutions tailored to the region’s specific needs. The adoption of international ballistic standards is also influencing purchasing decisions in both military and private security sectors.

Latin America presents an evolving market, largely driven by law enforcement agencies, private security firms, and military forces tackling organized crime and internal unrest. Brazil, Mexico, and Colombia are leading markets, with government agencies focusing on equipping police forces with ballistic-resistant gear to combat rising crime rates. One of the key trends in this region is the increasing requirement for a product that offers protection against both firearms and edged weapons. Additionally, paramilitary forces and private security personnel in high-risk areas are driving market demand for lightweight, concealable armor solutions. Latin American governments are also strengthening collaborations with international manufacturers to improve the quality and availability of protective equipment. However, fluctuating economic conditions and inconsistent regulatory enforcement pose challenges to market stability. Investment in local manufacturing capabilities and training programs for proper usage of the product will be critical in sustaining development in this region.

Top Key Players & Market Share Insights:

The body armor market is highly competitive, with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global market. Key players in the body armor industry include -

- Honeywell International Inc. (USA)

- 3M Company (USA)

- Samyang Comtech Co., Ltd. (South Korea)

- EnGarde (Netherlands)

- DFNDR Armor (USA)

- MKU Ltd. (India)

- Armor Express (USA)

- Safariland (USA)

- Point Blank Enterprises (USA)

- BAE Systems (UK)

Recent Industry Developments :

Partnerships & Collaborations:

- In January 2025, DuPont and Point Blank Enterprises announced an exclusive partnership for DuPont™ Kevlar EXO™ and showcased the new soft armor Elite EXO.

Product Launches:

- In April 2024, the Defence Research and Development Organisation (DRDO) of India successfully developed the lightest bulletproof jacket in the country for protection against the highest threat level. Based upon a new design method, the armor is made up of a monolithic ceramic plate with polymer backing which enhances wearability and comfort during the operation.

Body Armor Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4.87 Billion |

| CAGR (2025-2032) | 8.2% |

| By Product Type |

|

| By Material Type |

|

| By Protection Level |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Body Armor Market? +

The global body armor market size is estimated to reach over USD 4.87 Billion by 2032 from a value of USD 2.60 Billion in 2024 and is projected to grow by USD 2.77 Billion in 2025, growing at a CAGR of 8.2% from 2025 to 2032.

What specific segmentation details are covered in the Body Armor Market report? +

The body armor market report includes specific segmentation details for product type, material type, protection level, and end-use.

Which is the fastest-growing region in the Body Armor Market? +

Asia Pacific is the fastest-growing region in the body armor market. These trends are encouraged by increasing defense expenditures, law enforcement modernization, and a rise in cross-border tensions.

Who are the major players in the Body Armor Market? +

The key participants in the body armor market are Armor Express (USA), Safariland (USA), Point Blank Enterprises (USA), BAE Systems (UK), Honeywell International Inc. (USA), 3M Company (USA), MKU Ltd. (India), Samyang Comtech Co., Ltd. (South Korea), EnGarde (Netherlands) and DFNDR Armor (USA).