- Summary

- Table Of Content

- Methodology

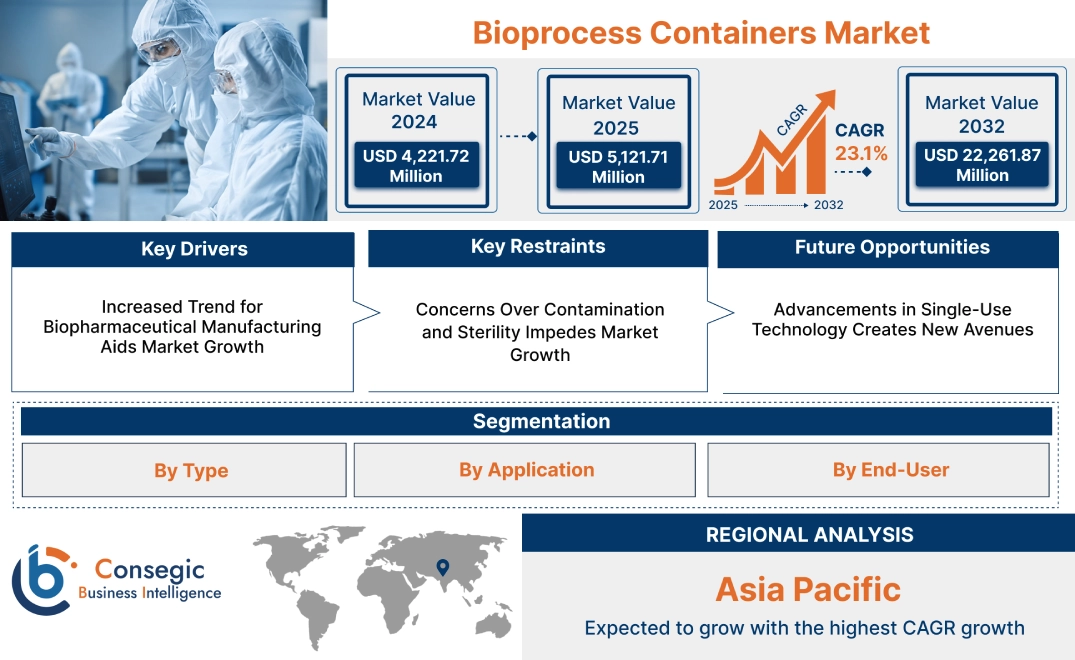

Bioprocess Containers Market Size:

Bioprocess Containers Market size is estimated to reach over USD 22,261.87 Million by 2032 from a value of USD 4,221.72 Million in 2024 and is projected to grow by USD 5,121.71 Million in 2025, growing at a CAGR of 23.1% from 2025 to 2032.

Bioprocess Containers Market Scope & Overview:

Bioprocess containers are single-use flexible containers designed for the storage, transportation, and handling of liquids in biopharmaceutical manufacturing. These containers are made from high-grade polymer films that ensure sterility, durability, and compatibility with biologics. Key features of bioprocess containers include leak-proof construction, customizable designs, and scalability to meet varying production needs. These containers reduce the risk of cross-contamination and simplify cleaning and sterilization processes.

The benefits of bioprocess containers include cost efficiency, enhanced operational flexibility, and reduced downtime in bioprocessing workflows. They support the manufacturing of vaccines, monoclonal antibodies, and other biologics. Applications span pharmaceutical production, biotechnology research, and clinical trials. End-use industries include biopharmaceutical companies, research institutions, and contract manufacturing organizations seeking reliable single-use solutions.

Bioprocess Containers Market Dynamics - (DRO) :

Key Drivers:

Increased Trend for Biopharmaceutical Manufacturing Aids Market Growth

Biopharmaceuticals are at the forefront of medical advancements, with growing bioprocess containers market trend for treatments such as monoclonal antibodies, vaccines, and gene therapies. The manufacturing of these biologic products requires a highly specialized process that involves the use of bioprocess containers, such as bags, vessels, and tubing. These containers are essential in bioreactors, where the cell cultures and biochemical reactions take place. The trend towards biopharmaceuticals is fueled by the growing global need for advanced treatments for chronic diseases, cancer, and infectious diseases.

For example, during the COVID-19 pandemic, bioprocess containers played a crucial role in vaccine production, facilitating the rapid scaling of vaccine manufacturing.

Thus, as biopharmaceutical production continues to expand, the trend for bioprocess containers rises, significantly driving bioprocess containers market growth.

Key Restraints:

Concerns Over Contamination and Sterility Impedes Market Growth

Bioprocess containers are crucial in maintaining sterile environments during the production of biopharmaceuticals. However, contamination risks remain a major concern. Any failure in the sterility of containers can result in costly production setbacks, compromised product quality, and potential harm to patients. The complex nature of biologic manufacturing means that even slight contamination can disrupt entire production batches. This leads to stringent regulations and extensive validation processes for these containers.

Consequently, the fear of contamination can hinder the widespread adoption of bioprocess containers, especially among companies looking to scale production quickly. Therefore, concerns over contamination and sterility slow the growth of the market.

Future Opportunities:

Advancements in Single-Use Technology Creates New Avenues

Single-use bioprocess containers are emerging as a more efficient and cost-effective solution for biopharmaceutical production. Unlike traditional stainless-steel vessels, these disposable containers eliminate the need for cleaning and sterilization between uses, reducing operational costs and time. The growing trend towards single-use technologies offers significant bioprocess containers market opportunities for innovation in container design, material selection, and functionality. For example, new materials that offer enhanced durability and better resistance to chemical reactions are being developed.

As single-use bioprocess containers become more widely adopted and improved, they present significant opportunities for growth in the market. These innovations are expected to further streamline manufacturing processes and reduce costs, making them increasingly attractive to biopharmaceutical companies.

Bioprocess Containers Market Segmental Analysis :

By Type:

Based on type, the market is segmented into 2D bioprocess containers, 3D bioprocess containers, and accessories.

The 2D bioprocess containers sector accounted for the largest revenue in bioprocess containers market share in 2024.

- 2D bioprocess containers are widely used in cell culture processes for pharmaceutical production. They are designed for easy manipulation of media and cell growth, which is critical in biopharmaceutical manufacturing.

- These containers offer several advantages, including scalability, ease of use, and cost-effectiveness. They are primarily used for the storage and transportation of raw materials, culture media, and intermediates in biopharmaceutical production.

- The increasing bioprocess containers market demand for biologics and monoclonal antibodies has driven the adoption of 2D containers as they provide a reliable and efficient solution for cultivating cells in large-scale processes.

- As the demand for advanced therapies increases, the segment is expected to maintain a dominant position in the market.

- Therefore, according to bioprocess containers market analysis, the 2D bioprocess containers segment remains the market leader due to its established use in biopharmaceutical manufacturing and scalability advantages.

The 3D bioprocess containers sector is anticipated to register the fastest CAGR during the forecast period.

- 3D bioprocess containers are gaining popularity as they offer enhanced cell culture conditions, mimicking the natural growth environment for cells. This is crucial for producing high-quality therapeutic proteins and vaccines.

- Their ability to support complex bioprocesses such as tissue engineering and regenerative medicine makes them a valuable asset in the growing field of personalized medicine.

- Technological advancements in 3D cell culture systems, such as microcarrier technology and bioreactor development, are driving the bioprocess containers market demand for 3D bioprocess containers.

- As the biotechnology industry expands, particularly in the fields of gene therapy and cell-based therapies, 3D containers are expected to see rapid adoption.

- Thus, according to bioprocess containers market analysis, the 3D bioprocess containers sector is poised for significant growth, driven by innovations in cell culture techniques and the increasing need for advanced therapeutic applications.

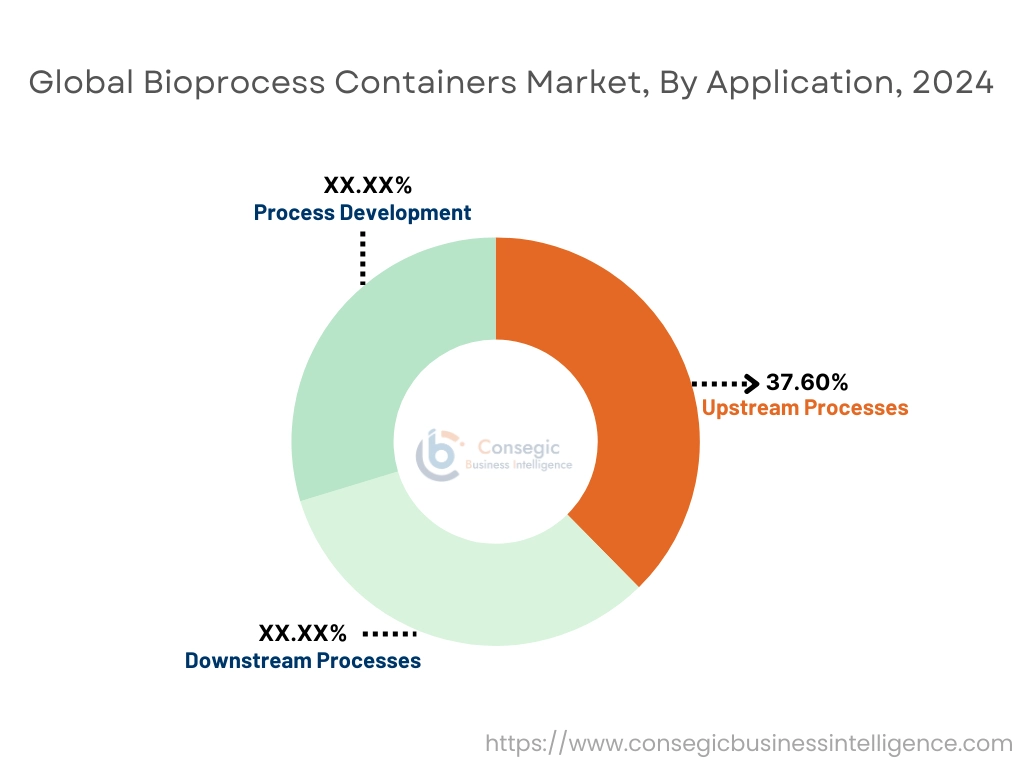

By Application:

Based on application, the market is segmented into upstream processes, downstream processes, and process development.

The upstream processes sector accounted for the largest revenue in bioprocess containers market share by 37.60% in 2024.

- Upstream processes in biopharmaceutical manufacturing involve cell culture and fermentation, where bioprocess containers play a vital role in cultivating cells and microorganisms.

- Bioreactors and cell culture bags are key components in the upstream process, supporting cell growth and media exchange, which is essential for producing biopharmaceutical products.

- The growing demand for monoclonal antibodies, vaccines, and other biologic drugs is driving the need for efficient upstream processing technologies.

- Furthermore, the increasing shift towards biologics in the pharmaceutical industry has led to a greater emphasis on upstream process optimization, boosting the bioprocess containers market trend for bioprocess containers in this application.

- Therefore, according to market analysis, the upstream processes segment continues to dominate the market due to the increasing demand for biologics and the critical role of bioprocess containers in cell culture operations.

The downstream processes sector is anticipated to register the fastest CAGR during the forecast period.

- Downstream processes are focused on the purification and separation of the biologic products generated in upstream processes. Bioprocess containers are essential for storage, filtration, and final formulation of the drug product.

- As the biopharmaceutical industry grows, the need for efficient purification techniques and the development of high-quality therapeutics are driving the expansion of the downstream processes segment.

- Advancements in filtration and chromatography technologies are fuelling bioprocess containers market expansion for containers that can handle the more complex separation processes involved in downstream production.

- Thus, according to market analysis, the downstream processes segment is expected to experience rapid growth, driven by the increasing need for purification and final product formulation in biopharmaceutical production.

By End-User:

Based on end-user, the market is segmented into biopharmaceutical companies, life science R&D companies, and others.

The biopharmaceutical companies sector accounted for the largest revenue share in 2024.

- Biopharmaceutical companies are the largest consumers of bioprocess containers, utilizing them in the production of vaccines, therapeutic proteins, and monoclonal antibodies.

- The growth of biologics and the ongoing demand for new treatments have made biopharmaceutical companies the primary end-users of bioprocess containers. The continuous expansion of the global pharmaceutical market further strengthens this trend.

- These companies rely on bioprocess containers for both large-scale production and the storage and transportation of biological products, making them integral to the overall manufacturing process.

- Therefore, according to market analysis, the biopharmaceutical companies segment remains the market leader, driven by the increasing demand for biologics and the essential role of bioprocess containers in large-scale manufacturing.

The life science R&D companies sector is anticipated to register the fastest CAGR during the forecast period.

- Life science R&D companies utilize bioprocess containers for laboratory-scale cell culture, protein production, and research applications. These containers are integral to research in fields such as drug discovery, gene therapy, and vaccine development.

- The increasing number of biotechnology research projects, as well as advancements in personalized medicine, are driving the demand for bioprocess containers in this sector.

- Furthermore, as the life sciences industry continues to expand globally, the need for efficient and scalable research tools like bioprocess containers will drive substantial growth.

- Thus, according to market analysis, the life science R&D companies segment is expected to grow rapidly, driven by the ongoing advancements in research and the increasing demand for biopharmaceutical and biotechnology innovations.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

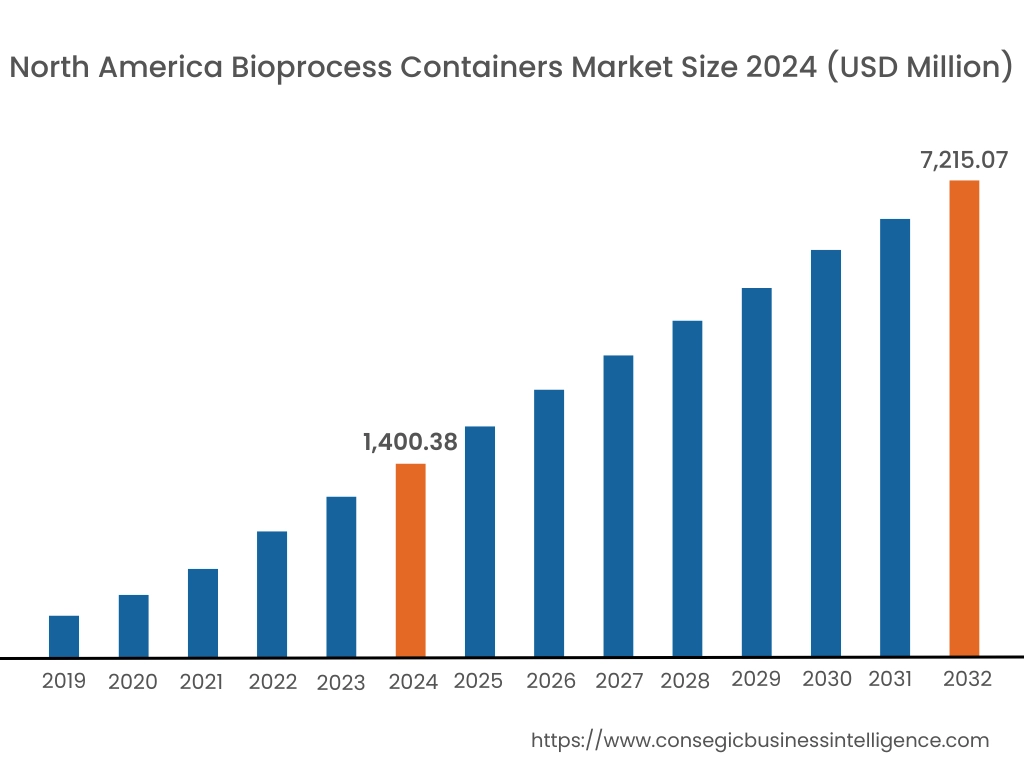

In 2024, North America was valued at USD 1,400.38 Million and is expected to reach USD 7,215.07 Million in 2032. In North America, the U.S. accounted for the highest share of 72.15% during the base year of 2024. North America leads the bioprocess containers market due to strong demand from the biotechnology and pharmaceutical industries. The United States plays a significant role, with extensive use of bioprocess containers in drug development, cell culture, and vaccine production. The presence of major biopharmaceutical companies and advanced healthcare infrastructure contributes to bioprocess containers market growth. Additionally, investments in biomanufacturing technologies and increasing research activities further enhance the demand for bioprocess containers in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 23.6% over the forecast period. The Asia-Pacific region exhibits notable growth potential in the bioprocess containers market, driven by rapid industrialization, increasing healthcare investments, and growing demand for biologics. Countries like China, India, and Japan are experiencing expanding biotechnology sectors and improvements in healthcare facilities. The region's rising manufacturing capabilities and adoption of advanced biotechnologies are factors that positively impact the demand for bioprocess containers. However, challenges remain in terms of standardization and regulatory concerns in some areas.

Europe maintains a significant share in the bioprocess containers market, supported by a robust pharmaceutical and biotechnology industry. Leading countries like Germany, the United Kingdom, and France continue to advance biomanufacturing processes, creating high demand for bioprocess containers. The region benefits from stringent regulatory standards that encourage the adoption of standardized, safe containers. Additionally, increasing investment in biologic drug production and research into advanced therapeutics further strengthens market dynamics in Europe.

The Middle East and Africa show moderate growth in the bioprocess containers market. While healthcare infrastructure in countries like the United Arab Emirates and Saudi Arabia is improving, challenges persist in many African regions. However, increasing government investments in healthcare and biotechnology sectors are driving market demand. The growing interest in biologic drug production in the Middle East, particularly in Saudi Arabia, presents opportunities for bioprocess containers market expansion. In Africa, the limited number of biopharmaceutical companies slows market uptake.

Latin America is witnessing gradual market development, with countries like Brazil and Mexico leading the charge in bioprocess container adoption. Rising demand for biologic drugs, especially in vaccine production, and government efforts to improve healthcare systems are important factors affecting the market. However, limited access to advanced manufacturing technologies and regional disparities in healthcare infrastructure pose challenges. Increased focus on public-private partnerships and investments in biotechnology industries are expected to positively impact market growth in Latin America.

Top Key Players & Market Share Insights:

The Global Bioprocess Containers Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Bioprocess Containers Market. Key players in the Bioprocess Containers industry include-

- Sartorius AG (Germany)

- Thermo Fisher Scientific Inc. (United States)

- Merck Group (Germany)

- Becton, Dickinson and Company (United States)

- Pall Corporation (United States)

- Corning Incorporated (United States)

- Lonza Group (Switzerland)

- Eppendorf AG (Germany)

- Danaher Corporation (United States)

- Starlim Spritzguss GmbH (Austria)

Recent Industry Developments :

Product Launches:

- In April 2023, Merck introduced the Ultimus Single-Use Process Container Film, designed to enhance leak resistance and durability for bioprocessing liquids. This innovation aims to improve operational efficiency and support healthy cell growth.

Mergers and Acquisitions:

- In November 2024, Amcor PLC agreed to acquire Berry Global Group Inc. for approximately $8.4 billion in stock. This merger aims to enhance Amcor's presence in the U.S. by incorporating Berry Global's strengths in consumer packaging and health and hygiene containers. The combined entity is expected to accelerate innovation in sustainable packaging and expand product offerings.

Bioprocess Containers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 22,261.87 Million |

| CAGR (2025-2032) | 23.1% |

| By Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Bioprocess Containers Market? +

In 2024, the Bioprocess Containers Market was USD 4,221.72 million.

What will be the potential market valuation for the Bioprocess Containers Market by 2032? +

In 2032, the market size of Bioprocess Containers Market is expected to reach USD 22,261.87 million.

What are the segments covered in the Bioprocess Containers Market report? +

The type, application, and end-user are the segments covered in this report.

Who are the major players in the Bioprocess Containers Market? +

Sartorius AG (Germany), Thermo Fisher Scientific Inc. (United States), Corning Incorporated (United States), Lonza Group (Switzerland), Eppendorf AG (Germany), Danaher Corporation (United States), Starlim Spritzguss GmbH (Austria), Merck Group (Germany), Becton, Dickinson and Company (United States), Pall Corporation (United States) are the major players in the Bioprocess Containers market.