- Summary

- Table Of Content

- Methodology

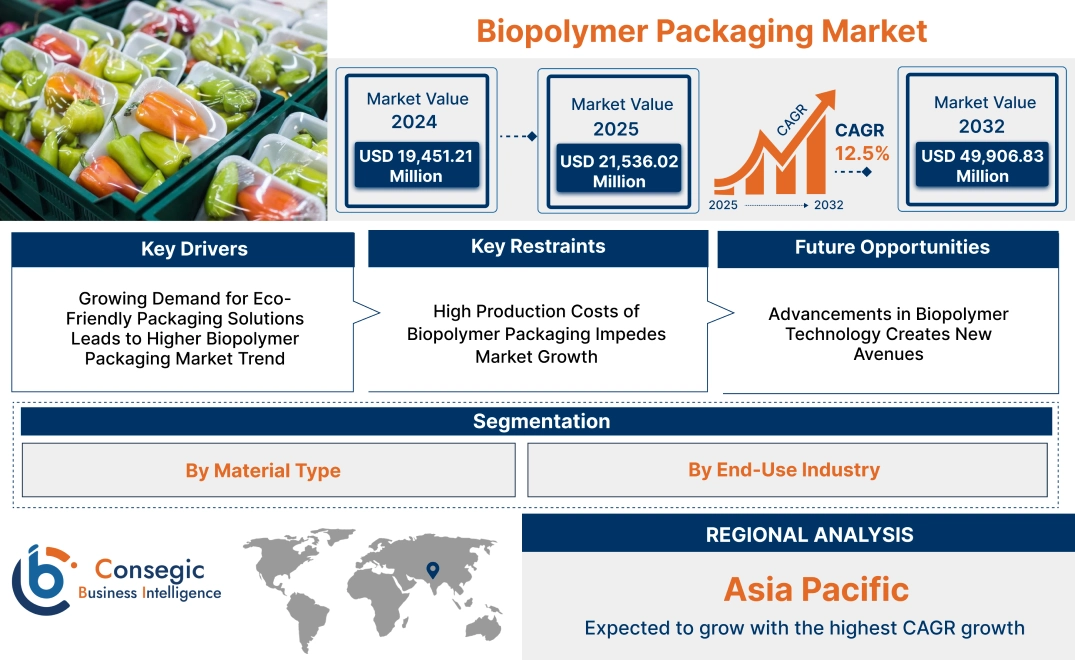

Biopolymer Packaging Market Size:

Biopolymer Packaging Market size is estimated to reach over USD 49,906.83 Million by 2032 from a value of USD 19,451.21 Million in 2024 and is projected to grow by USD 21,536.02 Million in 2025, growing at a CAGR of 12.5% from 2025 to 2032.

Biopolymer Packaging Market Scope & Overview:

Biopolymer packaging refers to packaging materials made from renewable resources, offering an eco-friendly alternative to traditional petroleum-based plastics. These materials are derived from natural sources such as plants, starch, and cellulose, making them biodegradable and compostable. Biopolymer packaging is characterized by its sustainable nature, reducing the environmental impact associated with conventional plastic packaging. These materials exhibit properties like flexibility, durability, and barrier resistance to moisture, gases, and light, making them suitable for various packaging needs. The benefits of this packaging include reduced carbon footprint, enhanced biodegradability, and the use of renewable resources. These advantages support efforts to minimize plastic waste and promote environmental sustainability.

Applications of biopolymer packaging are seen in food and beverage, pharmaceuticals, cosmetics, and consumer goods industries. In these sectors, it is used for packaging products ranging from fresh produce to beauty products. Biopolymer packaging plays a key role in advancing sustainable packaging solutions. Its ability to replace conventional plastic with biodegradable materials supports eco-conscious practices in diverse industries, aligning with growing trend for environmentally friendly products.

Biopolymer Packaging Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for Eco-Friendly Packaging Solutions Leads to Higher Biopolymer Packaging Market Trend

The rising consumer preference for sustainable and eco-friendly products significantly drives the Biopolymer Packaging Market demand. Traditional plastic packaging has long been a concern due to its environmental impact, prompting manufacturers to shift towards biodegradable and renewable alternatives. Biopolymer packaging, derived from natural sources like starch, cellulose, and polylactic acid (PLA), offers a biodegradable solution that reduces plastic waste and carbon footprints. In the food industry, for instance, biopolymer packaging is increasingly used for packaging fresh produce, ready-to-eat meals, and beverages, as consumers demand packaging materials that are both functional and environmentally friendly. This shift towards sustainable packaging practices is spurred by regulatory policies and consumer awareness about plastic pollution.

Consequently, as businesses respond to the growing trend for green alternatives, the biopolymer packaging market continues to expand.

Key Restraints:

High Production Costs of Biopolymer Packaging Impedes Market Growth

Despite the rising trend for eco-friendly packaging, the high production costs of biopolymer materials remain a significant constraint. Biopolymers often require more complex and costly production processes compared to conventional plastics, leading to higher prices for end consumers. For example, the production of PLA requires the fermentation of sugars, which adds to the overall cost, making it less competitive compared to petroleum-based plastics. While prices have decreased with technological advancements, the cost disparity continues to hinder widespread adoption, particularly among small and medium-sized businesses in cost-sensitive industries. This financial burden limits the use of biopolymer packaging in some regions and sectors, slowing down its market penetration. Therefore, high production costs remain a key barrier to the accelerated adoption of biopolymer packaging.

Future Opportunities :

Advancements in Biopolymer Technology Creates New Avenues

Ongoing research and technological advancements in biopolymer materials present a significant biopolymer packaging market opportunity. New developments are focused on improving the performance, cost-effectiveness, and scalability of biopolymers. For instance, emerging biopolymers that combine multiple biodegradable materials, or the development of bio-based polymers with enhanced barrier properties, offer potential to expand their use across various applications, including the packaging of high-moisture content products. These innovations make biopolymers more competitive with traditional plastics, addressing concerns related to packaging durability and shelf life. As these technologies advance, they will likely lead to a reduction in production costs, further accelerating the market adoption of biopolymer packaging. Therefore, ongoing advancements in biopolymer technology present a substantial opportunity to meet both sustainability goals and consumer expectations.

Biopolymer Packaging Market Segmental Analysis :

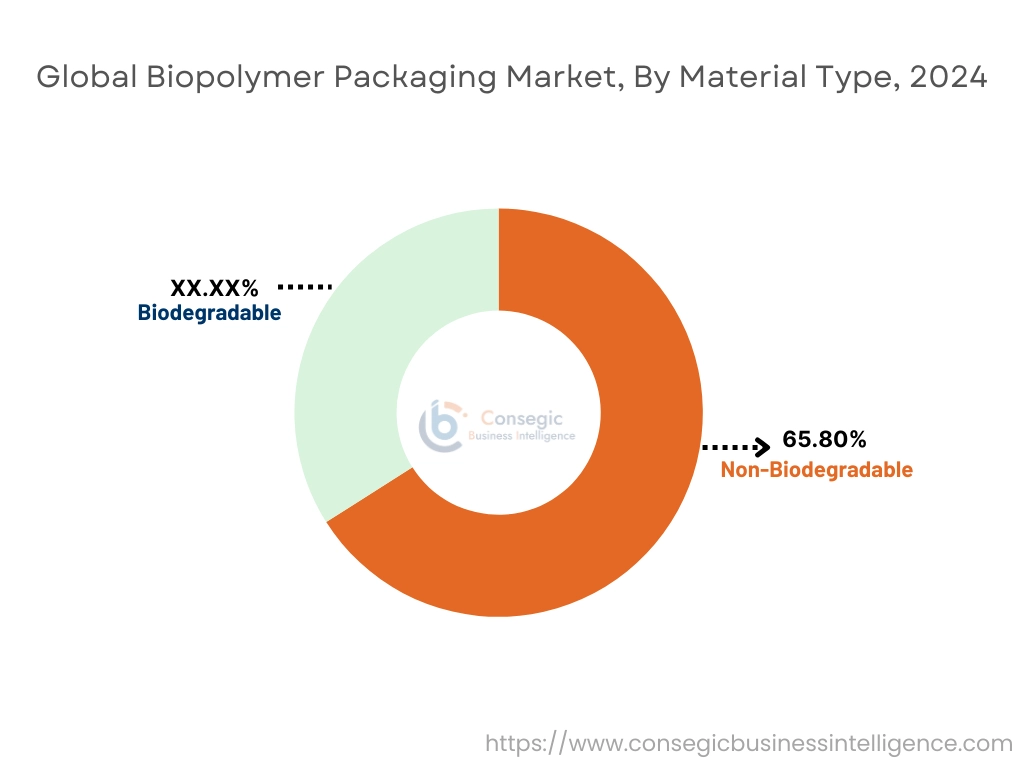

By Material Type:

Based on material type, the biopolymer packaging market is segmented into non-biodegradable (polyethylene terephthalate (PET), polyamide (PA), polytrimethylene terephthalate (PTT), and others) and biodegradable categories (polylactic acid (PLA), polybutylene adipate co-terephthalate (PBAT), starch blends, and others).

The non-biodegradable materials segment accounted for the largest revenue in Global Biopolymer Packaging Market share by 65.80% in 2024.

- Non-biodegradable biopolymers such as PET and PTT are known for their excellent strength, rigidity, and high barrier properties, which make them ideal for packaging applications requiring durability and long shelf life.

- These materials are highly resistant to moisture, oxygen, and chemicals, ensuring that packaged products are well-protected from environmental factors.

- The ability to recycle these materials, alongside their compatibility with existing recycling infrastructure, supports their sustained trend in the market.

- With industries focused on increasing the use of recyclable packaging, non-biodegradable materials like PET and PA are key contributors to sustainability goals, aligning with global packaging trends.

- Their widespread use in food and beverage, personal care, and healthcare packaging, where both protection and presentation are important, continues to drive biopolymer packaging market growth.

- Therefore, according to biopolymer packaging market analysis, the dominance of non-biodegradable biopolymers is attributed to their performance in packaging applications where strength, durability, and recyclability are critical.

The biodegradable materials segment is anticipated to register the fastest CAGR during the forecast period.

- PLA and PBAT are biodegradable plastics with properties that align with the increasing global push towards sustainability and environmental protection.

- These materials are able to decompose naturally in composting environments, reducing their environmental footprint and offering an eco-friendly alternative to traditional plastics.

- The trend for biodegradable packaging has been driven by stringent regulations and consumer awareness about the harmful effects of plastic pollution, especially in the food and beverage sector.

- Biodegradable biopolymers also offer advantages like flexibility, strength, and thermal stability, making them suitable for various food and cosmetic packaging solutions.

- As consumer demand for greener packaging continues to grow, biodegradable materials are expected to gain further traction, especially in eco-conscious markets.

- Thus, according to biopolymer packaging market analysis, the rapid growth of biodegradable materials is fueled by the increasing regulatory focus on sustainability and consumer demand for environmentally friendly packaging.

By End User Industry:

Based on the end-use industry, the market is categorized into food & beverage, healthcare, personal care & cosmetics, industrial goods, and others.

The food & beverage segment accounted for the largest revenue Biopolymer Packaging Market share in 2024.

- Biopolymer packaging is crucial in the food & beverage industry due to its ability to preserve food freshness and prevent contamination while being eco-friendly.

- Materials like PLA, which is derived from renewable resources like corn starch, are popular for their compostable and non-toxic nature, offering an environmentally conscious alternative to petroleum-based plastics.

- There is an increasing trend in sustainable food packaging solutions that cater to the growing demand for organic, natural, and health-conscious products.

- With the rise in consumer awareness about the environmental impact of packaging waste, food manufacturers are prioritizing biopolymer options to meet eco-conscious consumer preferences.

- Additionally, innovative applications such as edible films and coatings for food packaging are gaining popularity, driving the Biopolymer Packaging Market demand in the food industry.

- Therefore, according to market analysis, the food & beverage industry remains the largest market for biopolymer packaging due to its essential role in meeting both packaging performance and sustainability demands.

The healthcare segment is anticipated to register the fastest CAGR during the forecast period.

- Biopolymer packaging is increasingly used in the healthcare industry due to its non-toxic, biodegradable, and sterilizable properties, making it ideal for medical and pharmaceutical applications.

- Biopolymers like PLA and PBAT are used for packaging medical devices, pharmaceuticals, wound care products, and medical packaging due to their biocompatibility and environmental benefits.

- The need for sustainable and eco-friendly packaging solutions in healthcare is being driven by regulatory mandates and increasing public awareness about the environmental effects of conventional plastic waste.

- Innovations in biopolymer technology are enhancing their performance, making them suitable for high-performance applications such as controlled drug delivery systems and sterile packaging.

- As the healthcare industry continues to seek greener alternatives, biopolymer packaging is poised for significant growth, especially in packaging for medical equipment and pharmaceutical products.

- Therefore, according to market analysis, the healthcare industry's rapid adoption of biopolymer packaging is driven by growing regulatory demands and increasing consumer and industry preference for sustainable healthcare solutions.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

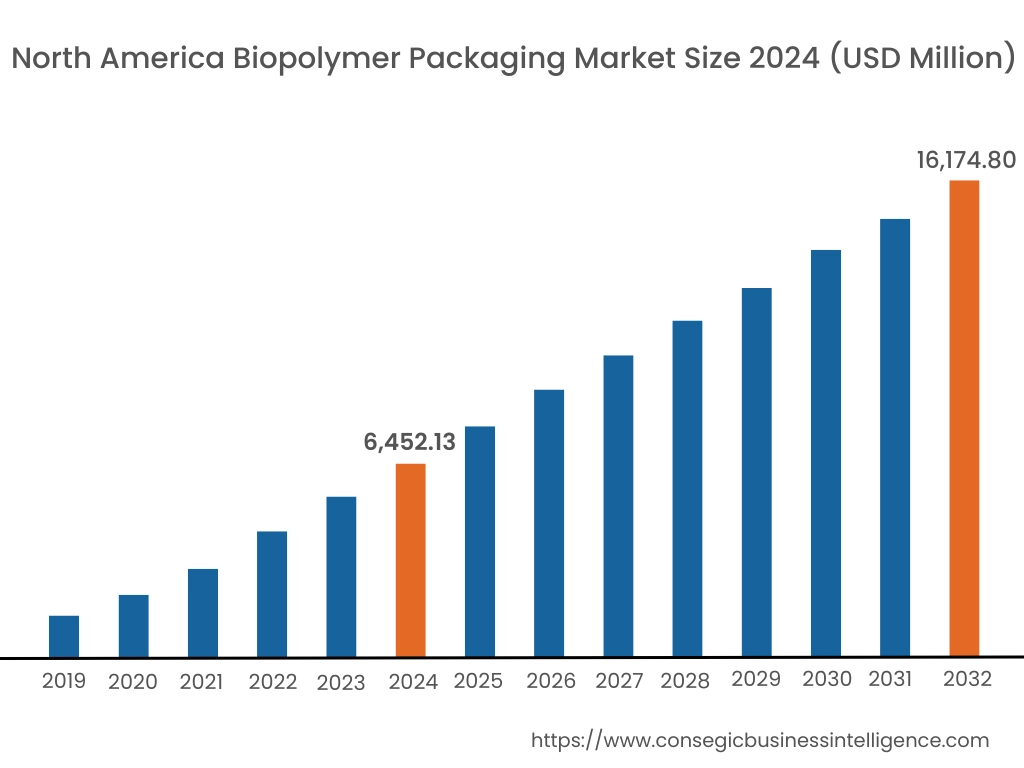

In 2024, North America was valued at USD 6,452.13 Million and is expected to reach USD 16,174.80 Million in 2032. In North America, the U.S. accounted for the highest share of 73.60% during the base year of 2024. North America holds a significant share of the biopolymer packaging market. The region has a well-established demand for sustainable packaging solutions due to increasing environmental awareness. Regulatory support from governments, particularly in the United States and Canada, promotes the adoption of biodegradable materials. Major industries, including food and beverages, pharmaceuticals, and consumer goods, prioritize eco-friendly packaging solutions, further strengthening biopolymer packaging market growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 13.0% over the forecast period. Asia-Pacific exhibits substantial demand for biopolymer packaging driven by rapid industrialization and rising consumer awareness about sustainability, leading it to have substantial market shares. Countries like China, India, and Japan are adopting biopolymer-based packaging materials, especially in the food and beverage sector. The region’s large population and increasing disposable income contribute to a higher demand for packaged goods, influencing the biopolymer packaging market expansion. Additionally, government policies focused on reducing plastic waste support the use of biopolymers.

Europe is a leading region in the biopolymer packaging market. Strict environmental regulations, such as the European Union’s ban on single-use plastics, have led to a surge in demand for biopolymer packaging alternatives. Countries like Germany, France, and the UK are key contributors to market growth, with a strong focus on reducing plastic waste and carbon footprints. European consumers’ preference for eco-friendly products accelerates the shift toward biopolymer-based solutions in packaging.

The Middle East and Africa (MEA) region has a relatively smaller but growing market for biopolymer packaging. Rising awareness about sustainability and environmental challenges has led to increased demand for biodegradable packaging solutions. In the Middle East, countries such as the UAE and Saudi Arabia are increasingly adopting biopolymers in packaging, driven by government initiatives aimed at reducing plastic pollution. However, the market in Africa remains nascent, with challenges related to infrastructure and affordability.

Latin America’s biopolymer packaging market expansion is quite steady, primarily driven by the rising demand for sustainable packaging options in the food and beverage sector. Countries like Brazil and Mexico are at the forefront, with initiatives to promote the use of biopolymers in packaging to reduce environmental impact. The region’s commitment to sustainability and environmental protection contributes to the increasing adoption of biopolymer-based materials. However, challenges such as high production costs and limited raw material availability hinder market growth to some extent.

Top Key Players & Market Share Insights:

The Global Biopolymer Packaging Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Biopolymer Packaging Market. Key players in the Biopolymer Packaging industry include-

- BASF SE (Germany)

- DuPont de Nemours, Inc. (United States)

- Uflex Limited (India)

- Corbion (Netherlands)

- Total Corbion PLA (Netherlands)

- NatureWorks LLC (United States)

- Mitsubishi Chemical Corporation (Japan)

- Novamont S.p.A. (Italy)

- Sappi Lanxess (South Africa)

- Stora Enso Oyj (Finland)

Biopolymer Packaging Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 49,906.83 Million |

| CAGR (2025-2032) | 12.5% |

| By Material Type |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Biopolymer Packaging Market? +

In 2024, the Biopolymer Packaging Market was USD 19,451.21 million.

What will be the potential market valuation for the Biopolymer Packaging Market by 2032? +

In 2032, the market size of Biopolymer Packaging Market is expected to reach USD 49,906.83 million.

What are the segments covered in the Biopolymer Packaging Market report? +

The material type and end-user industry are the segments covered in this report.

Who are the major players in the Biopolymer Packaging Market? +

BASF SE (Germany), DuPont de Nemours, Inc. (United States), NatureWorks LLC (United States), Mitsubishi Chemical Corporation (Japan), Novamont S.p.A. (Italy), Sappi Lanxess (South Africa), Stora Enso Oyj (Finland), Uflex Limited (India), Corbion (Netherlands), Total Corbion PLA (Netherlands) are the major players in the Biopolymer Packaging market.