- Summary

- Table Of Content

- Methodology

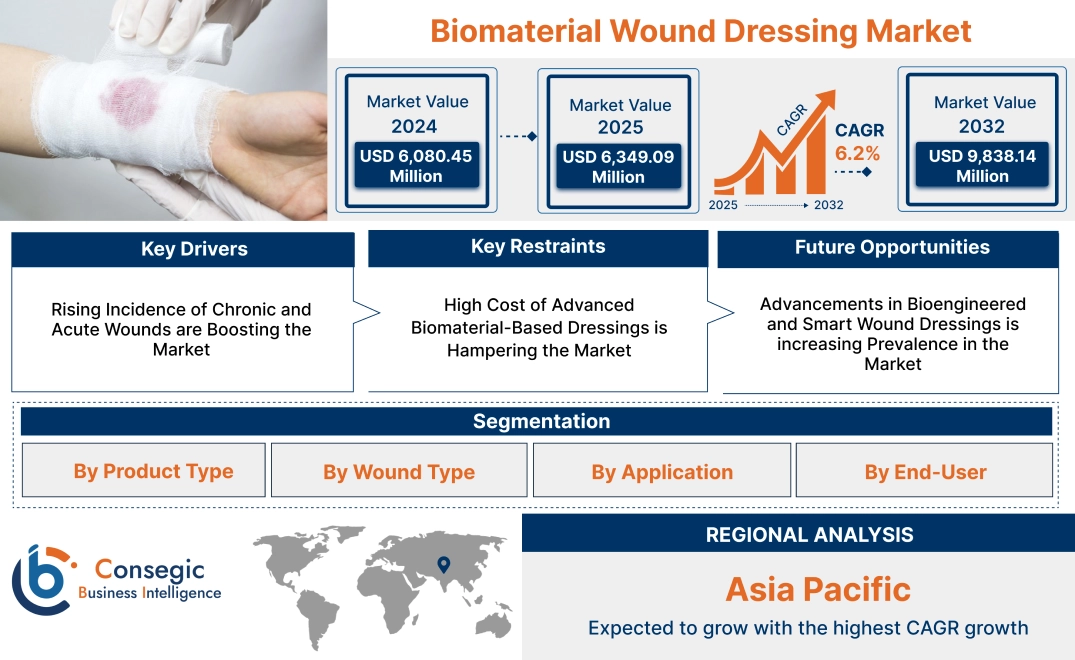

Biomaterial Wound Dressing Market Size:

Biomaterial Wound Dressing Market size is estimated to reach over USD 9,838.14 Million by 2032 from a value of USD 6,080.45 Million in 2024 and is projected to grow by USD 6,349.09 Million in 2025, growing at a CAGR of 6.2% from 2025 to 2032.

Biomaterial Wound Dressing Market Scope & Overview:

The biomaterial wound dressing focuses on advanced wound care products made from natural and synthetic biomaterials designed to accelerate the healing process, prevent infections, and improve patient outcomes. These dressings provide a moist healing environment, facilitate cell regeneration, and reduce scarring. Key products in this market include hydrocolloids, hydrogels, alginates, collagen dressings, and bioengineered skin substitutes.

Key characteristics of biomaterial wound dressings include high biocompatibility, antimicrobial properties, and the ability to promote tissue regeneration. The benefits include faster wound healing, reduced risk of infection, and improved management of acute and chronic wounds.

Applications span the treatment of diabetic foot ulcers, pressure ulcers, surgical wounds, burns, and traumatic injuries. End-users include hospitals, wound care centers, home healthcare settings, and ambulatory surgical centers, driven by the rising incidence of chronic wounds, increasing surgical procedures, advancements in biomaterial technologies, and growing awareness of advanced wound care solutions.

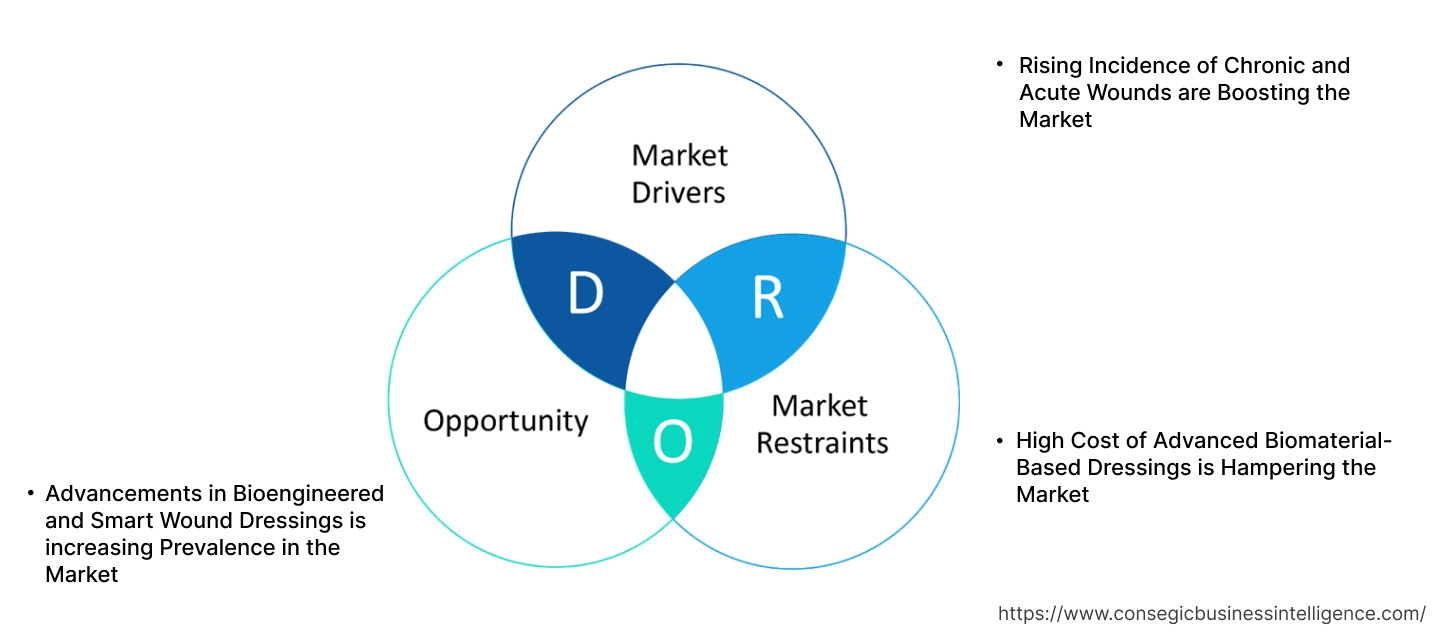

Biomaterial Wound Dressing Market Dynamics - (DRO) :

Key Drivers:

Rising Incidence of Chronic and Acute Wounds are Boosting the Market

The increasing prevalence of chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, alongside acute wounds resulting from surgeries, trauma, and burns, is a major driver for the market. Chronic wounds require prolonged and specialized care to prevent infections and promote healing. Biomaterial-based dressings, including collagen, alginate, chitosan, and hydrogel dressings, provide superior wound healing properties due to their biocompatibility, moisture retention, and ability to promote cell regeneration. The rising global incidence of diabetes and obesity, both of which are key contributors to chronic wounds, has further fueled the demand for advanced wound care products. Additionally, the growing geriatric population, which is more susceptible to wounds and delayed healing, continues to drive biomaterial wound dressing market expansion.

Key Restraints:

High Cost of Advanced Biomaterial-Based Dressings is Hampering the Market

The high cost associated with biomaterial wound dressings poses a significant challenge to widespread market adoption, particularly in price-sensitive markets. Compared to traditional wound care products, advanced biomaterial dressings are more expensive due to complex manufacturing processes and the use of high-quality bioactive materials. This cost barrier limits their use in underfunded healthcare systems and low- to middle-income countries, where affordability often dictates product selection. Additionally, inconsistent reimbursement policies for advanced wound care products in various regions further restrict market growth, as patients and healthcare providers are hesitant to adopt premium-priced solutions without adequate financial support.

Future Opportunities:

Advancements in Bioengineered and Smart Wound Dressings is increasing Prevalence in the Market

The development of bioengineered and smart wound dressings presents significant trends for biomaterial wound dressing market opportunities. Innovations in bioactive dressings that incorporate growth factors, antimicrobial agents, and stem cells are transforming wound management by accelerating tissue regeneration and reducing infection risks. Additionally, the emergence of smart dressings equipped with sensors to monitor wound conditions such as pH levels, temperature, and moisture content allows for real-time wound assessment and timely intervention. These advanced solutions not only enhance patient outcomes but also minimize healthcare costs by reducing hospital stays and the frequency of dressing changes. Companies investing in the research and development of bioengineered and sensor-integrated dressings are well-positioned to capitalize on the growing demand for personalized and effective wound care solutions.

These market dynamics highlight the critical role of biomaterial wound dressings in managing complex wound care needs, driven by the rising burden of chronic and acute wounds. While high costs pose challenges, ongoing innovations in bioengineered and smart wound care products offer promising pathways for biomaterial wound dressing market trends, providing enhanced healing outcomes and advancing patient care standards.

Biomaterial Wound Dressing Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into natural biomaterial dressings and synthetic biomaterial dressings.

The natural biomaterial dressings segment accounted for the largest revenue in biomaterial wound dressing market share in 2024.

- Natural biomaterial dressings, such as collagen, alginate, gelatin-based, and chitosan dressings, are widely used for their superior biocompatibility and healing properties.

- Collagen dressings promote faster tissue regeneration, making them ideal for chronic and surgical wounds.

- Alginate dressings, derived from seaweed, offer excellent moisture absorption and are effective in managing exudative wounds.

- Increasing preference for natural, biodegradable wound care products drives the growth of this segment.

The synthetic biomaterial dressings segment is anticipated to register the fastest CAGR during the forecast period.

- Synthetic dressings, including hydrocolloid, hydrogel, foam, and film dressings, offer enhanced moisture retention and protection.

- Hydrogel and hydrocolloid dressings are increasingly used for pressure ulcers and diabetic foot ulcers due to their superior wound hydration capabilities.

- Foam dressings are preferred for highly exudative wounds due to their high absorption capacity.

- Technological advancements in synthetic materials for better antimicrobial properties and comfort are driving trends in this segment.

By Wound Type:

Based on wound type, the market is segmented into acute wounds, chronic wounds, and burn wounds.

The chronic wounds segment accounted for the largest revenue in biomaterial wound dressing market share in 2024.

- Chronic wounds, such as diabetic foot ulcers, pressure ulcers, venous leg ulcers, and arterial ulcers, require long-term wound care management.

- The increasing global prevalence of diabetes and obesity significantly drives biomaterial wound dressing market demand for advanced wound dressings.

- Rising geriatric populations, who are more prone to chronic wounds, further support segmental analysis.

- Growing awareness and advancements in biomaterial-based solutions for chronic wound care enhance market expansion.

The burn wounds segment is anticipated to register the fastest CAGR during the forecast period.

- Burn injuries require specialized dressings for pain management, infection control, and faster healing.

- Increasing incidence of burn injuries globally is driving demand for advanced biomaterial dressings.

- Advancements in hydrogel and foam dressings for burn wound care are propelling segmental analysis.

- Expanding healthcare infrastructure for burn treatment in emerging economies is boosting this segment.

By Application:

Based on application, the market is segmented into wounds, burns, ulcers, and others.

The wounds segment accounted for the largest revenue share in 2024.

- This segment covers a wide range of acute and chronic wounds, including surgical and traumatic wounds.

- Rising surgical procedures globally and increasing traumatic injuries have fueled demand for effective wound dressings.

- The growing adoption of biomaterial dressings for faster recovery and infection prevention supports market dominance.

- Increasing awareness of proper wound care management across healthcare facilities contributes to this segment's trends.

The ulcers segment is anticipated to register the fastest CAGR during the forecast period.

- Ulcers, particularly diabetic foot ulcers and pressure ulcers, are becoming increasingly prevalent due to rising diabetes and obesity rates.

- Advanced biomaterial dressings offer better moisture control, infection prevention, and faster healing for ulcer management.

- The growing elderly population, which is more susceptible to pressure ulcers, is driving biomaterial wound dressing market growth.

- Enhanced healthcare awareness and government initiatives for chronic wound care are expected to fuel biomaterial wound dressing market growth in this segment.

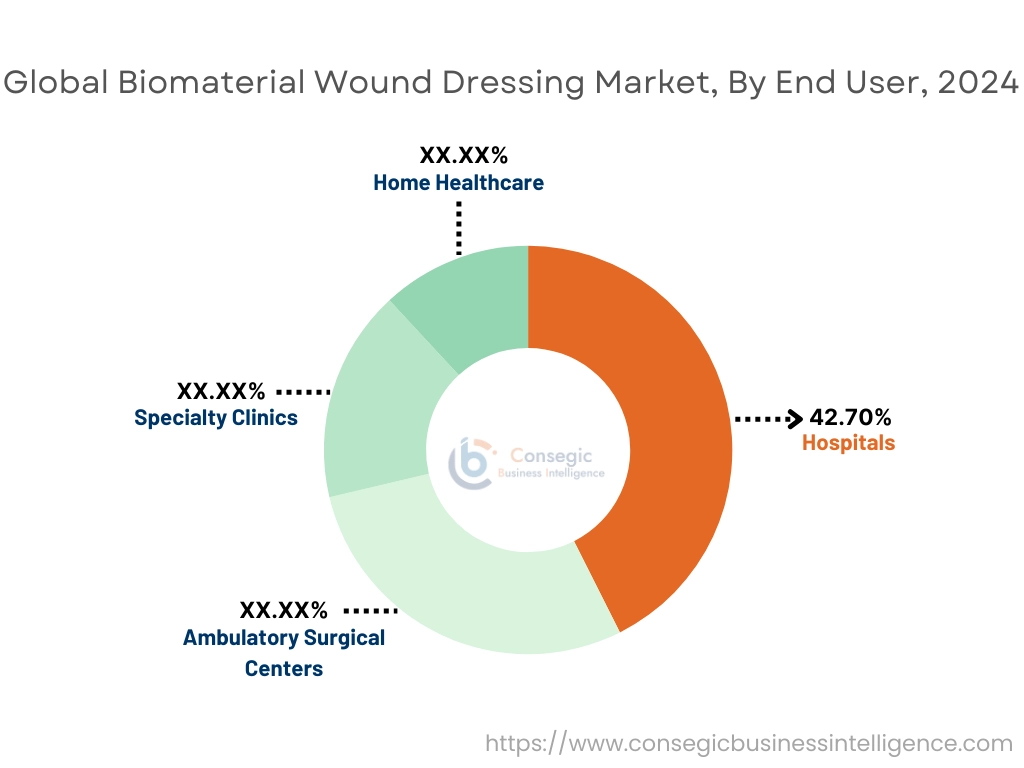

By End-User:

Based on end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and home healthcare.

The hospitals segment accounted for the largest revenue share of 42.70% in 2024.

- Hospitals are the primary providers of advanced wound care solutions due to their comprehensive treatment capabilities.

- Increasing surgical procedures and hospital admissions for chronic and burn wounds support the dominance of this segment.

- The availability of specialized wound care units and trained professionals in hospitals drives biomaterial wound dressing market demand for biomaterial dressings.

- Growing investments in hospital infrastructure and infection control practices further enhance market growth.

The home healthcare segment is anticipated to register the fastest CAGR during the forecast period.

- Rising trends for at-home wound care solutions, particularly for elderly and chronically ill patients, drives biomaterial wound dressing market trends in this segment.

- Increasing availability of user-friendly and self-applicable biomaterial dressings supports adoption in home settings.

- Advancements in telehealth services and remote monitoring enable better wound care management at home.

- Cost-effective homecare solutions and growing awareness about wound care among patients are expected to propel trends in this segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

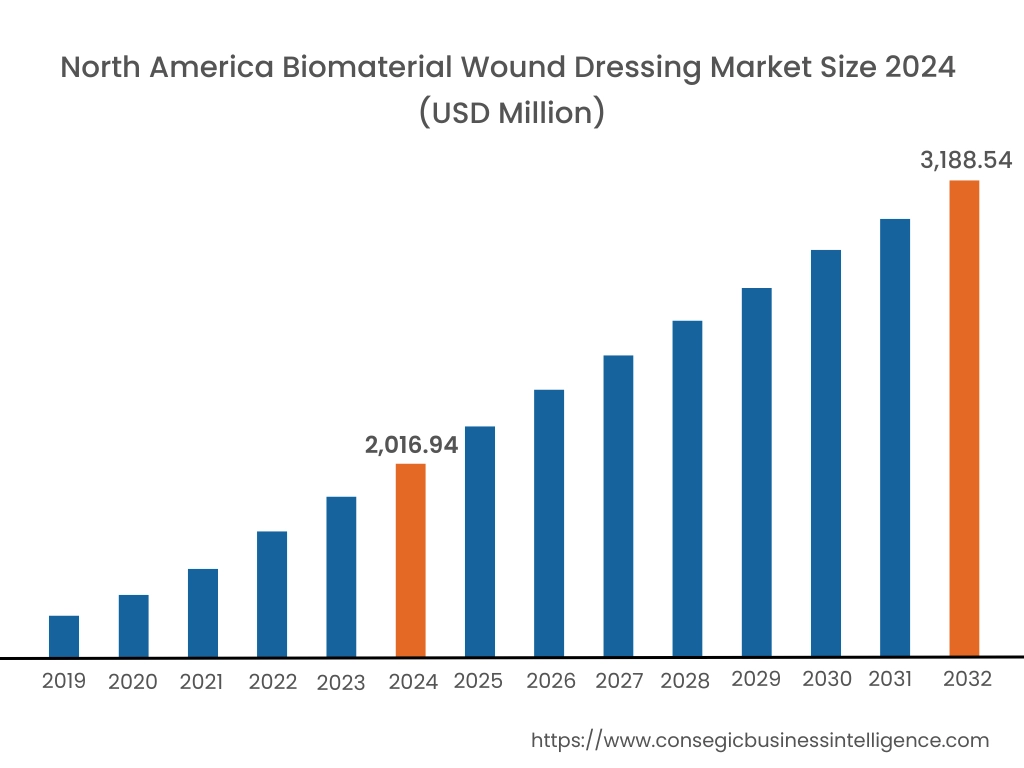

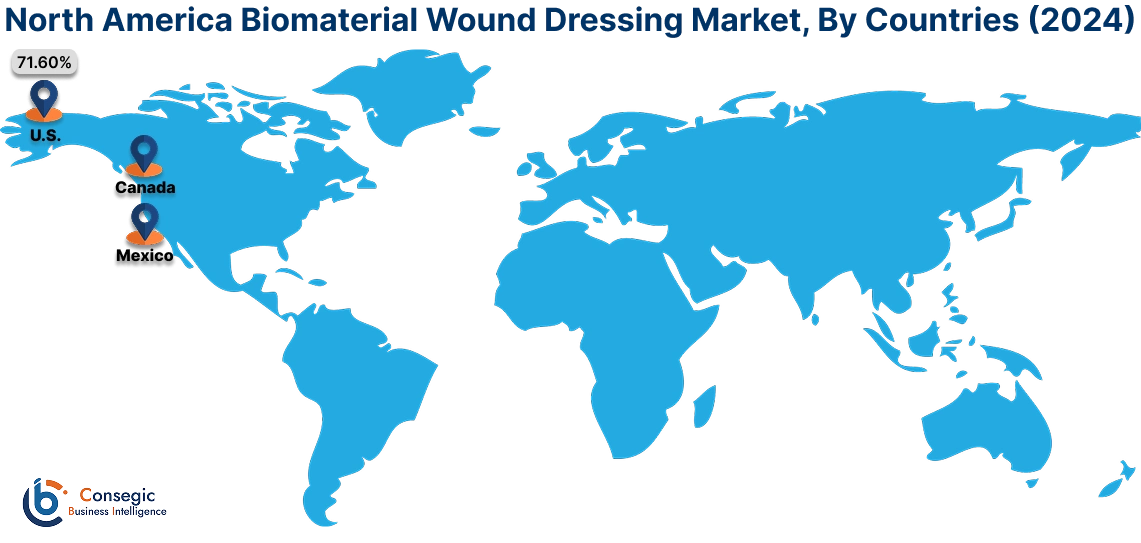

In 2024, North America was valued at USD 2,016.94 Million and is expected to reach USD 3,188.54 Million in 2032. In North America, the U.S. accounted for the highest share of 71.60% during the base year of 2024. North America holds a significant share in the global biomaterial wound dressing market, driven by the rising prevalence of chronic wounds, diabetic ulcers, and pressure ulcers. The U.S. leads the region due to advanced healthcare infrastructure, high healthcare expenditure, and the presence of leading wound care product manufacturers. The increasing geriatric population and rising incidence of diabetes contribute to the demand for advanced wound dressings market. As per the analysis Canada supports market growth through growing awareness of advanced wound care solutions and government initiatives to improve chronic wound management. However, the high cost of advanced wound dressings may limit adoption in certain healthcare settings.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 6.6% over the forecast period. The biomaterial wound dressing market analysis, is fueled by rising healthcare awareness, increasing incidence of diabetes, and improving healthcare infrastructure in China, India, and Japan. China dominates the region with growing demand for advanced wound care solutions in hospitals and homecare, supported by government investments in healthcare. India’s rapidly expanding healthcare sector drives the adoption of cost-effective biomaterial wound dressings for chronic wound management, especially in diabetic patients. Japan focuses on high-precision wound care technologies, leveraging its strong R&D capabilities in medical materials. However, limited access to advanced wound care products in rural areas may hinder biomaterial wound dressing market expansion.

Europe is a prominent market, it is supported by a growing elderly population, increasing cases of chronic wounds, and favorable reimbursement policies for advanced wound care. Countries like Germany, the UK, and France are key contributors. Germany leads the market with its strong focus on advanced healthcare technologies and chronic wound management programs. The regional analysis portrays, UK emphasizes the use of innovative wound dressings in its public healthcare system (NHS), while France focuses on expanding access to advanced wound care in both hospital and homecare settings. However, stringent regulatory approval processes may slow the entry of new biomaterial wound care products.

The Middle East & Africa region is witnessing steady growth in the global biomaterial wound dressing market, driven by rising healthcare investments and a growing burden of chronic conditions. Countries like Saudi Arabia and the UAE are adopting advanced wound care products to improve the management of diabetic ulcers and surgical wounds, supported by healthcare modernization initiatives. In Africa, South Africa is emerging as a key market, focusing on improving access to wound care products and managing chronic wounds associated with diabetes and infections. However, limited healthcare infrastructure and affordability challenges may restrict broader market development in the region.

Latin America is an emerging market for biomaterial wound dressings, with Brazil and Mexico leading the region. Brazil’s expanding healthcare sector and rising incidence of diabetes and obesity drive the trends for advanced wound care products. Mexico focuses on increasing access to affordable wound care solutions through public healthcare initiatives and partnerships with global medical device manufacturers. The region also benefits from growing awareness of infection control and advanced wound care technologies. However, economic instability and inconsistent healthcare infrastructure may pose challenges to biomaterial wound dressing market opportunities in smaller economies.

Top Key Players & Market Share Insights:

The biomaterial wound dressing market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global biomaterial wound dressing market. Key players in the biomaterial wound dressing industry include -

- Smith & Nephew plc (United Kingdom)

- Mölnlycke Health Care AB (Sweden)

- Derma Sciences Inc. (United States)

- Organogenesis Holdings Inc. (United States)

- Baxter International Inc. (United States)

- 3M Company (United States)

- ConvaTec Group PLC (United Kingdom)

- Coloplast A/S (Denmark)

- Medtronic plc (Ireland)

- Johnson & Johnson (United States)

Biomaterial Wound Dressing Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 9,838.14 Million |

| CAGR (2025-2032) | 6.2% |

| By Product Type |

|

| By Wound Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Mental Wellness Market by 2032? +

The Mental Wellness Market is expected to experience substantial growth, reaching over USD 298.42 Billion by 2032, driven by increasing mental health awareness, digital innovations, and supportive government policies.

What factors are driving the growth of the Mental Wellness Market? +

The market is primarily driven by growing awareness of mental health issues, rising cases of stress, anxiety, and depression, advancements in digital mental health platforms, and the integration of mental wellness programs in workplaces and educational institutions.

What challenges are limiting the growth of the market? +

High costs of professional mental health services, limited access to quality care in low- and middle-income regions, and a shortage of trained mental health professionals are key barriers to market expansion.

Which segment holds the largest share in the market? +

The therapy and counseling services segment holds the largest market share due to increased demand for professional mental health support and growing destigmatization of mental health treatment.

Which region leads the global Mental Wellness Market? +

North America leads the global market, driven by widespread adoption of digital mental health platforms, strong healthcare infrastructure, and government support for mental health initiatives.