- Summary

- Table Of Content

- Methodology

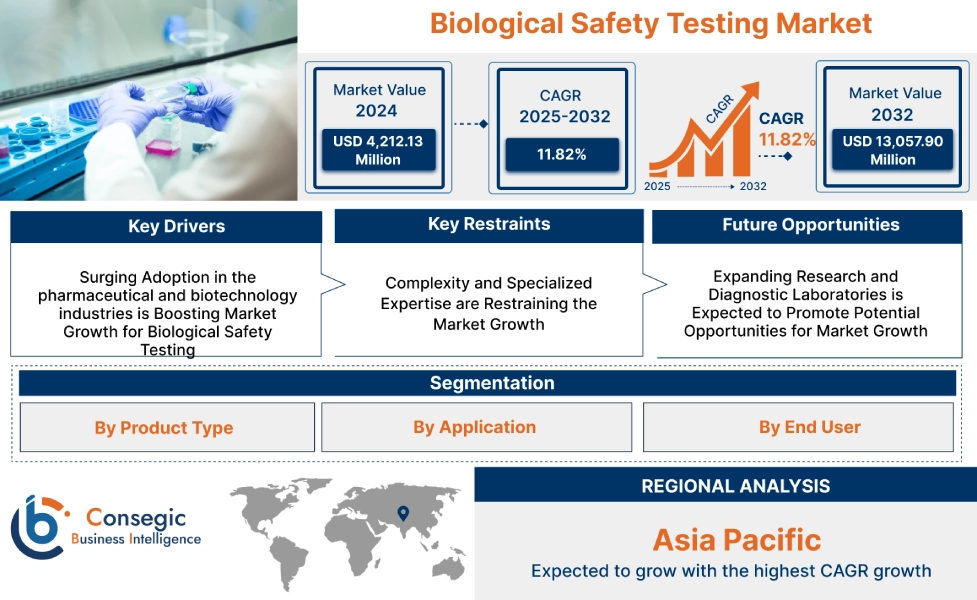

Biological Safety Testing Market Size:

Biological safety testing market size is estimated to reach over USD 8,327.78 Million by 2031 from a value of USD 3,730.46 Million in 2023, growing at a CAGR of 10.8% from 2024 to 2031.

Biological Safety Testing Market Scope & Overview:

The biologics safety testing market focuses on ensuring the safety, quality, and efficacy of biological products such as vaccines, monoclonal antibodies, gene therapies, and recombinant proteins. This market encompasses various testing methods, including sterility testing, endotoxin testing, and mycoplasma testing, which are crucial for detecting contaminants and verifying the safety of biological drugs before regulatory approval and commercialization. Key features of biologics safety testing include high sensitivity, regulatory compliance, and comprehensive screening capabilities. The primary benefits include enhanced product safety, minimized risk of adverse reactions, and adherence to stringent regulatory standards. Applications span pharmaceutical manufacturing, clinical trials, and quality assurance processes. End-users include biopharmaceutical companies, contract research organizations (CROs), and regulatory agencies, driven by the growing adoption of biologic therapies, increasing investments in biopharmaceutical R&D, and stringent regulatory guidelines for biologics manufacturing.

Biological Safety Testing Market Dynamics - (DRO) :

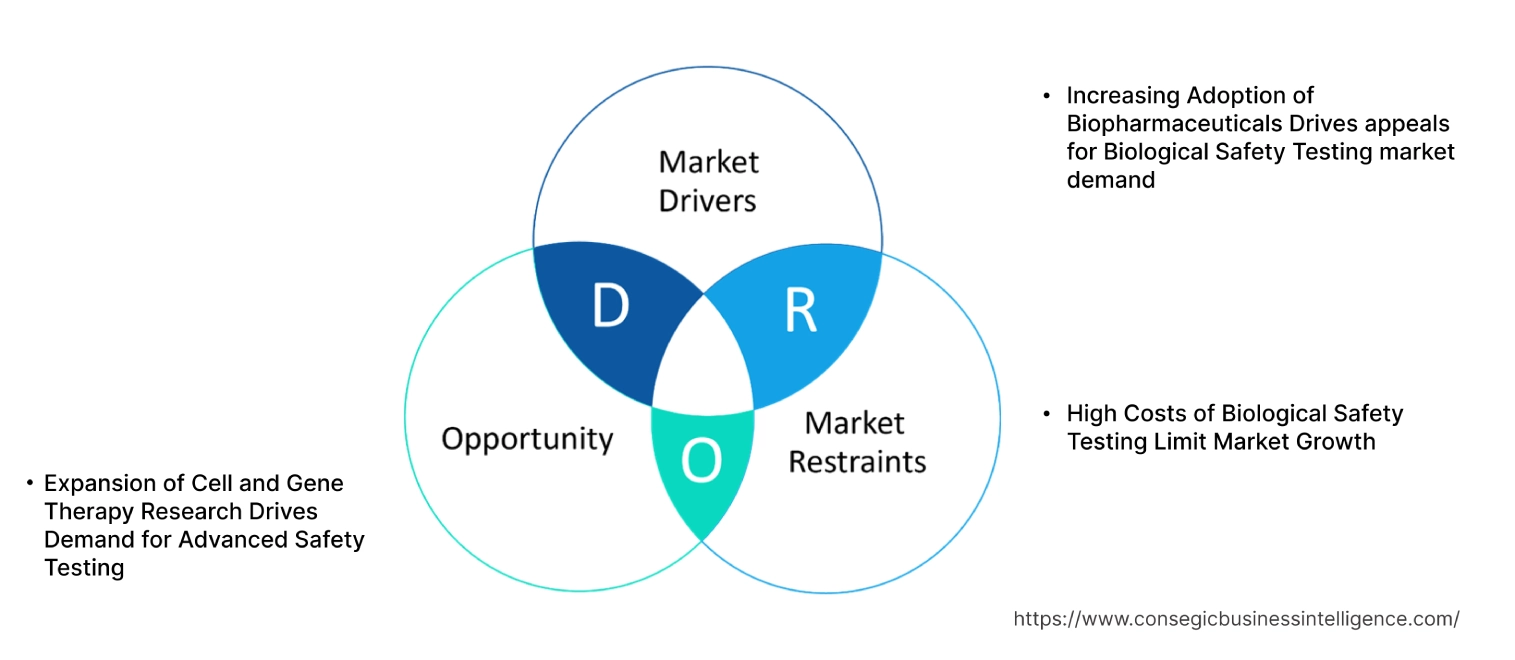

Key Drivers:

Increasing Adoption of Biopharmaceuticals Drives appeals for Biological Safety Testing market demand

The rising adoption of biopharmaceuticals, including monoclonal antibodies, vaccines, and gene therapies, is a significant driver for the biological safety testing market. As these biologics become a larger part of the pharmaceutical landscape, rigorous testing is required to ensure safety, efficacy, and regulatory compliance. Biological safety testing, including sterility testing, endotoxin detection, and mycoplasma testing, is essential for detecting contaminants that could compromise the quality of biopharmaceutical products. The growing pipeline of biologic drugs and the increasing number of clinical trials are further driving the need for comprehensive safety testing services, fueling biological safety testing market growth.

Key Restraints :

High Costs of Biological Safety Testing Limit Market Growth

The high costs associated with biological safety testing services act as a significant restraint for the market. Comprehensive safety testing involves a series of complex, labor-intensive procedures, such as sterility assays, cell line authentication, and viral clearance testing, which require specialized equipment and skilled personnel. The high cost of these tests, coupled with the need for advanced laboratory infrastructure, can be prohibitive, particularly for small and mid-sized biopharmaceutical companies. This financial barrier limits the adoption of comprehensive safety testing, especially in developing regions, thereby restraining biological safety testing market expansion.

Future Opportunities :

Expansion of Cell and Gene Therapy Research Drives Demand for Advanced Safety Testing

The rapid advancement of cell and gene therapy research creates a promising analysis for the biological safety testing market opportunity. Cell and gene therapies involve complex biological products that require rigorous safety assessments to ensure the absence of contaminants like viruses, bacteria, and mycoplasma. The surge in clinical trials for innovative therapies targeting genetic disorders, cancer, and rare diseases is boosting the need for advanced safety testing methods. High-sensitivity testing techniques, such as next-generation sequencing (NGS) and digital PCR, are becoming integral in ensuring the safety and efficacy of these cutting-edge therapies. As the market for cell and gene therapies grows, the trends for specialized safety testing solutions are expected to increase, creating new opportunities for market participants focused on innovative testing technologies.

Biological Safety Testing Market Segmental Analysis :

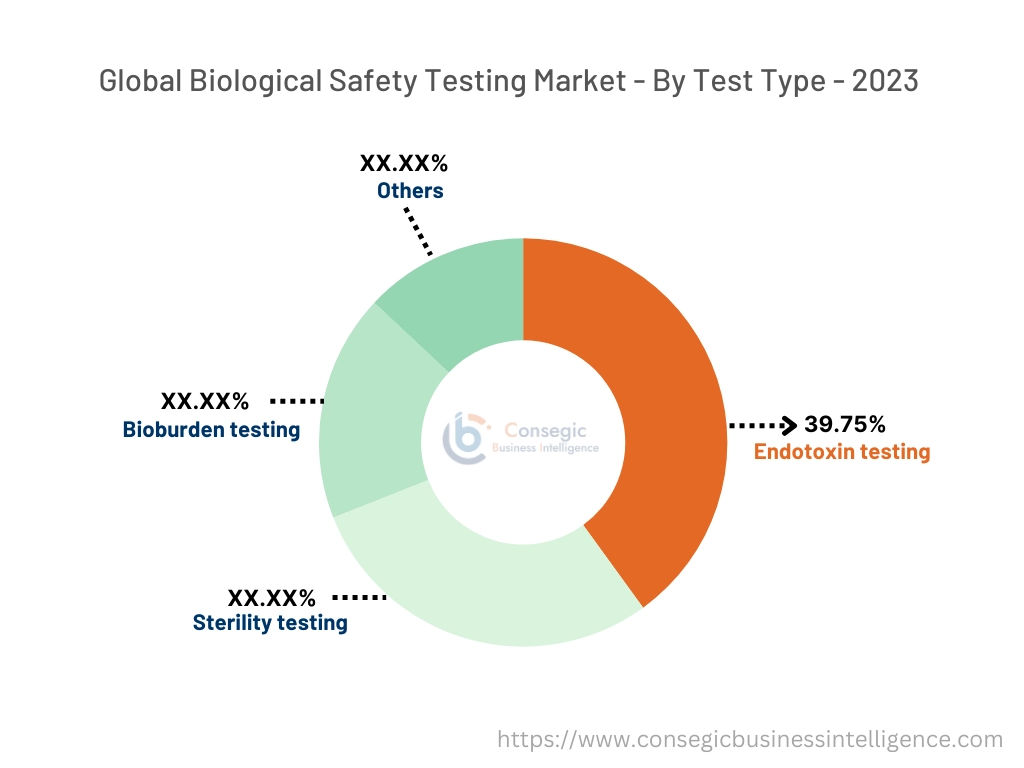

By Test Type:

Based on test type, the market is segmented into endotoxin testing, sterility testing, bioburden testing, and others.

The endotoxin testing segment accounted for the largest revenue of 39.75% in biological safety testing market share in 2023.

- Endotoxin testing is critical for detecting bacterial endotoxins in biological products, ensuring their safety, and reducing the risk of adverse reactions in patients.

- The Limulus amebocyte lysate (LAL) assay remains the most widely used method, although recombinant factor C (RFC) assays are gaining traction due to their non-animal origin and ethical considerations.

- The rising production of biologics, including vaccines and gene therapies, has significantly increased the trends for endotoxin testing.

- Additionally, regulatory requirements mandating strict endotoxin limits in pharmaceuticals are driving the development of this segment.

- Endotoxin testing dominates the biological safety testing market trends due to its essential role in ensuring the safety of biological products, supported by regulatory mandates and the increasing production of biologics.

The sterility testing segment is anticipated to register the fastest CAGR during the forecast period.

- Sterility testing is a mandatory quality control measure for ensuring that biological products, including vaccines and cell-based therapies, are free from microbial contamination.

- The adoption of rapid microbiological methods (RMM) in sterility testing, which significantly reduces testing time, is a key growth driver.

- The rise in gene and cell therapy products, coupled with the stringent requirements for sterility in these advanced therapies, is boosting demand for enhanced sterility testing solutions.

- Innovations in automated sterility testing systems are also contributing to this segment’s rapid biological safety testing market growth.

- Sterility testing is expected to grow rapidly, driven by trends and the increasing need for efficient and reliable testing solutions in the production of advanced therapies and vaccines.

By Application:

Based on application, the market is segmented into vaccine development, blood & blood products testing, gene therapy, cellular therapy, and others.

The vaccine development segment accounted for the largest revenue biological safety testing market share in 2023.

- Biological testing is an integral part of vaccine development, ensuring the safety and efficacy of vaccines before they are approved for use.

- The segment experienced substantial advancement during the COVID-19 pandemic, which accelerated vaccine development and increased trends for comprehensive safety testing.

- As new vaccines for emerging infectious diseases continue to be developed, the need for rigorous safety testing remains high.

- The appeal of vaccine research and production capabilities globally, alongside regulatory requirements for thorough testing, supports the dominance of this segment.

- Vaccine development analysis leads the market opportunities, driven by the critical role of biological safety testing market analysis in ensuring vaccine safety and efficacy, along with the continuous development of new vaccines.

The gene therapy segment is anticipated to register the fastest CAGR during the forecast period.

- Gene therapy products require extensive biological testing to ensure they are free from contaminants and genetically stable.

- The increasing number of gene therapy clinical trials and regulatory approvals for new gene therapy products are driving demand for specialized testing, including adventitious agent detection and genetic stability assessments.

- The complexity of gene therapy products necessitates advanced testing solutions, which are fueling growth in this segment.

- The expanding use of gene therapies for rare diseases and cancer treatments further accelerates the trends for comprehensive safety testing.

- Therefore, as per the analysis gene therapy is expected to grow rapidly, driven by the rising number of clinical trials and regulatory approvals, necessitating thorough safety testing for product quality and patient safety.

By End-User:

Based on end-user, the market is segmented into pharmaceutical & biotechnology companies, contract research organizations (CROs), academic & research institutes, medical device manufacturers, and others.

The pharmaceutical & biotechnology companies segment accounted for the largest revenue share in 2023.

- Pharmaceutical and biotechnology companies are the primary users of biological safety testing due to their extensive involvement in the development and production of biologics, including vaccines, gene therapies, and cell-based products.

- These companies are subject to stringent regulatory requirements that mandate comprehensive safety testing to ensure product quality and patient safety.

- The growing focus on biologics and biosimilars, along with advancements in testing technologies, supports the dominance of this segment. Additionally, automation in testing processes is improving efficiency and throughput in pharmaceutical labs.

- Pharmaceutical & biotechnology companies lead the biological safety testing market trends, driven by their significant role in biologics development and the stringent regulatory requirements for product safety testing.

The contract research organizations (CROs) segment is anticipated to register the fastest CAGR during the forecast period.

- CROs are increasingly favored for outsourcing biological safety testing as they offer specialized expertise, advanced technologies, and regulatory compliance.

- Outsourcing to CROs allows pharmaceutical and biotechnology companies to focus on core R&D activities while leveraging external capabilities for efficient testing.

- The development of CRO services, including comprehensive biological safety testing, and the growing trend of outsourcing complex processes are driving rapid advancement in this segment.

- The increasing trends for high-quality testing services and the need to expedite product development timelines are further propelling this trend.

- The CRO segment is expected to grow rapidly, driven by the increasing trend of outsourcing biological safety testing to leverage specialized expertise and reduce time-to-market for new products.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

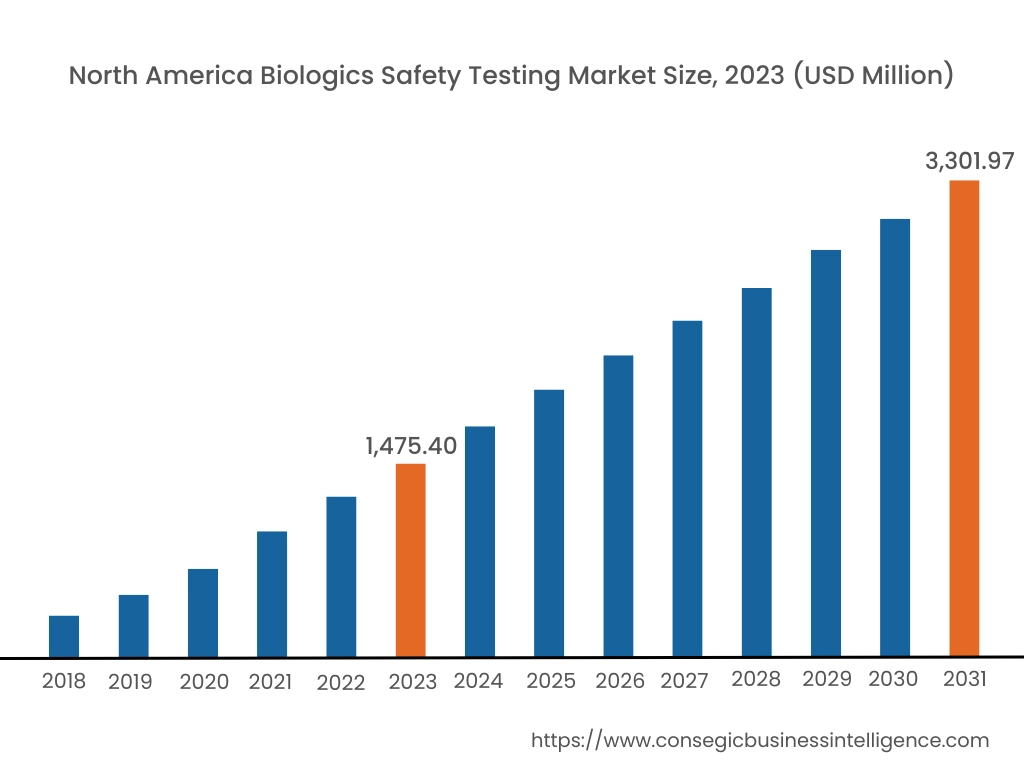

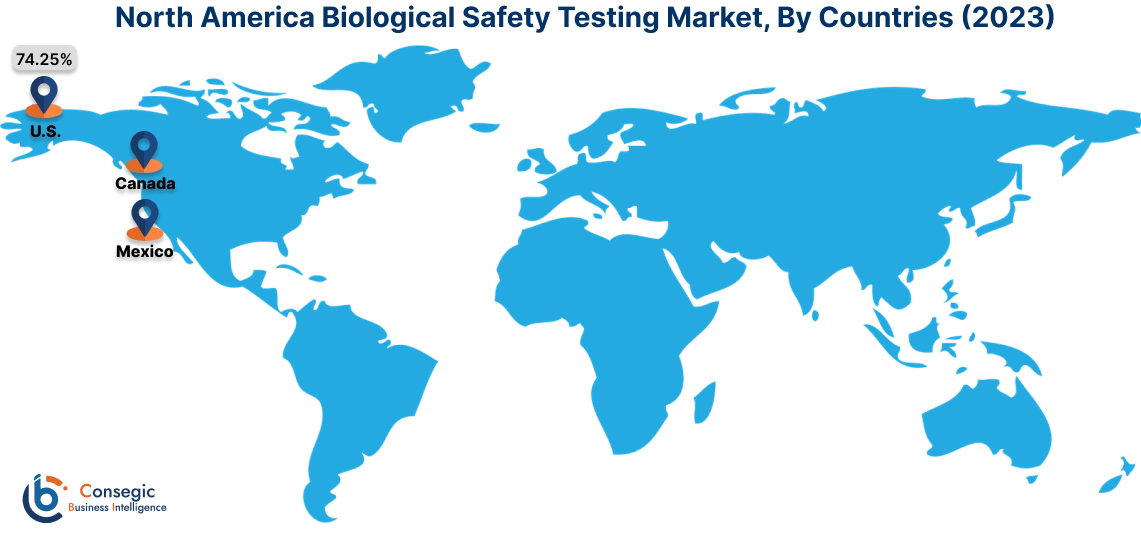

In 2023, North America accounted for the highest market share at 39.55% and was valued at USD 1,475.40 Million and is expected to reach USD 3,301.97 Million in 2031. In North America, the U.S. accounted for the highest share of 74.25% during the base year of 2023. North America holds a dominant share in the biological safety testing market analysis, driven by a well-established biotechnology and pharmaceutical industry. The U.S. leads the region, fueled by a high number of biologics and biosimilar product approvals, as well as stringent regulatory requirements set by the FDA for biological safety testing. The market benefits from the presence of numerous biopharmaceutical companies and a strong focus on developing new vaccines and gene therapies. Canada also contributes to market growth, particularly in the area of cell and gene therapy testing. However, the high costs associated with compliance and rigorous testing requirements can be a challenge for smaller biotech firms.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 11.3% over the forecast period. Asia-Pacific is the fastest-growing region in the biological safety testing market, driven by rapid adoption in the biotechnology and pharmaceutical sectors in countries like China, India, and Japan. China's analysis shows increasing investments in biosimilar production and biopharmaceutical manufacturing are significantly driving the demand for comprehensive biological safety testing. Japan's robust focus on regenerative medicine and cell therapy products requires stringent safety testing protocols. India's growing biopharma sector, supported by a surge in vaccine development projects, is also contributing to the market. However, the region faces challenges due to varying regulatory standards and limited access to advanced testing technologies in certain areas.

Europe is a significant market for biological safety testing, supported by strong regulatory frameworks and a growing emphasis on biosafety. The region's market is led by the UK, Germany, and France, driven by the increasing development of biologics, vaccines, and biosimilars. The European Medicines Agency (EMA) has stringent safety testing guidelines, which have led to a high demand for advanced endotoxin, sterility, and bioburden testing services. Germany's focus on biopharmaceutical innovation and the UK's expanding biosimilar market are major growth drivers. However, the market faces challenges related to the lengthy approval processes and high costs of testing, which can delay product launches.

The Middle East & Africa region is experiencing steady development in the biological safety testing market, with increasing investments in healthcare and biotechnology research in countries like the UAE and Saudi Arabia. The UAE's expanding focus on life sciences and the establishment of specialized testing labs are driving the biological safety testing market demand, particularly for vaccine and gene therapy products. Saudi Arabia's Vision 2030 initiative aims to enhance biopharmaceutical manufacturing capabilities, further boosting the need for comprehensive safety testing services. However, limited local expertise and infrastructure for advanced biological testing can hinder market expansion in some parts of Africa.

Latin America is an emerging market for biological safety testing, with Brazil and Mexico leading the way. The growing focus on biosimilar, vaccine development, and clinical trials in Brazil is driving demand for endotoxin, sterility, and cell line authentication testing. Mexico's expanding pharmaceutical and biopharmaceutical industry, along with increasing investments in research and development, supports market advancement. However, challenges such as inconsistent regulatory frameworks and limited funding for advanced testing technologies can impact the adoption of biological safety testing services in the region.

Top Key Players & Market Share Insights:

The Biological safety testing market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Biological safety testing market. Key players in the Biological safety testing market industry include -

- Charles River Laboratories (USA)

- Merck KGaA (Germany)

- Lonza Group Ltd. (Switzerland)

- Sartorius AG (Germany)

- Eurofins Scientific (Luxembourg)

- SGS S.A. (Switzerland)

- Thermo Fisher Scientific Inc. (USA)

- WuXi AppTec (China)

- Samsung Biologics (South Korea)

- Cytovance Biologics (USA)

Recent Industry Developments :

Technological Advancements:

- In February 2023, Lonza adopted innovative endotoxin testing techniques designed to streamline safety assessments in production processes, ensuring greater reliability and operational efficiency.

- In February 2022, India significantly enhanced its biological safety testing capabilities by introducing its first mobile biosafety Level 3 laboratory, enabling advanced research on highly infectious diseases.

Biological Safety Testing Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 8,327.78 Million |

| CAGR (2024-2031) | 10.8% |

| By Test Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the biological safety testing market? +

Biological safety testing market size is estimated to reach over USD 8,327.78 Million by 2031 from a value of USD 3,730.46 Million in 2023, growing at a CAGR of 10.8% from 2024 to 2031.

Which region dominates the biological safety testing market? +

North America leads the market due to strong regulatory frameworks and high R&D activity in biotechnology.

What are the main drivers of the market? +

Rising demand for biologics and vaccines, along with stringent safety regulations, are key growth drivers.

What challenges does the biological safety testing market face? +

High testing costs and complex regulatory compliance requirements are major restraining factors.

What are the key opportunities in the market? +

Innovations in rapid testing methods and increasing investments in cell and gene therapy offer significant growth opportunities.