- Summary

- Table Of Content

- Methodology

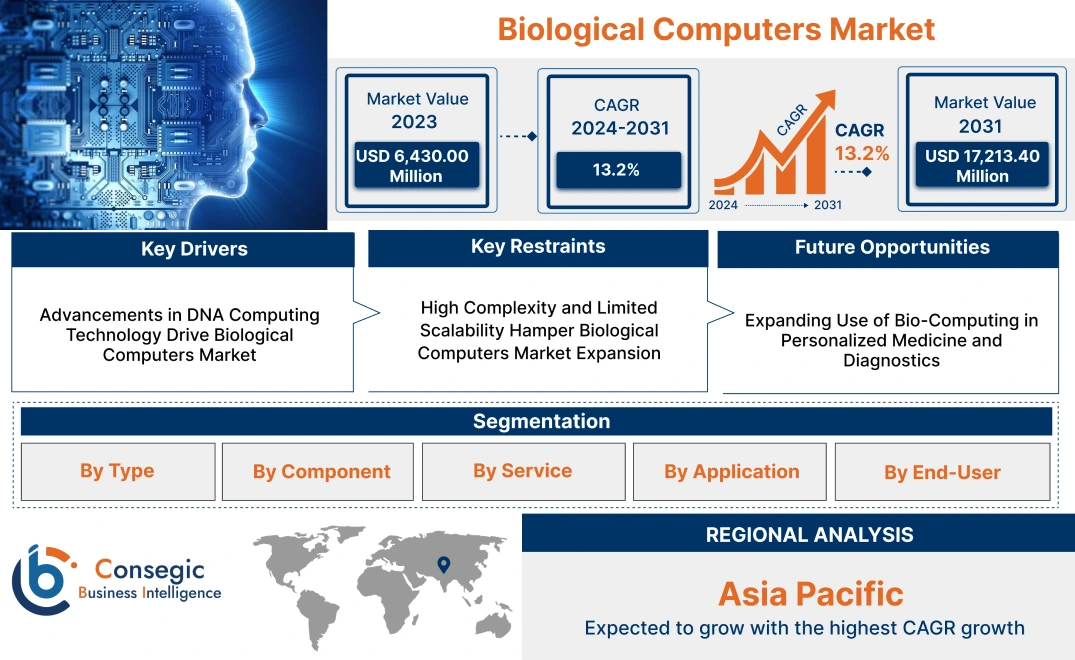

Biological Computers Market Size:

Biological Computers Market size is estimated to reach over USD 17,213.40 Million by 2031 from a value of USD 6,430.00 Million in 2023, growing at a CAGR of 13.2% from 2024 to 2031.

Biological Computers Market Scope & Overview:

The biological computers are computing systems that utilize biological molecules, like DNA, proteins, and enzymes, to perform complex computations. Unlike traditional silicon-based computers, biological computers leverage biochemical reactions to process information, offering unique capabilities for parallel processing and data storage. Key features include high-density data storage, the potential for self-repair, and the ability to function in biological environments. The benefits of biological computers include reduced energy consumption, increased computational efficiency, and enhanced integration with biological systems, making them suitable for applications in medical diagnostics, genetic research, and personalized medicine. The primary applications span DNA sequencing, targeted drug delivery, and biosensing. End-users include research institutions, pharmaceutical companies, and biotechnology firms, driven by increasing interest in advanced computing solutions and the growing demand for innovative approaches in biomedical research and healthcare.

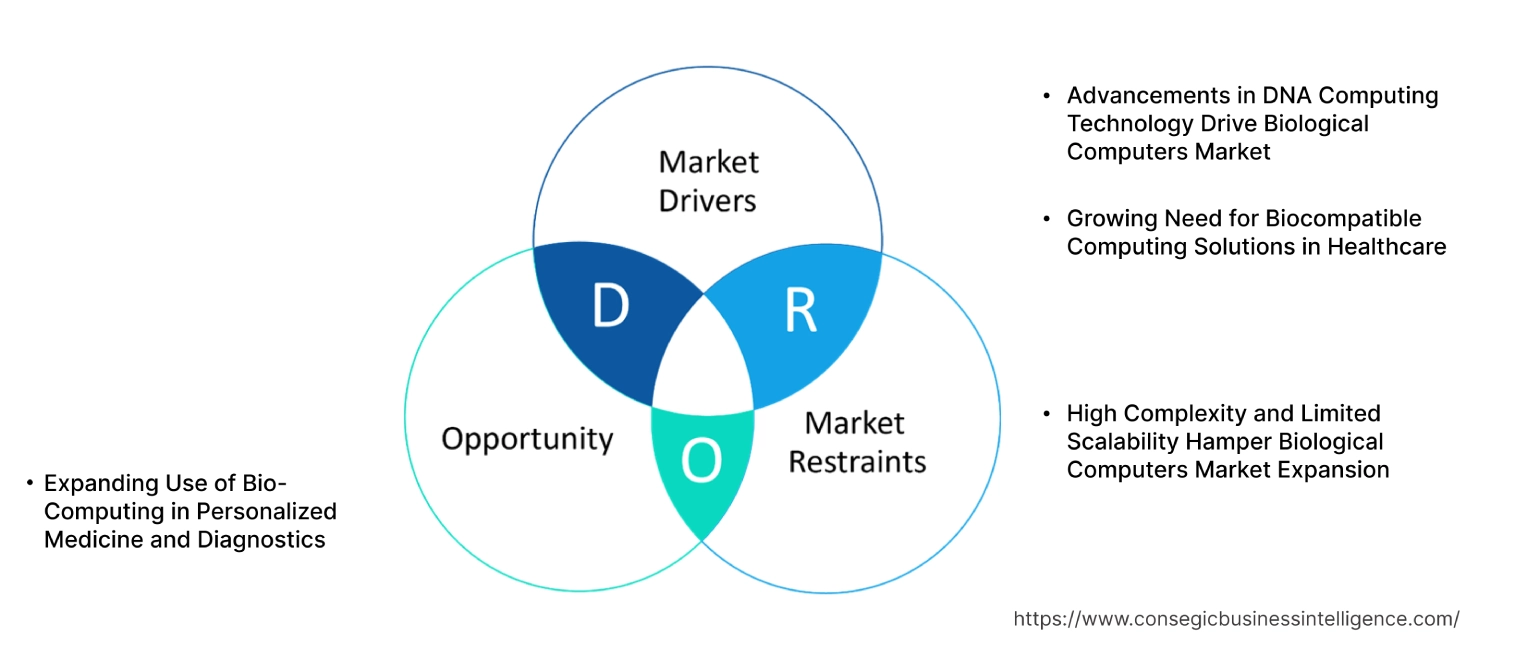

Biological Computers Market Dynamics - (DRO) :

Key Drivers:

Advancements in DNA Computing Technology Drive Biological Computers Market

Recent breakthroughs in DNA computing technology are a significant driver for the market. Unlike traditional silicon-based systems, DNA computing leverages the unique properties of nucleic acids to perform complex parallel processing and data storage tasks at the molecular level. Advancements in synthetic DNA synthesis and precise gene editing techniques, such as CRISPR-Cas9, have enabled the development of more efficient bio-computing systems capable of solving problems like cryptographic algorithms and combinatorial optimization. For instance, new methods in molecular logic gates and DNA-based circuits can process massive datasets simultaneously, offering enhanced computational power for applications in cryptography, bioinformatics, and complex system modeling. The increasing investment in DNA nanotechnology and molecular computing research is driving the adoption of bio-computing systems across industries, particularly in fields requiring high computational efficiency and innovative data processing capabilities.

Growing Need for Biocompatible Computing Solutions in Healthcare

The rising demand for biocompatible computing trends solutions in healthcare is propelling the biological computers market growth. It, made from naturally occurring biomolecules, offers seamless integration with living systems, making it ideal for real-time diagnostics and therapeutic applications. For instance, DNA-based biosensors are being developed for detecting specific biomarkers in diseases like cancer, diabetes, and neurodegenerative disorders. These bio-computing devices can interact directly with cellular processes, enabling personalized drug delivery and monitoring of physiological conditions at a molecular level. The adoption of biocompatible computing systems in precision medicine is gaining traction, as they provide targeted and less invasive diagnostic tools compared to conventional electronic devices. This growing interest in harnessing bio-computing for tailored healthcare solutions is expected to drive further biological computers market growth.

Key Restraints :

High Complexity and Limited Scalability Hamper Biological Computers Market Expansion

The high complexity of designing biological computers and the limited scalability of current bio-computing systems are major restraints in the market. It relies heavily on complex biochemical reactions and precise molecular interactions, making it challenging to create standardized, reliable, and reproducible computing devices. The lack of uniform protocols for DNA synthesis, data encoding, and signal processing leads to inconsistencies in performance, especially when scaling up bio-computing systems for industrial or commercial applications. Moreover, the integration of biological components with conventional hardware remains a significant technical hurdle, limiting the practical use of bio-computing systems in larger-scale projects. The intricate nature of bio-computing design, coupled with issues like enzymatic degradation and environmental sensitivity of biomolecules, makes the development and mass production of robust bio-computing devices challenging, hindering the market trends and widespread adoption of these technologies.

Future Opportunities :

Expanding Use of Bio-Computing in Personalized Medicine and Diagnostics

The increasing focus on personalized medicine and advanced diagnostics presents a significant biological computers market opportunity. Bio-computing systems offer unique capabilities for analyzing molecular data at a cellular level, making them highly suited for personalized treatment planning and patient monitoring. For instance, DNA-based computing devices can act as molecular diagnostic tools, capable of detecting specific genetic mutations and biomarkers associated with various diseases, such as cancer or cardiovascular conditions. These systems can be integrated with next-generation sequencing technologies, providing real-time insights into patient health and enabling tailored therapeutic approaches. As healthcare providers shift towards precision medicine, the adoption of bio-computing in clinical diagnostics is expected to grow, driven by its ability to offer highly accurate, individualized data analysis. This expanding use of bio-computing technologies in the healthcare sector is set to create new application avenues for market participants focused on innovative, patient-centric solutions.

Biological Computers Market Segmental Analysis :

By Type:

Based on type, the global biological computers market is segmented into DNA-based computers, RNA-based computers, protein-based computers, and cellular computers.

The DNA-based computers segment accounted for the largest revenue share in 2023.

- DNA-based computers are at the forefront of the market due to their high storage capacity, parallel processing capabilities, and efficiency in complex problem-solving.

- These computers utilize DNA molecules as data carriers, leveraging the inherent biological properties of DNA for computations, including data encoding and logic operations.

- Their applications span from advanced cryptography to solving combinatorial problems that traditional silicon-based computers struggle with.

- The growing interest in DNA computing for big data analysis and complex biological simulations is a key driver for this segment's dominance.

- DNA-based computers lead the market due to their superior data storage capabilities and increasing use of new opportunities in the industry and complex problem-solving applications, particularly in big data analysis and cryptography.

The protein-based computers segment is anticipated to register the fastest CAGR during the forecast period.

- Protein-based computers utilize proteins as computational elements, offering unique advantages in terms of dynamic biochemical reactions and real-time responsiveness to environmental changes.

- These computers are emerging as critical tools in biosensing and molecular diagnostics due to their ability to process biological signals at the molecular level.

- Advances in synthetic biology and protein engineering are enabling the development of protein circuits with enhanced computational efficiency, driving rapid appeal in this segment.

- The increasing use of protein-based computers in drug discovery and real-time diagnostic applications is further accelerating their adoption.

- Protein-based computers are expected to grow rapidly, driven by advancements in synthetic biology and their application in molecular diagnostics and real-time biosensing.

By Component:

Based on components, the market is segmented into biological hardware (molecular circuits, biochips), software, and biocompatible interfaces.

The biological hardware segment accounted for the largest revenue share in 2023.

- Biological hardware, including molecular circuits and biochips, forms the core of biological computing systems.

- These components enable the processing of biochemical signals and execution of logic operations within a biological framework.

- Molecular circuits, built from DNA, RNA, or proteins, are designed to perform specific computational tasks, while biochips integrate these circuits into functional computing devices.

- The increasing opportunities focus on developing biochips with higher computational efficiency and miniaturization capabilities is driving demand in this segment, particularly for applications in diagnostics and drug discovery.

- Therefore, biological hardware dominates the market due to its fundamental role in enabling biochemical computations and the growing demand for high-efficiency biochips in the diagnostic and pharmaceutical applications industry.

The biocompatible interfaces segment is anticipated to register the fastest CAGR during the forecast period.

- Biocompatible interfaces are essential for integrating biological computers with living tissues, facilitating seamless interaction between synthetic devices and biological systems.

- These interfaces are crucial in applications such as medical implants and biosensors, where real-time monitoring and data exchange are required.

- The development of advanced, biocompatible materials that minimize immune responses and enhance integration is driving growth in this segment.

- The increasing adoption of this market in personalized medicine and tissue engineering is further propelling the trends for biocompatible interfaces.

- Thus, biocompatible interfaces are expected to grow rapidly, the biological computers market analysis shows, the driving trends and advancements in material science and their critical role in enabling the seamless integration of biological computers with living systems.

By Service:

Based on service, the market is segmented into in-house and contract services.

The in-house segment accounted for the largest revenue biological computers market share in 2023.

- In-house services involve the development and deployment of biological computing systems within the facilities of pharmaceutical and biotechnology companies.

- These companies often prefer in-house solutions to maintain control over proprietary technologies, data security, and customization of biological computing systems for specific research needs.

- The increasing focus on developing proprietary biological computing platforms for drug discovery, diagnostics, and personalized medicine is supporting the advancement of in-house services.

- This approach also allows for greater flexibility and integration with existing laboratory infrastructure.

- In-house services lead the market, driven by the preference for control over proprietary technologies and the need for customized biological computing solutions in pharmaceutical research.

The contract services segment is anticipated to register the fastest CAGR during the forecast period.

- Contract services are becoming increasingly popular as companies seek to outsource the development and testing of biological computing systems to specialized service providers.

- These providers offer expertise in biological hardware, software integration, and system validation, reducing the need for in-house capabilities.

- The growing trend of outsourcing complex projects to leverage external expertise and reduce operational costs is driving the adoption of contract services.

- Additionally, the expanding ecosystem of contract research organizations (CROs) specializing in biological computing market trends further fueling development in this segment.

- Contract services trends are expected to grow rapidly, driven by the increasing trend of outsourcing and the expansion of specialized service providers in the biological computing field.

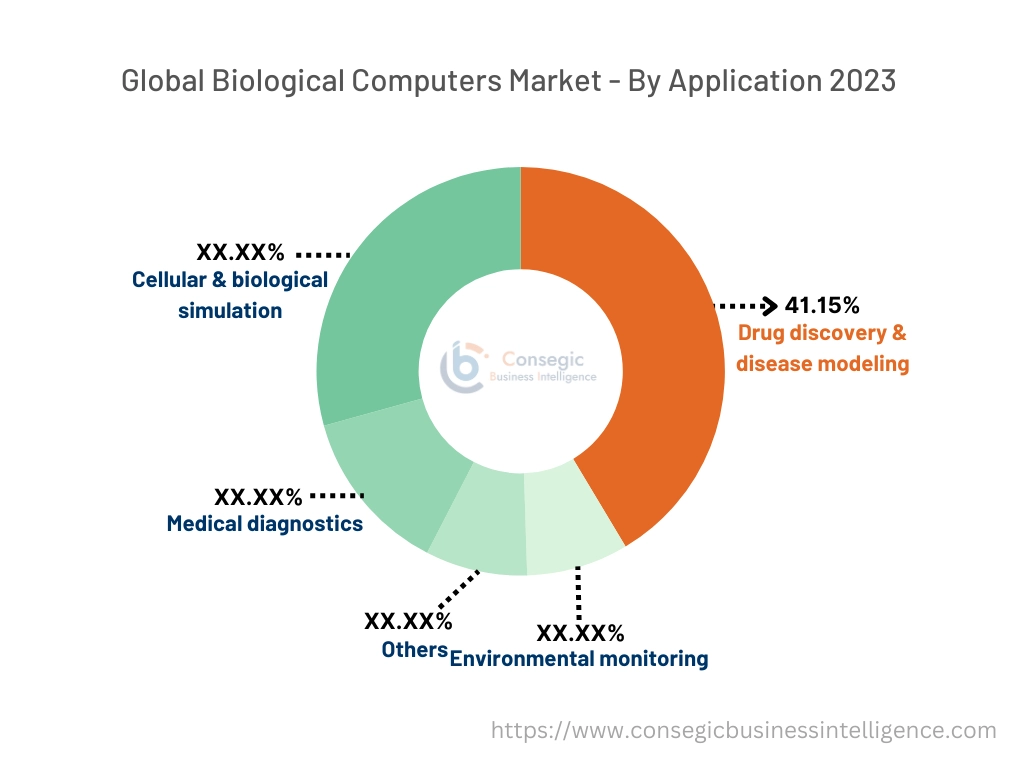

By Application:

Based on application, the market is segmented into medical diagnostics, cellular & biological simulation, drug discovery & disease modeling, environmental monitoring, and others.

The drug discovery & disease modeling segment accounted for the largest revenue of 41.15% in the biological computers market share in 2023.

- Biological computers are revolutionizing drug discovery and disease modeling by enabling precise simulations of cellular processes and interactions at the molecular level.

- These computers allow researchers to model complex biological pathways, predict drug interactions, and optimize lead compounds with greater accuracy.

- The increasing use of biological computing platforms in early-stage drug development and the growing emphasis on precision medicine are major factors driving the growth of this segment.

- The ability to accelerate drug discovery timelines while reducing costs and improving predictive accuracy is a key advantage.

- Drug discovery & disease modeling lead the market trends due to the increasing adoption of biological computing platforms for efficient and accurate drug development processes.

The medical diagnostics segment is anticipated to register the fastest CAGR during the forecast period.

- Biological computers are being increasingly integrated into diagnostic tools for real-time analysis of complex biological signals.

- Their ability to process biochemical data at the molecular level makes them ideal for detecting biomarkers associated with various diseases, including cancer and infectious diseases.

- The rising biological computing market demand for point-of-care diagnostics and personalized medicine solutions is driving the adoption of medical diagnostics.

- Ongoing advancements in bio-sensing technologies and biochip integration are further enhancing the capabilities of biological computers in this segment.

- Medical diagnostics is expected to grow rapidly, supported by the increasing demand for real-time, molecular-level analysis and advancements in bio-sensing technologies.

By End-User:

Based on end-user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, healthcare IT companies, environmental agencies, and others.

The pharmaceutical & biotechnology companies segment accounted for the largest revenue share in 2023.

- Pharmaceutical and biotechnology companies are the primary users of biological computing systems, leveraging these technologies for drug discovery, molecular diagnostics, and personalized medicine.

- The integration of biological computers in early-stage drug development and clinical research is enhancing the efficiency and accuracy of therapeutic discoveries.

- The increasing focus on complex disease modeling and the biological computers market demand for innovative drug discovery tools are driving significant investment in this market by pharmaceutical companies.

- Pharmaceutical & biotechnology companies dominate the market due to their extensive use of biological computing for drug discovery and the development of advanced diagnostic tools.

The academic & research institutes segment is anticipated to register the fastest CAGR during the forecast period.

- Academic and research institutes are at the forefront of developing new biological computing technologies and exploring novel applications.

- These institutions play a crucial role in advancing foundational research, including the design of new molecular circuits, biochips, and biocompatible materials.

- The growing number of collaborative research projects and increased funding for biological computing research are driving the rapid growth of this segment.

- Academic & research institutes are expected to grow rapidly, driven by their pivotal role in advancing biological computing technologies and the increasing funding trends for collaborative research initiatives.

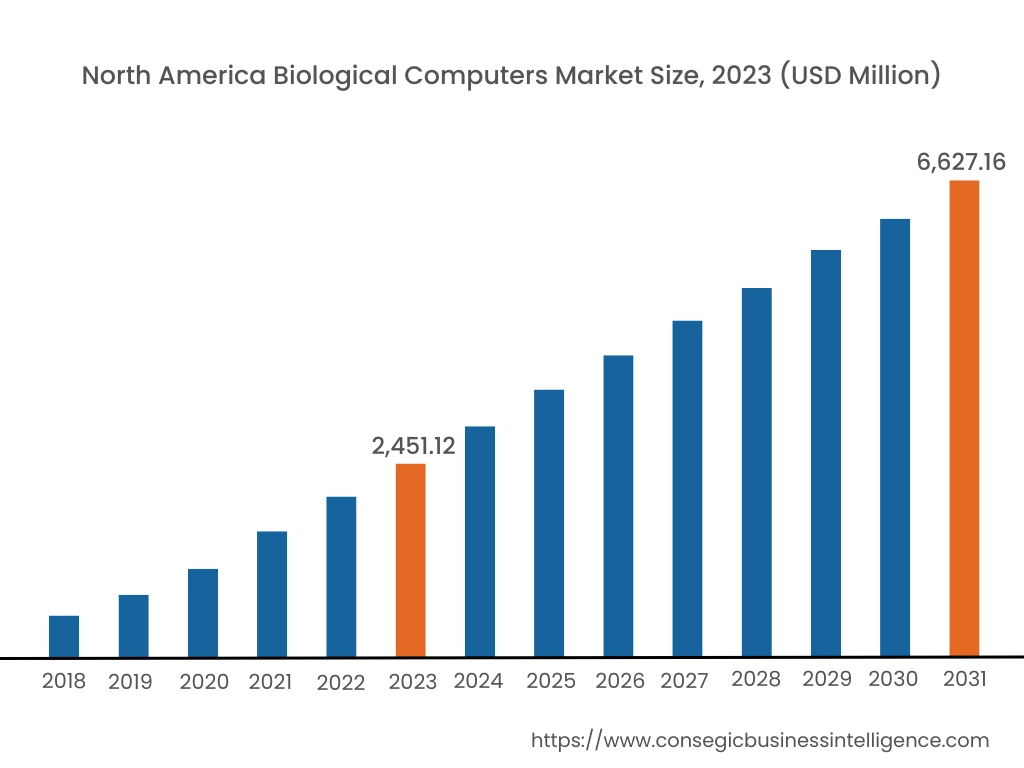

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2023, North America accounted for the highest market share at 38.12% and was valued at USD 2,451.12 Million and is expected to reach USD 6,627.16 Million in 2031. In North America, the U.S. accounted for the highest share of 72.25% during the base year of 2023. North America is a leading region in the biological computers market, driven by significant investments in research and innovation. The U.S. is at the forefront, with strong support from academic institutions and biotechnology firms focused on developing DNA-based and RNA-based computing systems for medical diagnostics and drug discovery. The collaboration between tech giants and biotech startups is accelerating advancements in bio-computation, particularly in personalized medicine and disease modeling. Canada is also contributing to market growth with research initiatives in biocompatible interfaces for healthcare applications. However, regulatory hurdles and ethical concerns around bio-computing technologies remain key challenges in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 13.9% over the forecast period. Asia-Pacific market is driven by increasing investments in biotechnology and synthetic biology, particularly in China, Japan, and South Korea. China's push towards becoming a global leader in advanced healthcare technologies includes substantial funding for DNA-based computing research and the development of biocompatible hardware. Japan is focusing on integrating biological computing with traditional healthcare systems to enhance diagnostic capabilities, especially in the context of aging populations. South Korea's growing emphasis on precision medicine and bioinformatics research is accelerating the development of cellular computing systems. However, challenges such as varying regulatory frameworks and limited access to cutting-edge technologies in some areas hinder the market's full potential.

Europe is a significant player in the biological computers market, supported by robust research funding and a focus on precision medicine. Countries like Germany, the UK, and France are leading the region, with active projects in cellular computers and biochips for real-time disease monitoring. The European Union's emphasis on advancing synthetic biology and bioinformatics under its Horizon Europe program is boosting innovation in biological computing. Germany's strong biotechnology industry and the UK's focus on computational biology are driving applications in drug discovery and environmental monitoring. However, strict regulatory standards and complex approval processes for biological computing devices may slow down commercialization efforts.

Top Key Players & Market Share Insights:

The Biological Computers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Biological Computers market. Key players in the Biological Computers industry include -

- Biometrix Technology Inc. (USA)

- Emulate Inc. (USA)

- IBM (USA)

- Illumina, Inc. (USA)

- IndieBio (USA)

- Macrogen Corp. (South Korea)

- Merck KGaA (Germany)

- Microsoft (USA)

- Sequenom Inc. (USA)

- Thermo Fisher Scientific (USA)

Recent Industry Developments :

Product Launch:

- In March 2024, MiLaboratories launched Platforma.bio, a computational biology platform utilizing AI-powered large language models to simplify and democratize biological analysis for researchers across various disciplines.

Technological Advancements:

- In May 2022, Ajinomoto adopted Genedata Bioprocess® to digitalize and automate R&D and manufacturing operations in Japan and Korea, enhancing efficiency in biopharmaceutical development.

Biological Computers Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 17,213.40 Million |

| CAGR (2024-2031) | 13.2% |

| By Type |

|

| By Component |

|

| By Service |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Biological Computers Market by 2031? +

The market is projected to reach over USD 17,213.40 Million by 2031, growing at a CAGR of 13.2% from 2024 to 2031.

What are the key drivers of growth in the biological computers market? +

Advancements in DNA computing technology, including synthetic DNA synthesis and gene editing techniques like CRISPR-Cas9.

Which region leads the biological computers market? +

North America leads the market with the highest share, supported by investments in research, innovation, and collaboration between tech giants and biotech startups.

Who are the key players in the biological computers market? +

Leading players include IBM (USA), Illumina, Inc. (USA), Merck KGaA (Germany), Thermo Fisher Scientific (USA), and Macrogen Corp. (South Korea).