- Summary

- Table Of Content

- Methodology

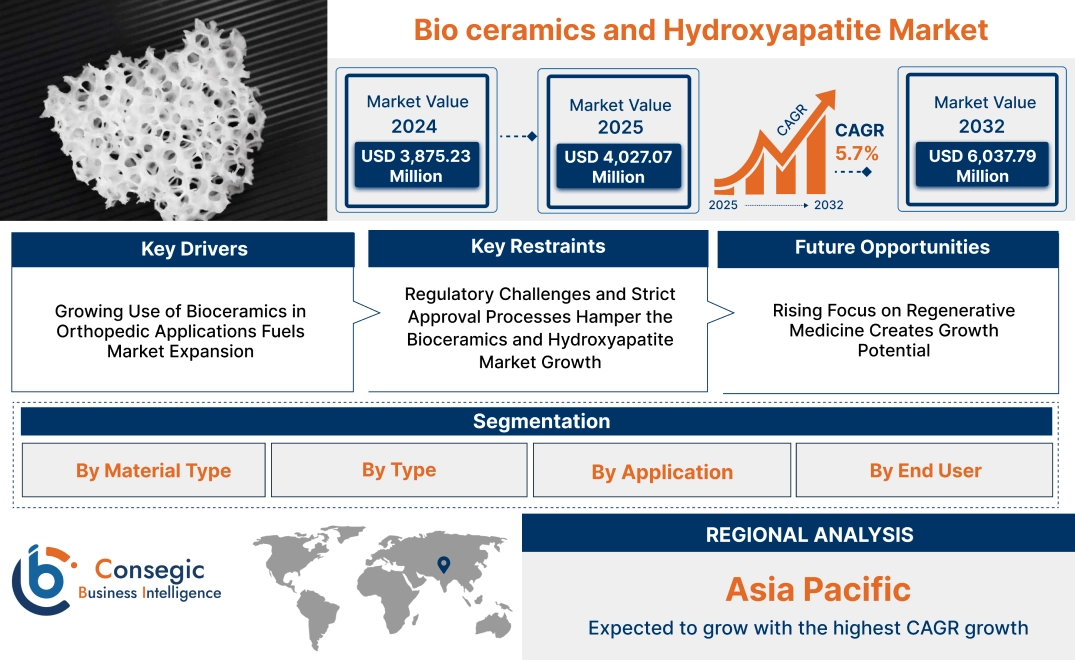

Bioceramics and Hydroxyapatite Market Size:

Bioceramics and Hydroxyapatite Market size is estimated to reach over USD 6,037.79 Million by 2032 from a value of USD 3,875.23 Million in 2024 and is projected to grow by USD 4,027.07 Million in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Bioceramics and Hydroxyapatite Market Scope & Overview:

The bioceramics and hydroxyapatite market involves the development and use of ceramic materials for medical and dental applications, particularly in bone and tooth repair. Bioceramics, including hydroxyapatite, alumina, and zirconia, are biocompatible, making them ideal for implants, bone grafts, and dental restorations. Hydroxyapatite, a calcium phosphate compound, closely resembles natural bone mineral, promoting osseointegration and enhancing bone regeneration. Key characteristics of these materials include high biocompatibility, durability, and resistance to wear. The primary benefits include improved healing, reduced risk of infection, and enhanced integration with surrounding tissues. Applications range from orthopedic implants and dental implants to bone fillers and tissue engineering scaffolds. End-users include hospitals, dental clinics, research laboratories, and biopharmaceutical companies, driven by the increasing prevalence of bone-related disorders, advancements in implant technologies, and the rising demand for bioactive and biocompatible materials in medical procedures.

Bioceramics and Hydroxyapatite Market Dynamics - (DRO) :

Key Drivers:

Growing Use of Bioceramics in Orthopedic Applications Fuels Market Expansion

The expanding use of bioceramics in orthopedic applications is driving Bioceramics and Hydroxyapatite Market growth. Bioceramics such as hydroxyapatite and zirconia are widely utilized in bone grafts, joint replacements, and fracture repair due to their excellent biocompatibility and ability to bond with natural bone. The rising incidence of orthopedic conditions, including osteoarthritis, bone fractures, and joint degeneration, is boosting the Bioceramics and Hydroxyapatite Market demand for innovative, bioactive materials that enhance healing and reduce recovery time. As the healthcare industry shifts towards minimally invasive surgical techniques, the applications for advanced bioceramic materials in orthopedic implants and prosthetics is increasing, contributing to Bioceramics and Hydroxyapatite Market expansion.

Key Restraints:

Regulatory Challenges and Strict Approval Processes Hamper the Bioceramics and Hydroxyapatite Market Growth

The bioceramics and hydroxyapatite market faces significant restraints due to stringent regulatory requirements and complex approval processes. Bioceramic materials used in medical and dental applications must undergo extensive testing for safety, biocompatibility, and efficacy before they can be approved for clinical use. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose rigorous guidelines for the evaluation of these materials, increasing the time and cost associated with product development. This regulatory burden can delay the commercialization of new bioceramic products, limiting market development and innovation, especially for smaller manufacturers.

Future Opportunities :

Rising Focus on Regenerative Medicine Creates Growth Potential

The increasing focus on regenerative medicine and tissue engineering offers a significant opportunity for the bioceramics and hydroxyapatite market. Bioceramics, especially hydroxyapatite, are used as scaffolding materials in regenerative applications due to their bioactive properties and ability to support cell rise and tissue regeneration. The growing interest in developing bioactive implants and bone graft substitutes for complex tissue reconstruction is driving demand for innovative bioceramic materials. Advancements in 3D printing technology are further enhancing the potential for custom-designed bioceramic implants, providing tailored solutions for individual patients and expanding Bioceramics and Hydroxyapatite Market opportunities.

Bioceramics and Hydroxyapatite Market Segmental Analysis :

By Material Type:

Based on material type, the bioceramics and hydroxyapatite market is segmented into hydroxyapatite (HA), zirconia, aluminum oxide, calcium phosphate, and others.

The hydroxyapatite (HA) segment accounted for the largest revenue in Bioceramics and Hydroxyapatite Market share in 2024.

- Hydroxyapatite, a naturally occurring form of calcium apatite, is extensively used in medical applications due to its excellent biocompatibility and osteoconductive properties.

- It closely mimics the mineral component of human bone, making it the material of choice for bone grafts, coatings on orthopedic and dental implants, and tissue engineering scaffolds.

- The rising demand for bone regeneration materials, particularly in orthopedic and dental surgeries, is driving the dominance of hydroxyapatite in this segment.

- Additionally, advancements in synthetic hydroxyapatite production are improving its mechanical properties, further expanding its applications.

- Thus, hydroxyapatite analysis leads the bioceramics and hydroxyapatite market trends due to its superior biocompatibility and extensive use in bone-related applications, supported by advancements in synthetic production techniques.

The zirconia segment is anticipated to register the fastest CAGR during the forecast period.

- Zirconia is known for its high strength, toughness, and wear resistance, making it ideal for dental and orthopedic implants.

- Its bio-inert nature ensures long-term stability without adverse tissue reactions, making it increasingly popular in dental crowns, bridges, and hip replacements.

- The trends of the dental sectors coupled with the analysis for durable and aesthetic implant materials, is propelling the adoption of zirconia.

- Ongoing innovations in zirconia-based ceramics, such as enhanced translucency for better aesthetic appeal in dental restorations, are further driving the market.

- Therefore, according the analysis zirconia is expected to grow rapidly, driven by its superior mechanical properties and increasing trends use in high-strength dental and orthopedic applications.

By Type:

Based on type, the market is segmented into bio-inert, bio-active, and bio-resorbable bioceramics.

The bio-inert segment accounted for the largest revenue share in 2024.

- Bio-inert ceramics, including zirconia and alumina, are designed to be chemically stable and non-reactive when implanted in the body.

- These materials provide excellent wear resistance and mechanical strength, making them suitable for load-bearing applications such as hip and knee replacements.

- The long-term stability of bio-inert ceramics and their widespread use in orthopedic and dental implants support their leading position.

- The segment’s analysis is further driven by the increasing adoption of zirconia in dental restorations and alumina in joint replacements.

- Bio-inert ceramics dominate the market, driven by their chemical stability and mechanical strength, making them ideal for load-bearing implants in orthopedic and dental applications.

The bio-resorbable segment is anticipated to register the fastest CAGR during the forecast period.

- Bio-resorbable ceramics, such as certain calcium phosphates, are designed to degrade gradually in the body, being replaced by natural bone tissue over time.

- This property makes them highly suitable for bone grafts and tissue engineering applications. The rising demand for materials that support natural bone regeneration and reduce the need for secondary surgeries is driving the applications of bio-resorbable ceramics.

- Advancements in bio-resorbable ceramic formulations are enhancing their degradation rates and mechanical properties, further supporting their adoption in complex orthopedic and dental procedures.

- Therefore, the analysis shows bio-resorbable ceramics are expected to grow rapidly, supported by their role in promoting natural bone regeneration and reducing the need for follow-up surgeries.

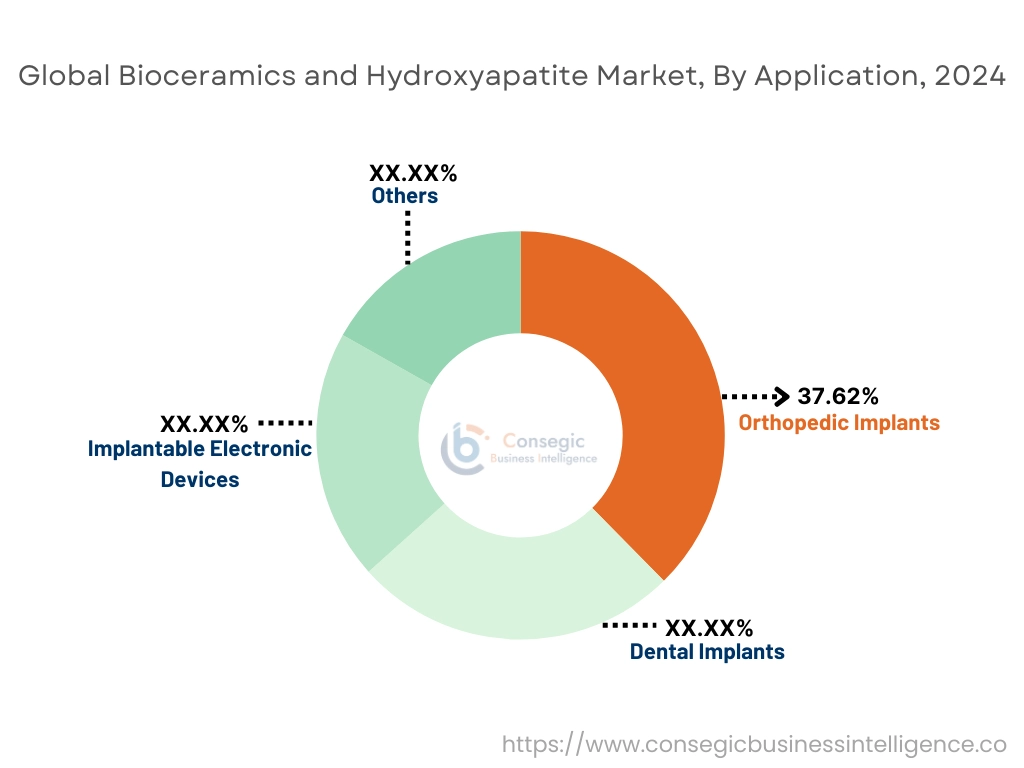

By Application:

Based on application, the bioceramics and hydroxyapatite market is segmented into orthopedic implants, dental implants, implantable electronic devices, and others.

The orthopedic implants segment accounted for the largest revenue of 37.62% share in 2024.

- Bioceramics are widely used in orthopedic implants due to their excellent biocompatibility and mechanical properties, which enhance the longevity and performance of implants.

- Materials like hydroxyapatite are frequently applied as coatings on metal implants to improve osseointegration, while zirconia and alumina are used in hip and knee replacements for their wear resistance.

- The increasing incidence of osteoarthritis, trauma cases, and the growing elderly population are driving the demand for orthopedic implants.

- Additionally, advancements in 3D printing technology are enabling the production of custom implants with enhanced bioceramic coatings.

- Orthopedic implants lead the market, driven by the superior properties of bioceramics that enhance implant performance and the growing rise for joint replacement surgeries.

The dental implants segment is anticipated to register the fastest CAGR during the forecast period.

- The dental sectors is increasingly adopting bioceramics, particularly zirconia and hydroxyapatite, for dental implants due to their aesthetic appeal and biocompatibility.

- Zirconia dental implants offer excellent strength and a natural tooth-like appearance, making them a preferred choice for patients seeking metal-free solutions.

- Hydroxyapatite coatings are used to enhance the integration of titanium implants with bone.

- The rising trends for cosmetic dentistry, the increasing prevalence of dental disorders, and the appeal of the aging population are key factors driving this segment's rapid advancment.

- Therefore, dental implants trends are expected to grow rapidly, supported by the increasing advancement for aesthetic, biocompatible materials and the rising adoption of metal-free zirconia implants.

By End User:

Based on end-user, the market is segmented into hospitals & clinics, research institutes, and others.

The hospitals & clinics segment accounted for the largest revenue in bioceramics and hydroxyapatite market share in 2024.

- Hospitals and clinics are the primary settings for the use of bioceramic materials, particularly in orthopedic and dental procedures.

- The increasing number of joint replacement surgeries, dental implant procedures, and trauma surgeries drives the appeal for bioceramics in these settings.

- The adoption of advanced bioceramic materials for implants and coatings, along with the availability of specialized surgical expertise, supports the dominance of this segment.

- The focus on improving patient outcomes and reducing recovery times further encourages the use of high-performance bioceramics.

- Therefore, hospitals & clinics dominate the market trends due to their role as primary providers of orthopedic and dental surgeries, where bioceramics are extensively used to enhance Bioceramics and Hydroxyapatite Market analysis implant success rates.

The research institutes segment is anticipated to register the fastest CAGR during the forecast period.

- Research institutes play a crucial role in the development of new bioceramic materials and applications.

- Ongoing research focuses on enhancing the properties of bioceramics, such as improving their mechanical strength, bioactivity, and resorbability for use in advanced medical applications.

- The increasing investment in biomaterials research, coupled with collaborative projects between academia and sector, is driving applications in this segment.

- Innovations in bioceramic formulations and fabrication techniques, including 3D printing, are further supporting the expansion of research activities.

- Research institutes are expected to grow rapidly, driven by ongoing advancements in bioceramic material science and increasing investments in biomaterials research.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

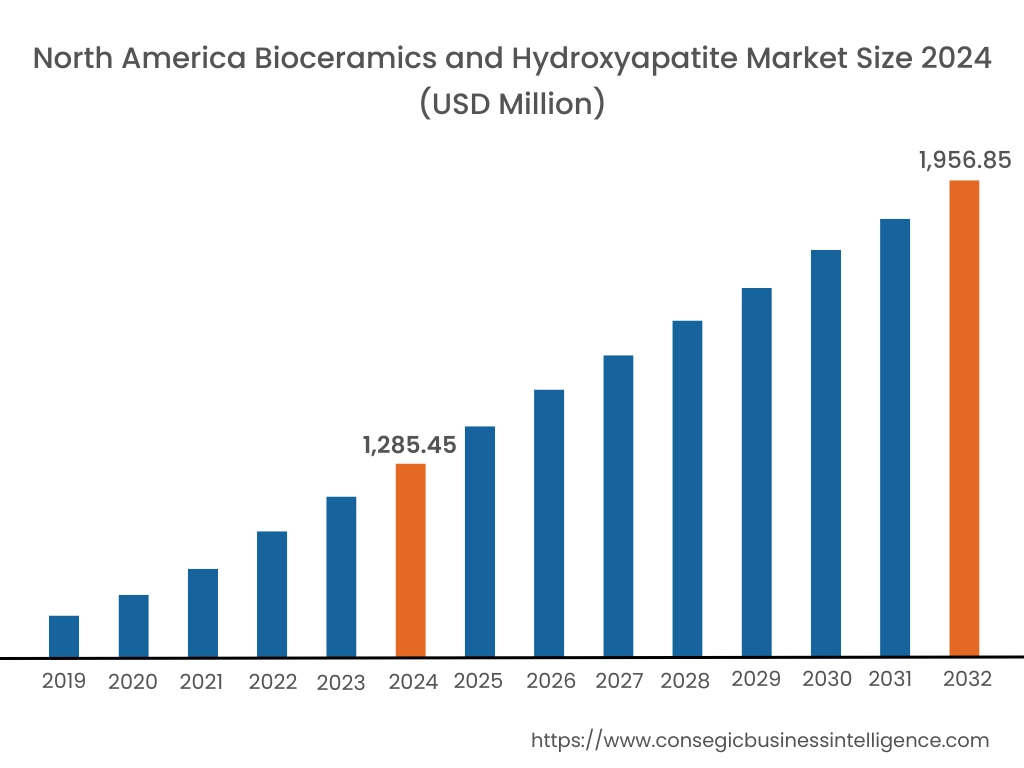

In 2024, North America was valued at USD 1,285.45 Million and is expected to reach USD 1,956.85 Million in 2032. In North America, the U.S. accounted for the highest share of 70.10% during the base year of 2024. North America dominates the bioceramics and hydroxyapatite market, driven by a strong presence of dental, orthopedic, and medical implant industries. The U.S. leads the region, benefiting from advanced healthcare infrastructure, high healthcare expenditure, and increasing rise for dental and orthopedic implants due to an aging population. The presence of key sector players and extensive research activities focused on innovative bioceramic materials for bone grafting and tissue engineering bolster the market. Canada is also contributing to the market, with rising adoption of hydroxyapatite in dental and orthopedic procedures. However, the high costs associated with bioceramics production and stringent regulatory requirements pose challenges.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 6.1% over the forecast period. Asia-Pacific is the fastest-growing region for bioceramics and hydroxyapatite, propelled by increasing healthcare expenditure, rising dental tourism, and expanding orthopedic implant markets in China, Japan, and India. China’s rapidly growing aging population and emphasis on improving healthcare infrastructure are boosting trends for dental and orthopedic implants. Japan’s advanced research in bioceramics for bone grafting and tissue engineering applications contributes significantly to market growth. In India, the increasing prevalence of bone-related disorders and rising awareness about dental health are driving the adoption of hydroxyapatite-based implants. However, challenges such as varying regulatory frameworks and limited local production capabilities hinder market expansion.

Europe is a significant market for bioceramics and hydroxyapatite, supported by strong appeals from the dental and orthopedic sectors in countries like Germany, France, and the UK. Germany’s robust medical device industry and focus on advanced materials for dental implants drive market growth. The UK is increasingly investing in research on hydroxyapatite coatings for joint replacements and bone regeneration. France is witnessing a rise in dental procedures using bioceramic materials due to increased awareness about dental health. However, strict regulatory standards and the high cost of advanced bioceramic materials are barriers to wider adoption.

The Middle East & Africa region is witnessing steady growth in the bioceramics and hydroxyapatite market, particularly in the UAE and South Africa. The UAE is investing heavily in advanced healthcare infrastructure, leading to increased rise for dental and orthopedic implants using bioceramic materials. Saudi Arabia’s focus on improving healthcare services and expanding medical device manufacturing supports the use of hydroxyapatite in bone grafts and implant coatings. In South Africa, rising cases of bone disorders and increasing healthcare investments are boosting the adoption of bioceramics. However, the region faces challenges related to limited local production and high costs of imported materials.

In Latin America, Brazil and Mexico are the leading markets for bioceramics and hydroxyapatite, driven by growing healthcare investments and increasing demand for dental and orthopedic implants. Brazil’s strong dental industry and focus on cosmetic dentistry drive the use of hydroxyapatite in dental applications. Mexico’s expanding medical tourism sector is boosting the trends for affordable and effective implant materials, including bioceramics. However, economic instability and limited regulatory support for innovative medical devices can affect the market’s growth potential in the region.

Top Key Players & Market Share Insights:

The Bioceramics and Hydroxyapatite Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Bioceramics and Hydroxyapatite Market. Key players in the Bioceramics and Hydroxyapatite Market industry include -

- Zimmer Biomet (USA)

- Stryker Corporation (USA)

- Taihei Chemical Industrial Co., Ltd. (Japan)

- SigmaGraft Biomaterials, Inc. (USA)

- Bonesupport AB (Sweden)

- Cam Bioceramics B.V. (Netherlands)

- Fluidinova, S.A. (Portugal)

- SofSera Corporation (Japan)

- Berkeley Advanced Biomaterials, Inc. (USA)

Bioceramics and Hydroxyapatite Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6,037.79 Million |

| CAGR (2025-2032) | 5.7% |

| By Material Type |

|

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Bioceramics and Hydroxyapatite market? +

Bioceramics and Hydroxyapatite Market size is estimated to reach over USD 6,037.79 Million by 2032 from a value of USD 3,875.23 Million in 2024 and is projected to grow by USD 4,027.07 Million in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

What are the main applications of bioceramics and hydroxyapatite? +

Key applications include orthopedic implants, dental implants, and implantable electronic devices.

Which region leads the bioceramics and hydroxyapatite market? +

North America holds the largest market share, driven by advanced healthcare infrastructure and high adoption of medical implants.

What challenges does the bioceramics market face? +

High production costs and complexities in material design are key restraints for market growth.

What are the growth opportunities in this market? +

Increasing use of bio-active and bio-resorbable materials in dental and orthopedic implants presents significant growth opportunities.