- Summary

- Table Of Content

- Methodology

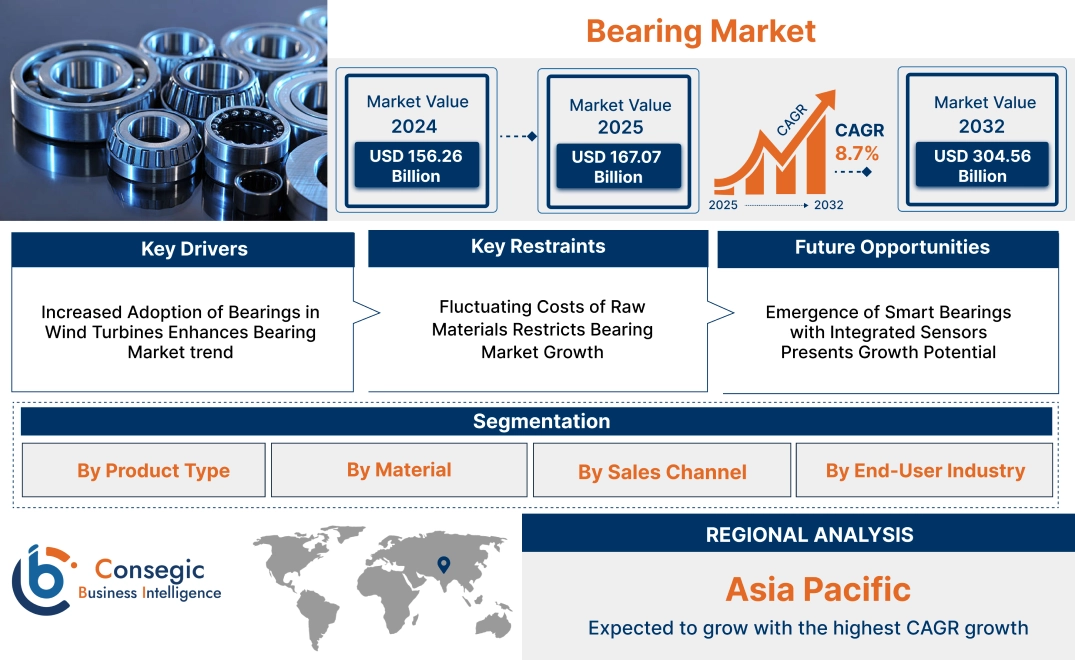

Bearing Market Size:

Bearing Market size is estimated to reach over USD 304.56 Billion by 2032 from a value of USD 156.26 Billion in 2024 and is projected to grow by USD 167.07 Billion in 2025, growing at a CAGR of 8.7% from 2025 to 2032.

Bearing Market Scope & Overview:

Bearings are mechanical components designed to reduce friction between moving parts and support rotational or linear motion within machinery. They are critical for efficient mechanical operation. Key properties include durability, high load-bearing capacity, and resistance to wear and heat. Bearings enhance operational efficiency by minimizing energy loss and ensuring smooth movement. The benefits include reduced friction, extended machinery lifespan, improved operational performance, and energy efficiency in industrial and mechanical systems. Applications include automotive components, industrial machinery, aerospace equipment, and medical devices requiring precise motion control. End-use industries encompass automotive, aerospace, manufacturing, construction, and healthcare sectors, where bearings contribute to enhanced machine reliability and performance.

Bearing Market Dynamics - (DRO) :

Key Drivers:

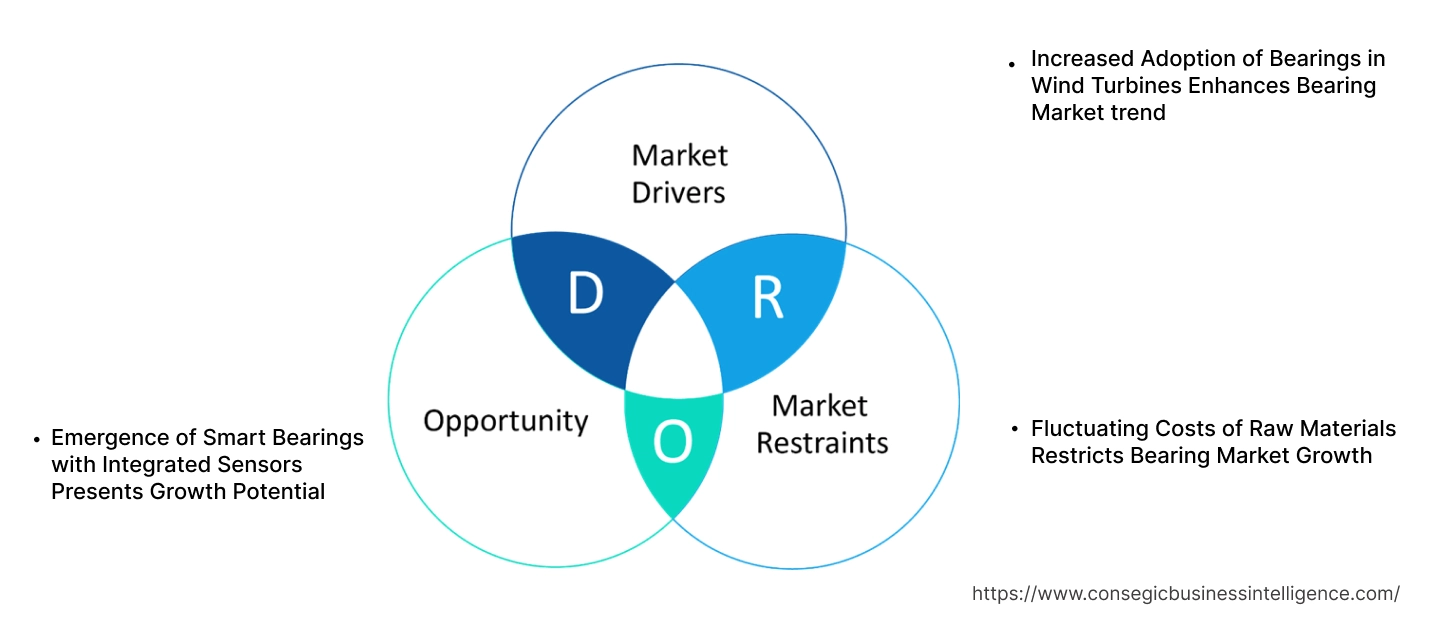

Increased Adoption of Bearings in Wind Turbines Enhances Bearing Market trend

The use of bearings in wind turbines plays a crucial role in ensuring smooth and efficient rotation of blades under varying loads and environmental conditions. Bearings reduce friction and support axial and radial loads, which are critical for the reliability and performance of wind turbines.

For example, as global investments in renewable energy increase, there is a rising demand for bearings in wind turbines to enhance energy generation efficiency. Manufacturers are developing specialized bearings to meet the durability and precision requirements of wind turbines.

Therefore, the increasing deployment of wind turbines for renewable energy generation is driving the bearing market trend.

Key Restraints:

Fluctuating Costs of Raw Materials Restricts Bearing Market Growth

The production of bearings relies heavily on raw materials like steel, which is subject to price volatility due to global supply-demand dynamics and geopolitical factors. This variability impacts manufacturing costs and profit margins for bearing manufacturers, making it challenging to maintain consistent pricing.

Additionally, the rising costs of advanced materials like ceramics and composites, which are used in high-performance bearings, further exacerbate the issue. Manufacturers may face difficulty in passing these costs to end users, particularly in price-sensitive markets. Thus, the uncertainty in raw material costs hampers the steady bearing market expansion.

Future Opportunities :

Emergence of Smart Bearings with Integrated Sensors Presents Growth Potential

The development of smart bearings equipped with integrated sensors for real-time monitoring of performance parameters is anticipated to create new Bearing market opportunities. These sensors enable predictive maintenance by monitoring factors like temperature, vibration, and load, reducing downtime and enhancing efficiency.

For instance, industries like automotive and aerospace are increasingly adopting smart bearings to ensure operational safety and minimize equipment failures. These advancements align with the growing emphasis on Industry 4.0 and IoT-enabled systems.

As industries continue to adopt predictive maintenance strategies, smart bearings are expected to revolutionize the bearing market trend and drive future growth.

Bearing Market Segmental Analysis :

By Product Type:

Based on product type, the bearing market is segmented into ball bearings (deep groove bearings and others), roller bearings (split, tapered, and others), plain bearings (journal plain bearing, linear plain bearings, thrust plain bearings, and others) and Others.

Ball Bearings accounted for the largest revenue of the total Bearing Market share in 2024.

- Ball bearings are further divided into deep groove bearings and others.

- Deep groove bearings are widely used due to their versatility and ability to handle radial and axial loads, making them suitable for applications in automotive, industrial machinery, and aerospace sectors.

- Their high efficiency, reduced friction, and low maintenance make them indispensable across industries aiming for operational optimization.

- The increasing Bearing Market demand for electric vehicles and precision machinery has further boosted the adoption of ball bearings.

- Consequently, ball bearings dominate the market due to their extensive application and functional advantages.

- Therefore, according to the Bearing Market analysis, wide-ranging applications of ball bearings in automotive, industrial, and aerospace sectors significantly contribute to their dominance and current trends.

Roller Bearings is anticipated to register the fastest CAGR during the forecast period.

- Roller bearings are segmented into split, tapered, and others.

- Tapered roller bearings exhibit superior load-handling capabilities, particularly in applications involving heavy radial and axial forces.

- These bearings are prominently used in the mining, construction, and agricultural sectors, where durability and precision are critical.

- Additionally, advancements in manufacturing technologies and increasing use in renewable energy sectors, such as wind turbines, propel their growth.

- Thus, according to market analysis, the rising adoption of roller bearings in high-demand applications like mining and renewable energy drives their accelerated growth.

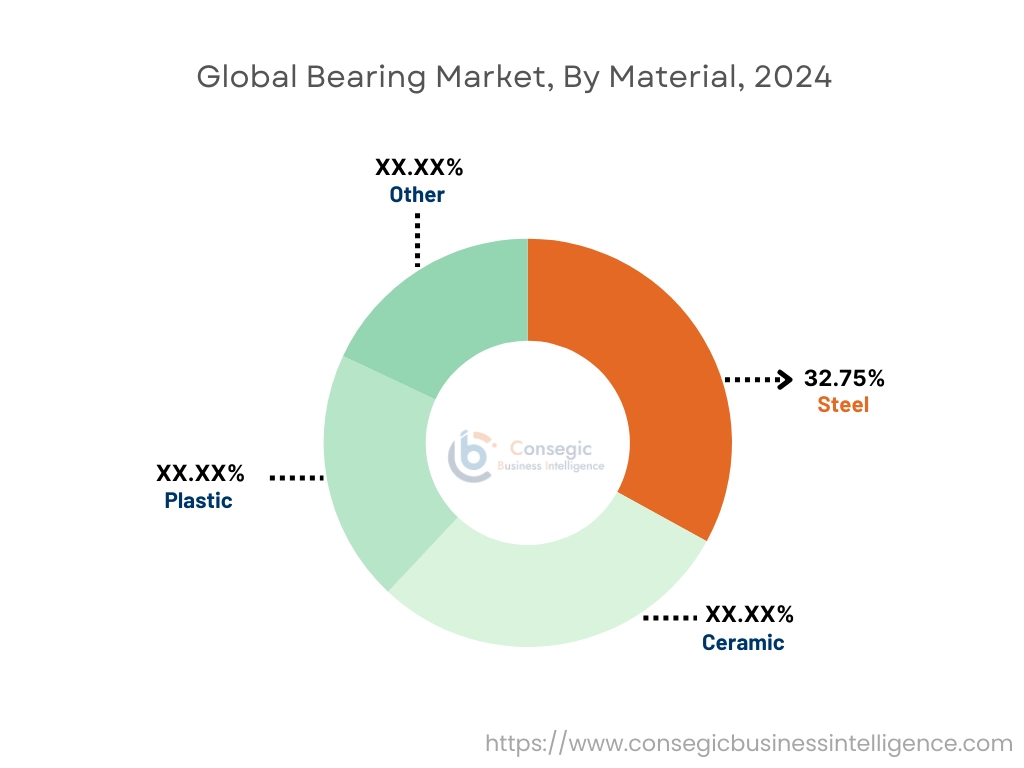

By Material:

Based on material, the market is segmented into steel, ceramic, plastic, and others.

Steel Bearings accounted for the largest revenue share of 32.75% in 2024.

- Steel bearings are preferred for their durability, strength, and resistance to wear and tear.

- They are widely used across heavy industries such as automotive, industrial machinery, and construction due to their ability to endure high loads and harsh environments.

- Continuous innovations in heat treatments and coatings further enhance the longevity and efficiency of steel bearings, maintaining their market leadership.

- Therefore, according to Bearing Market analysis, steel bearings' unparalleled strength and adaptability across heavy-load applications ensure their dominance in the market.

Ceramic Bearings is anticipated to register the fastest CAGR during the forecast period.

- Ceramic bearings are lightweight, corrosion-resistant, and capable of operating at high speeds with minimal lubrication.

- These features make them ideal for aerospace, high-speed machinery, and medical applications.

- Growing Bearing Market demand for lightweight and energy-efficient components further accelerates their adoption.

- Thus, according to market analysis, the rising preference for lightweight and high-performance components positions ceramic bearings for rapid growth.

By Sales Channel:

Based on sales channel, the market is segmented into original equipment manufacturers (OEMs) and aftermarket.

OEMs accounted for the largest revenue of the total Bearing Market Share in 2024.

- OEMs are the primary source of high-quality bearings, ensuring compatibility and reliability in original machinery and equipment.

- Partnerships with manufacturers across automotive, aerospace, and industrial sectors strengthen this segment's position.

- Therefore, according to market analysis, OEMs’ ability to provide high-quality and reliable products tailored to specific industry needs ensures their leadership in the market.

Aftermarket segment is anticipated to register the fastest CAGR during the forecast period.

- The aftermarket provides replacement bearings and services for machinery maintenance and repair.

- The increasing operational lifespan of machinery and equipment, coupled with advancements in predictive maintenance, supports the growth of this segment.

- The aftermarket's cost-effectiveness and accessibility further enhance its appeal to industries requiring regular servicing.

- Thus, according to market analysis, the aftermarket’s focus on maintenance and cost-efficiency drives its accelerated growth trajectory.

By End-User Industry:

Based on end-user industry, the market is segmented into automotive, aerospace, industrial machinery, construction, mining, agriculture, and others.

The automotive industry accounted for the largest revenue share in 2024.

- Bearings are integral to automotive systems, including engines, transmissions, and wheel assemblies.

- The increasing production of vehicles, coupled with the transition toward electric vehicles, fuels demand for high-quality, durable bearings.

- Bearings designed for energy efficiency and minimal friction are crucial for enhancing vehicle performance.

- Therefore, according to market analysis, the automotive industry's reliance on bearings for critical systems ensures its market trend.

The aerospace industry is anticipated to register the fastest CAGR during the forecast period.

- Bearings used in aerospace are designed to withstand extreme temperatures, pressures, and forces.

- The Bearing Market expansion is driven by growing air travel and defense investments, contributes to the rising demand for advanced bearing solutions.

- Lightweight and high-precision bearings enhance performance and fuel efficiency in modern aircraft.

- Thus, according to market analysis, the aerospace industry's need for high-performance and lightweight solutions drives the rapid adoption of advanced bearings, leading to an improved trend.

Regional Analysis:

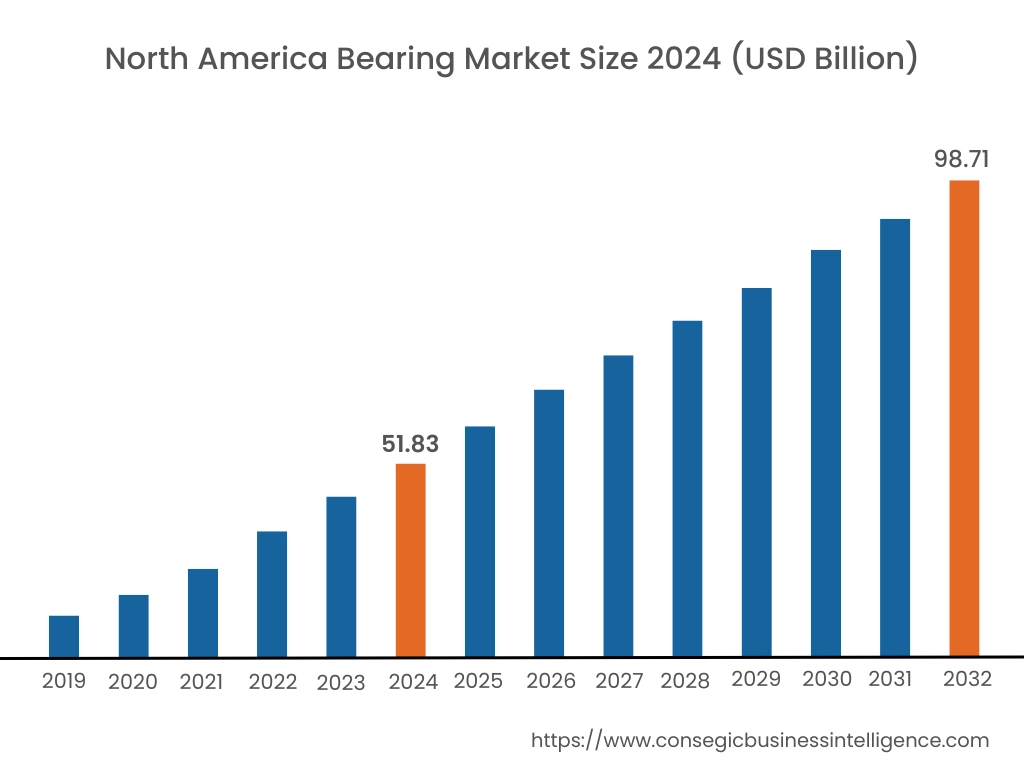

In 2024, North America was valued at USD 51.83 Billion and is expected to reach USD 98.71 Billion in 2032. In North America, the U.S. accounted for the highest share of 72.50% during the base year of 2024. The Bearing Industry in North America benefits from advancements in industrial machinery and rising demand from the automotive and aerospace sectors. The United States leads with investments in precision engineering and automation. Strong manufacturing activity and the adoption of technologically advanced bearing solutions support market performance across industries.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 9.2% over the forecast period. In Asia-Pacific, the Bearing Industry is driven by rapid industrialization and the expansion of automotive production. Countries like China, India, and Japan dominate due to robust manufacturing capabilities and rising demand for heavy machinery. Infrastructure development and increasing use of industrial robots also influence market trends, particularly in construction and electronics.

Europe’s Bearing Market opportunities are characterized by a strong need for sustainability and high-performance solutions. Countries like Germany, France, and Italy show significant demand from automotive and renewable energy industries. Emphasis on reducing friction and energy consumption in industrial applications enhances Bearing Market growth in this region. Strict environmental regulations influence product development strategies.

The Bearing Market in the Middle East and Africa is shaped by the expansion of the oil and gas, mining, and construction industries. Countries like Saudi Arabia and the UAE invest in advanced machinery requiring durable and efficient bearing solutions. Limited local manufacturing capacities create opportunities for imports, while infrastructure projects stimulate demand.

In Latin America, the Bearing Market experiences steady demand from agriculture, automotive, and industrial sectors. Brazil and Mexico show increased adoption of bearing technologies to improve machinery efficiency. Challenges such as economic instability and limited access to high-quality products impact market penetration in some areas. Regional manufacturers focus on affordable solutions.

Top Key Players & Market Share Insights:

The global bearing market is highly competitive with major players providing FWA to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Bearing Market. Key players in the Bearing Market industry include-

- SKF Group (Sweden)

- Schaeffler AG (Germany)

- MinebeaMitsumi Inc. (Japan)

- C&U Group (China)

- Nachi-Fujikoshi Corp. (Japan)

- NSK Ltd. (Japan)

- NTN Corporation (Japan)

- Timken Company (United States)

- JTEKT Corporation (Japan)

- RBC Bearings Incorporated (United States)

Recent Industry Developments :

Product launches:

- In October 2024, SKF has launched DuraPro, an advanced wind turbine gearbox bearings using thermo-chemical heat treatment. These bearings feature improved surface hardness, microstructure, and compressive stresses, offering up to 5x longer life, downsized components, and reduced maintenance costs.

Partnerships & Collaborations:

- In July 2024, SKF has partnered with Duracar to advance sustainable electric vehicle technology by supplying precision-engineered bearings and components, enhancing efficiency and reducing the carbon footprint of Duracar's electric vehicles.

Mergers and Acquisitions:

- In February 2024, Timken acquired American Roller Bearing Company (ARB), a North Carolina-based manufacturer, to expand its portfolio. ARB generated over $30 billion in 2022 sales, enhancing Timken's U.S. customer base and aftermarket services.

Bearing Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 304.56 Billion |

| CAGR (2025-2032) | 8.7% |

| By Product Type |

|

| By Material |

|

| By Sales Channel |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Bearing Market? +

In 2024, the Bearing Market was USD 156.26 billion.

What will be the potential market valuation for the Bearing Market by 2031? +

In 2031, the market size of Bearing Market is expected to reach USD 304.56 billion.

What are the segments covered in the Bearing Market report? +

The product types, materials, sales channels and end-user industry are the segments covered in this report.

Who are the major players in the Bearing Market? +

SKF Group (Sweden), Schaeffler AG (Germany), NSK Ltd. (Japan), NTN Corporation (Japan), Timken Company (United States), JTEKT Corporation (Japan), RBC Bearings Incorporated (United States), MinebeaMitsumi Inc. (Japan), C&U Group (China), Nachi-Fujikoshi Corp. (Japan) are the major players in the Bearing market.