- Summary

- Table Of Content

- Methodology

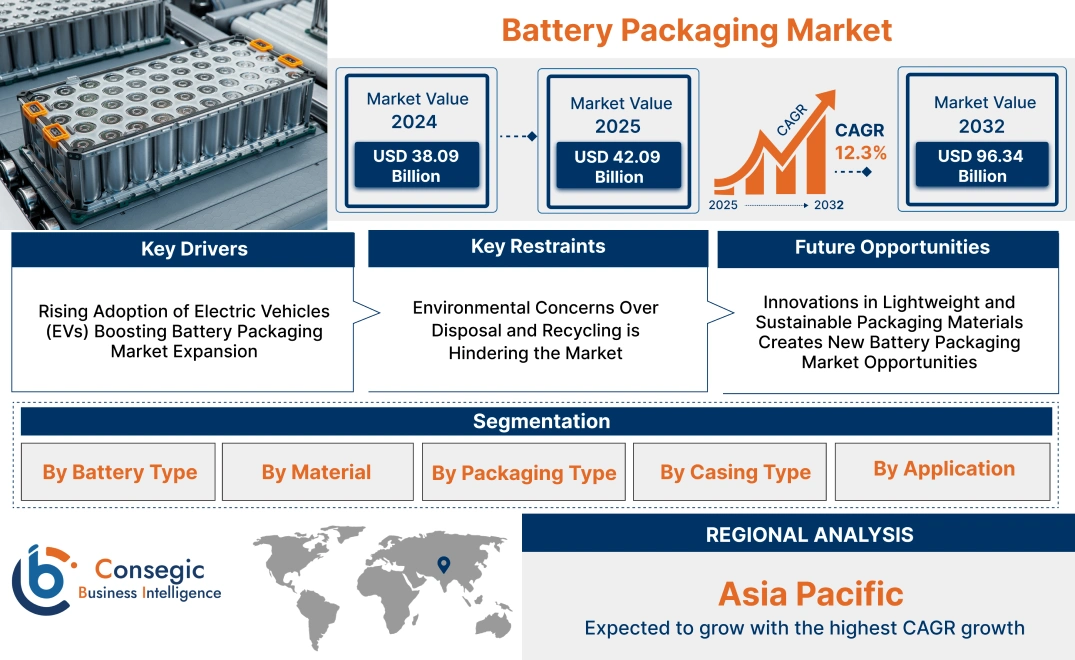

Battery Packaging Market Size:

Battery Packaging Market size is estimated to reach over USD 96.34 Billion by 2032 from a value of USD 38.09 Billion in 2024 and is projected to grow by USD 42.09 Billion in 2025, growing at a CAGR of 12.3% from 2025 to 2032.

Battery Packaging Market Scope & Overview:

The battery packaging focuses on the development and supply of protective packaging solutions tailored for batteries used across various industries, including automotive, electronics, and energy storage. These packaging solutions are designed to ensure the safe transportation, storage, and handling of batteries, minimizing risks associated with thermal runaway, mechanical damage, and chemical leaks. Key characteristics of the market include high durability, lightweight construction, thermal insulation, and compliance with safety regulations. The benefits include enhanced safety, improved logistics efficiency, and extended battery lifespan. Applications span packaging for lithium-ion, nickel-metal hydride (NiMH), lead-acid, and solid-state batteries. End-users include electric vehicle manufacturers, consumer electronics companies, and renewable energy firms, driven by the rapid adoption of electric vehicles, advancements in battery technologies, and increasing global emphasis on sustainable energy storage solutions.

Battery Packaging Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of Electric Vehicles (EVs) Boosting Battery Packaging Market Expansion

EV batteries require robust, thermally stable, and lightweight packaging solutions to ensure safety, performance, and longevity. The transition from traditional internal combustion engine vehicles to EVs has created a heightened need for advanced packaging that supports high energy densities and ensures protection against thermal runaway, vibration, and mechanical shocks.

Battery packaging in EVs not only safeguards the cells but also facilitates efficient heat dissipation, crucial for maintaining optimal battery performance. Trends in EV innovation, including the development of ultra-fast charging batteries and solid-state technologies, have further emphasized the importance of advanced packaging solutions. With governments promoting EV adoption through subsidies and infrastructure development, the analysis suggests that the growth for high-performance battery packaging tailored to automotive applications will continue to rise.

Key Restraints:

Environmental Concerns Over Disposal and Recycling is Hindering the Market

The disposal and recycling of battery packaging materials present significant environmental challenges. Most packaging relies on plastics, metals, and other non-biodegradable materials, which contribute to waste accumulation and environmental degradation. Improper disposal of these materials often leads to soil and water contamination, particularly in regions lacking efficient waste management systems.

Additionally, the complexity of recycling battery packaging due to the presence of adhesives, coatings, and composite materials poses technical and economic hurdles. These environmental concerns are prompting stricter regulations and encouraging industries to explore sustainable alternatives. Addressing these challenges through the adoption of recyclable materials and circular economy principles is crucial for mitigating the environmental impact of packaging, aligning with broader sustainability goals.

Future Opportunities :

Innovations in Lightweight and Sustainable Packaging Materials Creates New Battery Packaging Market Opportunities

Manufacturers are increasingly focusing on bio-based polymers, recyclable composites, and renewable fibers to reduce the environmental footprint of packaging while maintaining performance standards. These materials not only contribute to weight reduction, which is critical for applications such as electric vehicles, but also align with global trends toward eco-friendly practices.

Sustainable battery packaging solutions are particularly valuable in sectors where compliance with stringent environmental regulations is a priority. For instance, the use of recyclable and biodegradable materials addresses waste management concerns while supporting the broader adoption of green technologies. Analysis highlights that as industries prioritize sustainability and efficiency, the integration of advanced lightweight materials will transform the battery packaging landscape, offering a balance between functionality and environmental responsibility.

Battery Packaging Market Segmental Analysis :

By Battery Type:

Based on battery type, the market is segmented into lithium-ion batteries, lead-acid batteries, nickel-metal hydride batteries, nickel-cadmium batteries, and others.

The lithium-ion batteries segment accounted for the largest revenue in battery packaging market share in 2024.

- Lithium-ion batteries dominate the market due to their widespread use in automotive, consumer electronics, and energy storage systems.

- Their high energy density, long cycle life, and lightweight properties make them the preferred choice for electric vehicles (EVs) and portable electronic devices.

- The aim of transitioning to clean energy solutions and the increasing adoption of EVs drive battery packaging market growth for lithium-ion battery packaging solutions, ensuring safety and thermal stability during transportation and usage.

- Lithium-ion batteries lead the market, supported by their extensive use in EVs and energy storage, along with the growing battery packaging market trends of clean energy adoption.

The nickel-metal hydride batteries segment is anticipated to register the fastest CAGR during the forecast period.

- Nickel-metal hydride batteries are gaining traction in hybrid electric vehicles (HEVs) and medical equipment due to their reliability and environmental friendliness compared to nickel-cadmium batteries.

- The rising aim of adopting sustainable battery technologies in niche applications has propelled the growth for innovative packaging solutions to enhance battery performance and longevity.

- Nickel-metal hydride batteries analysis depicts it is expected to grow rapidly, driven by their increasing adoption in HEVs and environmentally conscious applications.

By Material:

Based on material, the market is segmented into cardboard, metal, plastic, and others.

The plastic segment accounted for the largest revenue share in 2024.

- Plastic materials are extensively utilized in battery packaging due to their lightweight nature, durability, and cost-effectiveness. Their versatility enables customization for a wide range of battery types and sizes, ensuring protection against moisture, temperature fluctuations, and mechanical shocks.

- The increasing battery packaging market opportunities in adopting plastic packaging solutions tailored to specific battery applications, such as EV batteries and consumer electronics, supports its dominance.

- Advancements in bio-based and recyclable plastics align with the growing emphasis on sustainable packaging practices, reducing environmental impact while maintaining performance.

- The plastic segment dominates the market, driven by its adaptability, cost-effectiveness, and alignment with sustainability goals in various battery applications.

The metal segment is anticipated to register the fastest CAGR during the forecast period.

- Metal packaging is a preferred choice for high-performance batteries used in industrial and automotive applications, offering superior strength, durability, and thermal resistance. Its ability to withstand harsh conditions during transportation and usage enhances its reliability.

- The trends of adopting robust metal casings for EV and energy storage system batteries to ensure safety and prevent leaks or damage further drives this segment.

- Innovations in lightweight metal alloys and corrosion-resistant coatings have expanded the use of metal packaging in diverse applications, including aerospace and defense.

- The metal segment is expected to grow rapidly, supported by its unmatched strength, safety features, and suitability for high-performance batteries in demanding environments.

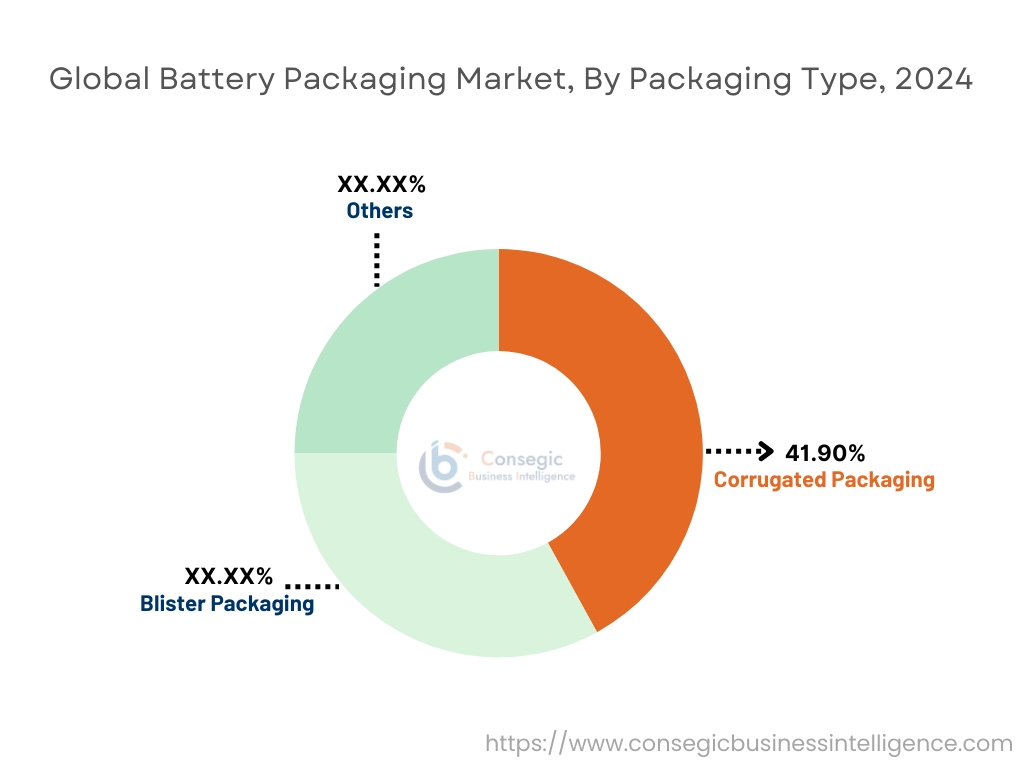

By Packaging Type:

Based on packaging type, the market is segmented into corrugated packaging, blister packaging, and others.

The corrugated packaging segment accounted for the largest revenue share of 41.90% in 2024.

- Corrugated packaging is widely adopted for its durability, lightweight properties, and cost-effectiveness, making it essential for transporting and storing large batteries, especially for EVs and energy storage systems.

- The increasing dominance in adopting recyclable corrugated materials aligns with sustainability goals, ensuring eco-friendly battery transport solutions.

- Its ability to protect batteries from mechanical damage and environmental factors during transportation further supports its widespread usage.

- The rise in battery packaging market growth for high-performance batteries in automotive and industrial applications drives the need for robust corrugated packaging solutions.

- Corrugated packaging leads the market, driven by its strength, lightweight nature, cost-efficiency, and compatibility with environmentally sustainable practices.

The blister packaging segment is anticipated to register the fastest CAGR during the forecast period.

- Blister packaging is increasingly used for small batteries in consumer electronics due to its ability to provide clear visibility of the product, enhance branding, and ensure tamper resistance.

- The trends of adopting compact and attractive packaging for retail battery products aligns with growing consumer preferences for convenience and visual appeal.

- Blister packaging also offers high product protection, ensuring safety during transportation and storage while maintaining battery integrity.

- The rise of portable electronic devices and small battery-powered gadgets further boosts demand for blister packaging in retail and consumer segments.

- Blister packaging is expected to grow rapidly, supported by its retail-friendly design, tamper resistance, and suitability for compact electronic batteries.

By Casing Type:

Based on casing type, the market is segmented into cylindrical, prismatic, and pouch.

The cylindrical segment accounted for the largest revenue in battery packaging market share in 2024.

- Cylindrical casings are widely adopted in lithium-ion batteries due to their superior structural strength, ease of manufacturing, and ability to handle high currents. These casings are a preferred choice in applications requiring robust and reliable energy storage solutions, such as power tools, medical devices, and electric vehicles (EVs).

- The trends of adopting cylindrical batteries for their enhanced thermal stability and safety features has further solidified their dominance in the market. The uniform shape and standardization of cylindrical batteries also contribute to simplified production processes, making them cost-effective and widely accessible for manufacturers.

- In the automotive sector, cylindrical casings are extensively used in EV battery packs, particularly in high-performance electric cars. Their ability to handle repeated charge-discharge cycles without significant degradation aligns with the growing battery packaging market demand for durable and efficient batteries.

- The cylindrical casing type leads the market, supported by its structural reliability, cost-effectiveness, and extensive application in EVs, power tools, and industrial devices.

The pouch segment is anticipated to register the fastest CAGR during the forecast period.

- Pouch casings are rapidly gaining traction in consumer electronics and electric vehicles due to their lightweight and flexible design. These casings offer higher energy density compared to cylindrical and prismatic counterparts, making them ideal for compact and space-constrained applications.

- The trends of developing thinner, lighter, and more efficient battery designs to meet consumer demand for portable electronics and electric vehicles has driven the adoption of pouch casings. Their flexible structure allows for customized battery shapes, which optimize space utilization in applications such as smartphones, laptops, and electric vehicles.

- In the EV sector, pouch casings are particularly advantageous for designing modular battery packs that enhance energy efficiency and improve vehicle range. Their lightweight nature contributes to overall vehicle weight reduction, which aligns with the industry's goals of improving energy efficiency and reducing carbon emissions.

- The pouch casing type is expected to grow rapidly, driven by its lightweight, flexible design, and suitability for compact, energy-dense applications in consumer electronics, EVs, and renewable energy systems.

By Application:

Based on application, the market is segmented into automotive, consumer electronics, energy storage systems, industrial, and others.

The automotive segment accounted for the largest revenue share in 2024.

- The automotive industry is the largest consumer of battery packaging, driven by the increasing production of electric vehicles (EVs) and hybrid electric vehicles (HEVs). As governments worldwide implement stricter emission regulations and promote clean energy vehicles, the demand for advanced packaging solutions is growing exponentially.

- The trends of transitioning to sustainable mobility solutions and the growing investment in EV battery technologies boost surge for packaging systems that ensure safety, thermal management, and compliance with regulatory standards.

- The adoption of modular battery packs in EVs, which require innovative packaging designs to optimize energy density and facilitate maintenance, further supports advancement in this segment.

- The automotive segment dominates the market, supported by the rising production of EVs, advancements in battery technologies, and the push toward sustainable transportation and circular economy practices.

The energy storage systems segment is anticipated to register the fastest CAGR during the forecast period.

- The increasing adoption of renewable energy sources such as solar and wind has driven development for energy storage systems, which rely heavily on advanced battery technologies to store energy efficiently and maintain grid stability.

- The trends of integrating energy storage solutions into residential, commercial, and grid-level applications supports the need for efficient battery packaging systems to enhance durability, thermal management, and safety.

- The growing focus on deploying utility-scale energy storage projects to address intermittent energy supply challenges has further propelled requirement for robust and scalable battery packaging solutions.

- The energy storage systems segment is expected to grow rapidly, driven by the rising advancement for renewable energy integration, utility-scale storage solutions, and advancements in energy storage technologies.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

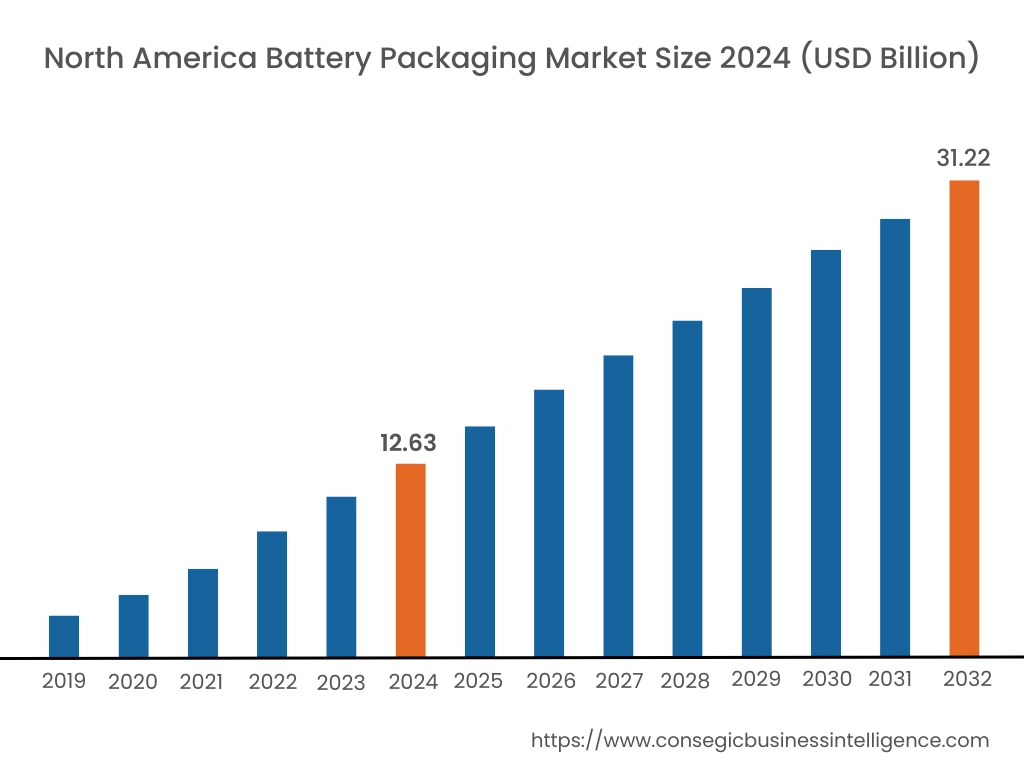

In 2024, North America was valued at USD 12.63 Billion and is expected to reach USD 31.22 Billion in 2032. In North America, the U.S. accounted for the highest share of 73.10% during the base year of 2024. North America holds a significant stake in the battery packaging market analysis, driven by the growing adoption of electric vehicles (EVs) and renewable energy storage systems. The U.S. leads the region, with strong need for advanced battery packaging solutions from EV manufacturers and energy storage system providers. The region also benefits from increasing investments in lithium-ion battery production facilities, which require durable and efficient packaging solutions to ensure safety and performance. Canada contributes with its focus on renewable energy projects and battery manufacturing for both EVs and grid storage. However, challenges such as high material costs and stringent regulatory requirements for safe battery packaging can impact market dynamics.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 12.8% over the forecast period. Asia-Pacific is the largest and fastest-growing region in the market, driven by the analysis of rapid industrialization and the expansion of EV and consumer electronics manufacturing in China, Japan, and South Korea. China leads the market with its large-scale production of batteries for EVs and energy storage, fueling growth for innovative packaging solutions to ensure safe handling and transportation. Japan and South Korea focus on advanced packaging technologies for high-performance lithium-ion batteries used in electronics and EVs. India is also witnessing increasing opportunities in the adoption of battery packaging due to its growing EV market and renewable energy initiatives. However, challenges such as cost pressures and environmental concerns over packaging waste persist in the region.

Europe hold a prominent share of the market, supported by the region’s strong emphasis on sustainability and decarbonization. The Battery Packaging Market analysis shows that countries like Germany, France, and the UK are major contributors. Germany, as a leading hub for EV manufacturing, drives the battery packaging market demand for robust packaging solutions to enhance battery safety and efficiency. France focuses on advanced packaging technologies for renewable energy storage batteries, while the UK is investing in next-generation packaging for EVs and portable electronics. The region’s regulatory framework on safe and recyclable packaging materials further boosts innovation in the market. However, challenges related to raw material availability and compliance with EU packaging standards may impact manufacturers.

The Middle East & Africa region is witnessing steady growth in the market, primarily driven by increasing investments in renewable energy storage and the adoption of energy-efficient technologies. Countries like Saudi Arabia and the UAE are investing in grid storage solutions and electric mobility, requiring robust packaging for safety and durability. In Africa, South Africa is a key market, leveraging battery packaging for off-grid renewable energy projects and industrial applications. However, limited local manufacturing capabilities and reliance on imports for advanced packaging materials constrains battery packaging market expansion in the region.

Latin America is an emerging market for battery packaging, with Brazil and Mexico leading the region. Brazil’s focus on renewable energy projects and the growing adoption of EVs are driving the need for efficient packaging solutions. Mexico’s expanding automotive manufacturing sector, including EV production, boosts the market for durable and lightweight packaging materials. The region is also exploring innovations in recyclable and eco-friendly packaging to align with global sustainability battery packaging market trends. However, economic instability and limited infrastructure for large-scale battery production may pose challenges for market progress.

Top Key Players & Market Share Insights:

The Battery Packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Battery Packaging market. Key players in the Battery Packaging industry include -

- Nefab Group (Sweden)

- United Parcel Service (UPS) (United States)

- DS Smith (United Kingdom)

- Smurfit Kappa Group (Ireland)

- Umicore (Belgium)

- DHL (Germany)

- Zarges (Germany)

- Heitkamp & Thumann Group (Germany)

- FedEx (United States)

- Rogers Corporation (United States)

Battery Packaging Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 96.34 Billion |

| CAGR (2025-2032) | 12.3% |

| By Battery Type |

|

| By Material |

|

| By Packaging Type |

|

| By Casing Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Battery Packaging Market by 2032? +

Battery Packaging Market size is estimated to reach over USD 96.34 Billion by 2032 from a value of USD 38.09 Billion in 2024 and is projected to grow by USD 42.09 Billion in 2025, growing at a CAGR of 12.3% from 2025 to 2032.

Which battery type dominates the Battery Packaging Market? +

The lithium-ion battery segment holds the largest market share in 2024 due to its widespread use in electric vehicles, consumer electronics, and energy storage systems.

Which material type is most commonly used in battery packaging? +

Plastic is the most commonly used material due to its lightweight nature, durability, cost-effectiveness, and adaptability to various battery applications.

Which region is expected to witness the fastest growth in the Battery Packaging Market? +

Asia Pacific is expected to experience the fastest growth, driven by rapid industrialization, expansion of EV manufacturing, and increasing adoption of energy storage systems in countries like China, Japan, and South Korea.