- Summary

- Table Of Content

- Methodology

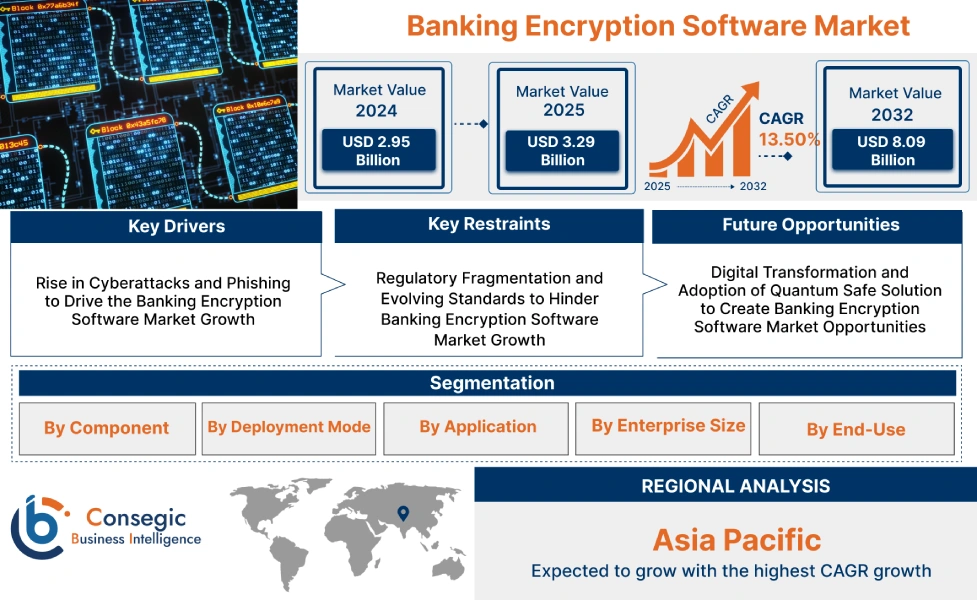

Banking Encryption Software Market Size:

Banking Encryption Software Market size is estimated to reach over USD 8.09 Billion by 2032 from a value of USD 2.95 Billion in 2024 and is projected to grow by USD 3.29 Billion in 2025, growing at a CAGR of 13.50 % from 2025 to 2032.

Banking Encryption Software Market Scope & Overview:

Banking encryption software refers to specialized solutions designed to secure sensitive financial data by converting it into encrypted formats that are accessed with authorized decryption keys. These solutions are integral to safeguarding data during storage and transmission, protecting banking operations, and ensuring compliance with stringent regulatory standards. They are widely used to secure transactions, protect customer information, and safeguard internal communications.

The software integrates advanced encryption algorithms, multi-layered security protocols, and real-time monitoring capabilities to provide robust protection against data breaches and cyber threats. It is tailored for applications such as securing online banking platforms, mobile banking apps, payment gateways, and internal databases. These solutions are scalable and are customized to meet the specific needs of financial institutions, ensuring both operational security and seamless user experiences.

End-users of this software include banks, credit unions, financial service providers, and fintech companies that rely on encryption to protect sensitive data, maintain customer trust, and ensure the integrity of their operations across digital platforms.

Banking Encryption Software MarketDynamics - (DRO) :

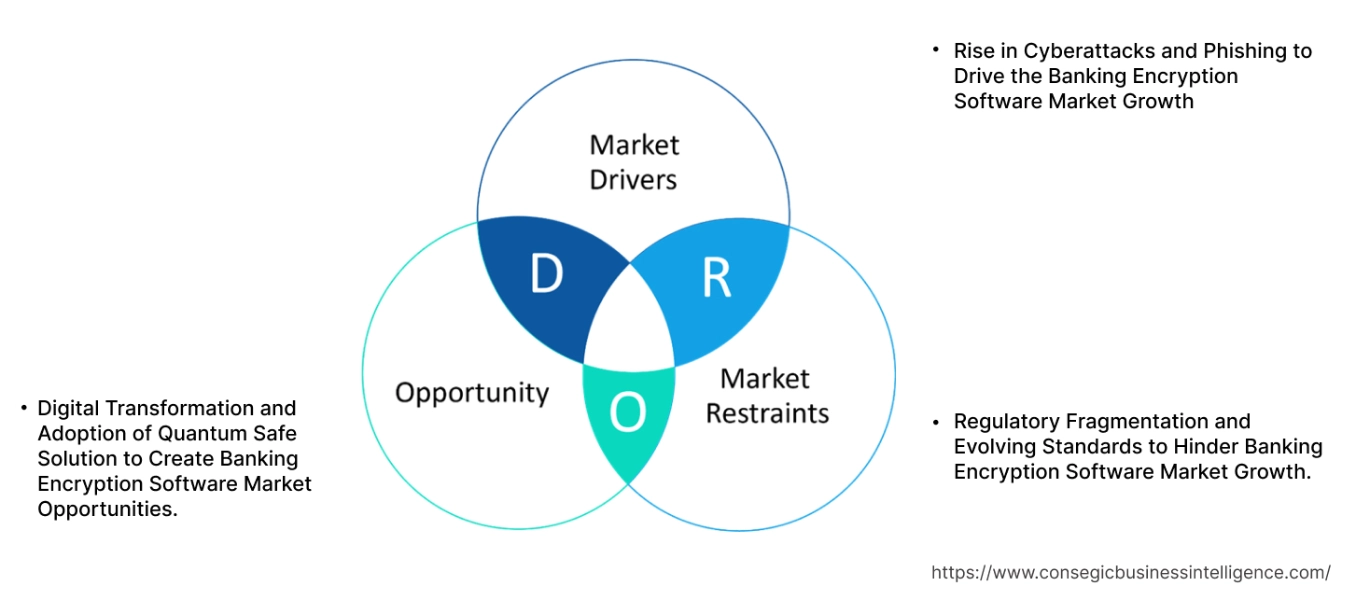

Key Drivers:

Rising Phishing Attacks in the Banking Sector Fuel the Market Development

The increasing frequency and sophistication of phishing attacks are driving the demand for robust encryption solutions in the banking sector. Phishing attacks, which deceive individuals into revealing sensitive information such as login credentials and financial details, pose significant risks to both customers and financial institutions. These attacks often exploit vulnerabilities in digital communication channels, including emails, SMS, and fake websites, leading to unauthorized access to accounts and financial fraud. To counter these threats, banks are adopting advanced encryption software to secure data transmission, authenticate user identities, and safeguard sensitive information.

End-to-end encryption and multi-factor authentication ensure that even if phishing attempts occur, critical data remains inaccessible to unauthorized entities. Additionally, regulatory bodies are imposing stricter compliance measures, requiring banks to enhance their security frameworks to protect customers from phishing attacks. The growing threat of phishing, coupled with rising consumer awareness about data security, is accelerating the adoption of encryption technologies to maintain trust, ensure compliance, and mitigate financial losses in the banking sector, driving banking encryption software market growth.

Key Restraints :

Performance Trade-Offs in High-Volume Transactions Hinders Market Progress

The implementation of encryption software in banking operations often creates performance issues, especially during high-volume transactions. Real-time encryption and decryption processes significantly increase the computational workload, as each transaction requires secure encoding and decoding of sensitive data. This additional processing load results in slower transaction times, bottlenecks in payment systems, and delays in services like fund transfers and account updates, particularly during peak operational hours. Such performance trade-offs adversely impact customer satisfaction, as users expect seamless and instantaneous banking experiences in digital and mobile platforms.

The issue is amplified for banks handling large-scale operations or international transactions, where speed and reliability are critical. Financial institutions often face difficulties in balancing robust data security measures with the demand for high-performance systems. Addressing these trade-offs requires advanced hardware solutions, such as hardware security modules (HSMs), and optimized encryption protocols, which increase implementation costs. For smaller banks with limited resources, these constraints make it harder to adopt advanced encryption systems, hindering their ability to maintain competitive and secure banking operations, thereby restraining banking encryption software market demand.

Future Opportunities :

Rising Adoption of Cloud-Based Encryption Solutions Opens New Doors

The shift toward cloud computing in the banking sector is creating significant growth opportunities for cloud-based encryption solutions. As banks increasingly adopt hybrid and multi-cloud environments to enhance flexibility, scalability, and cost-efficiency, the demand for robust encryption technologies to secure sensitive data becomes paramount. Cloud-based encryption provides end-to-end data protection, ensuring the confidentiality of information during storage and transfer across distributed systems.

One of the key advantages of cloud encryption is its ability to centralize key management, allowing banks to maintain control over encryption keys while meeting stringent regulatory requirements for data protection. This capability is critical in ensuring compliance with global standards such as GDPR, PCI DSS, and ISO 27001. Moreover, cloud encryption enables real-time threat detection and response, enhancing the security of dynamic and high-volume transactions. The ease of deployment, scalability, and cost-effectiveness of cloud-based encryption make it particularly attractive for banks looking to transition to digital-first strategies. As the banking sector continues its digital transformation, cloud-based encryption is expected to play a pivotal role in securing sensitive financial data and fostering trust among customers, creating banking encryption software market opportunities.

Banking Encryption Software Market Segmental Analysis :

By Component:

Based on component, the market is segmented into Software (Encryption Tools, Key Management Systems) and Services (Consulting, Integration & Deployment, and Support & Maintenance).

The software segment accounted for the largest revenue of the total banking encryption software market share in 2024.

- Encryption tools, such as advanced cryptographic algorithms, are widely deployed to safeguard sensitive customer data and financial transactions.

- Key management systems ensure the secure creation, distribution, and storage of encryption keys, mitigating risks associated with unauthorized data access.

- Financial institutions increasingly rely on software solutions to meet compliance requirements, such as GDPR and PCI DSS, enhancing data security measures.

- According to market trends, the dominance of the software segment reflects its critical role in automating encryption processes and streamlining security workflows, driving banking encryption software market expansion.

The services segment is expected to register the fastest CAGR during the forecast period.

- Consulting services assist banks in evaluating vulnerabilities and implementing customized encryption solutions tailored to their specific needs.

- Integration and deployment services simplify the adoption of encryption tools, ensuring compatibility with legacy systems and minimizing operational disruptions.

- Ongoing support and maintenance services ensure that encryption technologies remain up-to-date with evolving cyber threats and regulatory mandates.

- As per banking encryption software market analysis, the growing complexity of encryption systems is driving the demand for expert service providers to optimize implementation and performance.

By Deployment Mode :

Based on deployment mode, the market is segmented into on-premise, cloud-based, and hybrid.

The On-Premise segment held the largest revenue of the total banking encryption software market share in 2024.

- On-premise solutions offer complete control over encryption infrastructure, making them ideal for banks with stringent security requirements.

- These systems are widely preferred by large financial institutions that manage high volumes of sensitive data, ensuring compliance with internal governance policies.

- On-premise deployments support the use of proprietary encryption algorithms, providing enhanced customization and security for financial data.

- As per banking encryption software market trends, the segment’s dominance is supported by trends emphasizing data sovereignty and the need for robust, in-house security solutions.

The Cloud-Based segment is expected to register the fastest CAGR during the forecast period.

- Cloud-based encryption solutions provide scalability and flexibility, enabling banks to protect data stored in dynamic cloud environments.

- These systems integrate seamlessly with Software-as-a-Service (SaaS) platforms, offering cost-effective options for small and medium-sized banks.

- Innovations in cloud security, such as homomorphic encryption, are addressing concerns related to data confidentiality and breach risks.

- As per industry analysis, the adoption of cloud-based encryption reflects the growing reliance on cloud platforms for banking operations and data storage, driving banking encryption software market growth.

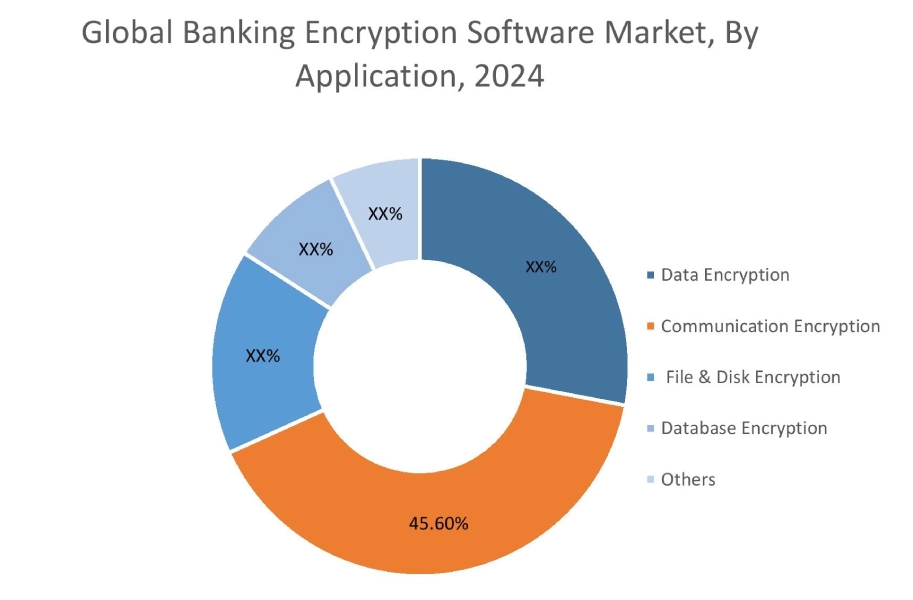

By Application:

Based on application, the market is segmented into Data Encryption, Communication Encryption, File & Disk Encryption, and Database Encryption.

The Data Encryption segment accounted for the largest revenue of 45.60% share in 2024.

- Data encryption solutions are critical for securing sensitive information during storage and transmission, preventing unauthorized access and data breaches.

- Financial institutions use advanced encryption standards (AES) to protect customer information, transaction records, and account details.

- Data encryption technologies are increasingly integrated with real-time monitoring systems, enhancing their capability to detect and mitigate cyber threats.

- The dominance of this segment is attributed to its fundamental role in ensuring data confidentiality and maintaining customer trust in banking operations, fueling banking encryption software market demand.

The Communication Encryption segment is expected to register the fastest CAGR during the forecast period.

- Communication encryption solutions protect data exchanged through email, chat applications, and voice communication channels, ensuring secure collaboration.

- Banks rely on secure messaging platforms and end-to-end encryption protocols to safeguard internal and external communications.

- The segment’s growth is fueled by trends in neobanking and digital collaboration, which require robust encryption technologies to maintain security and confidentiality.

- As per market analysis, the increasing frequency of phishing and interception attacks highlights the importance of communication encryption in the banking sector, driving banking encryption software market expansion.

By Enterprise Size :

Based on enterprise size, the market is segmented into Small & Medium Enterprises (SMEs) and Large Enterprises.

The Large Enterprises segment accounted for the largest revenue share in 2024.

- Large banks and financial institutions prioritize encryption solutions to protect extensive customer databases, transaction records, and critical financial assets.

- These organizations invest heavily in cutting-edge encryption technologies, such as quantum-safe encryption, to future-proof their security systems.

- As per industry analysis, the growing complexity of cyber threats targeting large enterprises underscores the need for advanced encryption tools and systems.

- The dominance of this segment reflects its focus on implementing robust data security measures to comply with global regulatory standards, creating banking encryption software market opportunities.

The Small & Medium Enterprises (SMEs) segment is expected to register the fastest CAGR during the forecast period.

- SMEs are adopting encryption software to secure customer information and financial transactions in response to increasing cybersecurity risks.

- Cloud-based encryption solutions are gaining popularity among SMEs due to their affordability, scalability, and ease of deployment.

- Government initiatives to promote cybersecurity awareness among smaller financial institutions are encouraging the adoption of encryption technologies.

- As per banking encryption software market trends, the rapid growth of this segment reflects its focus on enhancing data security while balancing cost-effectiveness and operational efficiency.

By End-User:

Based on end-user, the market is segmented into Retail Banking, Investment Banking, Commercial Banking, and Others.

The Retail Banking segment accounted for the largest revenue share in 2024.

- Retail banks deploy encryption solutions to secure customer data, online banking transactions, and mobile banking applications.

- The increasing adoption of digital wallets and contactless payment solutions highlights the critical role of encryption in protecting retail banking operations.

- Market trends indicate that retail banks are prioritizing encryption technologies to enhance customer trust and safeguard sensitive financial information.

- As per banking encryption software market analysis, the dominance of this segment is supported by its critical role in protecting large-scale transactions and ensuring secure banking experiences for individuals.

The Investment Banking segment is expected to register the fastest CAGR during the forecast period.

- Investment banks rely on encryption tools to secure high-value transactions, deal negotiations, and confidential client data.

- These banks adopt advanced key management systems to ensure secure communication and collaboration during mergers, acquisitions, and equity deals.

- The segment’s rapid growth is driven by trends emphasizing the need for advanced encryption in managing complex financial portfolios and high-value assets.

- As per segmental trends analysis, the increasing reliance on digital platforms for investment activities underscores the importance of encryption in mitigating financial risks.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

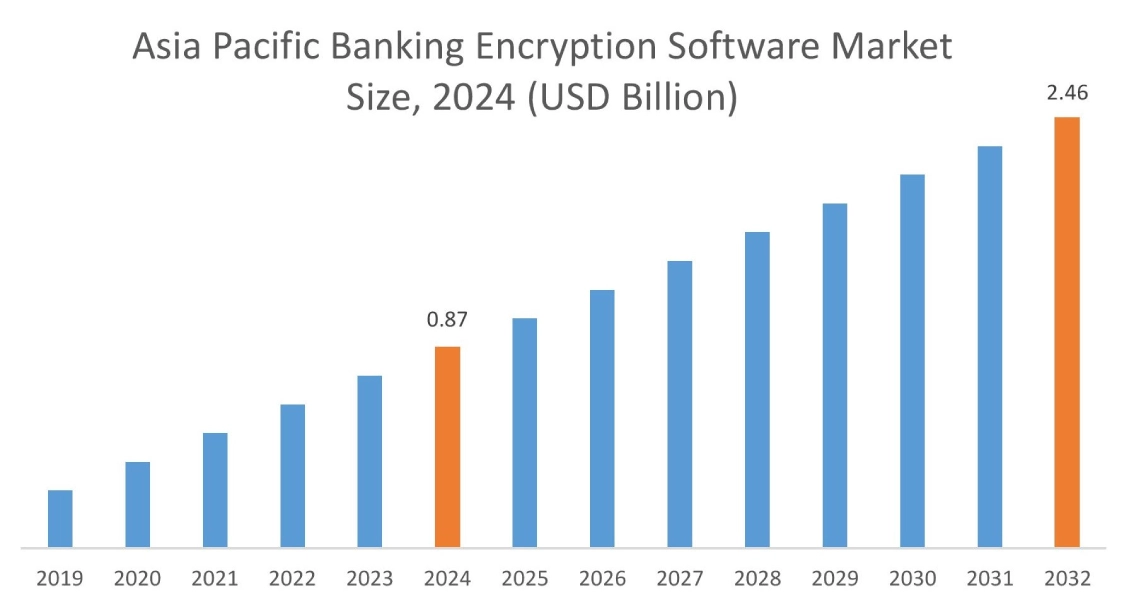

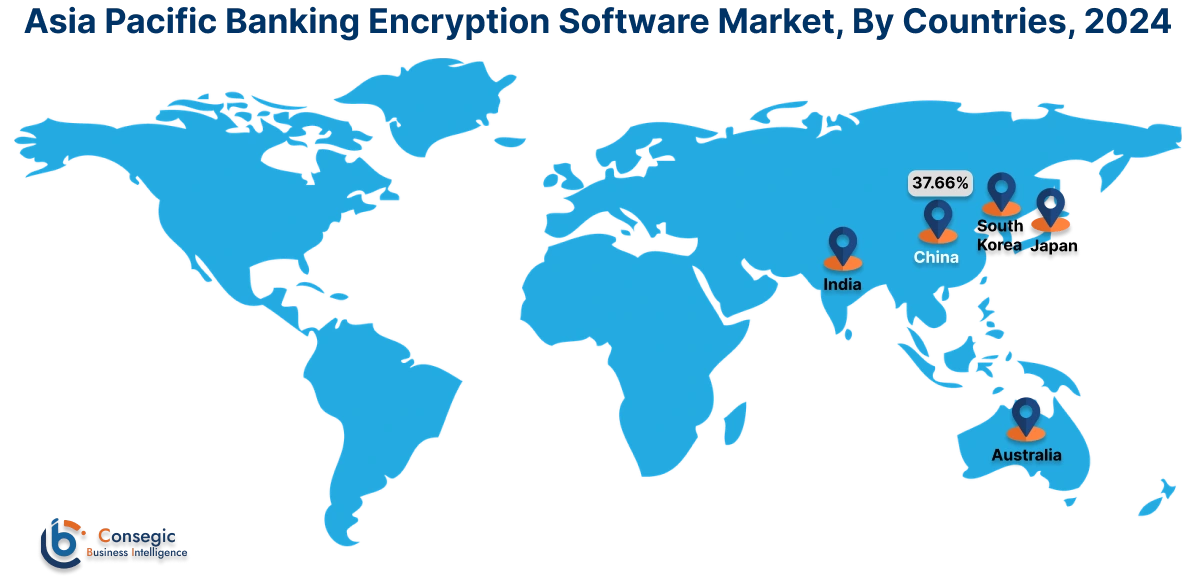

Asia Pacific region was valued at USD 0.87 Billion in 2024. Moreover, it is projected to grow by USD 0.97 Billion in 2025 and reach over USD 2.46 Billion by 2032. Out of these, China accounted for the largest share of 42.4% in 2024. Asia-Pacific is experiencing rapid growth in the banking encryption software market, driven by increasing digitalization in China, India, and Japan. The growing adoption of online banking platforms and mobile banking services has heightened the focus on encryption technologies to prevent cyber-attacks. Governments in the region are encouraging stronger cybersecurity frameworks, particularly in financial services, to build trust in digital platforms.

North America is estimated to reach over USD 2.62 Billion by 2032 from a value of USD 0.98 Billion in 2024 and is projected to grow by USD 1.09 Billion in 2025. North America leads the banking encryption software market due to stringent cybersecurity regulations, including CCPA in the U.S. and data protection laws in Canada. The region’s advanced digital banking ecosystem and high adoption of mobile and online banking services are driving the implementation of encryption software to secure transactions. Major financial institutions, in collaboration with technology providers, are investing heavily in solutions to combat the rising incidences of data breaches.

Europe is a prominent market for banking encryption software, primarily influenced by GDPR which mandates robust data protection measures. Countries such as Germany, the UK, and France are at the forefront, emphasizing the adoption of encryption tools to safeguard sensitive financial data. Additionally, the rapid shift to cashless transactions and contactless payments across the region has further strengthened the demand for encryption software.

The Middle East & Africa (MEA) region is rapidly expanding its use of encryption software, particularly in countries like Saudi Arabia, the UAE, and South Africa. The proliferation of digital banking services and the region’s push for financial sector modernization have underscored the importance of secure data management. Moreover, increasing cyber threats targeting banking systems have accelerated investments in encryption technologies.

Latin America is an emerging market for banking encryption software, with Brazil and Mexico leading adoption due to growing online banking activities and government initiatives promoting digital security. Financial institutions in these countries are focusing on improving encryption capabilities to comply with evolving data protection laws and prevent rising cyber frauds.

Top Key Players & Market Share Insights:

The Banking Encryption Software market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Banking Encryption Software market. Key players in the Banking Encryption Software industry include –

- IBM Corporation (USA)

- Microsoft Corporation (USA)

- Broadcom Inc. (USA)

- Thales Group (France)

- McAfee, LLC (USA)

- Intel Corporation (USA)

- Sophos Ltd. (UK)

- Trend Micro Incorporated (Japan)

- TaskUs (USA)

- ESET (Slovakia)

Recent Industry Developments :

- In July 2024, AxCrypt, a leading file encryption software company, emphasizes the importance of data security in the finance and banking sectors. With increasing cyber threats, encryption ensures compliance with regulations like GDPR and PCI-DSS, while protecting sensitive data during storage and transmission. The company highlights the role of end-to-end encryption in safeguarding confidential communications and preventing data breaches, supporting safer financial transactions.

- In September 2024, HDFC Bank emphasizes the critical role of encryption in online banking to safeguard sensitive customer data. It helps protect personal and financial details during online transactions, ensuring confidentiality and preventing unauthorized access. Encryption protocols are key in securing communication and protecting against cyber threats, thereby fostering trust and security in digital banking.

Banking Encryption Software Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 8.09 Billion |

| CAGR (2025-2032) | 13.5% |

| By Component |

|

| By Deployment Mode |

|

| By Application |

|

| By Enterprise Size |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|