- Summary

- Table Of Content

- Methodology

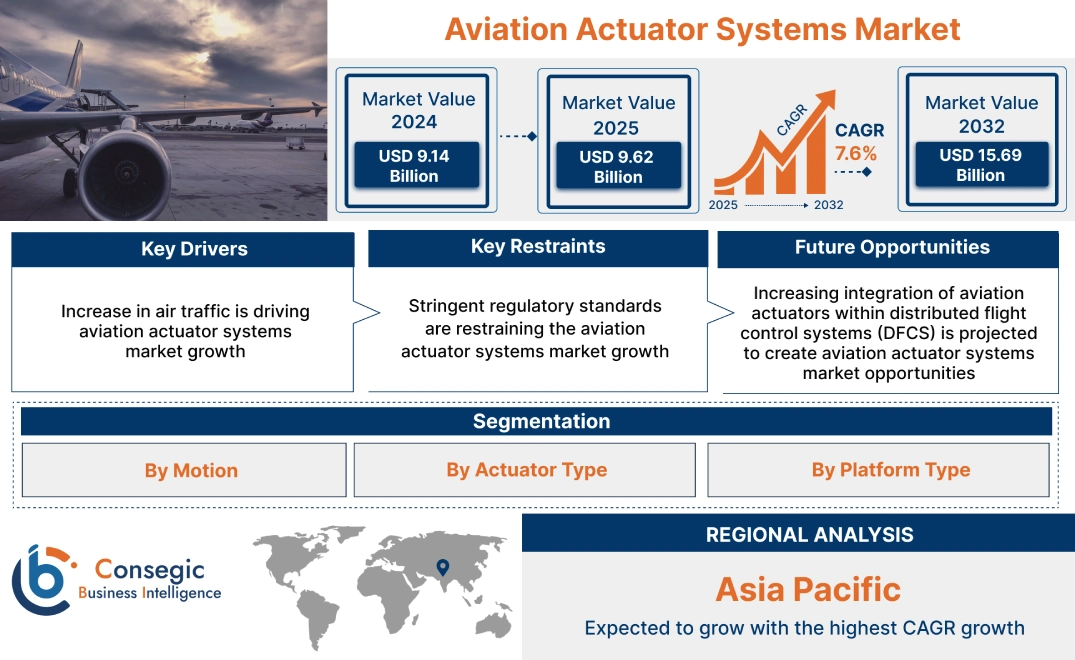

Aviation Actuator Systems Market Size:

Aviation Actuator Systems Market Size is estimated to reach over USD 15.69 Billion by 2032 from a value of USD 9.14 Billion in 2024 and is projected to grow by USD 9.62 Billion in 2025, growing at a CAGR of 7.6% from 2025 to 2032.

Aviation Actuator Systems Market Scope & Overview:

In aviation, actuator systems are critical components that convert power into mechanical motion, enabling the control of various aircraft functions. These systems facilitate movements ranging from simple tasks like valve operation to complex actions such as deploying landing gear or adjusting flight control surfaces.

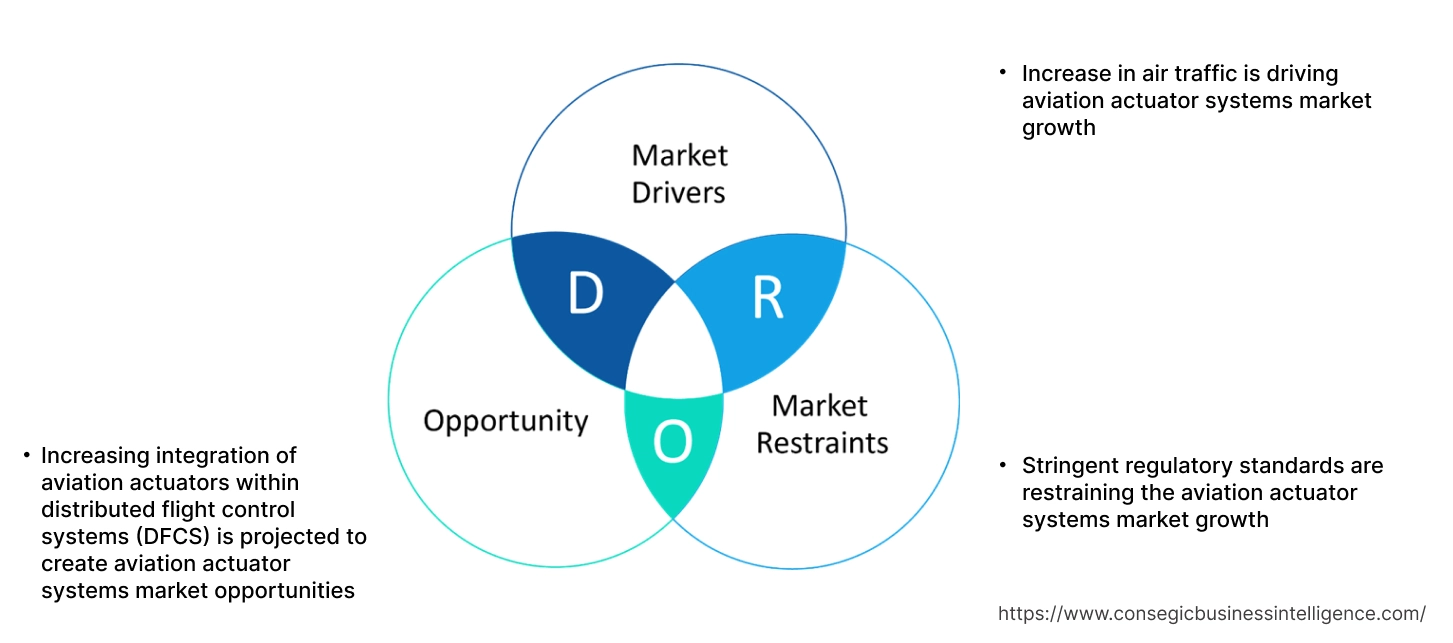

Aviation Actuator Systems Market Dynamics - (DRO) :

Key Drivers:

Increase in air traffic is driving aviation actuator systems market growth

Rising air traffic necessitates airline fleet expansion to handle increased passenger and cargo volumes, driving need for new aircraft from manufacturers like Boeing and Airbus. As each new aircraft requires numerous actuator systems for functions like flight control, landing gear, and doors, this directly fuels the aviation actuator systems market trend. Furthermore, heightened aircraft utilization due to increased air traffic leads to greater wear and tear on these systems, requiring more frequent maintenance and replacements, further boosting the aviation actuator systems market size.

- For instance, according to International Air Transport Association (IATA), in 2024, the aviation industry experienced a significant rebound, with total full-year traffic, measured in revenue passenger kilometers (RPKs), climbing by 10.4% compared to the previous year and surpassing pre-pandemic levels by 3.8%. This surge in demand was met with an 8.7% increase in available seat kilometers (ASK), resulting in a record-breaking overall load factor of 83.5%. Notably, international traffic saw even stronger growth, with RPKs rising by 13.6% and capacity by 12.8%, indicating a robust recovery in global travel.

Consequently, increasing air traffic is driving the aviation actuator systems market expansion.

Key Restraints:

Stringent regulatory standards are restraining the aviation actuator systems market growth

The aviation industry is governed by extremely rigorous standards set by agencies like the Federal Aviation Administration (FAA) in the U.S. and the European Union Aviation Safety Agency (EASA). These regulations mandate extensive testing, documentation, and certification processes for every component, including actuator systems, which results in very high standards for reliability and redundancy in actuator systems. Manufacturers must demonstrate that their products can withstand extreme conditions and perform flawlessly over extended periods. This often necessitates the use of expensive materials and complex manufacturing processes, further driving up costs, thereby restraining the global aviation actuator systems market size.

Therefore, as per the analysis, these combined factors are significantly hindering aviation actuator systems market expansion.

Future Opportunities :

Increasing integration of aviation actuators within distributed flight control systems (DFCS) is projected to create aviation actuator systems market opportunities

Distributed Flight Control System (DFCS) architecture, which distributes flight control functions across multiple actuators and computers, enhances precision and redundancy by mitigating the impact of individual actuator failures. This necessitates actuators capable of accurately and rapidly interpreting complex flight control signals. Consequently, this demand for advanced actuators with integrated sensors and processing capabilities significantly boosts the aviation actuator systems market demand.

- For instance, in Dec 2024, BAE Systems has been selected to supply and integrate its advanced actuator control units (ACUs) and active control sticks for JetZero's innovative blended wing body aircraft demonstrator. These ACUs, functioning as remote actuators within a distributed flight control system, will play a crucial role in interpreting pilot commands and managing flight surfaces, contributing to the aircraft's enhanced energy efficiency and reduced emissions through precise and responsive flight control.

Hence, based on the analysis, increasing integration of aviation actuators within distributed flight control systems (DFCS) is expected to create aviation actuator systems market opportunities.

Aviation Actuator Systems Market Segmental Analysis :

By Motion:

Based on the motion, the market is categorized into linear and rotary.

Trends in the Motion:

- Growing push for "more electric aircraft" (MEA) is heavily influencing linear actuator design.

- Increasing trend towards the adoption of rotary actuator in applications like valve control and other auxiliary systems.

Linear accounted for the largest revenue share in the market in 2024.

- The high precision requirements of flight control surfaces and landing gear systems are driving trends towards actuators equipped with advanced sensors and feedback loops. This demand for accurate positioning and consistent performance of these sophisticated actuators is a key factor influencing the aviation actuator systems market share.

- Additionally, linear actuators are becoming ‘smarter’ with built-in diagnostics and monitoring capabilities, which allows for predictive maintenance, reducing downtime and enhancing safety.

- For instance, in July 2022, Curtiss-Wright secured a contract with Airbus to supply specialized electric actuation systems for the A350F freighter's main cargo door. This includes linear actuators, control electronics, and power units, enabling the door to open, close, latch, and lock, marking a significant step in the aircraft's development.

- Thus, as per the aviation actuator systems market analysis, the aforementioned factors are driving the linear segment.

Rotary is predicted to register the fastest CAGR during the forecast period.

- Rotary actuators are being designed with advanced materials and optimized designs to minimize weight without sacrificing performance, thereby driving the aviation actuator systems market share.

- Applications requiring powerful rotational movement in confined spaces are driving the development of rotary actuators with high-torque density. This involves advancements in motor design and gear systems.

- For instance, in July 2024, Woodward, Inc. announced to supply rotary actuators for the NASA and Boeing X-66A aircraft, a demonstrator of the Transonic Truss-braced Wing design.

- Consequently, the aforementioned factors are driving the rotary actuator segment growth during the forecast period.

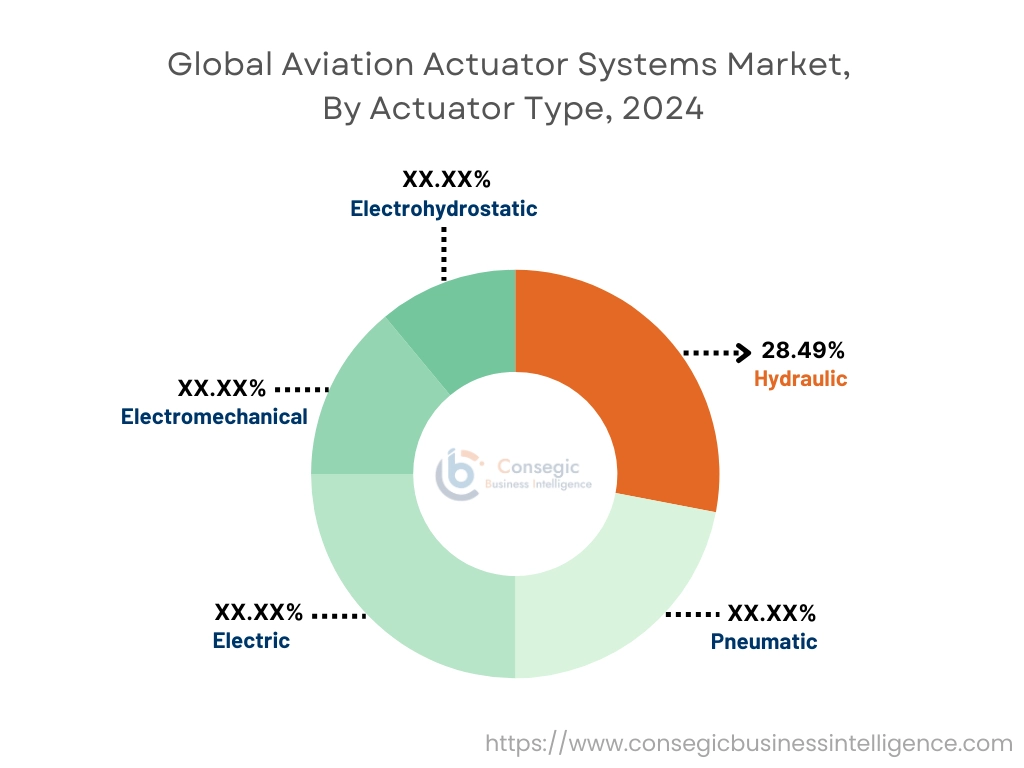

By Actuator Type:

Based on the actuator type, the market is classified into hydraulic, pneumatic, electric, electromechanical, and electrohydrostatic.

Trends in the Actuator Type:

- Trends in electromechanical actuators include improvements in motor design, gear systems, and control electronics to enhance performance and reliability.

- Electrohydrostatic actuators combine the power density of hydraulics with the control precision of electric systems.

Hydraulic accounted for the largest revenue share of 28.49% in 2024.

- Hydraulic actuators are relevant for high-load applications like primary flight control surfaces and landing gear where significant force is necessary, driving aviation actuator systems market trend.

- Moreover, efforts are being made to improve hydraulic system efficiency through advanced fluid management and reduced leakage, which is further driving the aviation actuator systems market demand.

- Thus, as per the aviation actuator systems market analysis, the aforementioned factors are driving the hydraulic actuators segment.

Electric is predicted to witness the fastest growth during the forecast period.

- Electric actuators are experiencing the most significant growth, driven by the "more electric aircraft" (MEA) trend.

- They are being used in a wide range of applications, including flight control surfaces, landing gear, and auxiliary power units.

- They offer improved efficiency, reduced weight, lower maintenance costs, and enhanced control precision.

- Therefore, the aforementioned factors are contributing in driving the market.

By Platform Type:

Based on the platform type, the market is categorized into fixed-wing and rotary-wing.

Trends in the Platform Type:

- Fixed-wing aircraft, particularly commercial airliners, prioritize fuel efficiency, which drives the adoption of lightweight electric actuators to replace heavier hydraulic systems.

- Increasing trend towards the adoption of rotary-wing aircraft, such as helicopters, require actuators that can handle complex and dynamic movements.

Fixed-Wing accounted for the largest revenue share in 2024.

- Advancements in materials and design are focused on minimizing actuator weight without compromising performance, driving the aviation actuator systems market share.

- Modern fixed-wing aircraft, especially those with advanced fly-by-wire systems, require highly precise actuators for flight control surfaces.

- Predictive maintenance is a growing trend, with smart actuators providing real-time data on their condition, which helps reduce downtime and improve safety.

- Thus, as per the aviation actuator systems market analysis, the aforementioned factors are driving the fixed-wing segment.

Rotary-Wing is predicted to register the fastest CAGR during the forecast period.

- Actuators must be robust and reliable, capable of withstanding high vibrations and challenging operational conditions.

- Space and weight constraints are critical in rotary-wing aircraft, which drives the development of compact actuators with high power-to-weight ratios.

- While hydraulic systems remain prevalent for primary rotor control, there's increasing adoption of electric actuators for auxiliary functions, and this trend is driven by the desire to improve efficiency and reduce maintenance.

- Consequently, the aforementioned factors are driving the rotary-wing segment growth during the forecast period.

Regional Analysis:

The global aviation actuator systems market has been classified by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America.

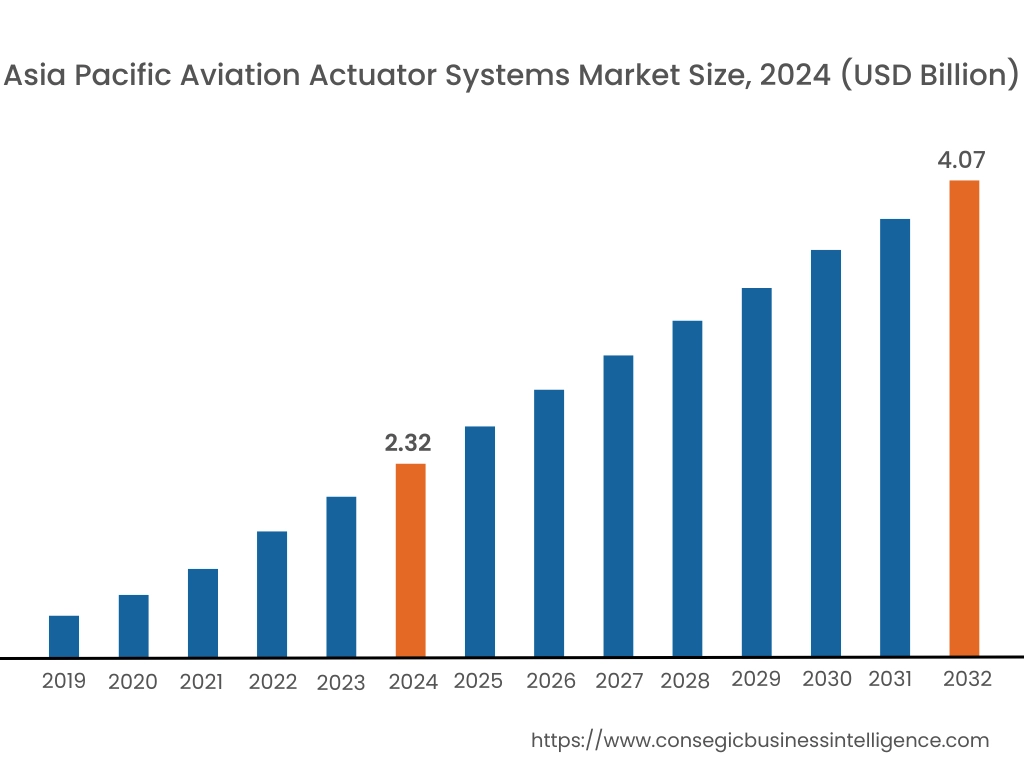

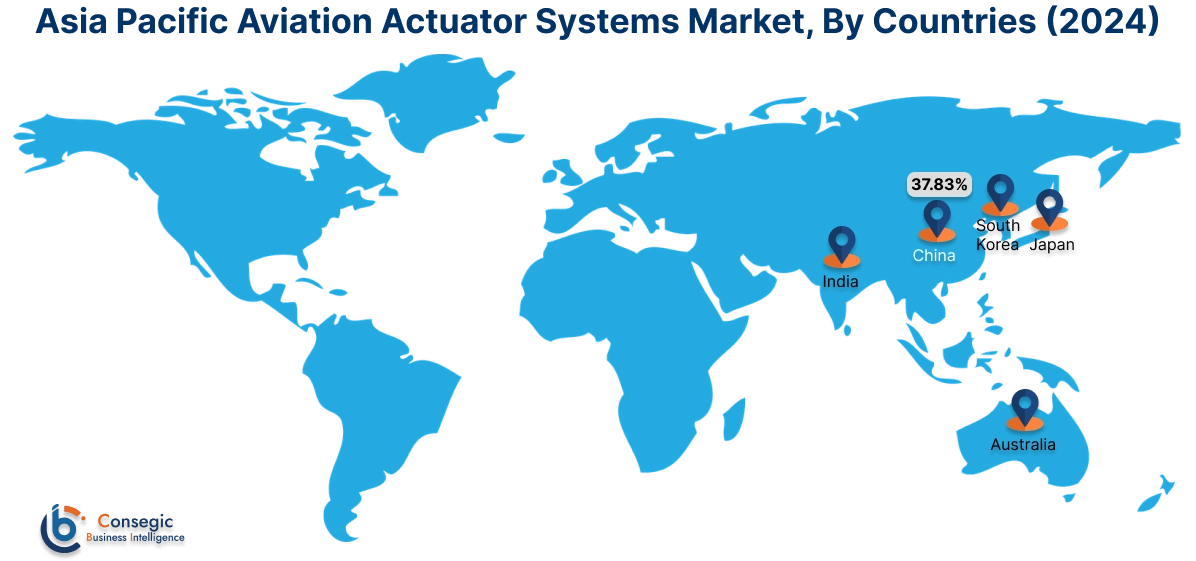

Asia Pacific region was valued at USD 2.32 Billion in 2024. Moreover, it is projected to grow by USD 2.44 Billion in 2025 and reach over USD 4.07 Billion by 2032. Out of these, China accounted for the largest revenue share of 37.83% in 2024. The increasing middle-class population across Asia-Pacific countries, particularly in China and India, is fueling a rapid increase in air travel. This surge in passenger traffic necessitates the extension of airline fleets, thereby driving needs for advanced aviation actuator systems. To meet the growing need for air travel, airlines in the region are actively expanding their fleets, leading to increased procurement of new aircraft. This increase directly translates to a higher demand for aviation actuator systems, which are essential components in aircraft operations.

- For instance, in April 2024, DRDO's Aeronautical Development Agency (ADA) achieved a key milestone in India's defense self-reliance by delivering the initial batch of domestically developed Leading Edge Actuators and Airbrake Control Modules to Hindustan Aeronautics Limited (HAL). HAL's Lucknow division is now prepared to manufacture these vital components for the 83 LCA Tejas Mk1A aircraft currently on order. This marks a significant step in indigenizing critical aeronautical technologies.

North America was valued at USD 3.40 Billion in 2024. Moreover, it is projected to grow by USD 3.57 Billion in 2025 and reach over USD 5.78 Billion by 2032. North America is home to major aircraft Original Equipment Manufacturers (OEMs) like Boeing, Bombardier, and Gulfstream. Their continuous production and innovation in aircraft design directly drive the need for advanced actuator systems. The United States holds the position of the world's largest defense spender. This substantial investment translates into significant procurement of new military aircraft, including advanced fighter jets, helicopters, and transport aircraft, all of which require sophisticated actuator systems for critical functions like flight control and landing gear.

- For instance, in June 2021, Curtiss-Wright Corporation has supplied Eviation Aircraft with the primary flight control actuators and control electronics for their all-electric Alice aircraft, which is gearing up for its maiden flight. These high-power density electromechanical actuators (EMAs) from Curtiss-Wright offer a modular and distributed system, facilitating a flexible control design.

As per the aviation actuator systems market analysis, Europe possesses a well-established aerospace industry with major aircraft manufacturers and a strong focus on sustainable aviation, in turn driving demand for advanced and efficient actuator systems. Additionally, Latin American aviation sector is experiencing gradual growth, driven by increasing air travel demand and the need for fleet modernization in several countries. Moreover, Middle East is witnessing significant expansion in its aviation infrastructure and airline fleets, fueled by helicopter tourism and strategic investments, leading to substantial need for advanced actuator systems.

Top Key Players and Market Share Insights:

The market is highly competitive with major players providing aviation actuator systems to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the aviation actuator systems industry include-

- Honeywell International Inc. (US)

- Eaton Corporation plc (Ireland/US)

- Moog Inc. (US)

- Triumph Group (US)

- Arkwin Industries Inc. (US)

- Electromech Technologies (TransDigm Group) (US)

- Safran SA (France)

- Liebherr-International Deutschland GmbH (Germany)

- Parker Hannifin Corporation (US)

- Raytheon Technologies Corporation (US) (via Collins Aerospace)

- Curtiss-Wright Corporation (US)

- Woodward, Inc. (US)

Recent Industry Developments :

Partnership:

- In July 2022, Safran, the France-based aviation component manufacturer, introduced an innovative electric nose landing gear actuator at the Farnborough International Airshow. This actuator is a first of its kind, providing both extension and retraction functions, as well as electric nose wheel steering capabilities for future narrow-body and wide-body aircraft.

Aviation Actuator Systems Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 15.69 Billion |

| CAGR (2025-2032) | 7.6% |

| By Motion |

|

| By Actuator Type |

|

| By Platform Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the aviation actuator systems market? +

The aviation actuator systems market size is estimated to reach over USD 15.69 Billion by 2032 from a value of USD 9.14 Billion in 2024 and is projected to grow by USD 9.62 Billion in 2025, growing at a CAGR of 7.6% from 2025 to 2032.

What specific segmentation details are covered in the aviation actuator systems report? +

The aviation actuator systems report includes specific segmentation details for motion, actuator type, platform type, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the aviation actuator systems market, rotary is the fastest-growing segment during the forecast period.

Who are the major players in the aviation actuator systems market? +

The key participants in the Aviation Actuator Systems market are Honeywell International Inc. (US), Eaton Corporation plc (Ireland/US), Moog Inc. (US), Safran SA (France), Liebherr-International Deutschland GmbH (Germany), Parker Hannifin Corporation (US), Raytheon Technologies Corporation (US) (via Collins Aerospace), Curtiss-Wright Corporation (US), Woodward, Inc. (US), Triumph Group (US), Arkwin Industries Inc. (US), Electromech Technologies (TransDigm Group) (US), and Others.