- Summary

- Table Of Content

- Methodology

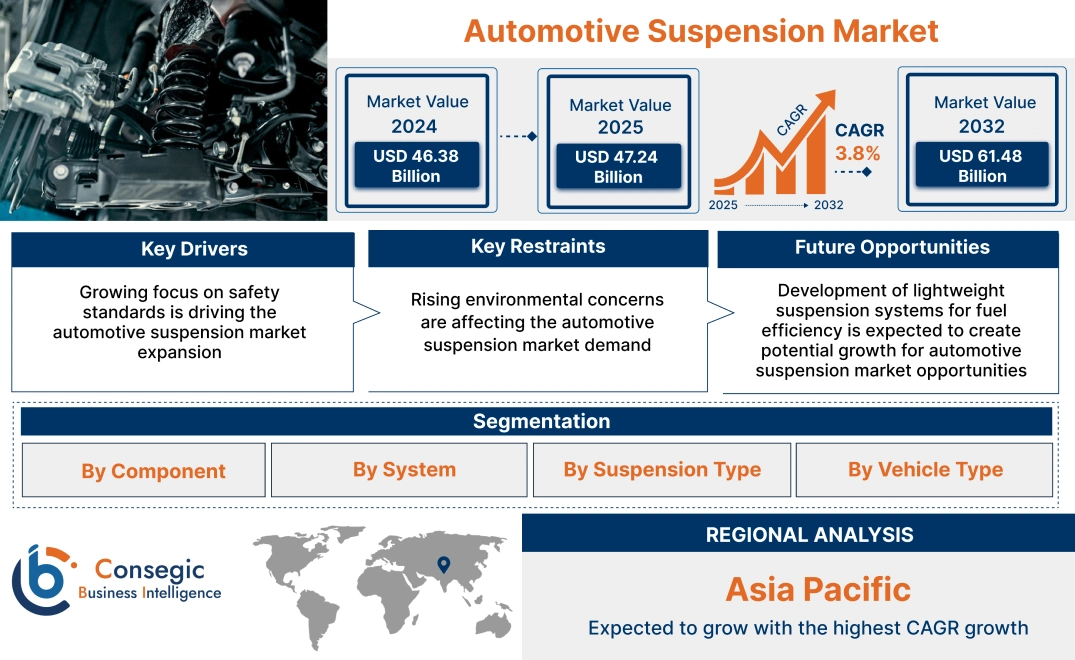

Automotive Suspension Market Size:

Automotive Suspension Market Size is estimated to reach over USD 61.48 Billion by 2032 from a value of USD 46.38 Billion in 2024 and is projected to grow by USD 47.24 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

Automotive Suspension Market Scope & Overview:

The automotive suspension refers to the system of components, such as linkages, springs, and shock absorbers that connect vehicles to their wheels, which ensures smooth ride, better control, and stable handling. Consumers are increasingly prioritizing a smooth ride experience, particularly in regions where road infrastructure may be less developed. This has led to a surge in the adoption of advanced suspension technologies, such as adaptive and air suspension systems, across various vehicle segments. In addition to this, advanced suspension systems incorporated by manufacturers enable vehicles to absorb road shocks formed by changes in surface level and road bumps.

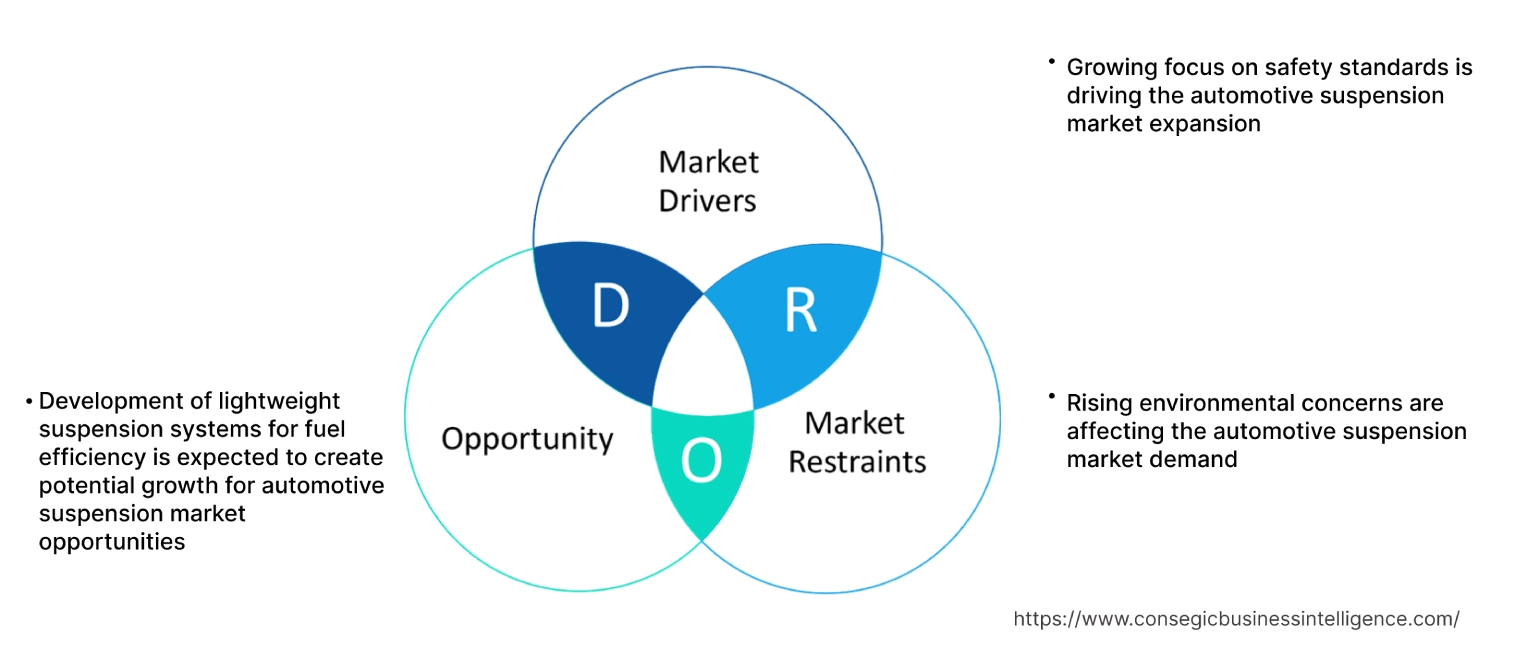

Automotive Suspension Market Dynamics - (DRO) :

Key Drivers:

Growing focus on safety standards is driving the automotive suspension market expansion

The global market is experiencing significant growth, driven by increasing vehicle production and rising consumer demand for enhanced ride comfort and safety. Safety standards play a crucial role in shaping the development and adoption of suspension systems. Governments and regulatory bodies worldwide are implementing stringent safety regulations, compelling manufacturers to integrate advanced suspension technologies that improve vehicle stability and control. These safety standards ensure that vehicles meet specific performance criteria, reducing the risk of accidents caused by poor suspension performance. As a result, automakers are focusing on innovative suspension solutions, such as electronic stability control (ESC) and active suspension systems, to comply with safety regulations and enhance overall vehicle safety.

- For instance, in June 2024, Hitachi Astemo developed semi-active suspension system, 360-degree camera, and steer-by-wire technologies, to improve autonomous and electric vehicles. The company’s next-generation G5 semi-active suspension system enhances primary ride balance, while focusing of ride comfort.

Thus, according to the automotive suspension market analysis, the growing focus on safety standards in all types of vehicles is driving the automotive suspension market size and trends.

Key Restraints:

Rising environmental concerns are affecting the automotive suspension market demand

The production and disposal of suspension components contribute to environmental pollution, including the release of harmful chemicals and the generation of waste. Moreover, the mining of raw materials, such as metals and rubber, used in suspension systems has a significant environmental impact, including habitat destruction and increased carbon emissions. Further, undercarriage of vehicles is highly susceptible to rust, as they are constantly exposed to water and road. It promotes the formation of rust, which can weaken the structure and components of car. This leads to significant damage to vehicles and the environment. Thus, the above analysis depicts that the aforementioned factors would further impact on the automotive suspension market size.

Future Opportunities :

Development of lightweight suspension systems for fuel efficiency is expected to create potential growth for automotive suspension market opportunities

The development of lightweight suspension systems for fuel efficiency is becoming a key driver in the automotive sector, as automakers strive to meet increasingly stringent fuel economy standards and consumer demand for more eco-friendly vehicles. Lightweight suspension systems play a critical role in reducing the overall weight of the vehicle, which directly impacts fuel consumption and emissions. By using materials like aluminum, carbon fiber, and composite components, manufacturers can reduce the weight of suspension systems without compromising strength, durability, or performance. Moreover, the shift towards electric and hybrid vehicles, which rely heavily on battery efficiency and energy regeneration, has encouraged the development of advanced, lightweight suspension systems. These systems not only help improve fuel efficiency but also enhance the overall driving experience by providing better handling and comfort.

- For instance, in February 2023, Elka Suspension tested a composite spring prototype for off-road vehicle applications at the King of Hammers 2023, a racing event held in California. The composite springs can be up to 30% lighter as compared to metal springs. Further, for utility vehicles, the composite springs lead to 14 pounds in weight reduction.

Thus, based on the above automotive suspension market analysis, these trends towards lightweight, high-performance suspension solutions are expected to drive the automotive suspension market opportunities and trends.

Automotive Suspension Market Segmental Analysis :

By Component:

Based on component, the automotive suspension market is segmented into air compressors, ball joint, control arm, shock dampener, struts, and others.

Trends in component:

- The innovations in the suspension components such as adaptive and semi-active shock absorbers, which automatically adjust damping characteristics based on road conditions and driving styles, are gaining popularity. These advanced systems contribute to improved vehicle stability, reduced vibration, and enhanced overall driving comfort.

- The emergence of online retail channels and the availability of a wide range of aftermarket products are providing consumers with convenient options for purchasing suspension components.

- Thus, the above factors are driving the automotive suspension market demand.

The shock dampener segment accounted for the largest revenue share in the year 2024.

- The integration of electronic and adaptive shock absorbers in premium and luxury vehicles is becoming more common. These systems adjust damping rates in real-time, providing a superior driving experience.

- The use of advanced materials also allows for more intricate and efficient designs, leading to better shock absorption and longer-lasting components. This shift towards advanced materials is being driven by stringent environmental regulations and the automotive industry's focus on sustainability and reducing carbon emissions.

- In April 2023, ZF Aftermarket launched TRW products, which included TRW brake pads, TRW brake discs, and TRW shock absorbers, for Indian market. The shock absorbers and brake pads are free from harmful chemicals and work to reduce carbon emissions by generating less heat.

- Thus, the above developments are further driving the automotive suspension market growth.

The control arm segment is anticipated to register the fastest CAGR during the forecast period.

- Control arms, also known as A-arms or wishbones, are crucial components of a vehicle's suspension system, connecting the wheel hub to the chassis. They play a vital role in maintaining stability, handling, and smooth ride quality.

- With the automotive sector shifting towards electric vehicles and the integration of advanced driver assistance systems (ADAS), there is a growing need for high-performance control arms that can enhance vehicle dynamics and safety.

- Stringent government regulations regarding vehicle emissions and fuel efficiency are compelling automakers to adopt lightweight materials like aluminum and composite materials for manufacturing control arms. These lightweight materials not only help in reducing vehicle weight but also contribute to improved fuel efficiency and reduced carbon emissions.

- Thus, the aforementioned factors are expected to drive the automotive suspension market share during the forecast period.

By System:

Based on the system, the automotive suspension market is segmented into a passive system, active system, and semi-active system.

Trends in system:

- The rising demand for enhanced vehicle comfort, with technological advancements in materials and electronic systems, are driving the development and adoption of these systems across various vehicle segments, including passenger cars, commercial vehicles, and electric vehicles.

- The innovations such as adaptive air suspension, semi-active and active suspension systems, and intelligent suspension technologies are becoming more prevalent in both high-end and mass-market vehicles.

The passive system segment accounted for the largest revenue in the year 2024.

- Passive suspension systems are the traditional choice, offering a simple and cost-effective solution for vehicle suspension. These systems use mechanical components such as springs and shock absorbers to dampen vibrations and maintain vehicle stability.

- Manufacturers are investing heavily in research and development to innovate new suspension technologies, including adaptive damping systems, air suspensions, and passive suspension systems. These advancements not only enhance ride quality but also contribute to improved fuel efficiency and overall vehicle safety.

- Thus, based on the above analysis, these developments in the passive system segment are driving the automotive suspension market growth.

The active system segment is anticipated to register the fastest CAGR during the forecast period.

- As consumers increasingly prioritize comfort and safety features in their vehicles, automakers are integrating active suspension systems to meet these expectations. These systems utilize sensors and control units to continuously adjust the vehicle's suspension settings, providing a smoother ride and better handling, especially on uneven terrain or during sudden manoeuvres.

- Active suspension systems utilize a network of sensors, actuators, and electronic controls to actively adjust suspension parameters in real-time, providing optimal ride quality, stability, and control across a wide range of driving conditions.

- The growing demand for luxury and high-performance vehicles is fuelling the adoption of active suspension systems among premium car manufacturers. These systems are becoming increasingly common in luxury sedans, SUVs, and sports cars, where they contribute to a comfortable and controlled ride quality that aligns with the expectations of customers.

- These developments in the system segment is anticipated to further drive the automotive suspension market trends during the forecast period.

By Suspension Type:

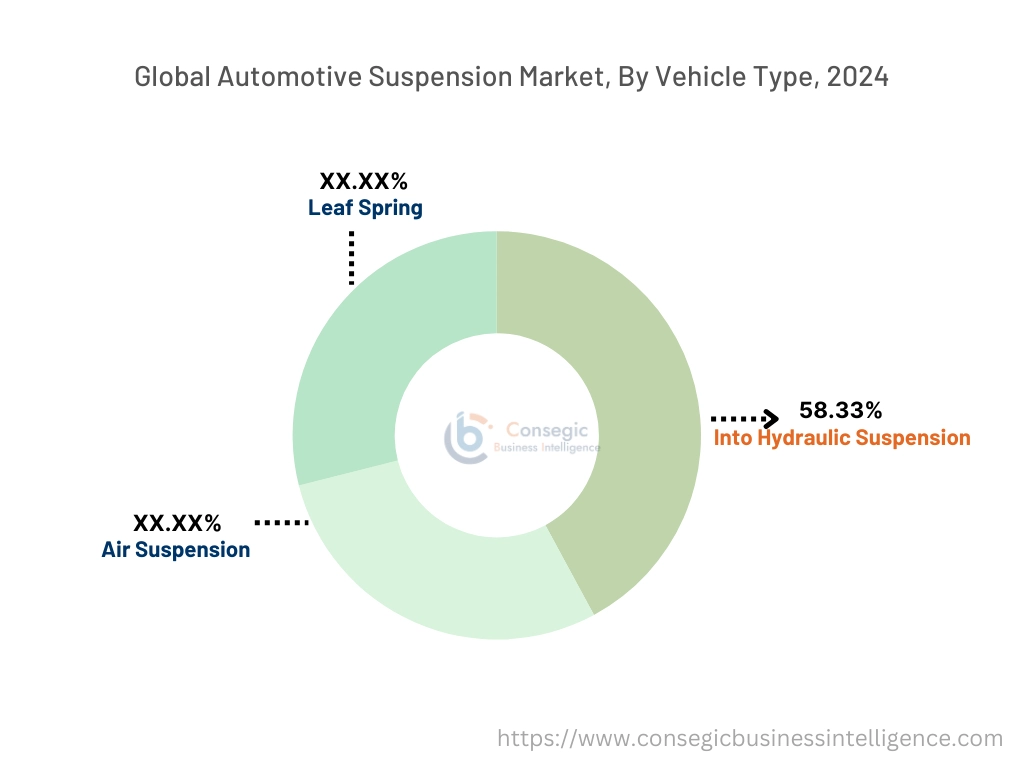

Based on suspension type, the market is segmented into hydraulic suspension, air suspension, and leaf spring.

Trends in suspension type:

- The rising disposable incomes in the emerging markets have led to a growing need for premium and high-performance vehicles, which are often equipped with advanced suspension systems.

- As commercial vehicles continue to evolve, the need for innovative suspension systems will grow, with manufacturers focusing on developing solutions that meet the specific needs of light and heavy commercial vehicles.

The air suspension segment accounted for the largest revenue share in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- As governments invest in modernizing transportation networks and improving road infrastructure to accommodate the growing population and economic activities, there is a need for advanced air suspension solutions that can enhance vehicle performance and ride quality, particularly in commercial vehicles that travel across long distances over varied terrain.

- Manufacturers in the automotive sector are exploring ways to develop sustainable technologies, including air suspension systems. By focusing on environmental benefits, such as reduced vehicle weight, improved fuel efficiency, and lower emissions, manufacturers can align their products with evolving market preferences and cater to environmentally conscious consumers.

- For instance, in July 2021, WABCO launched energy-efficient air suspension technologies, such as ECAS technology, for heavy-duty trucks, to improve fuel efficiency. WABCO’s air suspension with ECAS technology reacts with external factors, such as uneven road surfaces, braking, and road curves.

- These developments in the air suspension segment are driving the global market share during the forecast period.

By Vehicle Type:

Based on vehicle type, the automotive suspension market is segmented into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs)

Trends in vehicle type:

- With continuous technological advancements and increasing emphasis on safety and comfort, the segment is expected to witness sustained growth in the coming years.

- Stringent government regulations related to vehicle safety and emissions are influencing the adoption of advanced suspension systems in both passenger vehicles and commercial vehicles. Manufacturers are compelled to integrate features such as electronic stability control (ESC), adaptive damping systems, and air suspension systems to comply with these regulations and meet the evolving customer expectations.

The passenger vehicles segment accounted for the largest revenue share of 58.33% in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- The segment growth can be attributed to the rising disposable income levels and significant spending on maintenance and performance management by replacing parts, such as suspension systems.

- As consumers prioritize comfort and luxury features in their vehicles, air suspension systems have become a desirable option for automakers looking to differentiate their products and attract customers. These systems offer smoother rides, reduced road noise, and improved handling characteristics compared to traditional suspension systems, contributing to a more enjoyable driving experience for passengers.

- For instance, in September 2021, Continental AG extended its product portfolio in the automotive spare parts group, with the launch of air suspension dampers, thermostats, and compressors. The products will be initially available for Volkswagen and Audi models, including VW Touraeg, Audi Q7, and Audi Q8.

- Thus, based on the above analysis, the aforementioned factors are expected to drive the automotive suspension market trends during the forecast period.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

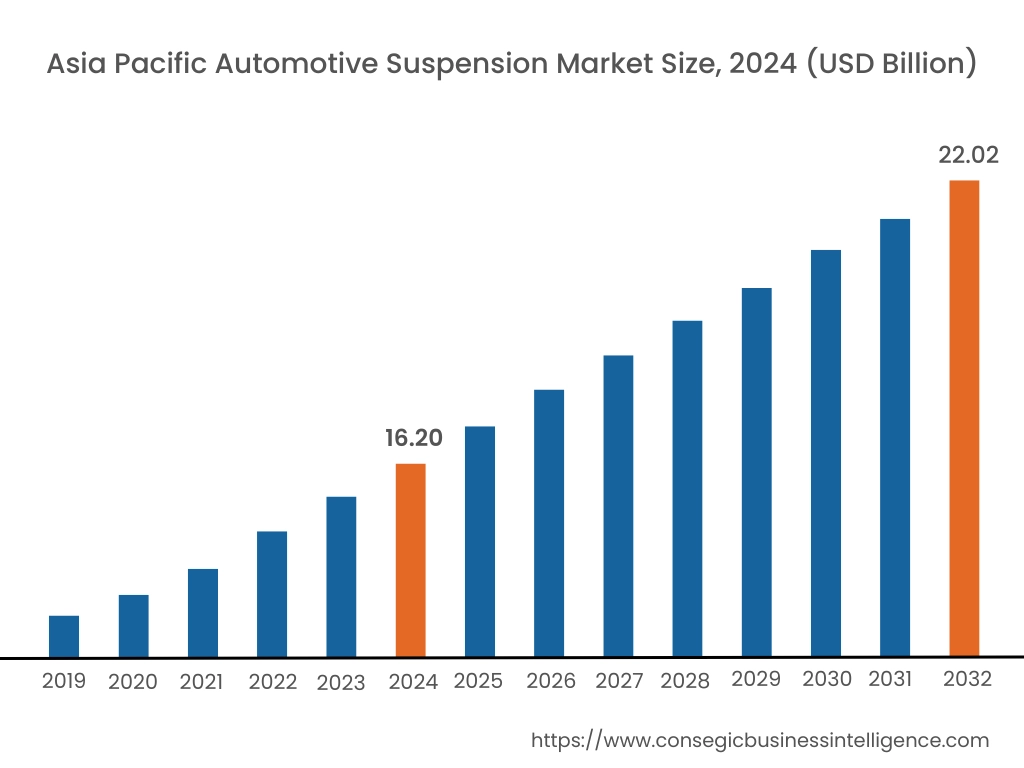

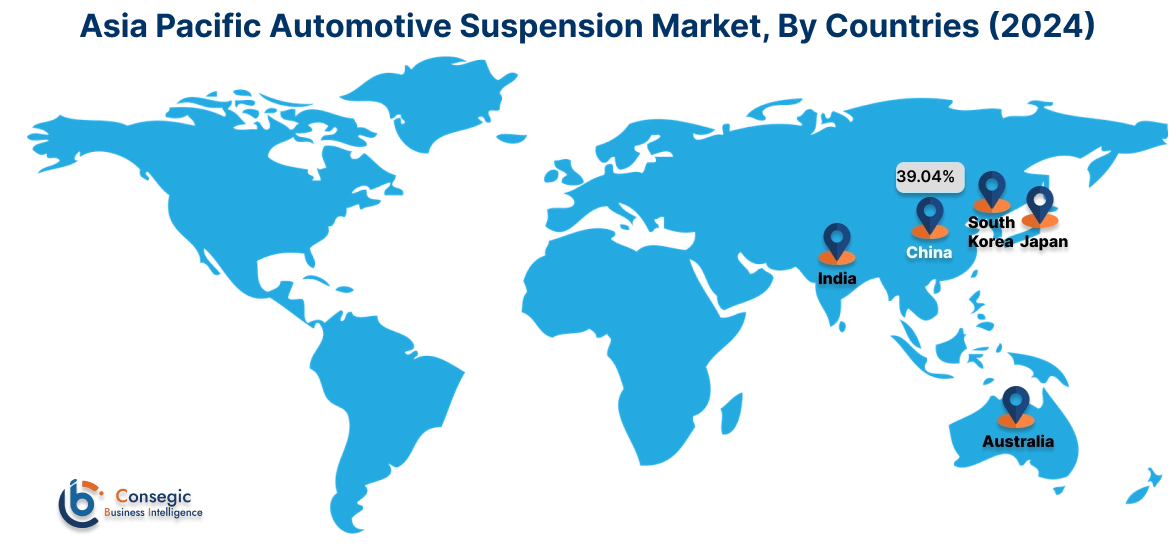

Asia Pacific automotive suspension market expansion is estimated to reach over USD 22.02 billion by 2032 from a value of USD 16.20 billion in 2024 and is projected to grow by USD 16.53 billion in 2025. Out of this, the China market accounted for the maximum revenue split of 39.04%. The region emerges as a significant growth hub for the global market, fueled by the rapid expansion of the automotive sector in emerging economies such as China and India. With growing urbanization, increasing disposable incomes, and rising consumer need for premium vehicles, Asia Pacific presents lucrative opportunities for manufacturers of air suspension systems. Additionally, infrastructure development initiatives and investments in transportation further support market development in the region, as governments prioritize modernizing transportation networks to accommodate the growing automotive sector. These factors would further drive the regional automotive suspension market share during the forecast period.

- For instance, in June 2024, Nidec Corporation developed a new air suspension motor for automobiles. The motor is compact, durable, and improves the driving performance based on running circumstances. Further, the use of electronic commutation facilitates motor to start and drive the compressor quickly and provide better power-up responsiveness.

North America market is estimated to reach over USD 16.55 billion by 2032 from a value of USD 12.62 billion in 2024 and is projected to grow by USD 12.84 billion in 2025. North America represents a significant market for automotive suspension, driven by the presence of established automotive manufacturers, technological innovation, and consumer demand for vehicles with advanced suspension systems. Further, the region's mature automotive sector and stringent safety regulations contribute to the adoption of high-quality control arms and shock absorbers that meet regulatory standards. In addition to this, the region’s focus on vehicle performance, customization, and off-road capabilities drives the need for specialized control arm solutions tailored to the needs of diverse vehicle segments and applications. These factors would further create the need of automotive suspension components in the regional market.

- For instance, in May 2022, Tenneco Inc. announced that 2022 Mercedes AMGSL-Class would feature intelligent suspension technologies from their Monroe brand portfolio. The new models of Mercedes will be available with Tenneco’s CSVA2 semi-active kinetic suspension systems.

According to the analysis, the automotive suspension industry in Europe is projected to witness significant development during the forecast period. The region is witnessing increasing investments in research and development activities aimed at enhancing suspension technologies to meet the evolving consumer preferences and regulatory requirements. Moreover, the presence of stringent emission norms and a trend towards electric and hybrid vehicles propelled the adoption of active suspension systems in Europe. Additionally, infrastructure development initiatives and investments in transportation infrastructure are supporting the market growth in the Latin American, as governments prioritize modernizing transportation networks to accommodate the growing automotive industry. Further, the need for off-road vehicles, SUVs, and pickup trucks in the Middle East & Africa region contributes to the need for robust and durable suspension system capable of withstanding rugged terrain and extreme weather conditions.

Top Key Players and Market Share Insights:

The global automotive suspension market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the automotive suspension industry include-

- Benteler International AG (Germany)

- Continental AG (Germany)

- HL Mando Corp. (South Korea)

- KYB Corporation (Japan)

- Marelli Corporation (Japan)

- NHK Springs Co., Ltd. (Japan)

- Sogefi Group (Italy)

- Tenneco Inc. (U.S.)

- ThyssenKrupp AG (Germany)

- ZF Friedrichshafen AG (Germany)

Recent Industry Developments :

Product Launch:

- In April 2023, BYD unveiled suspension systems and self-developed chassis. These launches showcase BYD’s commitment to vertical integration and independence in automotive products. The new products provide improved safety, enhanced driving experience, and better efficiency for electric vehicles.

Automotive Suspension Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 61.48 Billion |

| CAGR (2025-2032) | 3.8% |

| By Component |

|

| By System |

|

| By Suspension Type |

|

| By Vehicle Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Automotive Suspension market? +

Automotive Suspension Market Size is estimated to reach over USD 61.48 Billion by 2032 from a value of USD 46.38 Billion in 2024 and is projected to grow by USD 47.24 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

Which is the fastest-growing region in the Automotive Suspension market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. With the largest automotive production capacity globally, Asia Pacific offers lucrative opportunities for suspension system manufacturers to supply components to both domestic and export markets. The region's focus on vehicle electrification, fuel efficiency, and customization.

What specific segmentation details are covered in the Automotive Suspension report? +

The automotive suspension report includes specific segmentation details for component, system, suspension type, vehicle type, and region.

Who are the major players in the Automotive Suspension market? +

The key participants in the market are Benteler International AG (Germany), Continental AG (Germany), HL Mando Corp. (South Korea), KYB Corporation (Japan), Marelli Corporation (Japan), NHK Springs Co., Ltd. (Japan), Sogefi Group (Italy), Tenneco Inc. (U.S.), ThyssenKrupp AG (Germany), ZF Friedrichshafen AG (Germany), and others.