- Summary

- Table Of Content

- Methodology

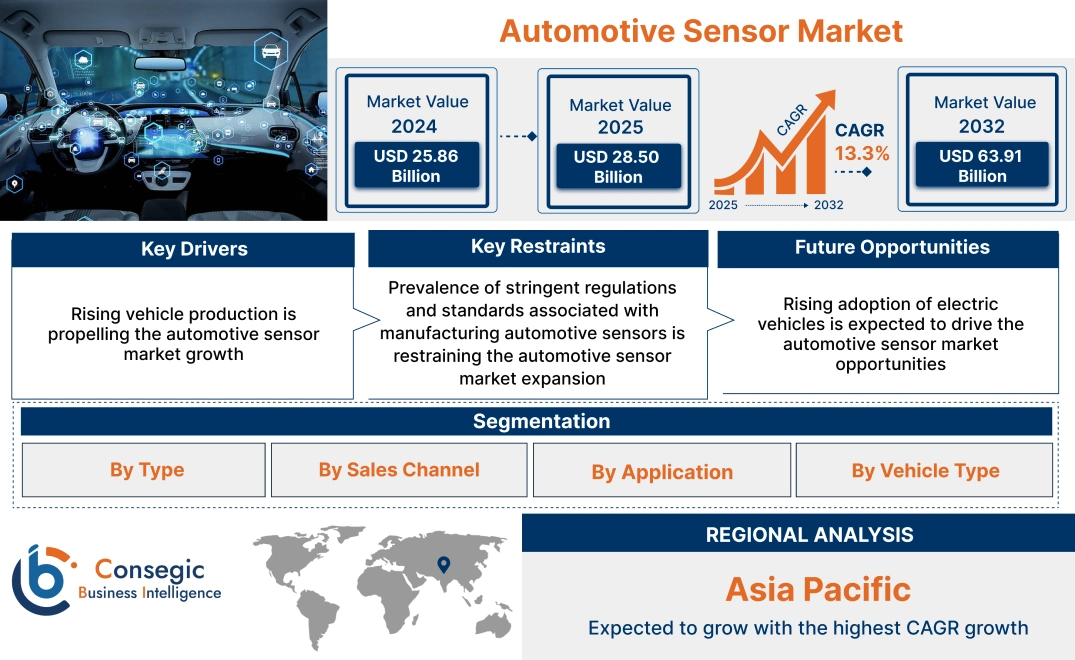

Automotive Sensor Market Size:

Automotive Sensor Market size is estimated to reach over USD 63.91 Billion by 2032 from a value of USD 25.86 Billion in 2024 and is projected to grow by USD 28.50 Billion in 2025, growing at a CAGR of 13.3% from 2025 to 2032.

Automotive Sensor Market Scope & Overview:

Automotive sensors play a crucial role in facilitating smooth operation of modern automobiles. Automobile sensors provide information regarding multiple vehicle parameters to the electronic control unit (ECU) in order to ensure improved vehicle efficiency, safety, and performance. Moreover, various types of automotive sensors such as temperature sensors, speed sensors, pressure sensors, position sensors, and others are primarily used in passenger cars and commercial vehicles.

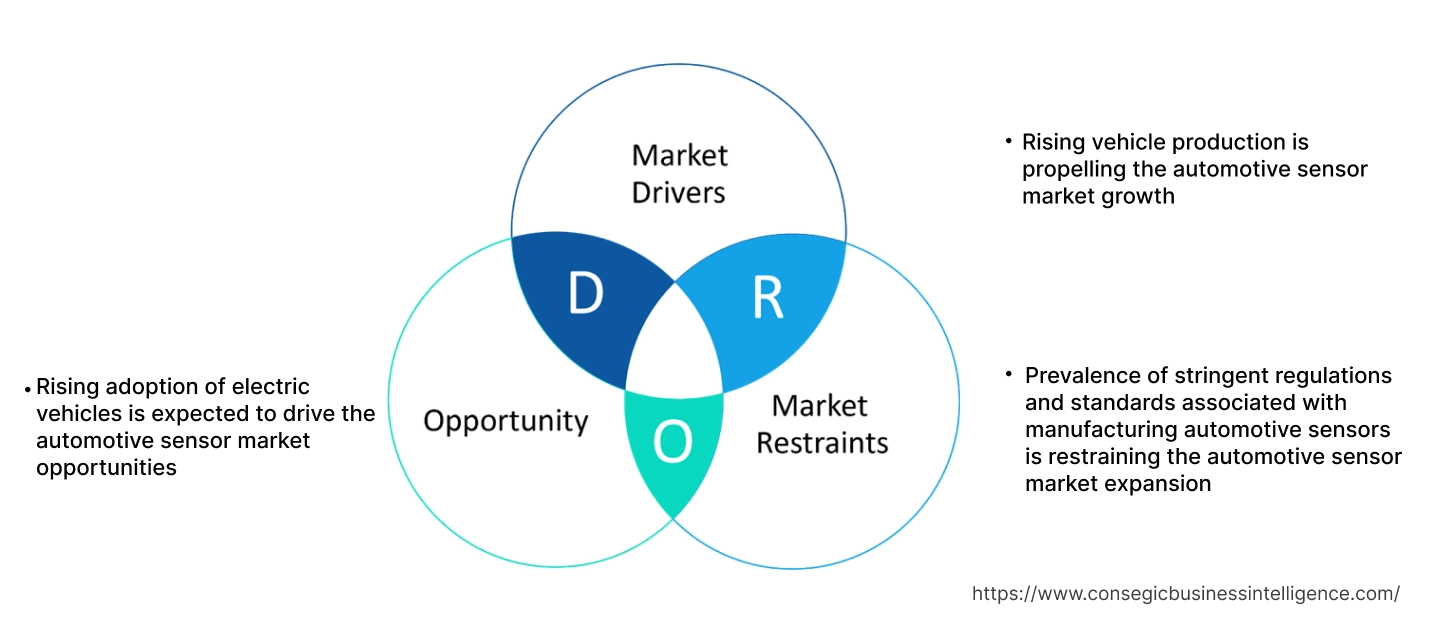

Automotive Sensor Market Dynamics - (DRO) :

Key Drivers:

Rising vehicle production is propelling the automotive sensor market growth

Automobile sensors are designed for measuring a wide range of physical parameters that are crucial for smooth functioning of vehicle. Sensors are integrated in vehicles for monitoring various aspects of a vehicle, including its temperature, engine, coolant system, oil pressure, vehicle speed, emission levels, and others. Similarly, automobile sensors send signals to the ECU for making appropriate adjustments or warning the driver. The sensors are integrated in vehicles for constant monitoring of various aspects of the vehicle to facilitate improved safety and performance. As a result, the rising vehicle production is further driving the market.

- For instance, according to the International Organization of Motor Vehicle Manufacturers, the passenger car production worldwide reached up to 68,020,265 units in 2023, depicting an increase of nearly 11% from 61,553,361 units in 2022. Further, the total passenger car production across the world reached 57,086,075 in 2021.

Therefore, as per the analysis, the rising vehicle production is driving the adoption of automotive sensors, in turn proliferating the automotive sensor market size.

Key Restraints:

Prevalence of stringent regulations and standards associated with manufacturing automotive sensors is restraining the automotive sensor market expansion

The manufacturers of automobile sensors have to comply with various stringent standards such as ISO (International Organization for Standardization) standard, Automotive Electronic Council: AEC-Q100 standard, International Electrotechnical Commission (IEC) standard, and others.

ISO standard is among the primary standards that include ISO 9001 and ISO 14001, which apply to quality management and environmental management respectively. ISO standards provide a set of guidelines for automobile sensor manufacturers to establish levels of homogeneity in accordance with the management, provision of services, and product development in the industry.

Additionally, automobile sensor manufacturers must comply with AEC-Q100 standard developed by Automotive Electronic Council. AEC-Q100 standard provides a set of rigorous requirements and tests that electronic components must pass to ensure its suitability for utilization in automotive applications. Hence, the prevalence of aforementioned regulations and standards associated with manufacturing automobile sensors are restraining the market.

Future Opportunities :

Rising adoption of electric vehicles is expected to drive the automotive sensor market opportunities

Factors including the prevalence of stringent automotive emission regulations, rising consumer preference for sustainable transportation, along with availability of subsidies and tax rebates are leading to significant adoption of electric vehicles (EVs). Moreover, modern EVs are often integrated with a wide range of sensors for monitoring, controlling, and optimizing numerous aspects of electric vehicles' safety and performance, which is providing lucrative aspects for market growth.

- For instance, according to International Energy Agency (IEA), the overall sales of electric car reached approximately 14 million in 2023, among which China, Europe and United States accounted for 95% of the total sales.

Hence, as per the analysis, the rising adoption of electric vehicles is projected to increase the integration of vehicle sensors in modern EVs, in turn driving the automotive sensor market opportunities during the forecast period.

Automotive Sensor Market Segmental Analysis :

By Type:

Based on type, the market is segmented into temperature sensors, speed sensors, pressure sensors, position sensors, and others.

Trends in the type:

- Rising advancements associated with temperature sensors, position sensors, and pressure sensors for improve vehicle safety, efficiency, and performance.

- There is a rising trend towards utilization of position sensors in modern automobiles for determining the steering wheel position, seat positions, and pedal positions among others.

The positon sensors segment accounted for a significant revenue in the overall market in 2024.

- Position sensors are primarily used in automobiles for determining the steering wheel position, seat positions, pedal positions, along with the position of various valves, actuators, and knobs within a vehicle.

- Moreover, position sensors are integrated in modern vehicles for facilitating steering angle and gear position, clutch/throttle actuation, and pedal position among others.

- For instance, in May 2024, Melexis introduced its new MLX90427 model of magnetic position sensor. The sensor is specifically designed for embedded position sensor applications in automobiles requiring high functional safety levels. The position sensor is ideal for steer-by-wire applications.

- According to the automotive sensor market analysis, rising innovations associated with position sensors for automotive applications are driving the automotive sensor market size.

The temperature sensors segment is anticipated to register a substantial CAGR growth during the forecast period.

- Automotive temperature sensors are utilized for measuring temperature at several places within an automobile. Temperature sensors are primarily used in vehicles for monitoring the engine's coolant, oil, and air temperatures among others.

- Moreover, automotive temperature sensor plays an essential role in ensuring vehicle performance, safety, and efficiency by providing accurate and timely temperature data to several control systems.

- For instance, in May 2024, NOVOSENSE launched its new NST175-Q1 series of automotive digital output temperature sensors along with NST86-Q1, NST235-Q1, and NST60-Q1 series of automotive analog output temperature sensors. The temperature sensors feature high-reliability, high-performance CMOS temperature measurement technology, along with high accuracy over the complete temperature range.

- Thus, increasing advancements associated with automotive temperature sensors are anticipated to propel the market during the forecast period.

By Sales Channel:

Based on sales channel, the market is segmented into original equipment manufacturer (OEM) and aftermarket.

Trends in the sales channel:

- Factors including the availability of targeted advertising, competitive pricing, ease of use, and reliable shipping and return policies are among the key prospects driving the OEM channel segment.

- Factors including the rising automotive MRO (maintenance, repair, and operation) activities, availability of economical products in comparison to OEM products, higher accessibility to a variety of products, and higher flexibility are primary determinants for boosting the aftermarket segment.

The original equipment manufacturer (OEM) segment accounted for a substantial revenue share in the total automotive sensor market share in 2024.

- In the automobile sensor sector, an OEM (original equipment manufacturer) refers to companies whose automobile sensor is utilized as components in the products of another company, which then sells the finished item to respective end users.

- OEM sales agreements enable a company to sell its products to another company by relabelling the products and selling them as its own. The process enables a manufacturer to quickly leverage existing marketing and sales infrastructure without the need of building their own infrastructure.

- Moreover, purchasing automobile sensors from an OEM offers various benefits including faster response time, higher product quality, competitive pricing, excellent support and warranty, faster production, and higher return on investments among others.

- Therefore, the above benefits OEM channels are primary determinants for driving the OEM segment.

Aftermarket segment is anticipated to register fastest CAGR growth during the forecast period.

- The aftermarket channel involves the sale of spare parts, components, and accessories for maintaining or improving an original product.

- The aftermarket channel for automobile sensors offers opportunities for the distribution of additional goods to support and improve the usage of automobile sensors that has already been procured. Purchases are also made for upgrading or replacing the existing automobile sensors after the initial purchase.

- Moreover, aftermarket sales channel provides numerous benefits including wider reach, increased customer convenience, enhanced product visibility, and others. The above benefits of aftermarket sales channel are vital aspects for increasing the distribution of automobile sensors from aftermarket sales channels.

- For instance, Continental Automotive Technologies GmbH offers a broad range of aftermarket temperature sensors, pressure sensors, and inertial sensors for automotive applications in its aftermarket product offerings.

- Hence, the increasing availability of automobile sensors in aftermarket sales channels, attributing to its aforementioned benefits, is a key factor projected to drive the aftermarket segment during the forecast period.

By Application:

Based on application, the market is segmented into engine management and control, safety systems, advanced driver assistance systems, and others.

Trends in the application:

- Increasing trend in adoption of automobile sensors such as temperature sensors, pressure sensors, and others for improved engine management and emission control.

- Rising integration of advanced driver assistance systems (ADAS) in modern vehicles is increasing the adoption of automobile sensors to support and enhance the driving experience.

Engine management and control segment accounted for a significant revenue in the overall automotive sensor market share in 2024.

- Sensors play a vital role in automotive engine management system and enable peak performance, fuel economy, and emission control.

- Automobile sensors are primarily used in engine management and control applications including fuel/air mixture control, ignition timing, cooling system, turbocharger control, and other related applications.

- Moreover, temperature sensors are used for monitoring the engine's coolant temperature. Similarly, pressure sensors are used in turbocharged engines for monitoring the boost pressure and ensuring that it remains within the safe operating parameters established for the engine.

- For instance, in June 2023, Infineon Technologies AG launched its KP464 model of air pressure sensors, which is specifically designed for automotive engine control and management applications.

- Therefore, increasing developments related to automobile sensors for engine management and control applications are driving the automotive sensor market trends.

Advanced driver assistance systems segment is anticipated to register fastest CAGR growth during the forecast period.

- Advanced driver-assistance system (ADAS) is designed for assisting drivers with the safe operation of a vehicle.

- ADAS systems utilize automated technology involving sensors and cameras for detecting nearby obstacles or driver errors, and responding accordingly to avoid an accident.

- Automotive sensors are primarily used in advanced driver assistance systems for applications involving parking assistance, lane-keeping assistance, lane departure warning, adaptive cruise control, and blind spot detection among others.

- For instance, in October 2024, OMNIVISION launched its new OX12A10 model of CMOS image sensor. The new sensor improves automotive safety by providing enhanced resolution and image quality and it is ideal for use in vision cameras for advanced driver assistance systems (ADAS) and autonomous driving applications among others.

- Therefore, the rising advancements related to automobile sensors for use in ADAS applications are anticipated to boost the automotive sensor market growth during the forecast period.

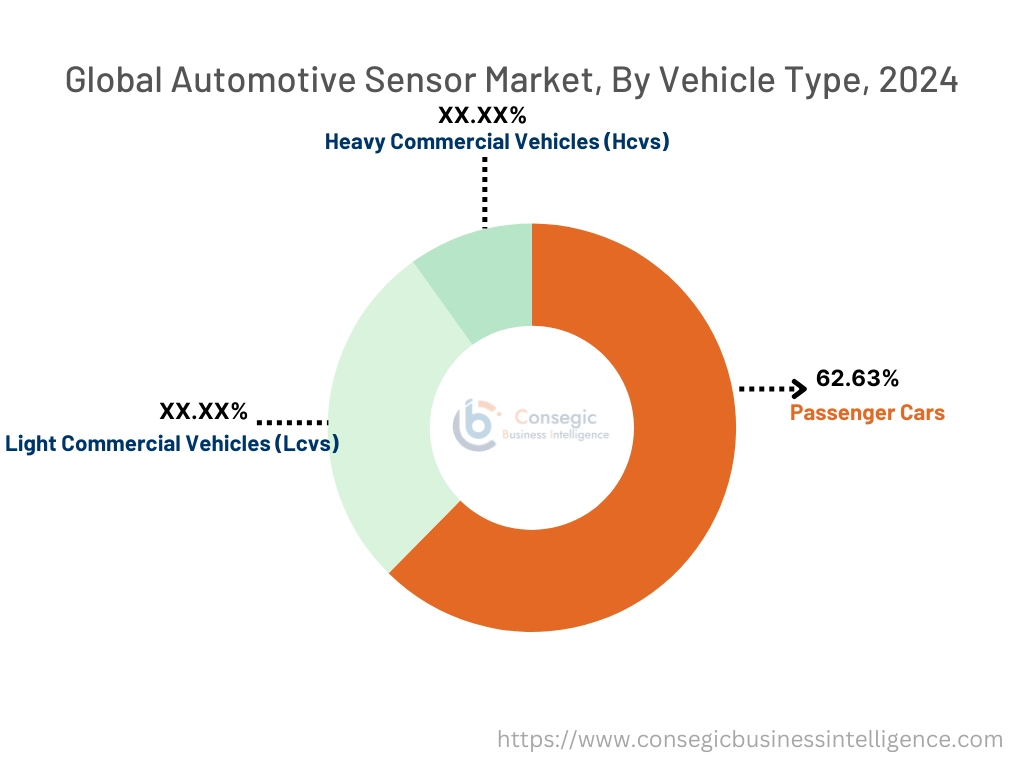

By Vehicle Type:

Based on the vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs).

Trends in the vehicle type:

- Factors including the rising disposable income, growing popularity of luxury cars, and progressions in autonomous driving systems are key aspects propelling the passenger cars segment.

- Factors including the rising sales of heavy-duty vehicles, growing investments in commercial vehicles, and increasing need for economical modes of transportation and logistics are primary determinants for driving the commercial vehicles segment.

Passenger cars segment accounted for the largest revenue share of 62.63% in the total market share in 2024, and it is anticipated to register substantial CAGR growth during the forecast period.

- Automobile sensors are primarily used in passenger cars for measuring a wide range of physical parameters that are crucial for smooth functioning of vehicle.

- Automobile sensors are integrated in passenger cars for monitoring various aspects of a vehicle, including its temperature, coolant system, engine, oil pressure, vehicle speed, emission levels, and others.

- Moreover, automobile sensors are used in passenger cars for application in safety systems, advanced driver assistance systems, engine management and control, and others.

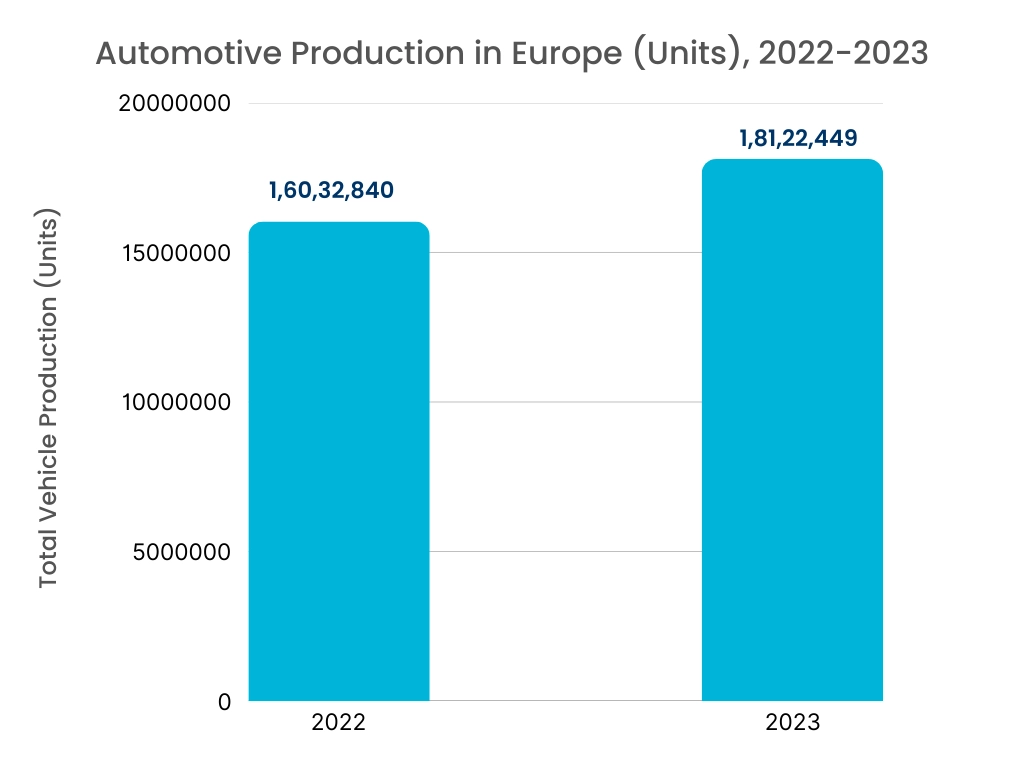

- For instance, according to the International Organization of Motor Vehicle Manufacturers, the total passenger car production in Europe reached up to 15,449,729 units in 2023, representing an increase of nearly 13% from 13,727,841 units in 2022.

- According to the analysis, the rising production of passenger cars is propelling the automotive sensor market trends.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

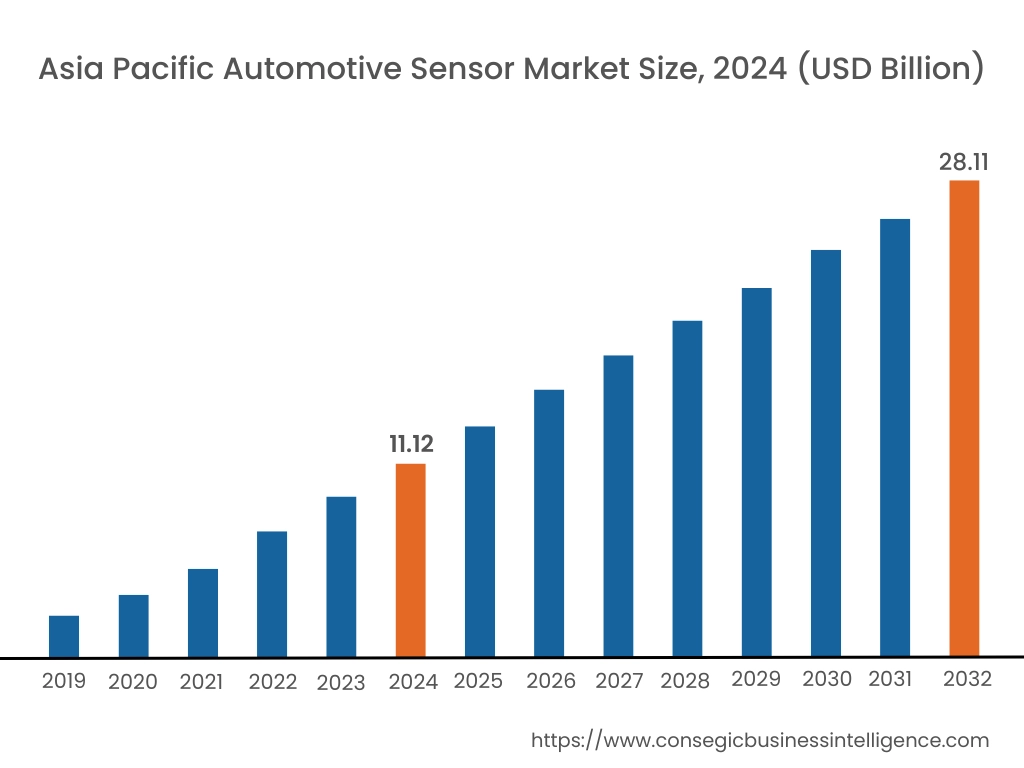

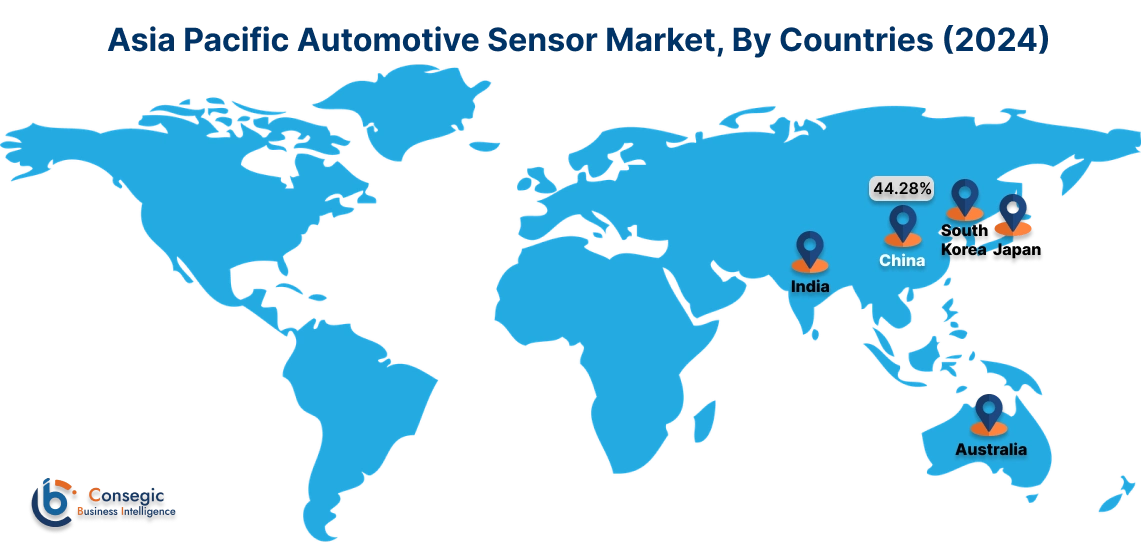

Asia Pacific region was valued at USD 11.12 Billion in 2024. Moreover, it is projected to grow by USD 12.29 Billion in 2025 and reach over USD 28.11 Billion by 2032. Out of this, China accounted for the maximum revenue share of 44.28%. As per the automotive sensor market analysis, the adoption of automobile sensors in the Asia-Pacific region is primarily driven by increasing government investments in automotive sector, rising automobile production, and increasing adoption of electric vehicles. Additionally, the rising advancements associated with passenger cars and increasing integration of advanced driver assistance system (ADAS) in modern vehicles are further accelerating the automotive sensor market expansion.

- For instance, according to the Society of Indian Automobile Manufacturers (SIAM), the total production of passenger cars in India reached 49,01,844 units during FY 2023-24, representing an incline of 7% in comparison to 45,87,116 units during FY 2022-23. The above factors are further propelling the market demand in the Asia-Pacific region.

North America is estimated to reach over USD 15.98 Billion by 2032 from a value of USD 6.49 Billion in 2024 and is projected to grow by USD 7.15 Billion in 2025. In North America, the growth of automotive sensor industry is driven by rising production of automobiles and increasing adoption of electric vehicles (EVs) in the region. Similarly, the rising advancements associated with autonomous vehicles are further contributing to the automotive sensor market demand.

- For instance, in October 2024, Tesla introduced the Cybercab, the company’s robotaxi, and also announced plans to commence autonomous driving of its Model 3 and Model Y cars in Texas and California states in the U.S in 2025. The above factors are projected to boost the market demand in North America during the forecast period.

Additionally, the regional analysis depicts that the increasing vehicle production, advent of electro mobility, and favorable government measures for integration of advanced driver assistance system in modern vehicles are propelling the automotive sensor market demand in Europe. Furthermore, as per the market analysis, the market demand in Latin America, Middle East, and African regions is expected to grow at a considerable rate due to factors such as growing automotive sector and increasing investments in electric vehicles among others.

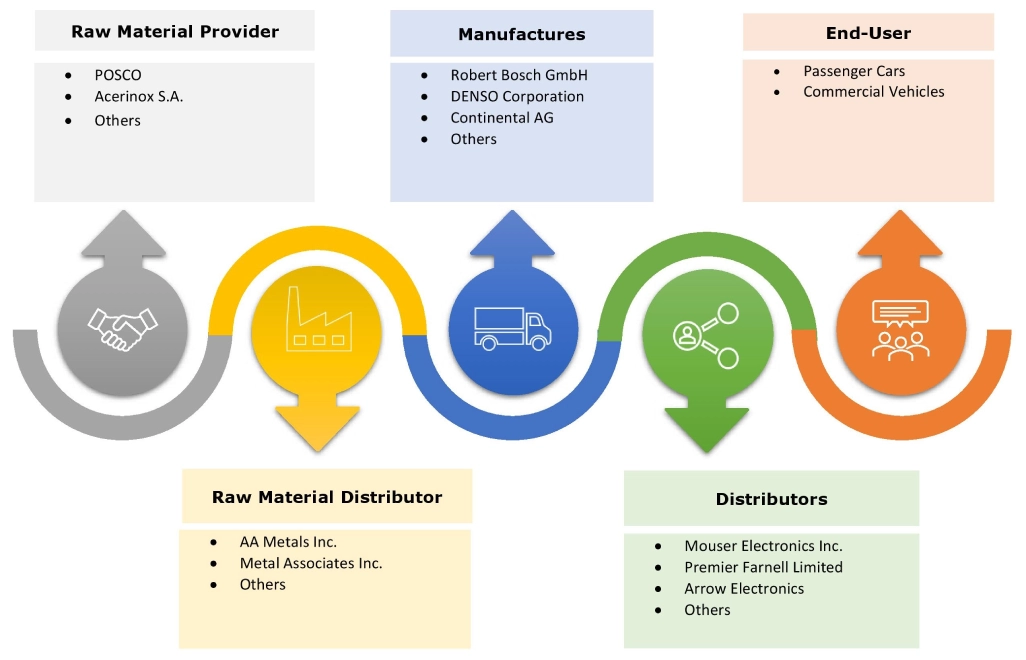

Top Key Players and Market Share Insights:

The global automotive sensor market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the automotive sensor market. Key players in the automotive sensor industry include-

- Robert Bosch GmbH (Germany)

- DENSO Corporation (Japan)

- Continental AG (Germany)

- Valeo (France)

- Sensata Technologies (U.S)

- Delphi Technologies (United Kingdom)

- STMicroelectronics N.V (Switzerland)

- Infineon Technologies AG (Germany)

- HELLA GmbH & Co. KGaA (Germany)

- CTS Corporation (U.S)

Recent Industry Developments :

Product Launch:

- In May 2024, NOVOSENSE launched its new NST175-Q1, NST86-Q1, NST235-Q1, and NST60-Q1 series of automotive temperature sensors. The temperature sensors feature high-reliability, high-performance, and high accuracy over a broad temperature range.

- In June 2023, Infineon Technologies AG launched its KP464 model of air pressure sensors. The pressure sensors are designed for automotive engine control and management applications among others.

Automotive Sensor Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 63.91 Billion |

| CAGR (2025-2032) | 13.3% |

| By Type |

|

| By Sales Channel |

|

| By Application |

|

| By Vehicle Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the automotive sensor market? +

The automotive sensor market was valued at USD 25.86 Billion in 2024 and is projected to grow to USD 63.91 Billion by 2032.

Which is the fastest-growing region in the automotive sensor market? +

Asia-Pacific is the region experiencing the most rapid growth in the automotive sensor market.

What specific segmentation details are covered in the automotive sensor report? +

The automotive sensor report includes specific segmentation details for type, sales channel, application, vehicle type, and region.

Who are the major players in the automotive sensor market? +

The key participants in the automotive sensor market are Robert Bosch GmbH (Germany), DENSO Corporation (Japan), Continental AG (Germany), Valeo (France), Sensata Technologies (U.S), Delphi Technologies (United Kingdom), STMicroelectronics N.V (Switzerland), Infineon Technologies AG (Germany), HELLA GmbH & Co. KGaA (Germany), CTS Corporation (U.S), and others.