- Summary

- Table Of Content

- Methodology

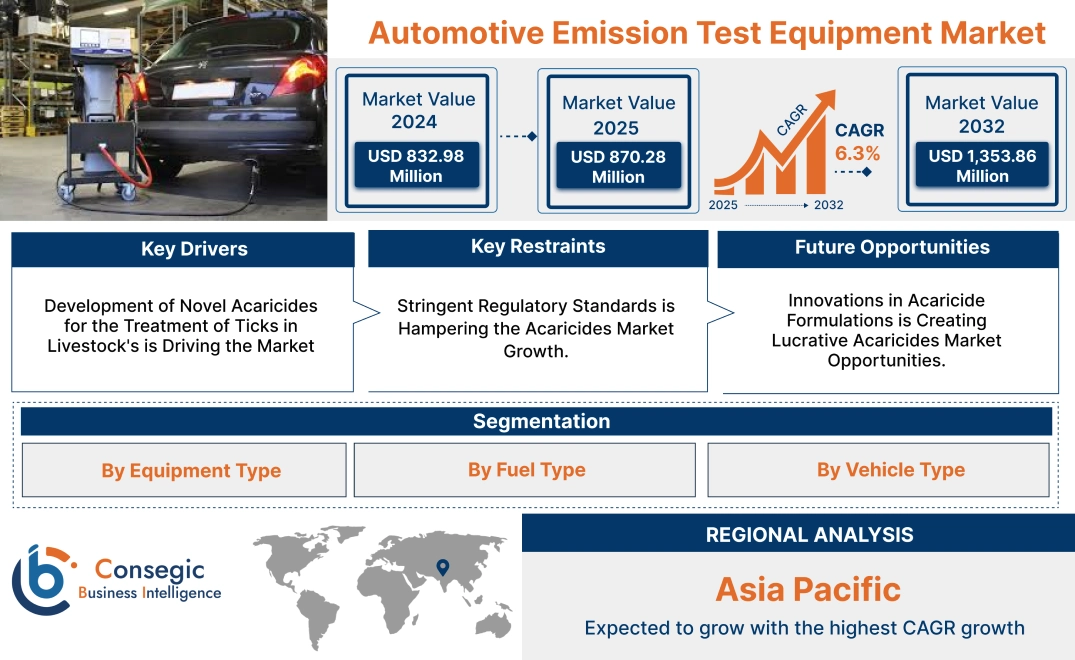

Automotive Emission Test Equipment Market Size:

Automotive Emission Test Equipment Market size is estimated to reach over USD 1,353.86 Million by 2032 from a value of USD 832.98 Million in 2024 and is projected to grow by USD 870.28 Million in 2025, growing at a CAGR of 6.3% from 2025 to 2032.

Automotive Emission Test Equipment Market Scope & Overview:

Automotive emission test equipment is used to measure and analyze the level of pollutants emitted by vehicles to ensure compliance with environmental regulations. These systems assess exhaust gases such as carbon monoxide, nitrogen oxides, and hydrocarbons to determine the efficiency of emission control technologies in internal combustion engines. They are widely utilized in vehicle inspection centers, research laboratories, and manufacturing facilities.

This equipment includes gas analyzers, smoke meters, dynamometers, and onboard diagnostic (OBD) systems, each designed to evaluate different aspects of vehicle emissions. Advanced models integrate software for real-time data monitoring, automated testing, and reporting to improve accuracy and efficiency. These systems are compatible with various vehicle types, including passenger cars, commercial trucks, and off-road vehicles, ensuring comprehensive emissions assessment across the automotive industry.

End-users include regulatory agencies, automotive manufacturers, and testing service providers that require reliable solutions for monitoring and controlling vehicle emissions. Automotive emission test equipment plays a critical role in maintaining air quality standards and ensuring compliance with regulatory frameworks.

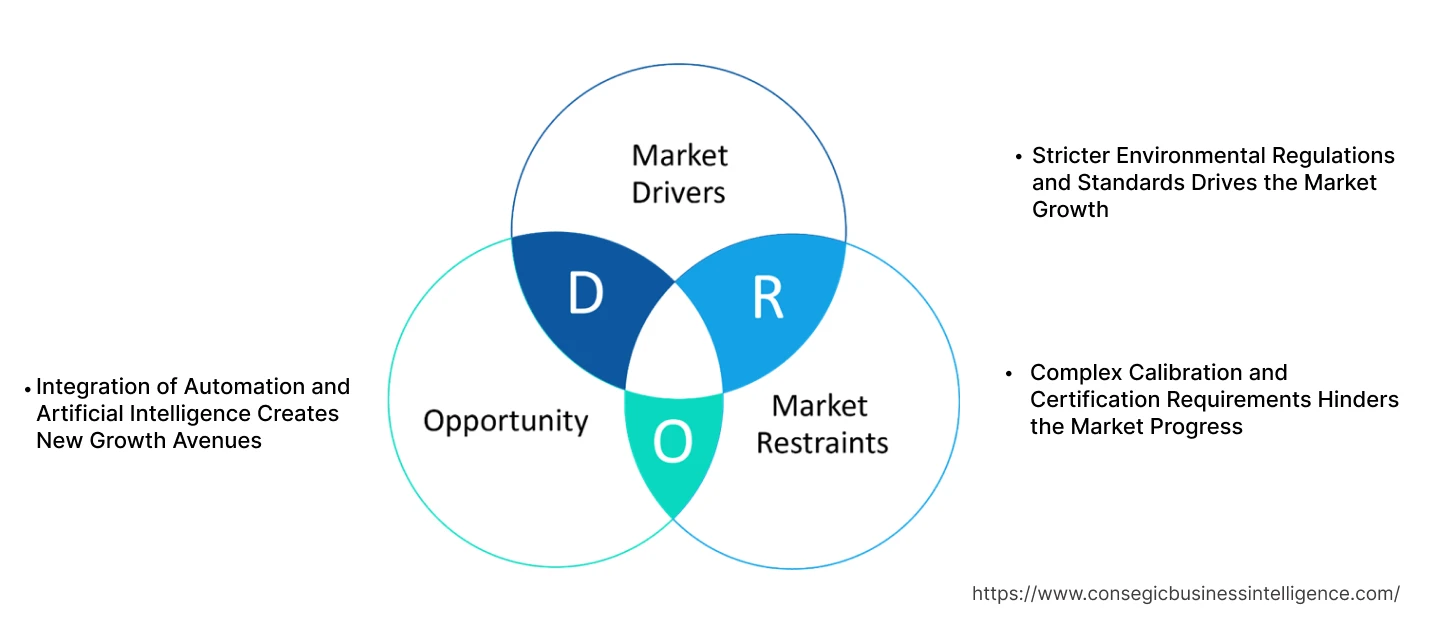

Automotive Emission Test Equipment Market Dynamics - (DRO) :

Key Drivers:

Stricter Environmental Regulations and Standards Drives the Market Growth

The growing demand for cleaner air and the tightening of environmental regulations worldwide are significantly driving the adoption of advanced emission testing equipment. As governments implement stricter emissions standards, manufacturers are required to ensure that their vehicles meet precise emission levels to comply with regulatory frameworks. These regulations aim to reduce pollution and limit the environmental impact of vehicles, particularly in urban areas where air quality is a major concern. As standards evolve and become more stringent, the need for accurate and reliable emission testing systems increases, accelerating market growth. Manufacturers must adopt advanced equipment to measure and monitor emissions more effectively, ensuring compliance with both local and international standards. This regulatory pressure is pushing the automotive industry to invest in state-of-the-art testing solutions, creating a significant demand for advanced emission testing technologies that accurately assess and manage vehicle emissions. Thus, the above factors are fueling the automotive emission test equipment market growth.

Key Restraints:

Complex Calibration and Certification Requirements Hinders the Market Progress

To meet the stringent standards set by regulatory authorities, equipment must undergo precise calibration and certification procedures, ensuring it provides accurate results for emissions testing. This process often involves multiple testing phases, paperwork, and compliance checks, which extends the timeline for deploying new equipment. The complexity of these procedures increases operational costs, particularly for smaller companies or those with limited resources, which struggle to meet regulatory requirements. As a result, smaller businesses hesitate to invest in advanced testing systems, limiting their market reach. The high costs and long timelines associated with calibration and certification also deter some businesses from adopting these solutions, slowing the automotive emission test equipment market demand and making it challenging for new entrants.

Future Opportunities :

Integration of Automation and Artificial Intelligence Creates New Growth Avenues

The integration of automation and artificial intelligence (AI) into emissions testing systems enhances efficiency and reduces costs. Automated systems streamline the testing process by eliminating manual interventions, leading to faster results and more consistent performance. AI-driven data analytics enhance accuracy by analyzing large volumes of data in real time, identifying patterns, and providing deeper insights into vehicle emissions. These advanced systems not only improve the precision of test results but also help optimize testing procedures, reducing the risk of human error. The ability to process and analyze data in real time allows for quicker decision-making and immediate adjustments, improving operational efficiency in both production and regulatory settings. As a result, businesses benefit from lower operational costs, enhanced productivity, and the ability to meet increasingly stringent environmental regulations, making automated and AI-integrated solutions highly attractive and boosting the overall automotive emission test equipment market expansion.

Automotive Emission Test Equipment Market Segmental Analysis :

By Equipment Type:

Based on equipment type, the market is segmented into opacity meters, smoke meters, CO and CO₂ analyzers, NOₓ analyzers, and others.

The CO and CO₂ analyzers segment accounted for the largest revenue of the total automotive emission test equipment market share in 2024.

- CO and CO₂ analyzers play a crucial role in assessing vehicle emissions and ensuring compliance with environmental regulations, particularly in passenger and commercial vehicles.

- These analyzers are widely integrated into emission testing stations due to their ability to measure carbon monoxide and carbon dioxide concentrations with high accuracy.

- Governments and regulatory bodies emphasize stringent emission norms, driving the use of CO and CO₂ analyzers in routine vehicle inspections.

- As per automotive emission test equipment market analysis, ongoing advancements in gas sensor technology and real-time monitoring capabilities enhance the efficiency and reliability of CO and CO₂ analyzers in emission testing.

The NOₓ analyzers segment is anticipated to witness the fastest CAGR during the forecast period.

- NOₓ emissions are a major contributor to air pollution, necessitating stringent testing standards for diesel and gasoline-powered vehicles.

- The increasing use of selective catalytic reduction (SCR) technology in vehicles has elevated the need for precise NOₓ measurement, ensuring compliance with emission standards.

- These analyzers are extensively used in laboratory settings and mobile emission testing units to assess nitrogen oxide levels under real-world driving conditions.

- As per automotive emission test equipment market trends, advancements in sensor-based NOₓ detection technologies are expected to improve testing accuracy and facilitate compliance with evolving regulatory frameworks.

By Fuel Type:

Based on fuel type, the market is segmented into gasoline, diesel, ethanol, compressed natural gas (CNG), and electricity.

The gasoline segment accounted for the largest revenue of the total automotive emission test equipment market share in 2024.

- Gasoline-powered vehicles represent a significant portion of the global vehicle fleet, making emission testing for this category a priority for regulatory agencies.

- Emission test equipment for gasoline engines focuses on measuring pollutants such as carbon monoxide (CO), hydrocarbons (HC), and nitrogen oxides (NOₓ) to ensure compliance with environmental standards.

- The adoption of advanced fuel injection and catalytic converter technologies in gasoline vehicles has increased the need for accurate emission monitoring systems.

- Thus, as per the market trends, regulatory frameworks targeting reductions in fuel-based emissions have driven the integration of advanced diagnostic tools in gasoline vehicle emission testing, fueling the automotive emission test equipment market demand.

The electricity segment is anticipated to witness the fastest CAGR during the forecast period.

- While fully electric vehicles (EVs) produce zero tailpipe emissions, hybrid electric vehicles (HEVs) require emission testing to assess fuel combustion efficiency and battery integration.

- Regulatory bodies emphasize the evaluation of hybrid powertrains, necessitating the development of emission test equipment that can analyze both fuel combustion and battery efficiency.

- The implementation of real-world driving emission (RDE) standards for hybrid and plug-in hybrid vehicles is prompting automakers to integrate enhanced emission monitoring systems.

- Therefore, the market trends shows that the transition toward electrification in the automotive sector is influencing the development of hybrid-specific emission testing technologies, creating significant automotive emission test equipment market opportunities.

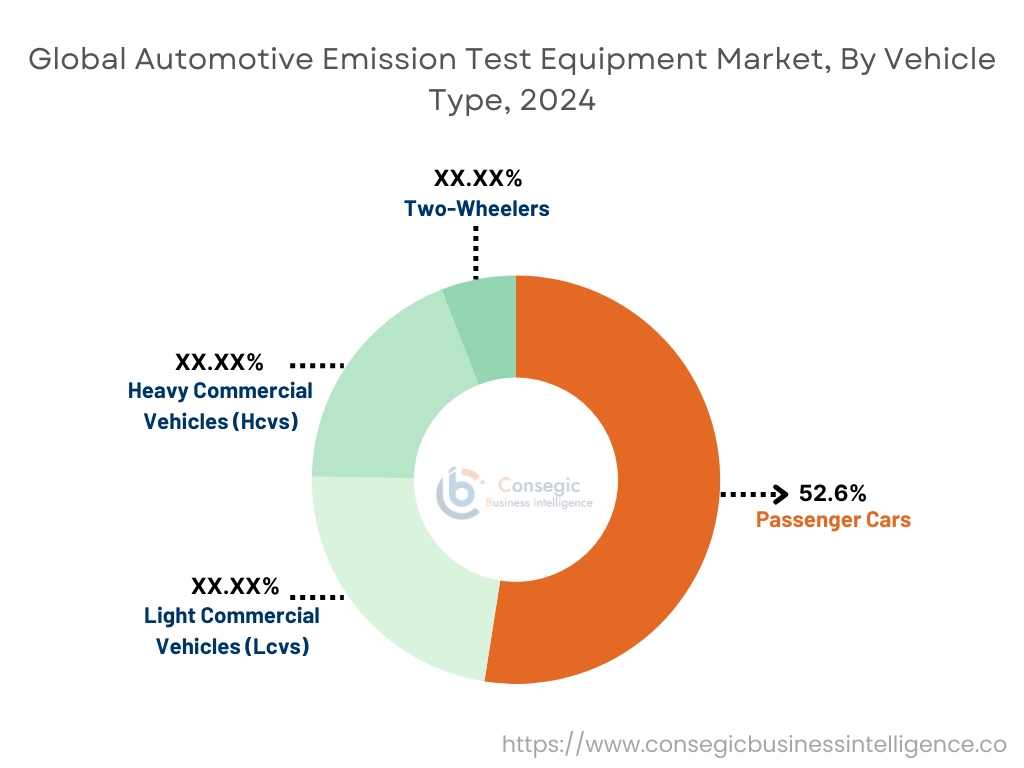

By Vehicle Type:

Based on vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and two-wheelers.

The passenger cars segment accounted for the largest revenue OF 52.6% share in 2024.

- Passenger cars are subject to strict emission regulations worldwide, requiring periodic testing to ensure compliance with fuel efficiency and environmental standards.

- Governments mandate emission testing programs for passenger vehicles, particularly in urban areas with high air pollution levels, driving the adoption of advanced testing systems.

- The increasing use of hybrid and turbocharged gasoline engines in passenger cars has heightened the need for precise emission test equipment capable of detecting complex pollutants.

- As per automotive emission test equipment market analysis, emission testing for passenger cars continues to evolve with the introduction of real-time monitoring solutions and connected diagnostic tools.

The heavy commercial vehicles (HCVs) segment is anticipated to witness the fastest CAGR during the forecast period.

- HCVs, including trucks and buses, contribute significantly to global emissions, necessitating stringent testing measures to control particulate matter (PM) and NOₓ levels.

- Diesel-powered commercial vehicles are subject to periodic emission testing, particularly in logistics and transportation sectors, where fuel efficiency and regulatory compliance are critical.

- The integration of portable emission measurement systems (PEMS) in HCV testing allows for real-world emissions assessment, improving the accuracy of compliance reporting.

- As per automotive emission test equipment market trends, governments are enforcing stricter emission norms for commercial fleets, leading to increased adoption of advanced emission testing technologies in heavy-duty vehicles.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

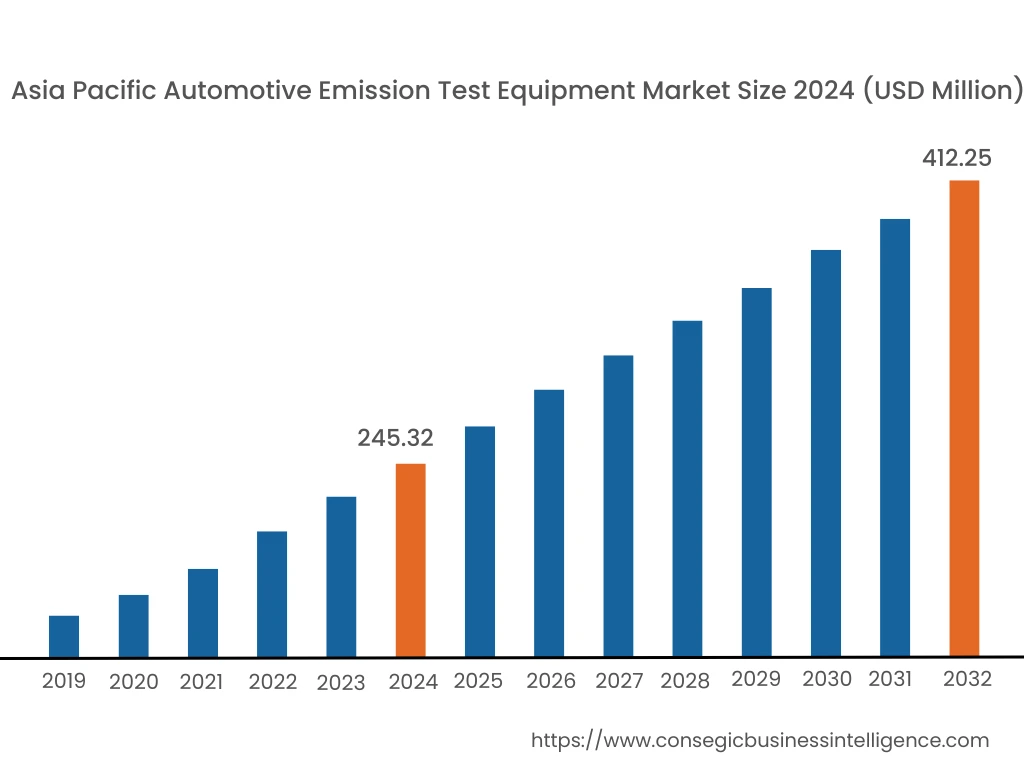

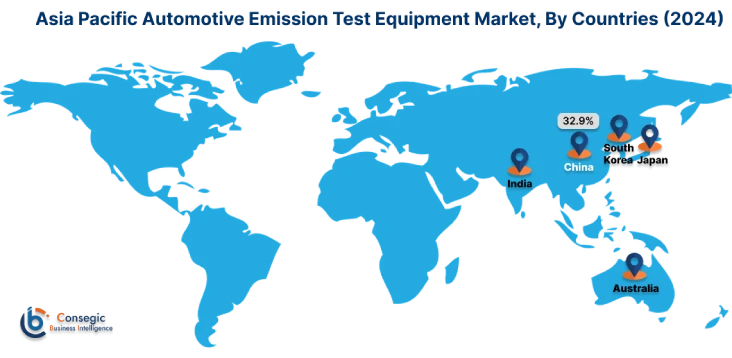

Asia Pacific region was valued at USD 245.32 Million in 2024. Moreover, it is projected to grow by USD 257.03 Million in 2025 and reach over USD 412.25 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.9%. The Asia-Pacific region holds a prominent share in the market and is witnessing rapid industrialization and urbanization, leading to increased vehicle production and usage. A prominent trend is the implementation of emission testing equipment to monitor and control vehicular emissions in densely populated urban centers. Analysis indicates that government initiatives aimed at curbing air pollution and the burgeoning automotive sector are significant factors influencing the automotive emission test equipment market opportunities in this region.

North America is estimated to reach over USD 438.79 Million by 2032 from a value of USD 276.31 Million in 2024 and is projected to grow by USD 288.13 Million in 2025. In this region, stringent environmental regulations have led to a heightened focus on vehicle emissions testing. A notable trend is the adoption of advanced emission testing technologies to ensure compliance with federal and state standards. Analysis indicates that the presence of established automotive industries and a proactive regulatory environment contribute to the demand for sophisticated emission test equipment.

European countries are at the forefront of implementing rigorous emission standards, particularly in the wake of environmental concerns. A significant trend is the integration of advanced emission testing protocols to meet the stringent Euro emission norms. Analysis suggests that the region's commitment to reducing vehicular pollution and adherence to strict regulatory frameworks are key drivers boosting the automotive emission test equipment market expansion.

In the Middle East and Africa, the automotive emission test equipment market is shaped by a growth in awareness of environmental issues and the need to comply with international emission standards. The focus is on establishing emission testing facilities to regulate and monitor vehicle emissions effectively. Analysis suggests that collaborations with international organizations and the adoption of global best practices are contributing to the market's growth in these regions.

Latin American countries are increasingly recognizing the importance of controlling vehicular emissions to address environmental and public health concerns. A notable trend is the enhancement of emission testing infrastructure to enforce compliance with emerging emission regulations. Analysis indicates that regional efforts to improve air quality and align with international environmental standards are key factors driving the automotive emission test equipment market growth.

Top Key Players and Market Share Insights:

The Automotive Emission Test Equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Automotive Emission Test Equipment market. Key players in the Automotive Emission Test Equipment industry include –

- Opus Inspection, Inc. (USA)

- AVL List GmbH (Austria)

- TEXA S.p.A. (Italy)

- TÜV Nord Group (Germany)

- ETAS GmbH (Germany)

- Applus+ (Spain)

- HORIBA, Ltd. (Japan)

- CAPELEC (France)

- GEMCO Equipment Ltd. (UK)

- SGS SA (Switzerland)

Automotive Emission Test Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,353.86 Million |

| CAGR (2025-2032) | 6.3% |

| By Equipment Type |

|

| By Fuel Type |

|

| By Vehicle Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Automotive Emission Test Equipment Market? +

The Automotive Emission Test Equipment Market size is estimated to reach over USD 1,353.86 Million by 2032 from a value of USD 832.98 Million in 2024 and is projected to grow by USD 870.28 Million in 2025, growing at a CAGR of 6.3% from 2025 to 2032.

What is the size of the Automotive Emission Test Equipment Market? +

The Automotive Emission Test Equipment Market size is estimated to reach over USD 1,353.86 Million by 2032 from a value of USD 832.98 Million in 2024 and is projected to grow by USD 870.28 Million in 2025, growing at a CAGR of 6.3% from 2025 to 2032.