- Summary

- Table Of Content

- Methodology

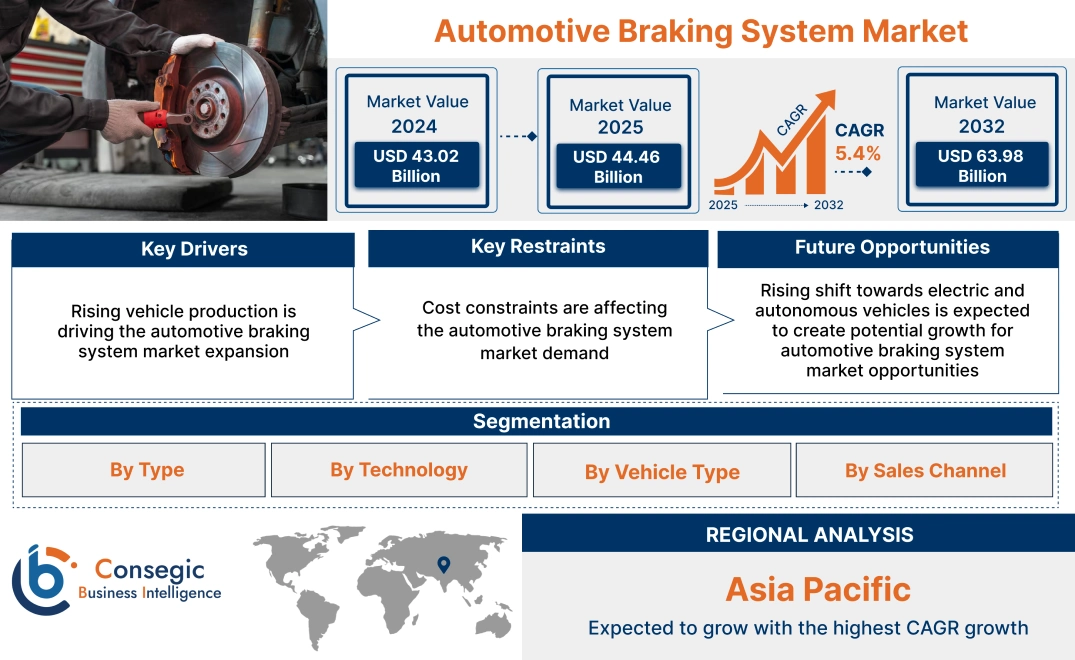

Automotive Braking System Market Size:

Automotive Braking System Market Size is estimated to reach over USD 63.98 Billion by 2032 from a value of USD 43.02 Billion in 2024 and is projected to grow by USD 44.46 Billion in 2025, growing at a CAGR of 5.4% from 2025 to 2032.

Automotive Braking System Market Scope & Overview:

Automotive braking system plays a crucial role in vehicle safety, providing drivers with the ability to decelerate and stop their vehicles effectively, thereby preventing accidents and saving lives. Beyond safety, modern brake systems also contribute to driving comfort and performance, offering responsive braking, reduced stopping distances, and enhanced control in various driving conditions. Manufacturers are increasingly integrating sensors, actuators, and electronic control units (ECUs) to develop intelligent automotive braking systems capable of adaptive responses to varying driving conditions. Moreover, the proliferation of electric and hybrid vehicles has fueled the demand for regenerative braking systems, enabling energy recuperation during deceleration and contributing to overall vehicle efficiency.

Automotive Braking System Market Dynamics - (DRO) :

Key Drivers:

Rising vehicle production is driving the automotive braking system market expansion

The growth in global vehicle production is a significant driver for the global market, with increasing urbanization playing a crucial role. As more people move to urban areas, the demand for personal transportation rises, leading to a surge in vehicle ownership. This trend is particularly evident in emerging economies where rapid urbanization is accompanied by an expanding middle class with rising disposable incomes. With more vehicles on the road, there is a heightened need for reliable braking systems to ensure safe operation and mitigate the risks associated with increased traffic density and congestion in urban environments.

Further, the rising disposable incomes contribute to the need for higher-quality vehicles equipped with advanced safety features, including state-of-the-art braking systems. Consumers are increasingly willing to invest in vehicles that offer superior performance, comfort, and safety, thereby driving the need for braking systems.

- For instance, in March 2024, Tata Motors has signed a Memorandum of Understanding (MoU) with Tamil Nadu government, to set-up an automobile manufacturing facility in the state. This MoU enables Tata Motors to commence the production of vehicles. The MoU stated an investment of USD 1,081.6 million over 5 years.

Thus, according to the automotive braking system market analysis, the growing vehicle production is driving the automotive braking system market size.

Key Restraints:

Cost constraints are affecting the automotive braking system market demand

The cost associated with developing and implementing advanced braking technologies represents a significant restraint for the automotive braking system. Innovations such as electronic brake systems (EBS), anti-lock braking systems (ABS), and regenerative braking systems (RBS) require substantial research and development investments to conceptualize, design, and validate new technologies. Additionally, manufacturers are investing in upgrading manufacturing processes, acquiring specialized equipment, and sourcing high-quality materials to produce these advanced brake systems efficiently. These upfront costs can be significant, specifically for smaller manufacturers with limited financial resources, while imposing a barrier to entry and innovation within the market. Thus, the above analysis depicts that the aforementioned factors would further hamper the automotive braking system market size.

Future Opportunities :

Rising shift towards electric and autonomous vehicles is expected to create potential growth for automotive braking system market opportunities

The transition towards electric and autonomous vehicles presents a transformative prospect for the global market. Electric vehicles (EVs) are characterized by their emphasis on energy efficiency and sustainability, require specialized braking systems tailored to their unique operational characteristics. This necessitates the development of automotive braking systems optimized for regenerative braking, capable of seamlessly transitioning between traditional friction braking and regenerative braking modes to optimize overall braking performance and efficiency.

Further, the proliferation of autonomous driving technologies represents a paradigm shift in vehicle control systems, requiring advanced braking systems capable of integration and collaboration with autonomous vehicle platforms. Autonomous driving technologies rely on a complex network of sensors, cameras, and artificial intelligence algorithms to perceive and interpret the surrounding environment, necessitating braking systems with adaptive responses to varying driving conditions. By leveraging predictive analytics and real-time data processing capabilities, advanced braking systems can anticipate changes in road conditions, traffic patterns, and vehicle dynamics, enabling proactive interventions to ensure safe and reliable vehicle operation in autonomous driving scenarios.

- For instance, in June 2022, Bosch unveiled advanced brake systems for electric and hybrid vehicles, which features regenerative braking capabilities, such as iBooster and ESP, to increase vehicle range and reduce environmental impact of braking systems.

Thus, based on the automotive braking system market analysis, the growing advancement in the automotive sector is expected to drive the automotive braking system market opportunities.

Automotive Braking System Market Segmental Analysis :

By Type:

Based on type, the automotive braking system market is segmented into disc brakes and drum brakes.

Trends in type:

- The emergence of autonomous driving technologies is creating lucrative opportunities for braking system manufacturers necessitating seamless integration with vehicle control systems to ensure reliable performance in automated driving scenarios.

- By developing advanced brake systems optimized for ADAS applications, manufacturers can differentiate themselves in a competitive market landscape, enhance their value proposition to OEMs and consumers, and position themselves as key enablers of vehicle safety and performance in the connected and autonomous mobility.

- Thus, based on the above factors, the aforementioned developments are driving the automotive braking system market demand.

The disc brakes segment accounted for the largest revenue in the year 2024.

- Disc brakes offer shorter stopping distances, better control, and improved performance under various driving conditions, making them essential components for ensuring vehicle safety.

- Disc brakes offer superior stopping power and heat dissipation, which are ideal for electric and hybrid vehicles operating under demanding conditions.

- Their design allows for efficient heat dissipation, reducing the risk of brake fade during prolonged or heavy braking, making disc brakes particularly suitable for demanding driving conditions and high-speed applications.

- There is a growing emphasis on the integration of smart technologies into disc brake systems. R&D initiatives are centered on incorporating sensors and electronic control units (ECUs) to enable features such as predictive maintenance, autonomous emergency braking, and regenerative braking.

- For instance, in June 2023, EBC Brakes introduced fully-floating two-piece discs high-performance brake pad options for GB7 BMW M2. With this launch, the company will provide aftermarket performance components for vehicles, while enhancing the driving experience.

- Thus, based on the above analysis, these developments and trends are further driving the automotive braking system market growth.

The drum brakes segment is anticipated to register the fastest CAGR during the forecast period.

- Drum brakes represent a traditional braking technology that remains relevant in various vehicle segments, particularly in rear-wheel braking systems and certain entry-level vehicles.

- Drum brakes feature brake shoes housed inside a cylindrical drum, which expand outward to create friction against the drum's inner surface when the brake pedal is applied.

- While drum brakes generally exhibit lower stopping power and heat dissipation capabilities compared to disc brakes, they are valued for their simplicity, durability, and cost-effectiveness.

- Drum brakes are often favoured for their reliable performance in less demanding driving scenarios and as parking brakes due to their inherent self-applying nature.

- Thus, above factors are expected to drive the automotive braking system market share during the forecast period.

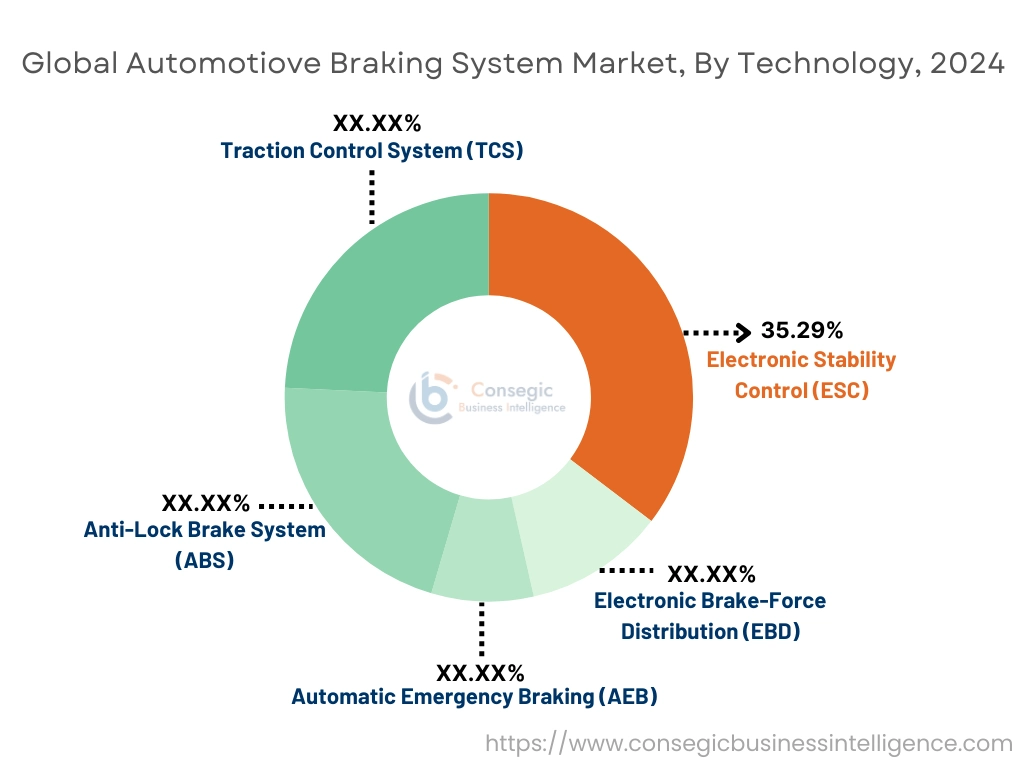

By Technology:

Based on technology, the automotive braking system market is segmented into anti-lock brake system (ABS), traction control system (TCS), electronic stability control (ESC), electronic brake-force distribution (EBD), and automatic emergency braking (AEB).

Trends in technology:

- As ADAS functionalities become standard features in modern vehicles, the need for advanced brake systems capable of supporting the technologies is expected to grow, driving further innovation and investment in the global market.

- Brake system manufacturers are developing advanced brake-by-wire and brake control systems equipped with predictive algorithms and sensor fusion technology to ensure precise and responsive braking performance in autonomous driving scenarios.

The electronic stability control (ESC) segment accounted for the largest revenue share of 35.29% in the year 2024.

- Electronic stability control (ESC) is an advanced safety feature that helps prevent skidding and loss of control by automatically applying brakes to individual wheels when it detects a loss of traction.

- ESC is widely recognized for its effectiveness in preventing accidents caused by oversteering or understeering, especially in emergency manoeuvres or adverse road conditions. As a result, ESC is increasingly becoming a standard feature in new vehicles, particularly in regions with stringent safety regulations.

- The growing focus on vehicle safety and consumer need for enhanced protection has driven the adoption of ESC, with many manufacturers now offering it as a standard or optional feature in a wide range of vehicles including passenger and commercial vehicles.

- For instance, in June 2022, Maruti Suzuki launched its Brezza, which is equipped with advanced safety features, such as ESC system, ABS with EBD, and others.

- As per the analysis, these developments in the ECS segment are driving the automotive braking system market growth.

The traction control system (TCS) segment is anticipated to register the fastest CAGR during the forecast period.

- Traction control system (TCS) works together with ABS to improve vehicle stability by preventing wheel spin during acceleration, particularly on slippery surfaces.

- These systems are crucial for ensuring that power is transferred efficiently to the road, especially in low-traction environments such as snow, ice, or mud.

- TCS is increasingly being integrated into passenger cars, light commercial vehicles, and even electric vehicles (EVs) as part of the growing trend of advanced driver-assistance systems (ADAS).

- These developments in the TCS segment are anticipated to further drive the automotive braking system market trends during the forecast period.

By Vehicle Type:

Based on vehicle type, the automotive braking system market is segmented into passenger vehicles and commercial vehicles.

Trends in vehicle type:

- The development of the global automotive sector directly influences the need for advanced automotive products and solutions. The rise in vehicle production across all segments leads to an increased need for original equipment and replacement parts including brakes.

- Older vehicles tend to experience greater wear and tear, resulting in an increased probability of requiring advanced braking systems. This factor drives a consistent need for replacement parts in the aftermarket.

The passenger vehicles segment accounted for the largest revenue share in the year 2024.

- The passenger vehicle segment has witnessed a significant shift towards electric vehicles (EVs) as part of the broader transition to cleaner, more sustainable energy sources.

- Consumers are increasingly opting for EVs due to their lower environmental impact, reduced fuel costs, and improved performance. This transition is also supported by governments worldwide, which are introducing stricter emission standards and offering incentives for electric car buyers.

- The increased availability of financing options and the development of affordable vehicle models are making passenger vehicles more accessible to a broader consumer base. As a result, automakers are adapting their strategies to cater to the diverse needs of consumers in these high-growth markets, including offering affordable, fuel-efficient, and compact vehicles.

- For instance, in February 2024, Brembo Brakes unveiled the Brembo Carbon Braking System in collaboration with the Bugatti Bolide. The unique carbon brakes allow the 1,825-horsepower vehicle to hit the speed over 300 mph.

- As per the analysis, these developments in the passenger vehicle segment are driving the automotive engine market growth.

The commercial vehicles segment is anticipated to register the fastest CAGR during the forecast period.

- Governments around the world are implementing increasingly stringent emissions standards, such as Euro VI in Europe and EPA regulations in the United States, to curb air pollution and mitigate the environmental impact of commercial vehicles. These regulations mandate the adoption of cleaner engine technologies, advanced brake systems, better exhaust after treatment systems, and alternative fuels to reduce emissions of harmful pollutants such as particulate matter (PM), nitrogen oxides (NOx), and greenhouse gases (GHGs).

- Manufacturers are investing in research and development to develop and commercialize electric vehicles, hybrid drivetrains, natural gas engines, and hydrogen fuel cell technologies to comply with emissions regulations and meet customer needs for cleaner and sustainable transportation solutions.

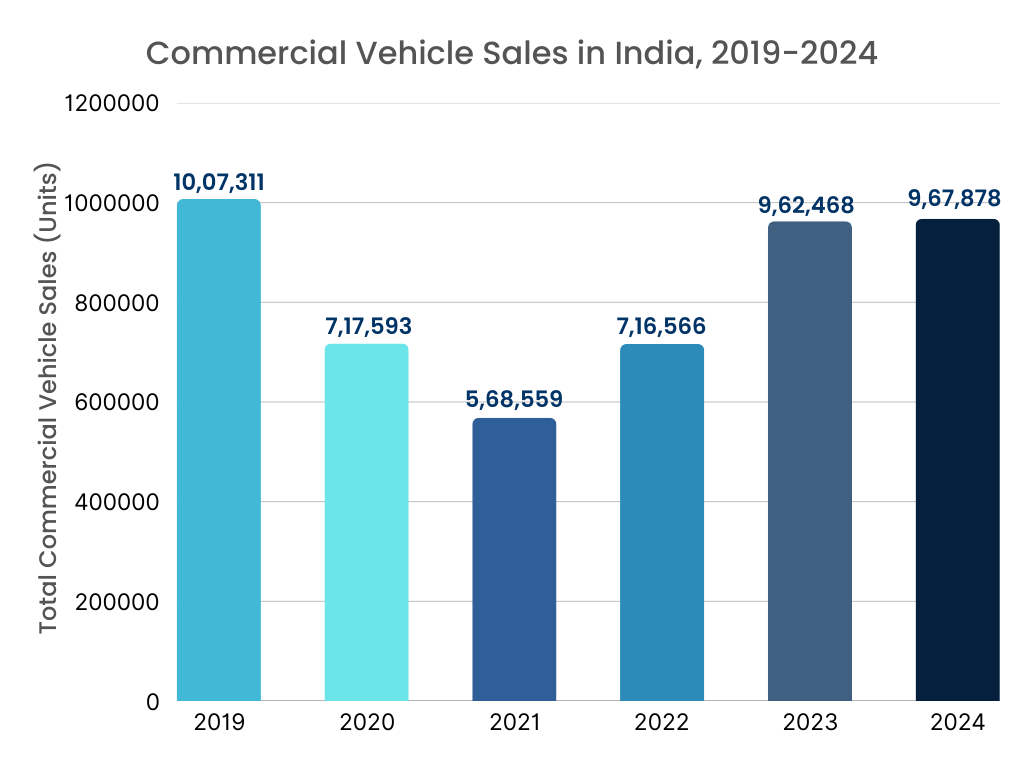

- For instance, According to Society of Indian Automobile Manufacturers (SIAM), the commercial vehicle sales in India increased from 9,62,468 units to 9,67,878 units. In addition to this, the sales of medium and heavy commercial vehicles increased from 3,59,000 units to 3,73,000 units while sales of light commercial vehicles decreased from 6,03,000 units to 5,95,000 units in fiscal year 2023-24.

- Thus, above analysis and factors are expected to drive the automotive braking system market trends during the forecast period.

By Sales Channel:

Based on sales channel, the market is segmented into original equipment manufacturers (OEMs) and aftermarket.

Trends in sales channel:

- Online sales platforms are becoming increasingly prominent, providing convenient access to a diverse action of automotive products for consumer and repair shops. These factors are further are disrupting the traditional distribution channels.

- Both OEMs and aftermarket suppliers are placing greater emphasis on quality and reliability. This sift is influenced by customer expectations and the necessity to uphold vehicle safety and performance.

The OEMs segment accounted for the largest revenue share in the year 2024.

- OEMs, which include vehicle manufacturers, are pivotal in the initial integration of braking systems into new vehicles throughout the production process. These collaborations with OEMs typically involve long-term contracts to guarantee the integration of braking systems that comply with rigorous quality standards and specifications.

- The OEM segment gains from the consistent requirement for automotive products, fuelled by rising vehicle production volumes and the ongoing necessity for suspension components that promote vehicle safety, stability, and performance.

- Technological innovations in suspension systems and an increasing focus on driving comfort further enhance the need for high-quality braking systems from OEMs.

- Thus, rise in technological innovations would further drive the global market trends.

The aftermarket segment is anticipated to register the fastest CAGR during the forecast period.

- The aftermarket segment is driven by factors including vehicle age, wear and tear, and the necessity for component replacements due to damage or malfunction. As vehicles age and increase mileage, components like suspension parts and brake systems may experience wear and need replacement to ensure optimal vehicle performance and safety.

- In this segment, a varied ecosystem of distributors, retailers, and e-commerce platforms primarily facilitates the distribution and sale of braking systems to end consumers. These channels provide a broad selection of automotive products, accommodating different vehicle makes and models as well as the budgetary needs of vehicle owners.

- Aftermarket suppliers frequently emphasize value-added services such as product warranties, technical support, and installation assistance to distinguish themselves in a competitive market environment.

- As the automotive industry continues to evolve, aftermarket sales channel expected to remain essential contributor to the continued development and innovation within the global market share.

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

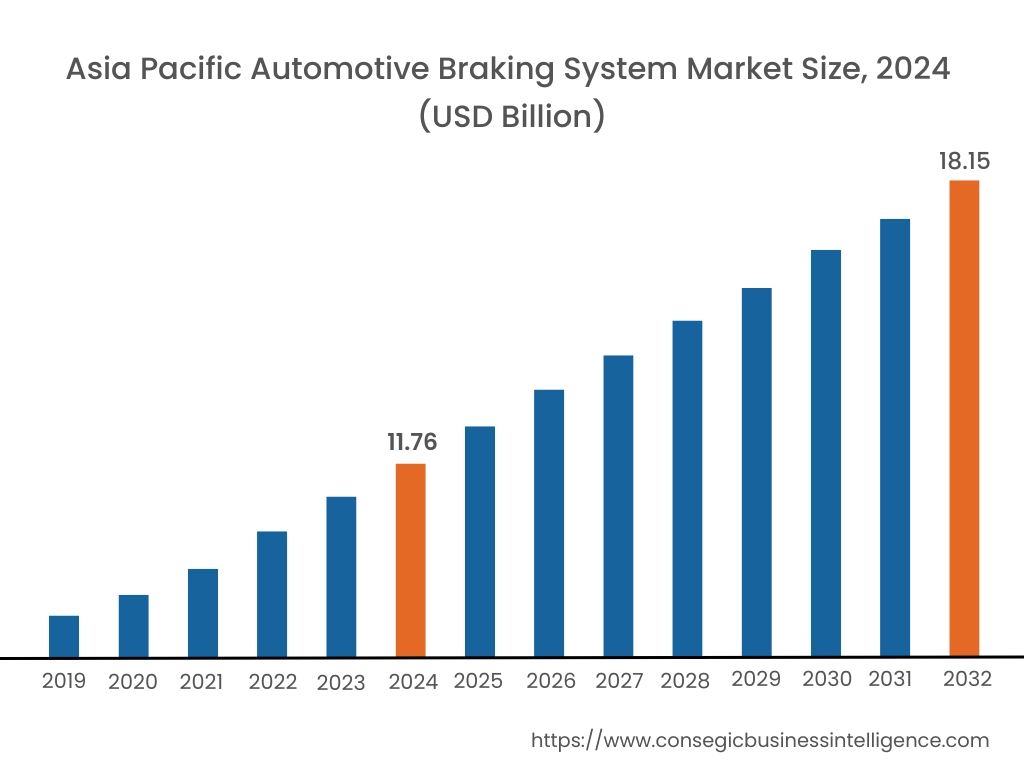

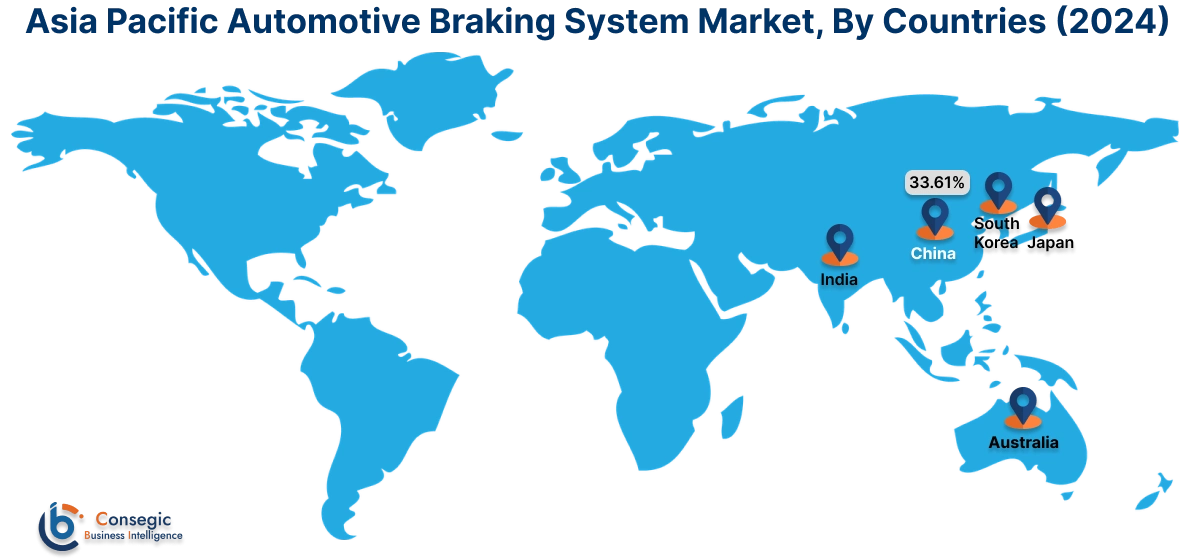

Asia Pacific automotive braking system market expansion is estimated to reach over USD 18.15 billion by 2032 from a value of USD 11.76 billion in 2024 and is projected to grow by USD 12.19 billion in 2025. Out of this, the China market accounted for the maximum revenue split of 33.61%. The regional growth can be attributed to the surge in industrialization and expanding automotive sector in China and India. This has created the need for affordable and reliable braking solutions tailored to local driving conditions. Further, in markets such as Japan and South Korea, a strong automotive manufacturing base drives technological innovation, leading to the development of cutting-edge braking systems that prioritize efficiency, performance, and safety. As the automotive sector continues to evolve in the Asia Pacific region, collaborations between domestic and international players drive market growth and facilitate the adoption of advanced braking technologies across diverse vehicle segments. These factors would further drive the regional automotive braking system market share during the forecast period.

- For instance, in January 2023, Continental India introduced a new single-channel ABS for two-wheelers for Indian market. The next-generation ABS module for motorcycles has been developed in Bengaluru-based tech center. In addition to this, the new module will be available in 125cc engine capacity and will be a cost-effective solution.

North America market is estimated to reach over USD 20.81 billion by 2032 from a value of USD 14.10 billion in 2024 and is projected to grow by USD 14.57 billion in 2025. Braking systems in this region often integrate advanced features such as collision mitigation and adaptive cruise control, aligning with consumer need for safer and more sophisticated driving experiences. Moreover, stringent regulatory frameworks drive the adoption of advanced braking technologies, stimulating market development and encouraging collaboration between automotive manufacturers and technology providers. Further, the U.S. and Canada have well-established automotive industries with a strong emphasis on safety features, including ABS. In addition to this, the growing need for electric vehicles and advanced driver assistance systems (ADAS) further propels the adoption of ABS technology in the region.

- For instance, in May 2023, the S. government proposed the mandatory inclusion of automatic emergency braking (AEB) on all new passenger cars and light commercial vehicles. This initiative by the government has a profound impact, and aims to significantly reduce the occurrence of crashes with pedestrians and rear-end collisions.

According to the analysis, the automotive braking system industry in Europe is projected to witness significant development during the forecast period. With a focus on reducing emissions and improving fuel economy, braking systems in Europe increasingly incorporate regenerative braking technologies to recapture kinetic energy during deceleration. Additionally, the region's commitment to road safety fosters the adoption of autonomous emergency braking systems and other active safety features, contributing to a competitive market landscape driven by innovation and regulatory compliance. Additionally, Latin American countries showcase a diverse automotive market characterized by varying consumer preferences and economic conditions. Moreover, government incentives and regulations aimed at reducing emissions and enhancing fuel efficiency are driving the automotive braking market in the region. Further, in the Middle East & Africa, the increasing urbanization and infrastructure development are expected to drive the need for commercial vehicles, thereby influencing the need for specialized braking systems tailored to these applications.

Top Key Players and Market Share Insights:

The global automotive braking system market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the automotive braking system industry include-

- AKEBONO BRAKE INDUSTRY CO., LTD. (Japan)

- ZF Friedrichshafen AG (Germany)

- Haldex (Sweden)

- Kiriu Corporation (Japan)

- Syensqo (Belgium)

- ADVICS CO.,LTD. (Japan)

- Hitachi Astemo, Ltd. (Japan)

- Brembo s.p.a (Italy)

- Tenneco Inc. (U.S.)

- Robert Bosch GmbH (Germany)

Recent Industry Developments :

Partnership:

- In March 2023, SSAB announced the partnership with MENETA, to introduce automotive brake components and sealing materials, which are manufactured using fossil-free steel. With this strategic partnership, companies reduce carbon emissions and transition to more sustainable materials.

Automotive Braking System Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 63.98 Billion |

| CAGR (2025-2032) | 5.4% |

| By Type |

|

| By Technology |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Automotive Braking System market? +

Automotive Braking System Market Size is estimated to reach over USD 63.98 Billion by 2032 from a value of USD 43.02 Billion in 2024 and is projected to grow by USD 44.46 Billion in 2025, growing at a CAGR of 5.4% from 2025 to 2032.

Which is the fastest-growing region in the Automotive Braking System market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. The rising popularity of automotive brake systems and increased sales of luxury and premium automobiles are expected to drive the regional market growth.

What specific segmentation details are covered in the Automotive Braking System report? +

The automotive braking system report includes specific segmentation details for type, technology, vehicle type, sales channel, and region.

Who are the major players in the Automotive Braking System market? +

The key participants in the market are AKEBONO BRAKE INDUSTRY CO., LTD. (Japan), ZF Friedrichshafen AG (Germany), ADVICS CO.,LTD. (Japan), Hitachi Astemo, Ltd. (Japan), Brembo s.p.a (Italy), Robert Bosch GmbH (Germany), Haldex (Sweden), Kiriu Corporation (Japan), Syensqo (Belgium), Tenneco Inc. (U.S.), and others.