- Summary

- Table Of Content

- Methodology

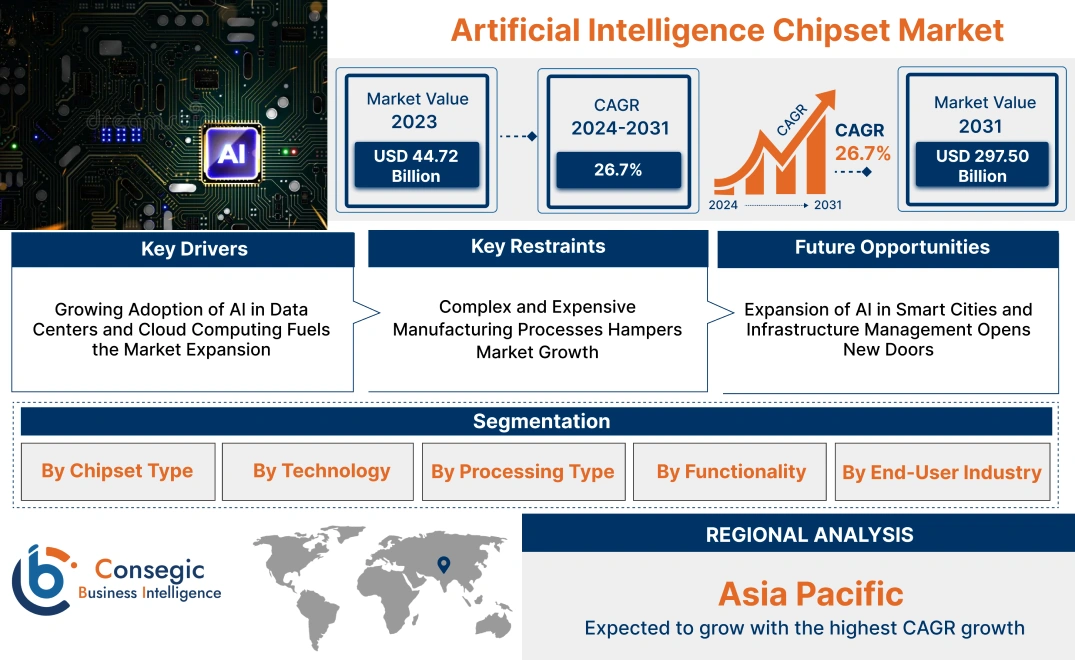

Artificial Intelligence Chipset Market Size:

The Artificial Intelligence Chipset Market size is estimated to reach over USD 297.50 Billion by 2031 from a value of USD 44.72 Billion in 2023 and is projected to grow by USD 55.88 Billion in 2024, growing at a CAGR of 26.7% from 2024 to 2031.

Artificial Intelligence Chipset Market Scope & Overview:

Artificial Intelligence (AI) chipsets are specialized hardware components designed to enhance the processing speed and efficiency of AI-related tasks, including machine learning, deep learning, and neural network operations. These chipsets are optimized to handle complex computations and data-intensive workloads, making them critical in applications such as image processing, natural language processing, and autonomous systems. AI chipsets are commonly used in sectors like automotive, healthcare, consumer electronics, and finance, where high-speed data analysis and real-time decision-making are essential. These chipsets are built with advanced architectures and parallel processing capabilities, allowing them to manage AI workloads with greater efficiency compared to traditional processors. The range of AI chipsets includes GPUs, CPUs, FPGAs, and custom AI accelerators, each designed to meet specific performance needs in AI-based applications. End-users of AI chipsets include cloud service providers, data centers, automotive manufacturers, and electronics companies, all of which require powerful computing solutions to implement AI systems effectively. As AI continues to evolve and expand its applications, AI chipsets remain an integral component in supporting these innovations across various industries.

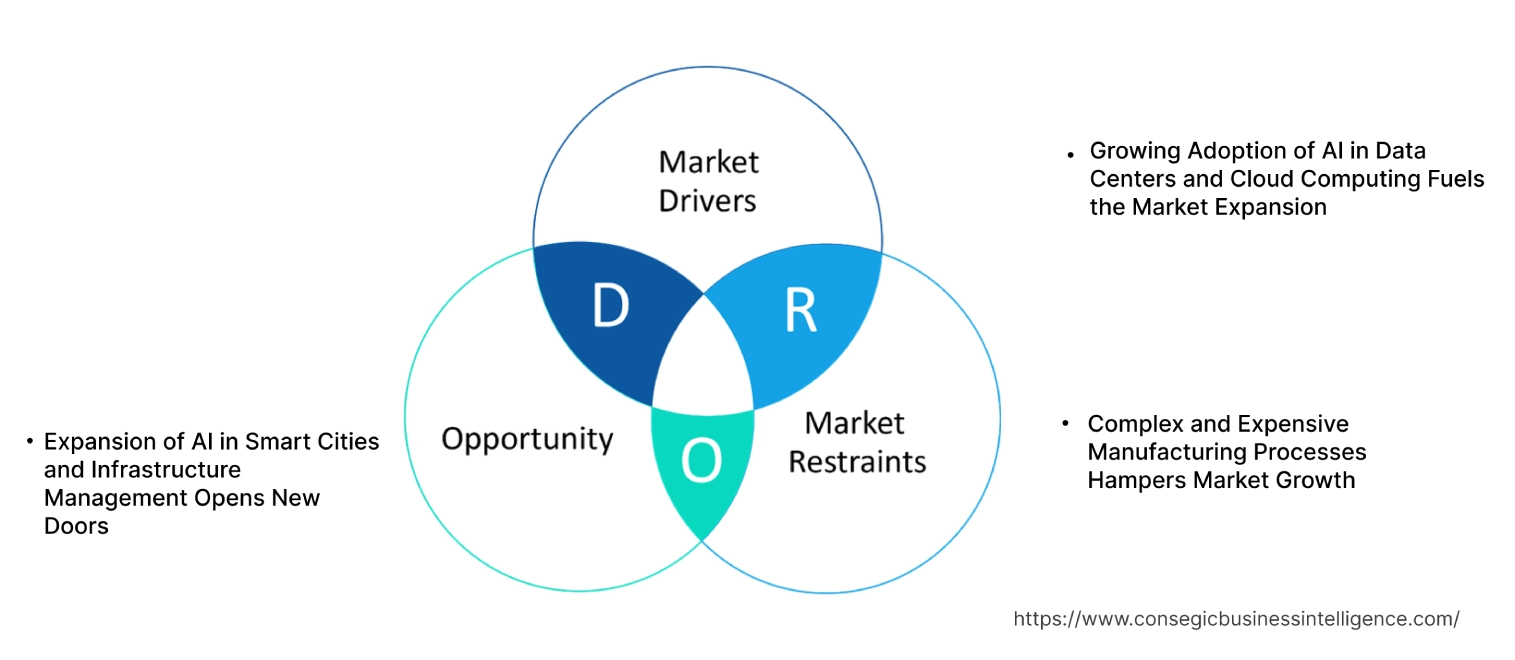

Artificial Intelligence Chipset Market Dynamics - (DRO) :

Key Drivers:

Growing Adoption of AI in Data Centers and Cloud Computing Fuels the Market Expansion

The rapid development of cloud computing services and data center infrastructure is a critical driver for the AI chipset market. AI workloads, including deep learning and machine learning applications, require substantial computing power, and specialized AI chipsets such as GPUs (Graphics Processing Units), ASICs (Application-Specific Integrated Circuits), and TPUs (Tensor Processing Units) are designed to handle these high-performance computing tasks efficiently. As enterprises increasingly rely on AI-driven analytics for tasks such as fraud detection, recommendation systems, and predictive maintenance, there is a rising need for chipsets that can support these complex workloads. Data centers, which serve as the backbone for cloud services, are rapidly deploying AI-optimized hardware to meet the growing requirement for real-time AI processing. Thus, the scalability and efficiency offered by AI chipsets in cloud environments further drive market growth.

Key Restraints :

Complex and Expensive Manufacturing Processes Hampers Market Growth

The manufacturing of AI chipsets is technologically complex and requires advanced fabrication processes using state-of-the-art technology nodes (often in the range of 5nm or 7nm). This increases both the cost and complexity of production, limiting the ability of smaller players to compete in the market. AI chipsets often need to be highly customized to optimize for specific AI workloads, such as natural language processing or computer vision, further increasing the design and manufacturing costs. The design complexity also leads to longer development cycles and higher risk, as the failure to meet performance benchmarks can lead to costly revisions. Additionally, the global semiconductor shortage and supply chain disruptions, exacerbated by the ongoing geopolitical tensions, have further increased production costs and limited the availability of key materials needed for AI chip manufacturing. The above-mentioned factors in scaling up manufacturing capacities and ensuring cost efficiency are significant restraints that hinder market demand.

Future Opportunities :

Expansion of AI in Smart Cities and Infrastructure Management Opens New Doors

The ongoing global investment in smart city infrastructure is driving a significant need for advanced AI chipsets. Cities are increasingly incorporating AI technologies into traffic management, surveillance systems, energy management, and public safety to enhance operational efficiency, optimize resource utilization, and reduce costs. AI chipsets play a crucial role in powering the real-time data processing required to manage vast streams of information generated by sensors, cameras, and IoT devices deployed across urban environments.

The rising adoption of edge AI solutions, which enable localized data processing and decision-making at the source, is opening new opportunities for AI chipset manufacturers to develop energy-efficient processors capable of supporting computer vision, pattern recognition, and predictive maintenance applications. These applications are essential for ensuring the responsiveness and sustainability of smart city systems. Furthermore, governments and municipal authorities are increasingly prioritizing AI-enabled public services, creating a substantial market for AI hardware solutions tailored to meet the specific requirements of smart infrastructure. Therefore, this growing emphasis on AI-driven urban management drives the artificial intelligence chipset market opportunities.

Artificial Intelligence Chipset Market Segmental Analysis :

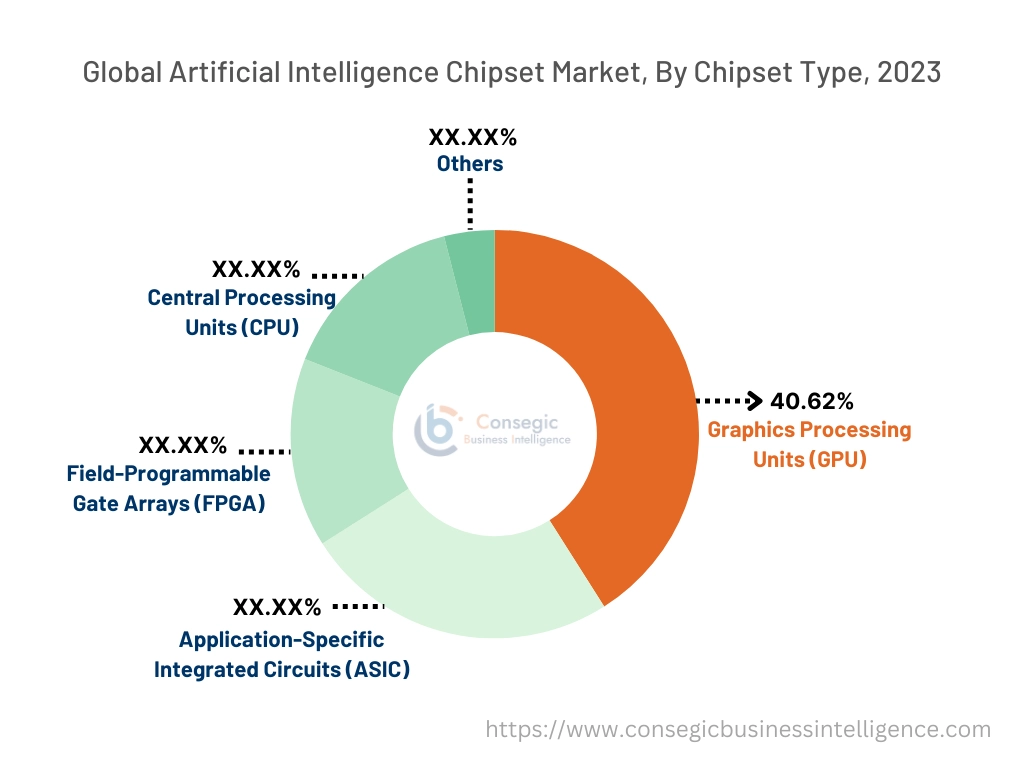

By Chipset Type:

Based on the Chipset type the artificial intelligence chipset market is divided into Graphics Processing Units (GPU), Application-Specific Integrated Circuits (ASIC), Field-Programmable Gate Arrays (FPGA), Central Processing Units (CPU), and others.

The GPU segment accounted for the largest revenue of 40.62% of the total artificial intelligence chipset market share in 2023.

- Graphics Processing Units (GPUs) have been central to accelerating AI workloads, particularly in deep learning applications, due to their parallel processing capabilities.

- GPUs offer significant computational power, which is essential for training complex AI models and processing large datasets in industries such as healthcare, automotive, and finance.

- The continuous improvements in GPU technology, coupled with the rising requirements for AI-driven solutions, solidify the GPU's dominant position in the market.

- The GPU segment continues to hold the largest share of the AI chipset market, fueled by its importance in training and inference tasks for AI models in several industries such as healthcare and finance.

- Therefore, the need for high-speed computing drives the artificial intelligence chipset market demand.

The ASIC segment is anticipated to register the fastest CAGR during the forecast period.

- Application-specific integrated Circuits (ASICs) are gaining traction as they offer tailored solutions for specific AI applications, such as speech recognition, natural language processing, and image classification.

- These custom-designed chips are highly efficient, consuming less power while delivering higher performance compared to general-purpose GPUs.

- As industries like automotive (autonomous driving) and consumer electronics (smart devices) seek specialized hardware for real-time AI applications, the need for ASICs is projected to grow rapidly.

- The ASIC segment is expected to witness the fastest development, driven by the rising need for highly efficient and application-specific AI hardware, particularly in sectors like automotive and consumer electronics.

- As per segmental trends analysis, the need for tailored solutions boosts the artificial intelligence chipset market expansion.

By Technology:

Based on the technology type the artificial intelligence chipset market is divided into System-on-Chip (SoC), System-in-Package (SiP), Multi-Chip Module, and others.

The System-on-Chip (SoC) segment accounted for the largest revenue share in 2023.

- System-on-chip (SoC) technology integrates multiple components of a computing system, such as processors, memory, and connectivity, onto a single chip.

- SoCs are essential in compact devices where space, power efficiency, and performance are critical.

- Their use is widespread across smartphones, tablets, and IoT devices, which require efficient processing for AI applications such as voice recognition, image processing, and predictive analytics.

- The versatility and efficiency of SoC solutions drive their market dominance.

- The SoC segment dominates the market due to its integration capabilities and crucial role in powering AI-enabled mobile devices, wearables, and IoT applications.

- Therefore, due to the versatility and high efficiency of SoC it drives the artificial intelligence chipset market growth.

The System-in-Package (SiP) segment is projected to witness the fastest growth.

- System-in-Package (SiP) technology allows multiple integrated circuits to be packaged together, enabling enhanced functionality within compact devices.

- This technology is becoming increasingly important in AI edge computing, where devices need to process data locally with limited power and space.

- As the demand for real-time AI processing at the edge grows, SiP technology is expected to see rapid adoption in industries such as automotive, consumer electronics, and smart infrastructure.

- SiP is projected to be the fastest-growing technology segment, driven by the increasing need for real-time AI processing in edge computing devices across various industries.

- Therefore, as per market trends analysis, SiP fuels the artificial intelligence chipset market trends.

By Processing Type:

Based on the Processing type the artificial intelligence chipset market is divided into Edge, Cloud, and Hybrid.

The cloud segment accounted for the largest revenue share in 2023.

- Cloud-based AI chipsets are critical for handling large-scale, data-intensive AI workloads such as machine learning model training, data analytics, and real-time inference.

- Leading cloud service providers like Amazon Web Services (AWS), Google Cloud, and Microsoft Azure rely on high-performance AI chipsets, such as GPUs and custom-designed AI chips (TPUs), to support a broad range of AI services.

- As enterprises continue to migrate workloads to the cloud, the requirement for AI chipsets optimized for cloud environments is growing rapidly.

- Cloud-based AI chipsets dominate the market, driven by the increasing reliance on cloud platforms for AI workloads, especially in data-heavy industries such as finance, healthcare, and retail.

- Therefore, as per the artificial intelligence chipset market analysis, the cloud segment boosts the market progress.

The edge segment is anticipated to register the fastest CAGR during the forecast period.

- Edge computing, where AI processing occurs locally on devices (e.g., smartphones, IoT devices, autonomous vehicles), is rapidly gaining momentum.

- Edge AI chipsets enable real-time data processing with minimal latency, which is crucial for applications like autonomous driving, smart city infrastructure, and industrial automation.

- The growing focus on AI-powered IoT devices and the need for decentralized processing capabilities are propelling the need for edge AI chipsets.

- Additionally, advancements in low-power, high-performance chipsets designed for edge computing are expected to drive improvement in this segment.

- The edge segment is expected to grow rapidly due to the increasing adoption of AI-enabled IoT devices and the need for real-time, low-latency processing in autonomous systems and smart applications.

- Therefore, as per the segmental trends analysis, the edge segment boosts the market demand.

By Functionality:

Based on the Functionality type the artificial intelligence chipset market is bifurcated into Training and Inference.

The training segment accounted for the largest revenue share in 2023.

- AI training involves processing vast amounts of data to build and optimize machine learning models, which require immense computational power.

- High-performance GPUs and specialized chips such as TPUs are crucial for training deep learning models used in various applications, including natural language processing (NLP), computer vision, and autonomous systems.

- The complexity of AI training tasks, particularly in research and development, drives the need for advanced AI chipsets capable of handling large-scale data processing.

- The increasing focus on developing sophisticated AI models is reinforcing the dominance of the training segment.

- The training segment dominates the market due to the high computational needs of building and optimizing AI models across sectors like healthcare, finance, and autonomous systems.

- Therefore, the need for computation and processing of large volumes of data drives the artificial intelligence chipset market demand.

The inference segment is anticipated to register the fastest CAGR during the forecast period.

- AI inference involves deploying trained models to make predictions or decisions in real-time, often on edge devices or in cloud environments.

- Inference chipsets are optimized for efficiency and speed, allowing AI applications to run in production environments, such as smart devices, autonomous vehicles, and real-time analytics platforms.

- As AI moves from research to real-world deployment, the requirement for inference-optimized chipsets is expected to grow significantly, particularly in industries like automotive, healthcare, and consumer electronics.

- The inference segment is expected to grow rapidly due to the increasing deployment of AI applications in real-time environments, particularly in edge devices and autonomous systems that require low-latency, high-efficiency processing.

- Therefore, the need for predictive models for decision-making fuels market development.

By End-User:

Based on the End-user industry the artificial intelligence chipset market is segmented into Automotive, Consumer Electronics, Healthcare, Retail, IT & Telecom, Banking, Financial Services, and Insurance (BFSI) and others.

The automotive segment accounted for the largest revenue share in 2023.

- The automotive sector has embraced AI chipsets for various applications, from advanced driver assistance systems (ADAS) to fully autonomous vehicles.

- AI chipsets are crucial for processing vast amounts of sensor data in real-time to ensure vehicle safety and enhance the driving experience.

- The push towards autonomous vehicles, coupled with the increasing integration of AI in connected cars, has positioned the automotive sector as the largest consumer of AI chipsets.

- Key players such as Tesla, NVIDIA, and Waymo are investing heavily in AI chipset solutions to accelerate the development of autonomous driving technologies.

- The automotive sector leads the AI chipset market, driven by the rapid development of ADAS and autonomous vehicles, and the need for real-time data processing capabilities.

- Therefore, as per the segmental trends analysis, the automotive segment boosts the market demand.

The healthcare segment is projected to witness the fastest CAGR during the forecast period.

- The healthcare sector is increasingly adopting AI for applications such as medical imaging, diagnostics, personalized medicine, and drug discovery.

- AI chipsets play a crucial role in enabling these advanced healthcare applications by processing complex algorithms that can identify diseases, suggest treatments, and enhance patient outcomes.

- With the growing requirement for AI-powered medical devices and diagnostics, the healthcare sector is expected to witness the highest growth in AI chipset adoption, particularly for improving diagnostic accuracy and operational efficiency.

- The healthcare segment is expected to grow at the fastest rate, fueled by the increasing adoption of AI in diagnostics, medical imaging, and personalized medicine, where AI chipsets are critical for delivering real-time, data-driven insights.

- Therefore, as per the segmental trends analysis, the healthcare segment boosts the market demand.

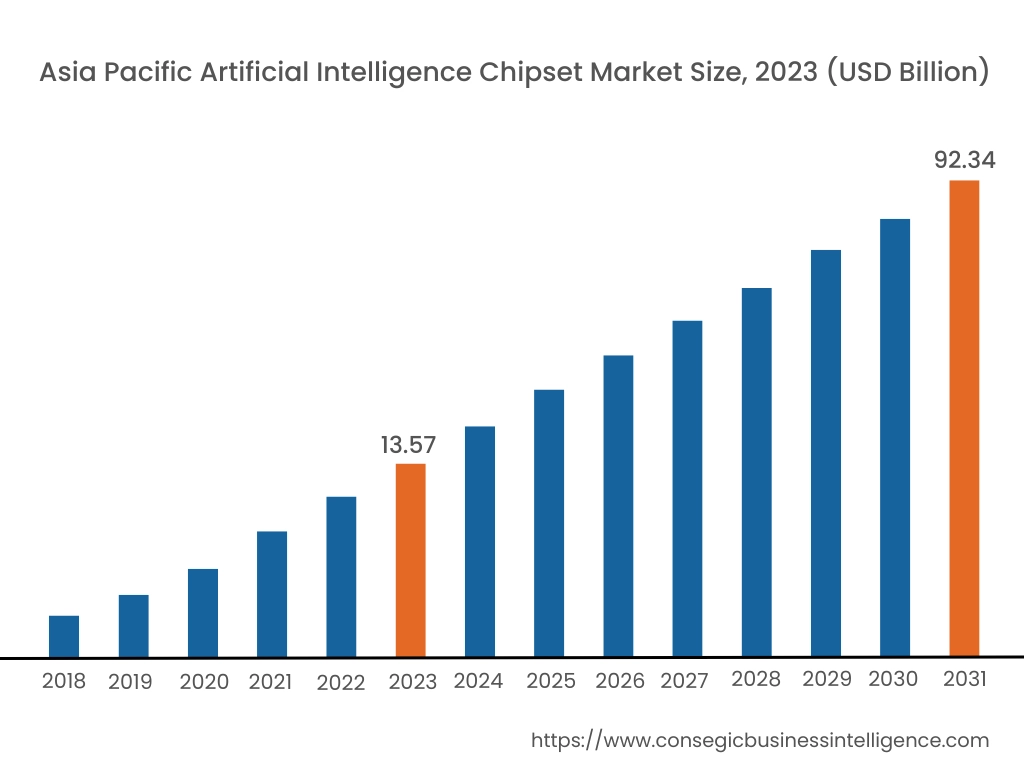

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

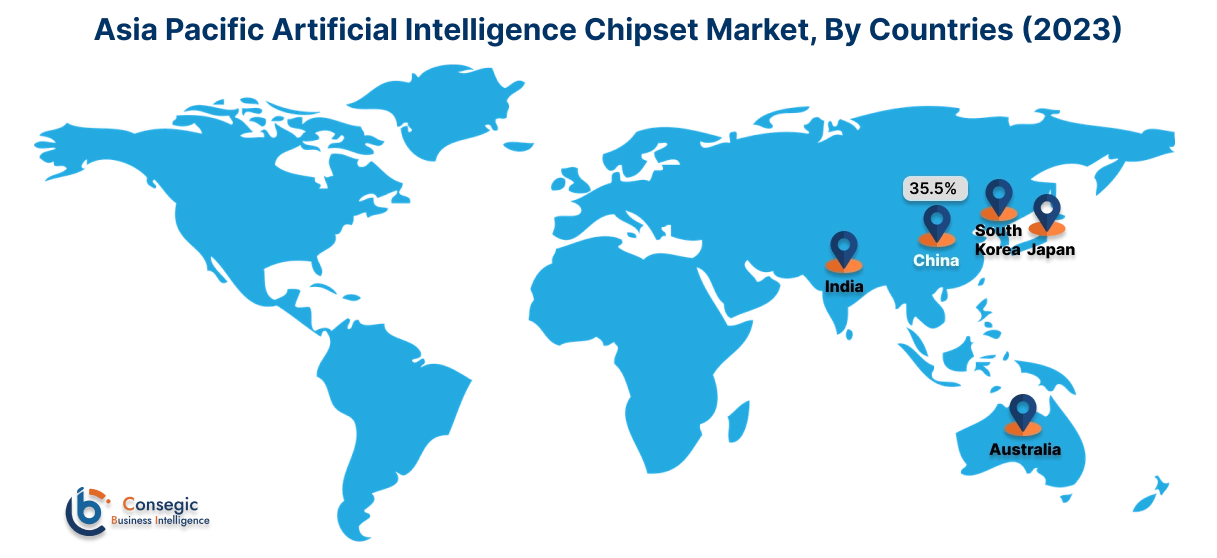

Asia Pacific region was valued at USD 13.57 Billion in 2023. Moreover, it is projected to grow by USD 16.99 Billion in 2024 and reach over USD 92.34 Billion by 2031. Out of this, China accounted for 35.5% of the total share in 2023. Asia-Pacific is the fastest-growing region for AI chipsets, driven by China's rapid investment in AI technologies and 5G infrastructure. China is not only a massive consumer but also a global leader in AI research and chipset production, with companies like Huawei and Baidu advancing AI applications in smart cities, healthcare, and autonomous driving. Japan is another key player, where the need for AI chipsets is bolstered by its leadership in robotics and manufacturing automation. India shows promise as a major adopter of AI, particularly in the fields of agriculture, education, and financial technology. Therefore, ongoing developments in the Asia Pacific region fuel the market growth.

North America is estimated to reach over USD 105.29 Billion by 2031 from a value of USD 15.68 Billion in 2023 and is projected to grow by USD 19.61 Billion in 2024. This region, particularly the United States is the dominant player in the AI chipset market, driven by technological advancements and strong industry presence. The U.S. houses major semiconductor companies like NVIDIA, Intel, and AMD, which are integral to the development of AI-driven technologies such as autonomous vehicles, cloud computing, and smart healthcare systems. The market benefits from significant R&D investments, with AI chipsets being essential for data centers and edge computing. Canada, although smaller in market size, is also witnessing a boom in AI, supported by its focus on AI ethics, research institutes, and collaboration with U.S.-based companies. As per analysis, the rise in technological developments in the North American region drives the artificial intelligence chipset market growth.

Europe holds a strategic position in the AI chipset market, led by nations such as Germany, the UK, and France. Germany, with its robust industrial sector, particularly in automotive manufacturing, is driving the use of AI chipsets in autonomous driving and smart factories. The UK excels in AI research, backed by initiatives like the AI strategy focusing on sectors like healthcare and finance, fostering the adoption of AI technology. France has also invested heavily in AI for healthcare and smart cities, where AI chipsets play a vital role in the deployment of solutions.

The Middle East and Africa show gradual yet steady development in AI chipset adoption, particularly in countries like UAE and South Africa. The UAE, with its ambitious smart city projects, has been a leader in deploying AI technologies and integrating AI chipsets into urban planning and healthcare systems. Additionally, the UAE's investment in AI research and partnerships with global tech companies drive market growth. South Africa, the largest economy in Africa, is focused on using AI for mining, financial services, and smart cities, which is increasing the need for AI chipsets.

Latin America is an emerging market for AI chipsets, with countries like Brazil, Mexico, and Argentina showing notable potential. Brazil is at the forefront of AI adoption, with growing investment in AI applications for agriculture, healthcare, and transportation. The country's AI strategy, backed by initiatives from the Brazilian government and private sector collaboration, is expected to drive AI chipset needs. Mexico has witnessed an increase in automotive manufacturing and electronics industries, where AI is integrated into smart manufacturing. Argentina is gradually adopting AI in industries like agriculture and energy, further contributing to market development.

Top Key Players & Market Share Insights:

The artificial intelligence chipset market is highly competitive with major players providing artificial intelligence chipset services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global artificial intelligence chipset market. Key players in the artificial intelligence chipset industry include -

Recent Industry Developments :

- In October 2024, AMD launched the Ryzen AI Pro 300 series processors, aimed at enhancing AI-powered capabilities in business laptops. These processors feature AMD's first hardware AI engine, built on Zen 4 architecture, offering improved energy efficiency and security for enterprise-level applications. Designed to handle modern AI workloads, they target users needing enhanced performance for business and security tasks.

- In October 2024, Qualcomm unveiled the Snapdragon 8 Elite, boasting the world's fastest mobile CPU. This chipset delivers superior performance for AI, gaming, and imaging with enhanced efficiency. It includes an advanced GPU for high-end gaming and a powerful AI engine to accelerate tasks like voice processing and photography. The Snapdragon 8 Elite also features next-gen connectivity with Wi-Fi 7 and 5G support, catering to premium smartphones and mobile devices.

- In March 2024, NVIDIA introduced the Blackwell platform, a significant advancement in accelerated computing. This platform is engineered to efficiently handle trillion-parameter large language models, offering up to 25 times greater cost and energy efficiency compared to its predecessor. The Blackwell GPU architecture incorporates six transformative technologies aimed at breakthroughs in data processing, engineering simulation, electronic design automation, computer-aided drug design, quantum computing, and generative AI. Major organizations are expected to adopt the Blackwell platform to enhance their AI and computing capabilities.

Artificial Intelligence Chipset Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 297.50 Billion |

| CAGR (2024-2031) | 26.7% |

| By Chipset Type |

|

| By Technology |

|

| By Processing Type |

|

| By Functionality |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the artificial intelligence chipset market? +

The Artificial Intelligence Chipset Market size is estimated to reach over USD 297.50 Billion by 2031 from a value of USD 44.72 Billion in 2023 and is projected to grow by USD 55.88 Billion in 2024, growing at a CAGR of 26.7% from 2024 to 2031.

What specific segmentation details are covered in the Artificial Intelligence chipset Market report? +

The artificial intelligence chipset market report includes segmentation details for chipset type, technology, processing type, functionality, end-user industry, and region.

Which is the fastest-growing industry in the Artificial Intelligence chipset market? +

According to the analysis, the healthcare industry is the fastest growing in the artificial intelligence chipset market due to the adoption of AI in diagnostics and treatment in the healthcare field.

Who are the major players in the artificial intelligence chipset Market? +

The key players in the artificial intelligence chipset market are Nvidia (USA), Intel (USA), Advanced Micro Devices (AMD) (USA), Qualcomm (USA), Samsung Electronics (South Korea), Apple (USA), IBM (USA), Graphcore (UK), Arm Holdings (UK) and MediaTek (Taiwan).