- Summary

- Table Of Content

- Methodology

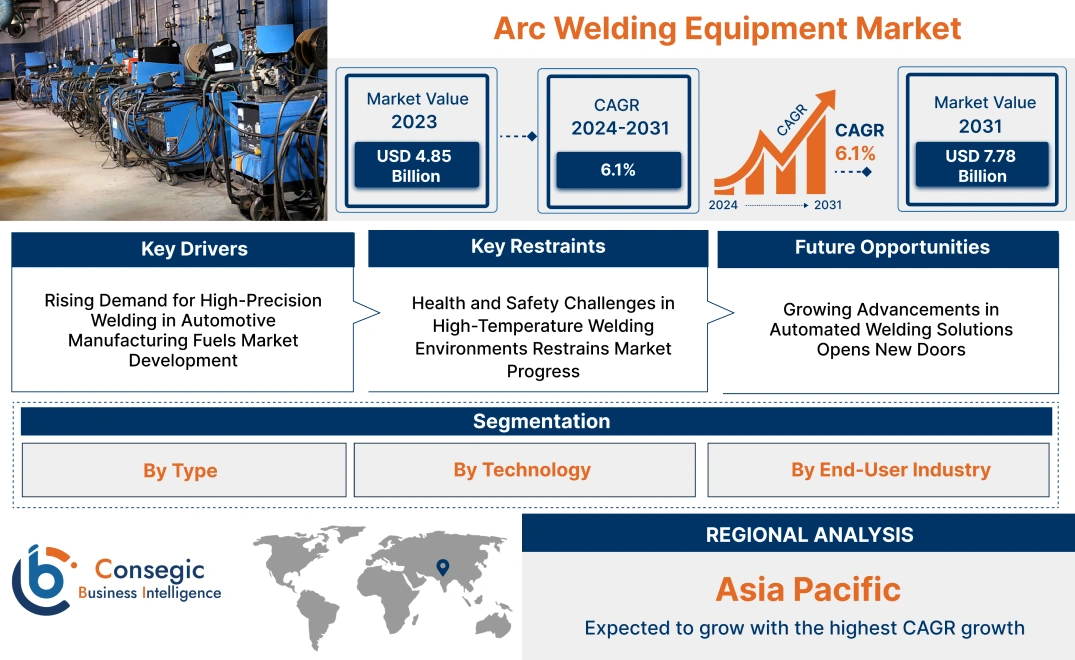

Arc Welding Equipment Market Size:

Arc Welding Equipment Market size is estimated to reach over USD 7.78 Billion by 2031 from a value of USD 4.85 Billion in 2023 and is projected to grow by USD 5.06 Billion in 2024, growing at a CAGR of 6.1% from 2024 to 2031.

Arc Welding Equipment Market Scope & Overview:

Arc welding equipment is designed to join metals by using an electric arc to melt and fuse materials at the point of contact. This equipment includes welding machines, electrodes, power supplies, and safety gear, ensuring precision and durability in welding operations. It is commonly used in industries such as construction, automotive, shipbuilding, and manufacturing for creating strong, reliable metal joints.

These systems are available in various configurations, such as manual, semi-automatic, and automatic, catering to a range of applications from small-scale fabrication to large industrial projects. The equipment is engineered for efficiency, providing consistent welding quality while reducing material waste. Modern arc welding technologies also integrate features like digital controls and thermal overload protection to enhance operational safety and performance.

End-users of this equipment include manufacturing plants, construction companies, and repair facilities that rely on arc welding processes for diverse applications requiring metal joining and fabrication. These solutions play a critical role in ensuring the structural integrity and longevity of metal-based products and infrastructures.

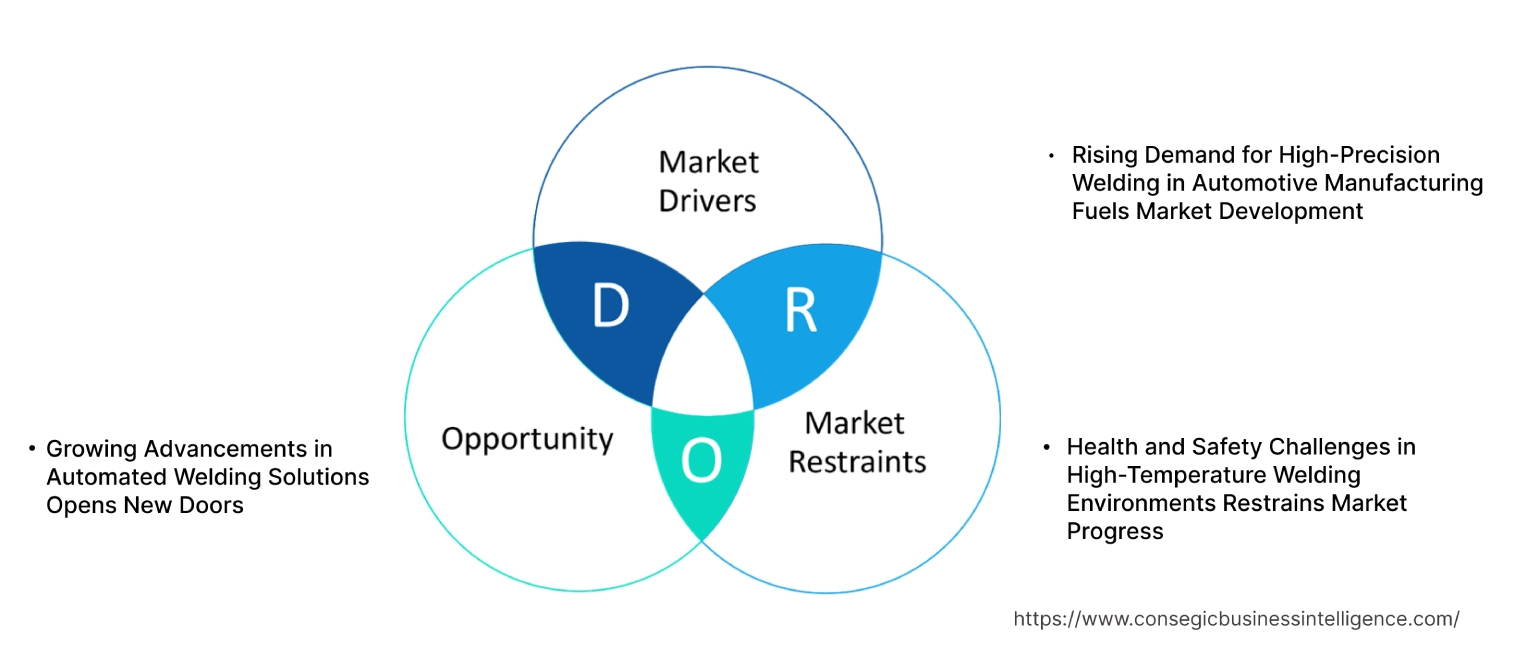

Arc Welding Equipment Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for High-Precision Welding in Automotive Manufacturing Fuels Market Development

The increasing adoption of high-precision welding technologies in automotive manufacturing is a significant driver for the market. Modern vehicle production processes, especially for electric and hybrid vehicles, demand precise and reliable welding to ensure structural integrity and safety. Advanced arc welding techniques, including gas metal arc welding (GMAW) and tungsten inert gas welding (TIG), are widely used for their ability to deliver superior joint quality in critical components such as chassis, body panels, and battery enclosures. As the automotive industry emphasizes lightweight materials and intricate designs, the growing need for precise joining techniques boosts arc welding equipment market demand, prompting investments in advanced welding technologies.

Key Restraints :

Health and Safety Challenges in High-Temperature Welding Environments Restrains Market Progress

The use of welding equipment poses significant safety risks for operators, including eye damage from intense light and UV radiation, which leads to conditions such as arc eye. The high heat generated during welding processes increases the risk of burns and fire hazards, particularly in environments with flammable materials. Additionally, improper handling of equipment or gas cylinders used in certain welding methods leads to explosions, endangering both operators and nearby personnel.

These safety concerns necessitate the use of protective gear and strict adherence to safety protocols, which increases operational costs. The inherent risks also deter some businesses, especially smaller enterprises, from adopting advanced welding equipment, limiting arc welding equipment market growth. Addressing these safety issues requires ongoing investment in training, equipment innovation, and workplace safety measures, creating additional constraints for the industry.

Future Opportunities :

Growing Advancements in Automated Welding Solutions Opens New Doors

The continuous advancements in automated welding technologies present significant growth opportunities for the market. Automated welding systems, such as robotic welding arms and programmable welding units, are revolutionizing industries like automotive, aerospace, and heavy machinery by improving precision, speed, and consistency. These systems handle repetitive and high-volume tasks with minimal human intervention, significantly reducing labor costs and operational errors. Recent innovations, such as the integration of artificial intelligence (AI) and machine learning, have further enhanced automated welding capabilities. AI-driven systems optimize welding parameters in real time, improve joint quality, and enable predictive maintenance by analyzing equipment performance.

Additionally, automated solutions are increasingly equipped with advanced monitoring and safety features, ensuring reliability in high-demand applications. As manufacturers aim to boost productivity and tackle labor shortages, the arc welding equipment market opportunities are expanding through the growing adoption of automated and high-precision welding technologies.

Arc Welding Equipment Market Segmental Analysis :

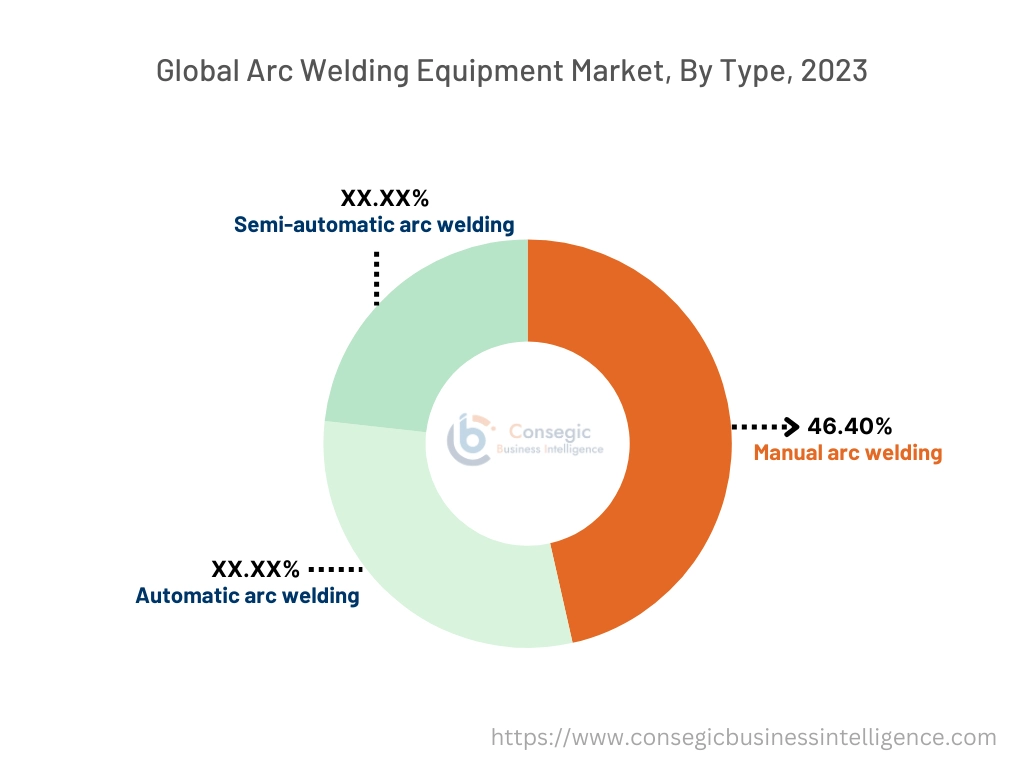

By Type:

Based on type, the market is segmented into manual arc welding, automatic arc welding, and semi-automatic arc welding.

The manual arc welding segment held the largest revenue of 46.40% of the total arc welding equipment market share in 2023.

- Manual arc welding remains a cornerstone in various industries due to its versatility, cost-effectiveness, and ability to operate in challenging environments.

- It is particularly favored in small-scale industries and repair operations, where precision and adaptability are crucial.

- The segment’s dominance is supported by the widespread availability of skilled welders and minimal equipment requirements, making it ideal for diverse applications.

- Manual arc welding remains integral to industries like construction and marine due to its adaptability to on-site tasks, supporting arc welding equipment market expansion in dynamic field applications.

The automatic arc welding segment is expected to register the fastest CAGR during the forecast period.

- Automatic arc welding systems are increasingly adopted in large-scale manufacturing environments due to their precision, consistency, and efficiency.

- These systems minimize human intervention, reducing errors and enhancing productivity in applications like automotive assembly lines and heavy machinery production.

- Advancements in automation and robotic integration are driving the adoption of automatic arc welding across high-volume production industries.

- As per arc welding equipment market analysis, the segment’s rapid expansion is attributed to its ability to deliver high-quality welds consistently, particularly in industries with stringent performance and safety standards.

By Technology:

Based on technology, the market is segmented into Shielded Metal Arc Welding (SMAW), Gas Metal Arc Welding (GMAW), Gas Tungsten Arc Welding (GTAW), Submerged Arc Welding (SAW), and Flux-Cored Arc Welding (FCAW).

The Gas Metal Arc Welding (GMAW) segment accounted for the largest revenue of the total arc welding equipment market share in 2023.

- GMAW, also known as MIG welding, is widely used for its speed, ease of use, and ability to weld a wide range of materials, including aluminum and steel.

- This technology is a preferred choice in industries such as automotive and construction due to its ability to deliver clean and high-strength welds.

- Advancements in GMAW technology, including pulse and spray transfer methods, are further enhancing its efficiency and versatility in complex welding applications.

- As per arc welding equipment market trends, the dominance of this segment is driven by its adaptability across diverse industrial applications and reduced training requirements for operators.

The Submerged Arc Welding (SAW) segment is expected to register the fastest CAGR during the forecast period.

- SAW technology is widely adopted for welding thick materials in heavy industries such as shipbuilding, pipelines, and oil & gas infrastructure.

- The use of flux to shield the arc ensures high-quality welds with minimal spatter, making SAW ideal for large-scale fabrication projects.

- Innovations in SAW equipment, such as multi-wire welding systems, are enhancing productivity and reducing operational costs.

- The rapid expansion of this segment highlights the growing use of SAW in heavy-duty industries, significantly supporting arc welding equipment market growth with its high-performance capabilities.

By End-User Industry:

Based on end-user industry, the market is segmented into aerospace, automotive, building & construction, energy, oil & gas, marine, and others.

The automotive segment accounted for the largest revenue share in 2023.

- Automotive manufacturers rely heavily on arc welding for the assembly of body structures, chassis components, and exhaust systems.

- The integration of robotic arc welding systems in automotive production lines enhances precision, repeatability, and speed, reducing production timelines.

- Lightweight material welding, such as aluminum and advanced high-strength steel, is gaining prominence in automotive applications, driving the adoption of advanced arc welding technologies.

- The dominance of the automotive segment is driven by rising vehicle production volumes and the demand for precise welding, highlighting growing arc welding equipment market demand.

The oil & gas segment is expected to register the fastest CAGR during the forecast period.

- Arc welding plays a critical role in the construction and maintenance of pipelines, storage tanks, and offshore platforms in the oil & gas sector.

- The need for durable and corrosion-resistant welds in extreme environments is driving the adoption of advanced arc welding technologies.

- Increasing investments in oil & gas infrastructure and exploration projects are creating significant opportunities for arc welding equipment.

- The rapid growth of this segment is driven by its critical role in ensuring the structural integrity of vital oil and gas infrastructure, contributing to the arc welding equipment market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

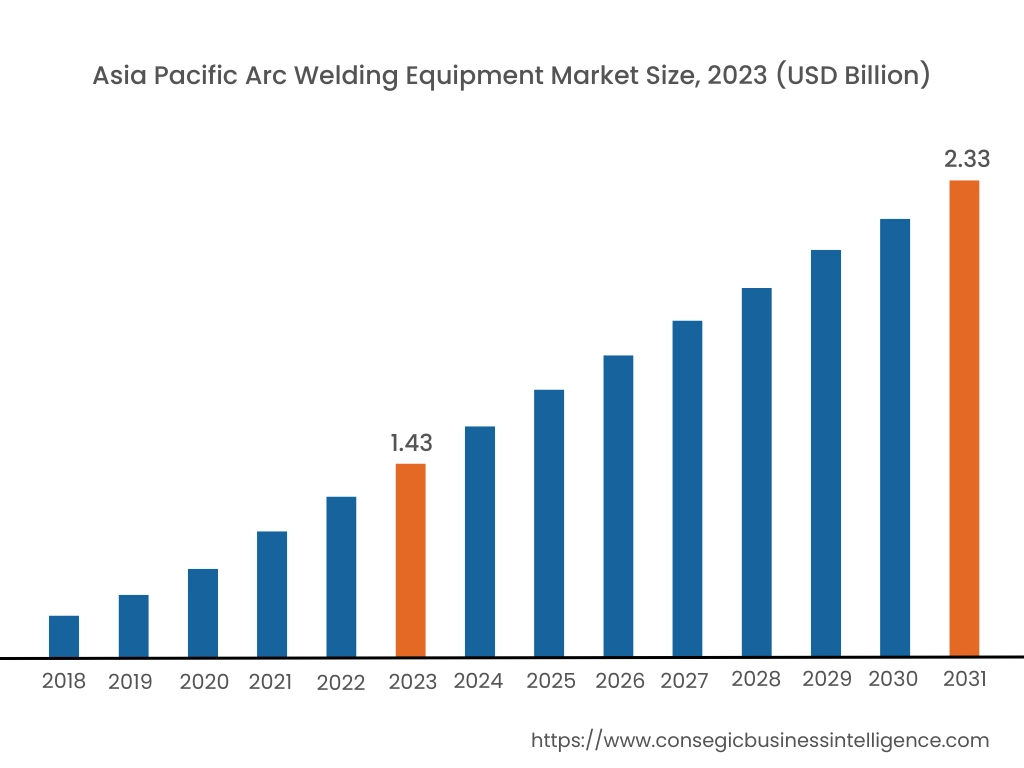

Asia Pacific region was valued at USD 1.43 Billion in 2023. Moreover, it is projected to grow by USD 1.49 Billion in 2024 and reach over USD 2.33 Billion by 2031. Out of these, China accounted for the largest share of 42.6% in 2023. Asia-Pacific is witnessing the fastest growth in the arc welding equipment market, driven by rapid industrialization and urbanization in countries like China, India, and Japan. The region has become a global hub for manufacturing, with a strong emphasis on sectors such as automotive, construction, and shipbuilding. The increasing investments in infrastructure projects and the expansion of the manufacturing sector are further propelling arc welding equipment market opportunities.

North America is estimated to reach over USD 2.56 Billion by 2031 from a value of USD 1.61 Billion in 2023 and is projected to grow by USD 1.68 Billion in 2024. In North America, the arc welding equipment market is bolstered by a robust manufacturing base and substantial investments in infrastructure development. The United States, in particular, leads the market with a strong presence of key industry players and a focus on adopting advanced welding technologies to enhance productivity and efficiency. The automotive and aerospace sectors are major contributors to the demand for arc welding equipment in this region.

Europe represents a significant portion of the global arc welding equipment market, with countries like Germany, France, and the United Kingdom leading in terms of adoption and innovation. The region benefits from a well-established industrial sector and a strong emphasis on automation and precision engineering. The need for lightweight and fuel-efficient vehicles is increasing, driving the adoption of advanced welding techniques.

The Middle East & Africa region shows promising potential in the arc welding equipment market, particularly in countries like Saudi Arabia, the United Arab Emirates, and South Africa. Increasing investments in infrastructure projects and the extension of the oil and gas sector are driving the need for welding equipment. The focus on diversifying economies and reducing dependence on oil revenues has led to growth in the construction and manufacturing sectors.

Latin America is an emerging market, with Brazil and Mexico being the primary growth drivers. The rising adoption of advanced manufacturing techniques, improving infrastructure, and increasing focus on enhancing industrial productivity contribute to the market’s enlargement. Government initiatives aimed at modernizing industrial infrastructure and promoting foreign investments are supporting market growth.

Top Key Players & Market Share Insights:

The arc welding equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global arc welding equipment market. Key players in the arc welding equipment industry include –

- Lincoln Electric (USA)

- Miller Electric (USA)

- ESAB (Sweden)

- Hobart Welding Products (USA)

- KEMPER GmbH (Germany)

- Fronius International GmbH (Austria)

- KUKA AG (Germany)

- Panasonic Corporation (Japan)

- Kobe Steel, Ltd. (Japan)

- Voestalpine Böhler Welding (Austria)

Recent Industry Developments :

Product Launches:

- In September 2024, Miller Electric Mfg. LLC introduced the XMT 400 ArcReach multiprocess welder, a versatile welding solution designed to enhance productivity and efficiency in demanding This advanced system supports various welding processes, including MIG, TIG, and stick welding, while offering ArcReach technology for seamless control without needing additional cables. It is built for durability and portability, catering to industrial needs with superior reliability and performance.

- In July 2023, Novarc Technologies introduced NovEye™ Autonomy Gen 2, a cutting-edge AI-powered real-time vision system that fully automates the pipe welding process. This system enhances weld quality through data collection and continuous AI model improvements, ensuring X-ray-level precision. Integrated into Novarc's Spool Welding Robot, it handles real-world welding challenges, improves productivity, and eliminates operator intervention. Designed for industries like aerospace and energy, it ensures compliance with ASME standards while improving safety by reducing exposure to hazards like fumes and heat.

Arc Welding Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 7.78 Billion |

| CAGR (2024-2031) | 6.1% |

| By Type |

|

| By Technology |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Arc Welding Equipment Market? +

Arc Welding Equipment Market size is estimated to reach over USD 7.78 Billion by 2031 from a value of USD 4.85 Billion in 2023 and is projected to grow by USD 5.06 Billion in 2024, growing at a CAGR of 6.1% from 2024 to 2031.

What specific segmentation details are covered in the Arc Welding Equipment Market report? +

The Arc Welding Equipment Market report includes segmentation details for type (Manual Arc Welding, Automatic Arc Welding, Semi-Automatic Arc Welding), technology (Shielded Metal Arc Welding (SMAW), Gas Metal Arc Welding (GMAW), Gas Tungsten Arc Welding (GTAW), Submerged Arc Welding (SAW), Flux-Cored Arc Welding (FCAW)), end-user industry(Aerospace, Automotive, Building & Construction, Energy, Oil & Gas, Marine, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Arc Welding Equipment Market? +

The Submerged Arc Welding (SAW) segment is projected to grow steadily, driven by its application in heavy industries such as shipbuilding, pipelines, and oil & gas infrastructure.

Who are the major players in the Arc Welding Equipment Market? +

The major players in the Arc Welding Equipment Market include Lincoln Electric (USA), Miller Electric (USA), ESAB (Sweden), Hobart Welding Products (USA), KEMPER GmbH (Germany), Fronius International GmbH (Austria), KUKA AG (Germany), Panasonic Corporation (Japan), Kobe Steel, Ltd. (Japan), and Voestalpine Böhler Welding (Austria).