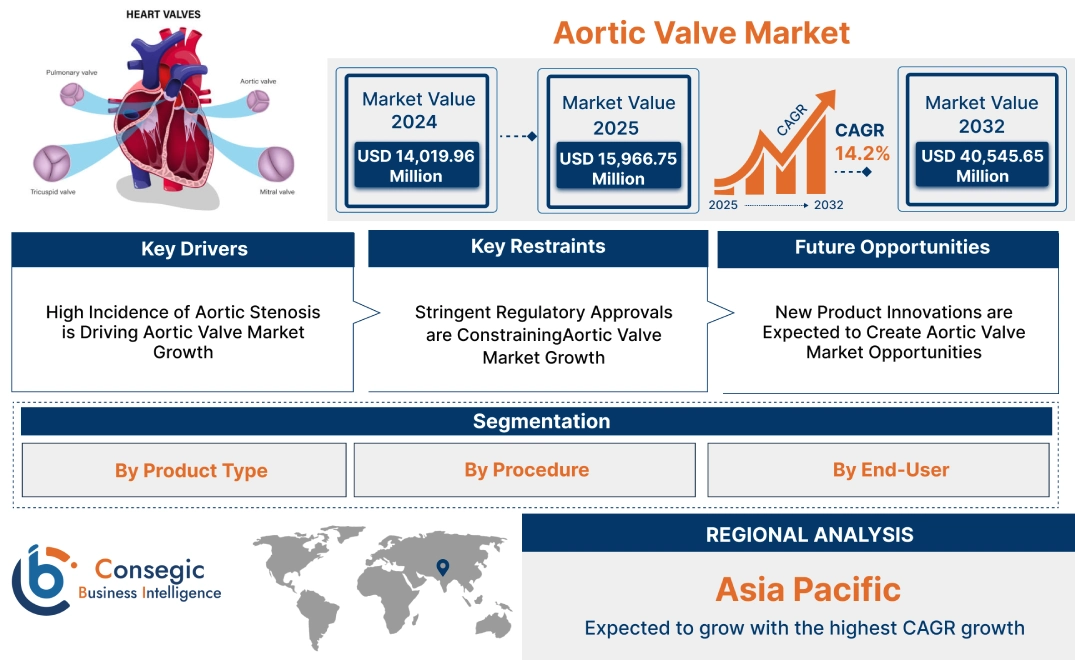

Aortic Valve Market Size:

The aortic valve market size is growing with a CAGR of 14.2% during the forecast period (2025-2032), and the market is projected to be valued at USD 40,545.65 Million by 2032 from USD 14,019.96 Million in 2024. Additionally, the market value for the 2025 attributes to USD 15,966.75 Million.

Aortic Valve Market Scope & Overview:

Aortic valve is a medical device which used to replace the damaged aortic valve in the patients. It mainly consists of leaflets or cusps, suture ring, and occluder disc. The aortic valve is of two types mechanical and biological. Further, mechanical valve consists of carbon or titanium and other sturdy materials while biological valve is made of cow tissue, pig tissue or human tissue. Aortic valve helps in restoring normal blood flow from the left ventricle to the aorta in patients. It is implanted through open surgery and and minimally invasive surgery. Moreover, aortic valve is utilized by hospitals, cardiac centers, ambulatory surgical centers, and others in the treatment of aortic stenosis and aortic regurgitation.

How is AI Transforming the Aortic Valve Market?

AI is being increasingly used in the development and application of aortic valve devices, particularly in transcatheter aortic valve replacement (TAVR) procedures. Moreover, AI-powered systems can analyze patient data, including echocardiograms, CT scans, and electronic health records, to improve patient selection, procedural planning, and post-operative monitoring. Additionally, AI-powered solutions can also enhance the accuracy of valve sizing and predict outcomes, potentially leading to improved patient outcomes and reduced complications. Therefore, the above factors are expected to positively impact the market growth in upcoming years.

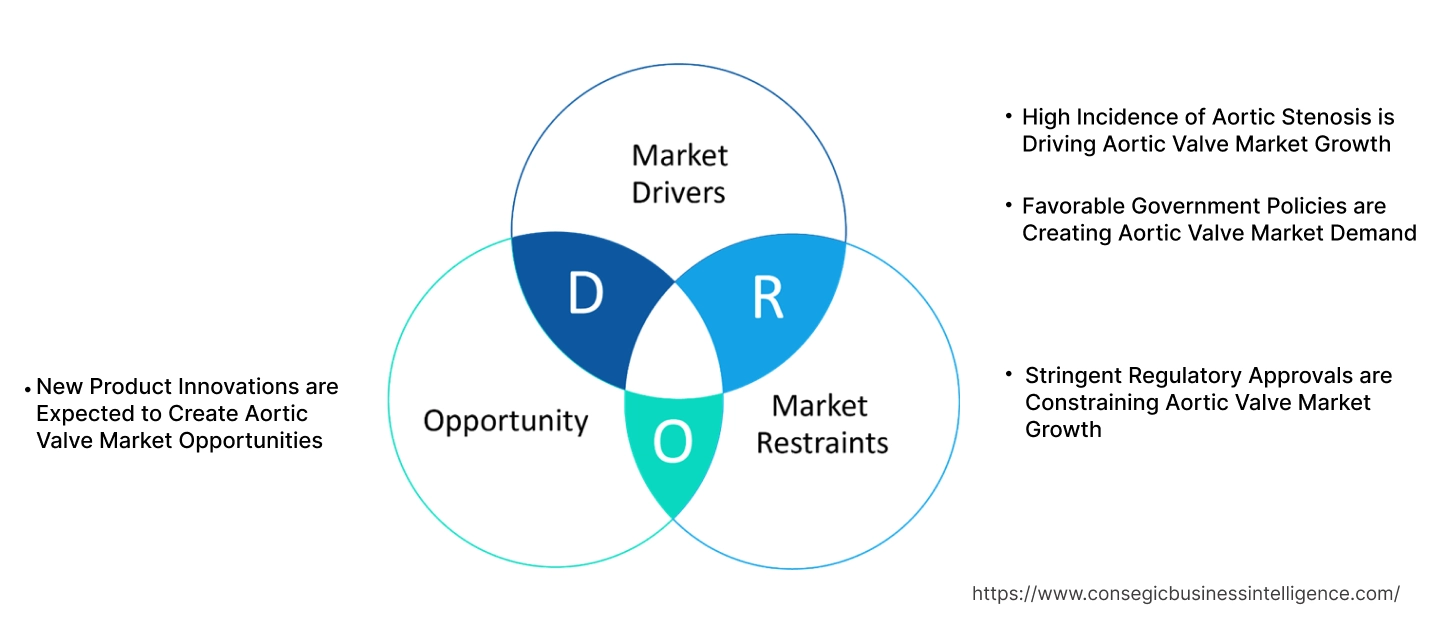

Aortic Valve Market Dynamics - (DRO) :

Key Drivers:

High Incidence of Aortic Stenosis is Driving Aortic Valve Market Growth

Aortic stenosis is a narrowing of the aortic valve opening and restricts the blood flow from the left ventricle to the aorta. Aortic valve is a device which replaces the damaged tissues of the aortic stenosis and restores the blood flow from the left ventricle to the aorta. The incidence of aortic stenosis is increasing due to several factors such as high blood pressure, diabetes, and chronic kidney disease, further driving the market.

- According to research article published by National Center of Biotechnology Information, in 2024, the incidence rate of aortic stenosis is 52.5% per 1,00,000 patient in the United States. This high prevalence of aortic stenosis is driving the adoption of aortic valve in the treatment.

Thus, the high incidence of aortic stenosis is leading to aortic valve market demand.

Favorable Government Policies are Creating Aortic Valve Market Demand

Favorable government policies are major driver in the market. It includes increasing reimbursement for surgical valve repair including aortic valve. The reimbursement is increased by updating current reimbursement rates according to the expenditure. This is helping more patients to opt for surgical treatment options. Further, the government is also investing in the payments for surgical valve procedures to enhance treatment access among the patients.

- In 2024, Edwards Lifesciences Corporation published an article stating Medicare Severity Diagnosis Related Group (MS-DRG) payments for surgical valve procedures have increased by 27.2% since 2016. This increased payment is enhancing the patient’s access to aortic valve for the treatment of aortic regurgitation.

Hence, favorable government policies are leading to aortic valve market expansion.

Key Restraints:

Stringent Regulatory Approvals are Constraining Aortic Valve Market Growth

The aortic valve is a medical device and hence their manufactures must adhere to regulatory standards for safety, performance and biocompatibility. Authorities such as United States Food and Drug Administration, European Medicines Agency (EMA) impose rigorous testing and documentation requirement for this valve before it is approved for clinical use. These regulations ensure that the aortic valve does not cause harm, function effectively in treatment and meet the required quality standards. The approval process involves multiple stages, including preclinical trials, testing, biocompatibility evaluations and clinical trials, which are time-intensive and costly. It typically causes delays due to lengthy evaluations of additional requirements for compliance. Thus, stringent regulatory approvals are constraining the market demand due to increased costs and limited availability of advanced technology.

Future Opportunities :

New Product Innovations are Expected to Create Aortic Valve Market Opportunities

Product innovations are increasing the applicability of aortic valve. It includes frame markers and bovine pericardium. Frame markers are ensuring precise implantation and ease of deployment. Bovine pericardium is increasing the durability and reliability of the valve. Moreover, companies are also developing valves with advanced design.

- In 2024, SMT Launches Hydra aortic valve in Mexico. It features supra-annular design which delivers a larger effective valve area for improved patient recovery and quality of life. Lower risks during operation and improved patient outcomes will further boost the adoption of this hydra aortic valve.

Thus, product innovations such as supra-annular design are expected to create aortic valve market opportunities.

Aortic Valve Market Segmental Analysis :

By Product Type:

Based on product type, the market is categorized into mechanical and biological.

Trends in Product Type

- According to aortic valve market trends, mechanical valve has better durability and reduces the chance of valve replacement in the patients.

- Demand for biological valve is growing among the patients due to reduced dependency on blood-thinner medication as per market trends.

The mechanical segment accounted for the largest market share in the year 2024.

- Mechanical valve is a type of aortic valve which is made from a special type of carbon or titanium and other sturdy materials.

- It contains two carbon leaflets mounted in a ring covered with polyester knit fabric.

- Mechanical valve is extensively utilized due to its long-lasting impact and durability in improving patients’ blood flow. It also reduces the chance of valve replacement due to its durability.

- Mechanical valve is usually recommended for the younger patients aged less than 50 to reduce the chance of valve replacement. Increasing cases of aortic regurgitation in younger patients is driving the segment.

- Hence, mechanical valve is dominating segment in the market due to rising aortic regurgitation cases in younger demographics.

The biological segment is expected to grow at the fastest CAGR over the forecast period.

- Biological valve is a type of aortic valve which is made of cow tissue, pig tissue or human tissue.

- It is recommended for patients older than 60 years of age due to avoidance of blood-thinner medication.

- Biological valve also prevents the development of blood clots in patients. Due to these advantages, companies are launching biological valves for the treatment of aortic stenosis or aortic regurgitation.

- For instance, in 2024, Edwards Lifesciences launched the Sapien 3 Ultra Resilia valve in Europe. It is a biological aortic valve which is made of bovine pericardial tissue. This valve reduces structural valve deterioration following the procedure, further enhancing application of aortic valve.

- Thus, prevention of blood clot formation is driving the adoption of biological valve thereby driving the segment.

By Procedure:

Based on procedure, the market is categorized into open surgery and minimally invasive surgery.

Trends in Procedure

- As per aortic valve market trends, open surgery provides easier access and greater visibility of the damaged valve.

- Adoption of minimally invasive surgery is growing in the implantation of aortic valve due to less trauma and faster patient recovery as per market trends.

The open surgery segment accounted for the largest market share in the year 2024.

- Open surgery is a procedure which involves opening the chest and performing surgery on the heart's muscles, valves, or arteries.

- In this surgery, the patient is connected to the heart- lung bypass machine to maintain the blood flow during the procedure.

- In open surgery, incision is made through the middle of the chest to reach the damaged aortic valve.

- It is widely utilized for the implantation of the aortic valve device due to easy access and greater visibility of the damaged part.

- Further, open surgery also offers excellent long-term outcomes, especially for patients without high surgical risks.

- Hence, open surgery is dominating segment in the market due to easier access and greater visibility of the damaged part.

The minimal invasive surgery segment is expected to grow at the fastest CAGR over the forecast period.

- Minimally invasive surgery is a procedure which involves small 2-3-inch incisions on the right side of the chest.

- As compared to open surgery, minimally invasive surgery reduces damage to the surrounding tissues and also improves clinical outcomes.

- It provides advantages such as reduced intensive care, decreased hospital length of stay, reduced ventilation time and others.

- Due to these advantages, adoption of minimally invasive surgeries is growing in the treatment.

- For instance, according to article published by Far North Surgery, minimally invasive surgeries are projected to grow by 6.27% by the year 2030. This growth will further enhance the adoption of minimally invasive surgery in implantation of aortic valve for the treatment of aortic stenosis.

- Thus, faster recovery and reduced damage to the surrounding tissues is driving the adoption of minimally invasive surgery in the market thereby driving the growth of the segment.

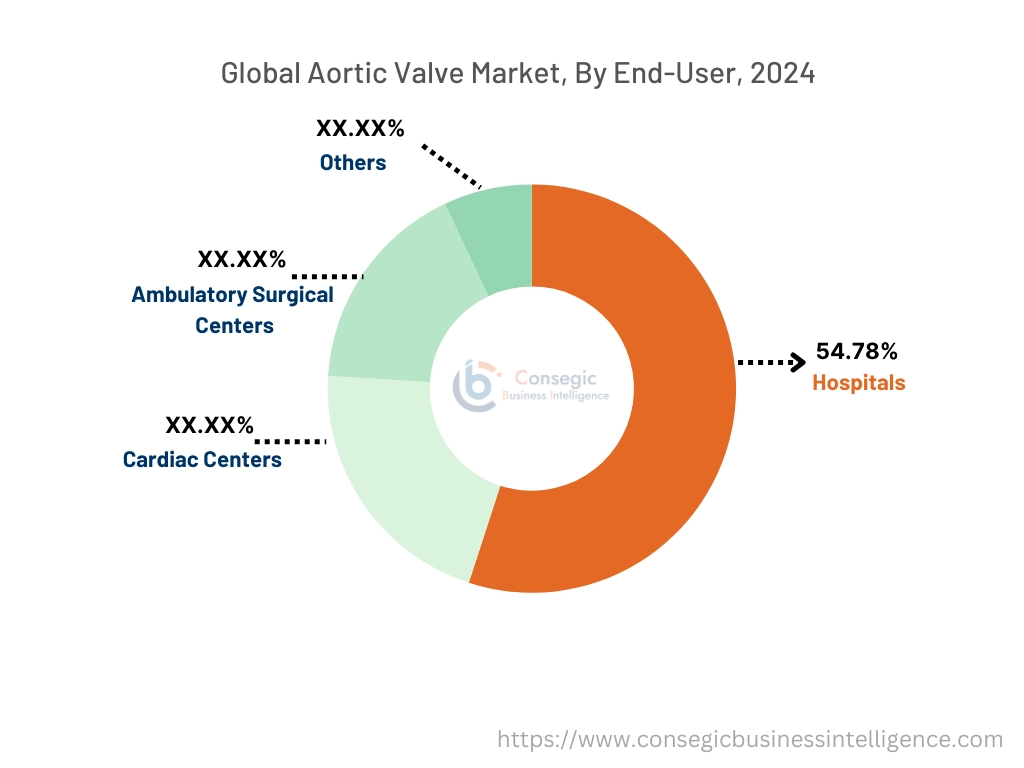

By End-User:

Based on end-user, the market is categorized into hospitals, cardiac centers, ambulatory surgical centers, and others.

Trends in End-User

- As per market trends, hospitals widely used aortic valve in the treatment of aortic stenosis or congenital defects.

- Adoption of aortic valve by ambulatory surgical center is growing due to increasing shift towards outpatient settings as per market trends.

The hospitals segment accounted for the largest market share of 54.78% in the year 2024.

- Aortic valve is widely used in the hospitals for the treatment of aortic stenosis or congenital aortic valve defect.

- Hospitals are widely preferred by the patients due to advanced technology, well-developed infrastructure and skilled healthcare professionals.

- Further, hospitals are incorporating newer procedures for the aortic valve implantation in the patients.

- For instance, in 2022, GB Pant Hospital implanted aortic valve in the patient with Ozaki procedure. This procedure uses the outer covering of the heart to develop aortic valve and has fewer complication rates as compared to the normal procedure.

- Thus, hospitals are dominating segment in the market due to adoption of advanced technology and innovative procedures.

The ambulatory surgical centers segment is expected to grow at the fastest CAGR over the forecast period.

- Ambulatory surgical centers (ASCs), are modern medical facilities specializing in outpatient surgical procedures.

- The adoption of aortic valve is growing in ambulatory surgical centers particularly for minimally invasive surgery.

- The shift towards outpatient settings is driven by advancements in surgical techniques and imaging technology such as 3D echocardiography, cardiac magnetic resonance imaging, and others.

- This has contributed to the growing role of ambulatory surgical centers in the adoption of aortic valve for the treatment of aortic stenosis or congenital aortic defects.

- Thus, consumer preference towards outpatient services is growing due to faster recovery and improved clinical outcomes thereby driving the growth of the segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2024, North America accounted for the highest market share at 38.97% and was valued at USD 5,463.58 Million and is expected to reach USD 14,690.33 Million in 2032. In North America, United States accounted for the highest market share of 72.08% during the base year of 2024. The aortic valve market share of the North America region is major due to technological advancements. Technological advancements in valve design and surgical techniques have enhanced the applicability of aortic valve. Moreover, companies are developing valve with advanced features for easy implantation further driving the market.

- In 2022, Medtronic launched EVOLUT aortic valve in the United States. It features Evolut platform to enhance ease-of-use and predictable valve deployment for physicians. Further, this aortic valve enhances the implantation through direct visualization of commissure alignment and redesigned catheter tip for a smoother insertion profile.

Thus, North America is leading in the market due to technological advancements and advanced healthcare technology as per analysis.

Asia-pacific is expected to witness the fastest CAGR of 16.2% over the forecast period during 2025-2032. According to aortic valve market analysis, the Asia Pacific region is growing rapidly driven by rising prevalence of cardiovascular diseases. Countries such as China, India, Japan, and South Korea are major contributors in the market due to growing cases of aortic stenosis and congenital heart disease. The increasing number of hospitals and cardiac centers is further driving the adoption of aortic valve in the treatment of patients. Hence, theaortic valve market share of Asia Pacific is experiencing rapid growth through rising prevalence of cardiovascular diseases as per market analysis.

According to aortic valve market analysis, Europe region is experiencing steady growth in the market driven by increasing heath expenditure. The region is well developed with modern diagnostic technology and skilled cardiologists along with digital healthcare infrastructure. The government in the region is also investing in research and development of aortic valve with advanced features for faster patient recovery and easy implantation during surgical procedures. It is further leading to aortic valve market expansion in the region.

The Middle East and Africa region is experiencing gradual demand in the market, driven by increasing awareness about cardiac health and improving healthcare industry. Countries such as Dubai, UAE, and South Arica are major contributors in the market where advanced hospitals and government organizations provide access to advanced treatments including aortic valve. Further, the ambulatory surgical centers in the region are offering minimally invasive surgery for less trauma and improved clinical outcomes as per analysis.

As per analysis, the market in Latin America is driven by rising disposable income and growing population. Countries such as Brazil, Mexico and Argentina are major contributors in the region due to modern healthcare infrastructure. The rise of diagnostic centers and private clinics has significantly impacted the availability of advanced cardiac diagnostic methods for aortic stenosis. Additionally, patients in the region are preferring biological valve for less complications and faster recovery.

Top Key Players and Market Share Insights:

The aortic valve industry is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global aortic valve market. Key players in aortic valve industry include-

- Boston Scientific Corporation (United States)

- Medtronic (Ireland)

- LivaNova PLC (United Kingdom)

- Abbott (United States)

- Artivion, Inc (United States)

- Edwards Lifesciences Corporation (United States)

- Biotronik (Germany)

- Colibri Heart Valve (United States)

- CryoLife, Inc. (United States)

- Micro Interventional Devices, Inc. (United States)

Recent Industry Developments :

Partnerships & Collaborations:

- In 2024, Meril Life Sciences Pvt. Ltd. launched transcatheter aortic valve. It introduced low frame foreshortening and enhanced operator control. Further, it also enables precise deployment for improved procedural predictability.

Mergers and Acquisitions

- In 2024, Edwards Lifesciences acquired JenaValve and Endotronix. This acquisition strengthened the product portfolio of Edward’s aortic valve for treatment of aortic regurgitation and heart failure.

Aortic Valve Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 40,545.65 Million |

| CAGR (2025-2032) | 14.2% |

| By Product Type |

|

| By Procedure |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the aortic valve market? +

In 2024, the aortic valve market is USD 14,019.96 million.

Which is the fastest-growing region in the aortic valve market? +

Asia Pacific is the fastest-growing region in the aortic valve market.

What specific segmentation details are covered in the aortic valve market? +

Product Type, Procedure, and End-User are covered in the aortic valve market.

Who are the major players in the aortic valve market? +

Boston Scientific Corporation (United States), Medtronic (Ireland), and LivaNova PLC (United Kingdom) are some of the major players in the market.