- Summary

- Table Of Content

- Methodology

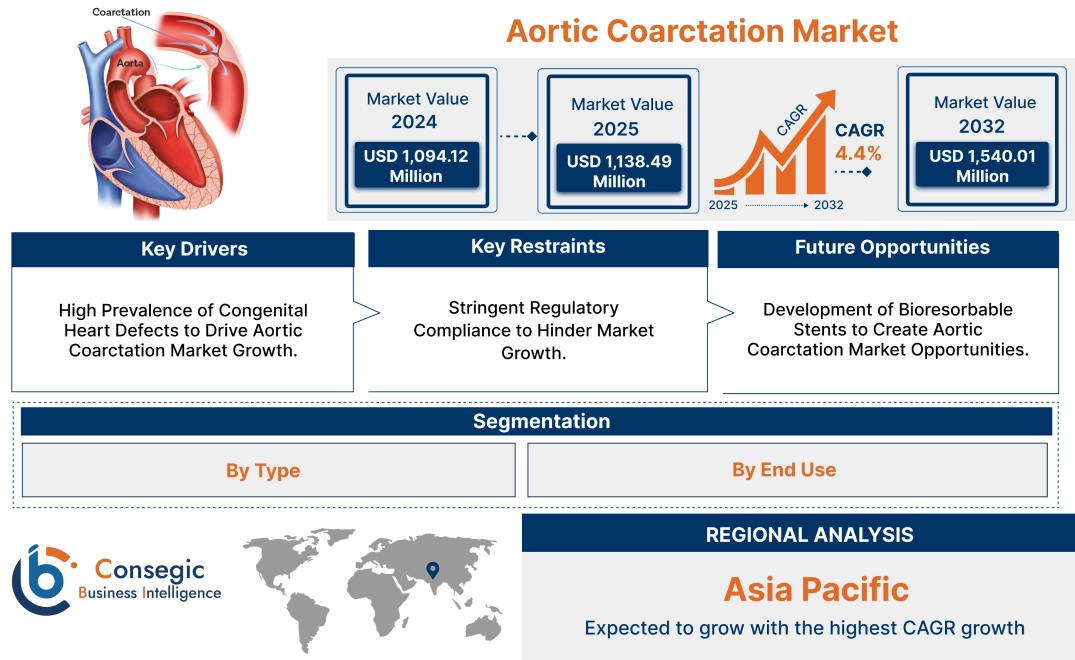

Aortic Coarctation Market Size:

The Aortic Coarctation Market size is growing with a CAGR of 4.4% during the forecast period (2025-2032), and the market is projected to be valued at USD 1,540.01 Million by 2032 from USD 1,094.12 Million in 2024. Additionally, the market value for 2025 attributed to USD 1,138.49 Million.

Aortic Coarctation Market Scope & Overview:

Aortic coarctation is a narrowing of the aorta. It is a heart defect that is present at birth. Aorta is the major artery responsible for systemic blood circulation. Coarctation of the aorta occurs between the upper body branches and the lower body branches. This constriction of aorta impedes blood flow. This further causes increased strain on the heart. Symptoms of coarctation of the aorta include irritability, pale skin, sweating, rapid breathing, enlarged liver, poor feeding, cold extremities, weak foot pulses, higher arm blood pressure than leg blood pressure, chest pain, and leg pain during walking. The condition is diagnosed using echocardiography, chest X-ray, cardiac MRI & CT scan, and others. Treatment strategies encompass medications and surgical intervention focused on alleviating the aortic narrowing.

Aortic Coarctation Market Dynamics - (DRO) :

Key Drivers:

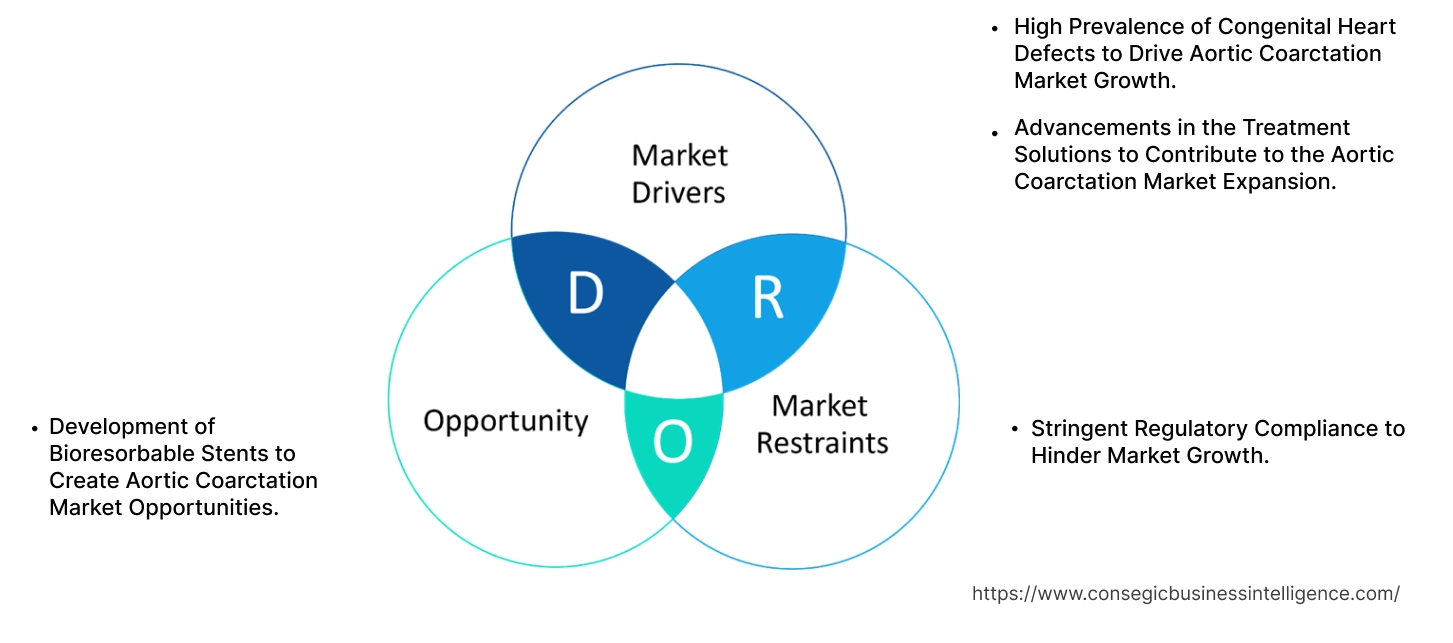

High Prevalence of Congenital Heart Defects to Drive Aortic Coarctation Market Growth.

The high prevalence of congenital heart defects (CHD) in infants is driving upward trajectory of the market. A congenital heart defect is a structural abnormality of the heart that's present at birth. Aortic coarctation is a type of CHD. The high incidences of these heart defects result in more cases of coarctation of aorta.

- For instance, according to the 2024 data from S Centers for Disease Control and Prevention, it is stated that each year approximately 40,000 babies are born in the United States with a congenital heart defect. This equals 1 child every 15 minutes. About 1 in 4 babies with a heart defect have a critical heart defect that requires surgery or other procedures in their first year of life.

This prevalence directly leads to the detection of more cases of aortic coarctation. As the diagnosis of CHDs improves, more cases of coarctation of the aorta are identified. This impacts the demand for effective solutions for diagnosis, treatment, and ongoing management of the condition further propelling the market growth.

Advancements in the Treatment Solutions to Contribute to the Aortic Coarctation Market Expansion.

The adoption of advanced treatment solutions such as minimally invasive surgeries are contributing to the improvement in patient outcomes. Procedures such as balloon angioplasty and stenting are advancing the treatment for coarctation of the aorta. These catheter-based interventions offer several advantages. Some of the advantages include smaller incisions, reduced pain and scarring, and faster recovery times. In addition to this, improvement in stent technology such as drug eluting stents and covered stents are further enhancing treatment outcomes. These advantages of minimally invasive stenting are leading to the development of innovative stents for coarctation of the aorta.

- For instance, in August 2024,Renata Medical received U.S. Food and Drug Administration (FDA) approval for its Minima Growth Stent. This first-of-its-kind stent is designed specifically for neonates, infants, and young children and is unique in its ability to be re-expanded as the child grows. Minima Stent represents a minimally invasive solution that is designed to be expanded over the course of the child’s life.

As a result, the advancements in the treatment options are contributing to aortic coarctation market expansion.

Key Restraints:

Stringent Regulatory Compliance to Hinder Market Growth.

Stringent regulatory standards imposed by government agencies and international organizations worldwide cause barriers in the market. Regulatory bodies such as Food and Drug Administration and European Medicines Agency among others impose long process for approvals of diagnostic devices and treatment solutions. This involves lengthy documentation, product safety assessment, and rigorous quality control procedures. It leads to increase production costs and slow down product development. Additionally, regulatory authorities and regulatory standards differ by country and region. This creates limitations for researchers and companies operating in multiple jurisdictions. Thus, the impact of these stringent regulations on the aortic coarctation market trend is multifaceted.

Future Opportunities :

Development of Bioresorbable Stents to Create Aortic Coarctation Market Opportunities.

The development of bioresorbable stents presents an opportunity for an upward trajectory of the market over the forecast period. A bioresorbable stent is a tube-shaped device that opens blocked arteries and then dissolves or is absorbed by the body. Bioresorbable stents offer several advantages over traditional stents. One of the most significant benefits is their ability to reduce the risk of in-stent restenosis. By gradually dissolving or degrading over time. Hence, these stents minimize the presence of a foreign body in the artery. This results in improved long-term outcomes. Considering these advantages, more effective and reliable bioresorbable stents are being developed.

- For instance, in October 2024, medical technology innovators at Massachusetts Institute of Technology received USD 50,000 award to help commercialize 3D printed, polymeric auxetic stent to treat pediatric aortic coarctation. It is a bioresorbable stent that reduces the need for frequent reinterventions.

Thus, developments towards bioresorbable are creating an upward market trajectory over the upcoming period.

Aortic Coarctation Market Segmental Analysis :

By Type:

Based on type, the market is bifurcated into diagnosis and treatment.

Trends in the Type:

- Adoption of prenatal ultrasound technology is a trend allowing earlier intervention and better management of the condition.

- Advancements in stent technology such as drug-eluting stents and covered stents are improving the outcomes of angioplasty procedures.

The treatment segment accounted for the largest market share in 2024 and is also expected to grow the fastest CAGR over the forecast period.

- Treatment type holds the dominant share in the market. The segment is further bifurcated into medications and surgery.

- Managing aortic coarctation depends on patient age and severity. Critically ill newborns require immediate stabilization with prostaglandin (PGE-1) to reopen the ductus arteriosus. Additionally, anti-hypertensive medications are used to manage high blood pressure caused by aortic constriction.

- Surgical techniques include resection and anastomosis, extended resection, and patch aortoplasty. Transcatheter therapy with balloon and stent angioplasty is the procedure widely used for the treatment of coarctation of aorta in older children.

- Innovations in medical devices and procedures such as use of covered stents are driving the upward trajectory of the treatment segment.

- For instance, according to research analysis published on NCBI in 2021, it is found that coarctation stenting with covered stents demonstrates effectiveness in maintaining obstruction relief for up to 60 months post-implantation. The study also noted a reduction in the number of patients requiring antihypertensive medication following the procedure.

- Collectively, aforementioned factors support upward trajectory of treatment segment in the overall aortic coarctation market demand.

By End-Use:

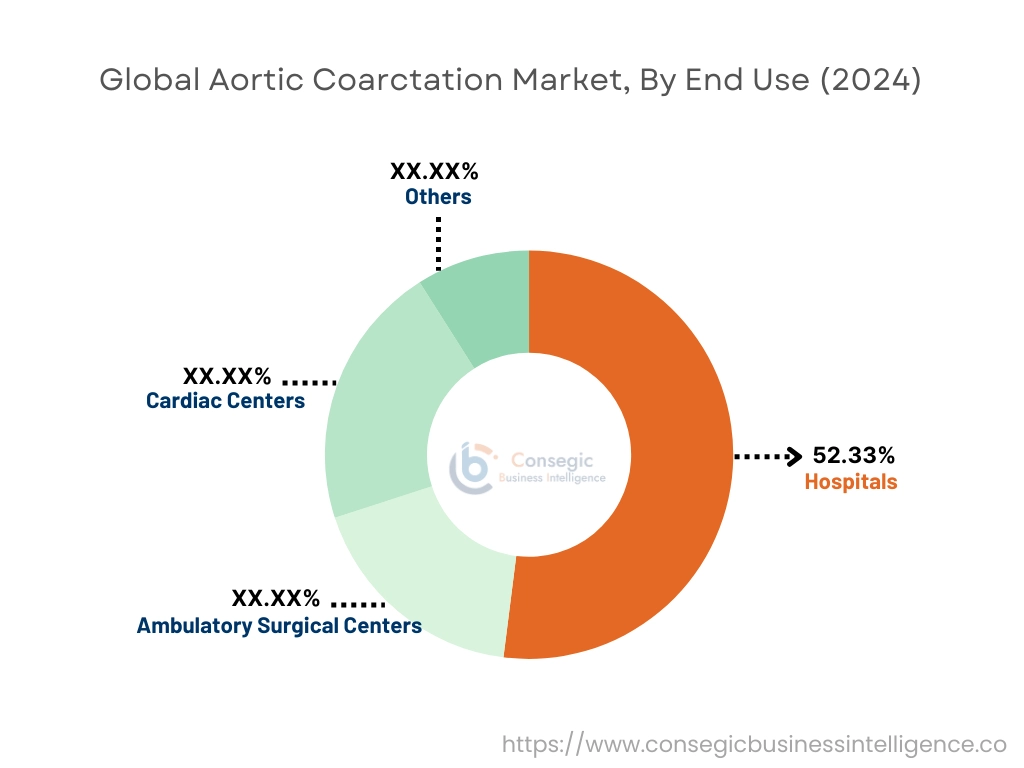

Based on end use, the market is categorized into hospitals, ambulatory surgical centers, cardiac centers, and others.

Trends in the End Use:

- There is a trend of shift towards ambulatory surgical centers for minimally invasive procedures due to cost-effectiveness and convenience.

- The use of remote monitoring technology is a growing trend, allowing healthcare providers to track patients' progress after treatment.

The hospitals segment accounted for the largest market share of 52.33% in 2024.

- Hospitals provide expertise, advanced infrastructure, well-established systems amongst others to diagnose and treat this condition.

- The complex nature of surgical procedures requires specialized infrastructure, advanced equipment and intensive care units for patient care.

- These procedures and conditions also necessitate teams that include highly skilled cardiologists, surgeons, and other specialists like nurses and technicians. Hospitals are well equipped to provide these teams.

- Furthermore, hospitals serve as central hubs for patients with coarctation in aorta. They are also involved in adopting advanced solutions for patient care.

- For instance, in September 2021, Fortis Escorts Heart Institute, a unit of the Fortis Hospital chain, India announced the launch of a dedicated Aorta Centre for the diagnosis and treatment of aortic diseases including aortic coarctation. The new hospital offers surgical interventions, endovascular interventions, radiological diagnosis, and facilities for hybrid interventions.

- This analysis positions the hospitals as a key end user segment within the dynamic market.

The ambulatory surgical center segment is expected to grow at the fastest CAGR in the forecast years.

- The ambulatory surgical center (ASC) end user is expected to hold growing contribution to the market.

- ASCs have the ability to provide effective and specialized care. They provide surgical procedures in less resource-intensive environments. This allows for quicker recovery and cost-effective solutions for the patient.

- Patients benefit from this setting as it offers minimally invasive surgery. Additionally, these facilities consist of advanced technology and specialized equipment. This helps them to deliver high-quality care and maintain a personalized approach.

- Thus, based on the market factor, the aforementioned factors contribute to ambulatory surgical centers as prominent end-users.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

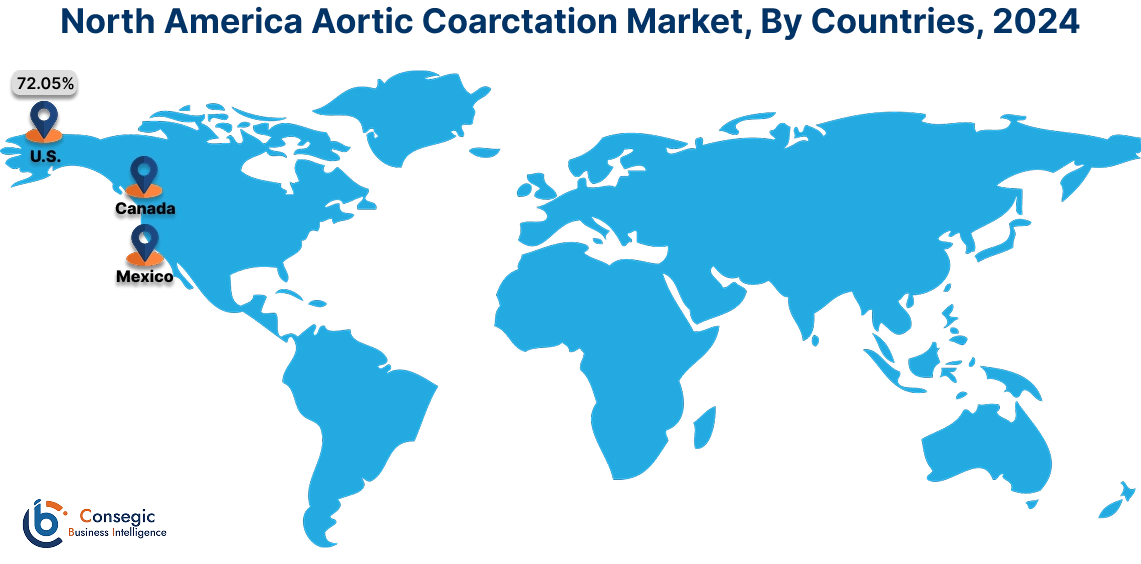

In 2024, North America accounted for the highest Aortic Coarctation market share at 40.23% and was valued at USD 440.16 Million and is expected to reach USD 605.69 Million in 2032. In North America, the U.S. accounted for the largest share of 72.05% during the base year of 2024.

The rising incidences of congenital heart defects is the key factor that is leading to the aortic coarctation market demand in North America. This creates demand for advanced diagnostic and treatment options. In addition to this, the region has well-developed healthcare system. This provides readily available access to specialized cardiac care, including interventional procedures and surgery. Moreover, the high healthcare industry expenditure including reimbursement benefits further supports the adoption of these advanced diagnostic and treatment technologies.

- For instance, based on the analysis published by the S. Centers for Medicare & Medicaid Services in December 2024, US Medicare spending rose 8.1% to USD 1,029.8 billion, while Medicaid spending increased 7.9% to USD 871.7 billion in 2023. Medicare offers health coverage to senior citizens, while Medicaid serves individuals with low incomes.

The combination of the aforementioned factors is driving growth in the North American market.

In Asia Pacific the aortic coarctation market analysis is experiencing the fastest growth with a CAGR of 5.1% over the forecast period. Increasing awareness of congenital heart defects serves a prominent role aortic coarctation market growth in Asia Pacific. The region is experiencing improvements in healthcare infrastructure. This includes the development of specialized cardiac centers and rise in access to diagnostic and treatment facilities. Rising awareness among healthcare providers leads to earlier detection of CHDs, including coarctation of aortic. This supports the increase in the number of cases identified and thus the demand for treatment. As a result, medical centers are focusing on adoption of advanced diagnostic and treatment solutions for the coarctation of the aorta, further supporting aortic coarctation market opportunities in Asia Pacific.

Europe makes a significant contribution to aortic coarctation market share. The European healthcare industry is mature. This creates a constant need for advanced solutions. Minimally invasive procedures are being prioritized, driven by investments in advanced imaging, robotics, and others. These advancements offer improved patient outcomes, such as reduced infection risk, less post-operative pain, and shorter hospital stays. Additionally, many European countries have strong public healthcare systems that provide access to quality healthcare services, including those for coarctation of aortic further propelling the market. Thus, the rise in demand for minimally invasive surgeries is influencing the market trends.

Ongoing advancements in healthcare infrastructure, including enhanced access to healthcare facilities and improved diagnostic capabilities, are contributing to better disease detection and treatment of coarctation of the aorta across Latin America. Increased healthcare expenditure is enabling greater access to healthcare services, including medications and diagnostic tests. Thus, as per analysis, these factors are influencing the aortic coarctation market analysis across Latin America.

The Middle East and Africa (MEA) region is witnessing contribution aortic coarctation market trends. The growing healthcare sector in the Middle East is playing a pivotal role in demand. Many countries in the MEA region are investing in developing their healthcare infrastructure with advanced diagnostic and treatment facilities. This includes building hospitals, and clinics, and improving access to diagnostic tools which are essential for detecting this heart defect. The combined impact of these factors is creating a favorable environment for the trajectory of the market for aortic coarctation in the MEA region.

Top Key Players & Market Share Insights:

The global Aortic Coarctation Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Aortic Coarctation market. Key players in the Aortic Coarctation industry include-

- RENATA MEDICAL (United States)

- Andramed GmbH (Germany)

- Artivion, Inc (United States)

- Terumo Corporation (Japan)

Recent Industry Developments :

Product Approval:

- In August 2024,Renata Medical received U.S. Food and Drug Administration (FDA) approval for its Minima Growth Stent. This first-of-its-kind stent is designed specifically for neonates, infants, and young children and is unique in its ability to be re-expanded as the child grows. Minima Stent represents a minimally invasive solution that is designed to be expanded over the course of the child’s life.

Aortic Coarctation Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,540.01 Million |

| CAGR (2025-2032) | 4.4% |

| By Type |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Aortic Coarctation market? +

In 2024, the Aortic Coarctation market is USD 1,094.12 Million.

Which is the fastest-growing region in the Aortic Coarctation market? +

Asia Pacific is the fastest-growing region in the Aortic Coarctation market.

What specific segmentation details are covered in the Aortic Coarctation market? +

By Type and End Use segmentation details are covered in the Aortic Coarctation market.

Who are the major players in the Aortic Coarctation market? +

B. Braun (Germany), NuMED (United States), RENATA MEDICAL (United States), Andramed GmbH (Germany) are some of the major players in the market.