- Summary

- Table Of Content

- Methodology

Anti-wear Additives Market Size:

Anti-wear Additives Market size is estimated to reach over USD 926.25 Million by 2032 from a value of USD 760.26 Million in 2024 and is projected to grow by USD 765.72 Million in 2025, growing at a CAGR of 2.5% from 2025 to 2032.

Anti-wear Additives Market Scope & Overview:

The anti-wear additives are chemical compounds added to lubricants and oils to minimize friction, reduce wear, and enhance the lifespan of machinery and equipment. These additives form protective films on metal surfaces, preventing direct contact under high pressure and extreme operating conditions. Key characteristics of anti-wear additives include thermal stability, high performance under heavy loads, and compatibility with a variety of lubricants such as engine oils, hydraulic fluids, and industrial lubricants. The benefits include extended equipment life, improved operational efficiency, and reduced maintenance costs. Applications span automotive engines, industrial machinery, hydraulic systems, and aerospace components, where reliable lubrication and wear protection are essential. End-users include automotive manufacturers, industrial machinery producers, and aerospace companies, driven by increasing demand for high-performance lubricants, rapid industrialization, and advancements in additive technologies to meet stringent performance standards.

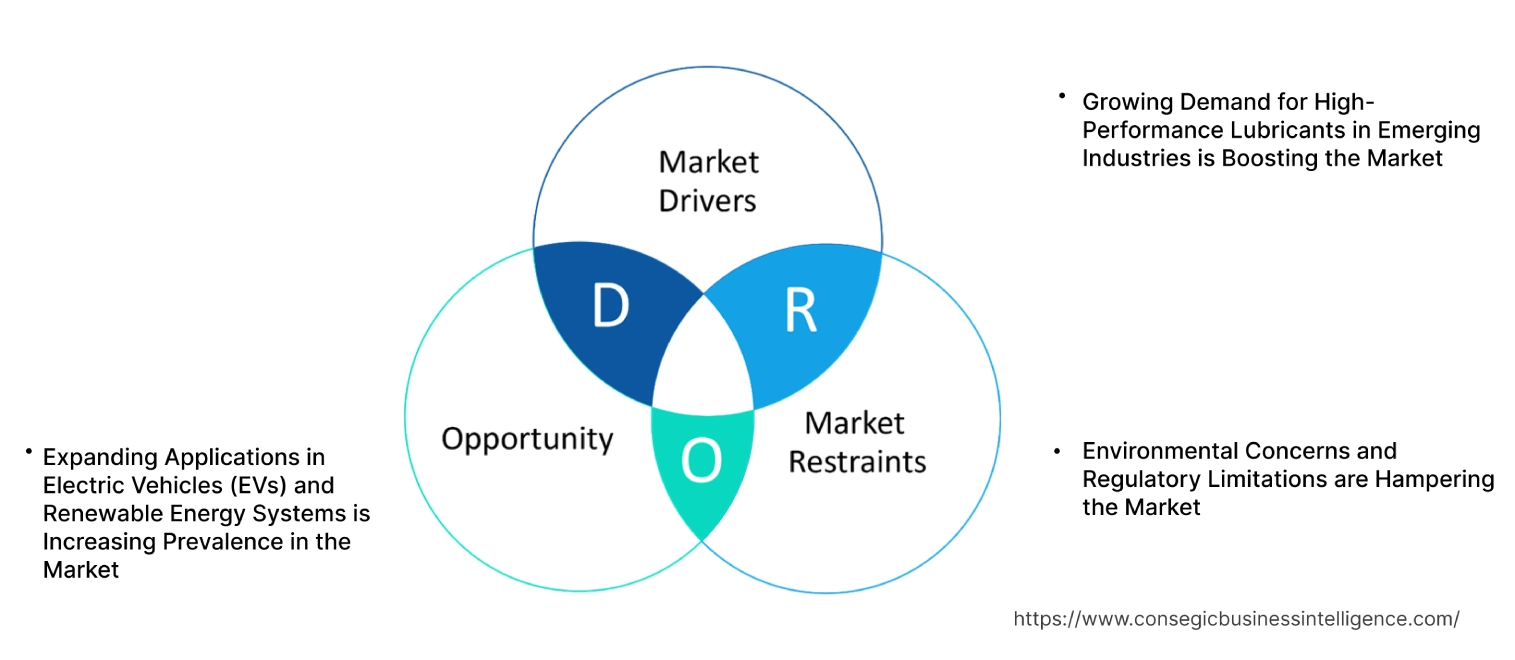

Anti-wear Additives Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for High-Performance Lubricants in Emerging Industries is Boosting the Market

High-performance lubricants, enhanced with anti-wear additives, are increasingly being adopted across emerging industries such as aerospace, renewable energy, and marine. These industries require lubricants capable of withstanding extreme conditions, including high loads, varying temperatures, and continuous operation, where anti-wear additives play a pivotal role in minimizing friction and reducing equipment wear. In renewable energy systems like wind turbines, these additives protect gearboxes and other critical components, ensuring prolonged operational life and efficiency.

Trends in industrial advancements and technological innovations are driving the use of specialized lubricants in heavy-duty applications, where precision and reliability are paramount. The analysis highlights that industries prioritizing efficiency, performance, and minimal downtime rely heavily on anti-wear solutions to improve machinery longevity, reduce maintenance costs, and meet operational standards in highly demanding environments.

Key Restraints:

Environmental Concerns and Regulatory Limitations are Hampering the Market

The anti-wear additives market faces increasing scrutiny due to environmental concerns and regulatory restrictions on certain formulations, particularly zinc-based additives like zinc dialkyl dithiophosphate (ZDDP). These additives, while effective in providing wear protection, can contribute to environmental pollution, including aquatic toxicity and emissions system degradation. Regulatory agencies in regions such as Europe and North America have imposed limitations on the use of such additives, forcing manufacturers to reassess their formulations.

These restrictions create challenges for lubricant producers, who must balance performance with sustainability. Developing eco-friendly alternatives that comply with strict environmental guidelines, while maintaining the same level of anti-wear efficiency, is a costly and time-consuming process. Trends in regulatory compliance and environmental stewardship highlight the need for innovation in greener and safer anti-wear additives to meet evolving industry standards.

Future Opportunities :

Expanding Applications in Electric Vehicles (EVs) and Renewable Energy Systems is Increasing Prevalence in the Market

The transition toward electric vehicles (EVs) and renewable energy systems has created new opportunities for anti-wear additives. In EVs, specialized lubricants containing anti-wear additives are essential for protecting critical components like bearings, transmissions, and electric motor systems, which operate under unique loads and temperatures. As EV adoption continues to rise, the need for lubricants that enhance performance, efficiency, and durability will grow, positioning anti-wear additives as a vital component in the evolving automotive sector.

Additionally, renewable energy systems, including wind turbines and solar energy installations, rely on anti-wear additives to ensure the longevity and reliability of mechanical components subjected to continuous stress. Trends in clean energy and sustainability emphasize the importance of reliable lubrication solutions to minimize wear, reduce operational disruptions, and optimize performance. Analysis suggests that manufacturers focusing on innovative anti-wear formulations tailored for these emerging applications can capture significant anti-wear additives market opportunities in the evolving energy and mobility markets.

Anti-wear Additives Market Segmental Analysis :

By Type:

Based on type, the market is segmented into zinc dialkyl dithiophosphate (ZDDP), phosphate esters, sulfur-containing compounds, boron compounds, and others.

The zinc dialkyl dithiophosphate (ZDDP) segment accounted for the largest revenue of anti-wear additives market share in 2024.

- Zinc dialkyl dithiophosphate (ZDDP) is a widely used anti-wear additive due to its exceptional performance in protecting metal surfaces from wear and tear.

- It is extensively applied in engine oils and gear oils to enhance lubrication and extend the lifespan of automotive and industrial machinery components.

- ZDDP’s ability to form a protective layer on metal surfaces under high pressure and temperatures has made it a preferred choice in demanding applications.

- The rising demand for automotive lubricants and industrial fluids, especially in developing regions, has further driven the dominance of this segment in the market.

The boron compounds segment is anticipated to register the fastest CAGR during the forecast period.

- Boron-based anti-wear additives are gaining traction due to their excellent thermal stability, low toxicity, and environmentally friendly characteristics.

- These additives are increasingly being used as alternatives to traditional ZDDP additives, particularly in applications where regulatory compliance regarding emissions and toxicity is critical.

- Boron compounds are widely applied in transmission fluids, hydraulic fluids, and metalworking fluids to enhance wear resistance and oxidation stability.

- The growing focus on sustainable and high-performance lubricants is expected to drive the rapid adoption of boron compounds in the coming years.

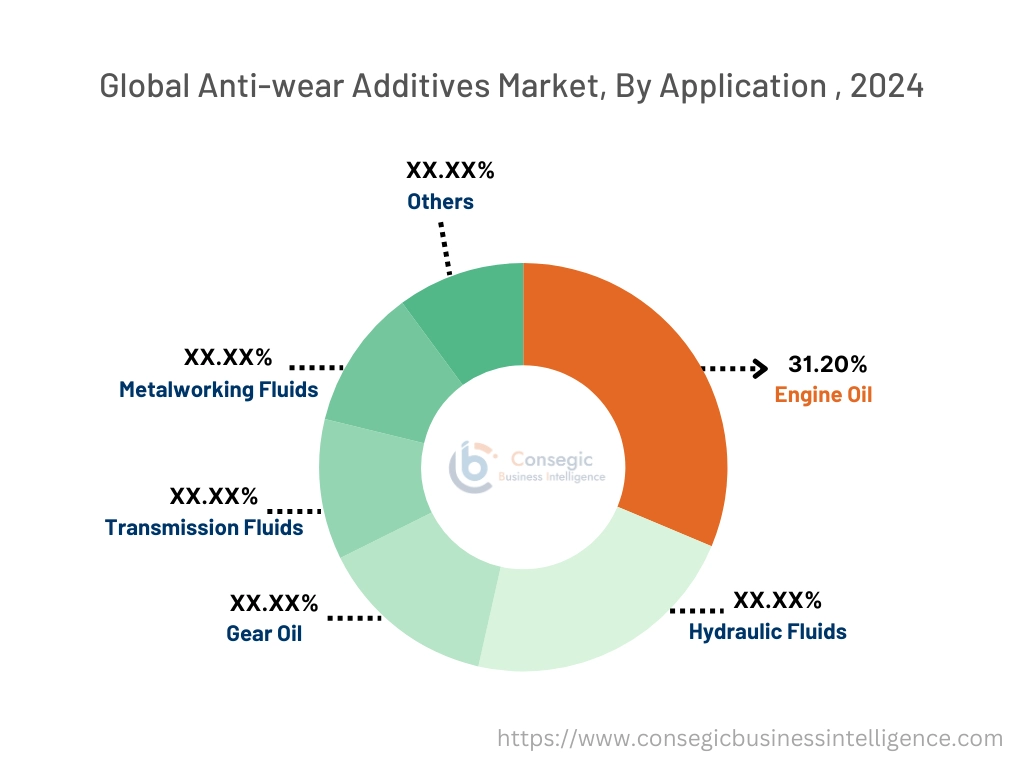

By Application:

Based on application, the anti-wear additives market is segmented into engine oil, hydraulic fluids, gear oil, transmission fluids, metalworking fluids, and others.

The engine oil segment accounted for the largest revenue of 31.20% anti-wear additives market share in 2024.

- Engine oil is the largest application area for anti-wear additives, driven by the increasing demand for automotive lubricants that can ensure superior engine performance and longevity.

- Anti-wear additives such as ZDDP and phosphate esters are crucial for minimizing friction, reducing wear, and preventing engine component failure under high-load and high-temperature conditions.

- The growing automotive sector, coupled with the rising production of passenger and commercial vehicles globally, has reinforced the anti-wear additives market demand for engine oils enhanced with additives.

- Additionally, the adoption of advanced engines in electric and hybrid vehicles has further increased the need for high-performance lubricants.

The hydraulic fluids segment is anticipated to register the fastest CAGR during the forecast period.

- Hydraulic fluids play a vital role in transmitting power in machinery and equipment across industries such as construction, industrial manufacturing, and aerospace.

- Anti-wear additives are essential for protecting hydraulic systems from wear, ensuring smooth operations, and extending equipment life.

- The increasing adoption of hydraulic systems in modern industrial and construction equipment, coupled with the anti-wear additives market trends for energy-efficient and durable fluids, has driven the growth of this segment.

- Moreover, advancements in hydraulic fluid formulations to meet stringent environmental and performance standards are expected to boost segment expansion.

By End-Use Industry:

Based on end-use, the market is segmented into automotive, aerospace, marine, industrial machinery, construction equipment, and others.

The automotive segment accounted for the largest revenue share in 2024.

- The automotive sector is a major consumer of anti-wear additives, particularly in engine oils, transmission fluids, and gear oils.

- These additives are critical for ensuring vehicle performance, fuel efficiency, and the durability of components subjected to extreme operating conditions.

- The increasing production of passenger cars and commercial vehicles, coupled with the rising adoption of electric vehicles (EVs) and hybrid vehicles, has fueled the anti-wear additives market trends for high-performance lubricants containing additives.

- Additionally, advancements in automotive technologies, including lightweight components and turbocharged engines, have further reinforced the need for enhanced lubrication solutions.

The aerospace segment is anticipated to register the fastest CAGR during the forecast period.

- The aerospace sector relies heavily on anti-wear additives to ensure the reliability and performance of critical components, including turbines, gear systems, and hydraulic systems.

- These additives play a crucial role in reducing wear, preventing equipment failure, and improving the efficiency of aerospace lubricants under extreme conditions such as high altitudes and temperatures.

- The increasing production of commercial and defense aircraft, coupled with the growing trends for fuel-efficient and high-performance lubricants, is driving significant anti-wear additives market growth in this segment.

- Furthermore, advancements in synthetic lubricants and the adoption of stringent safety and quality standards in the aerospace sectors are expected to propel the segment's rapid growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

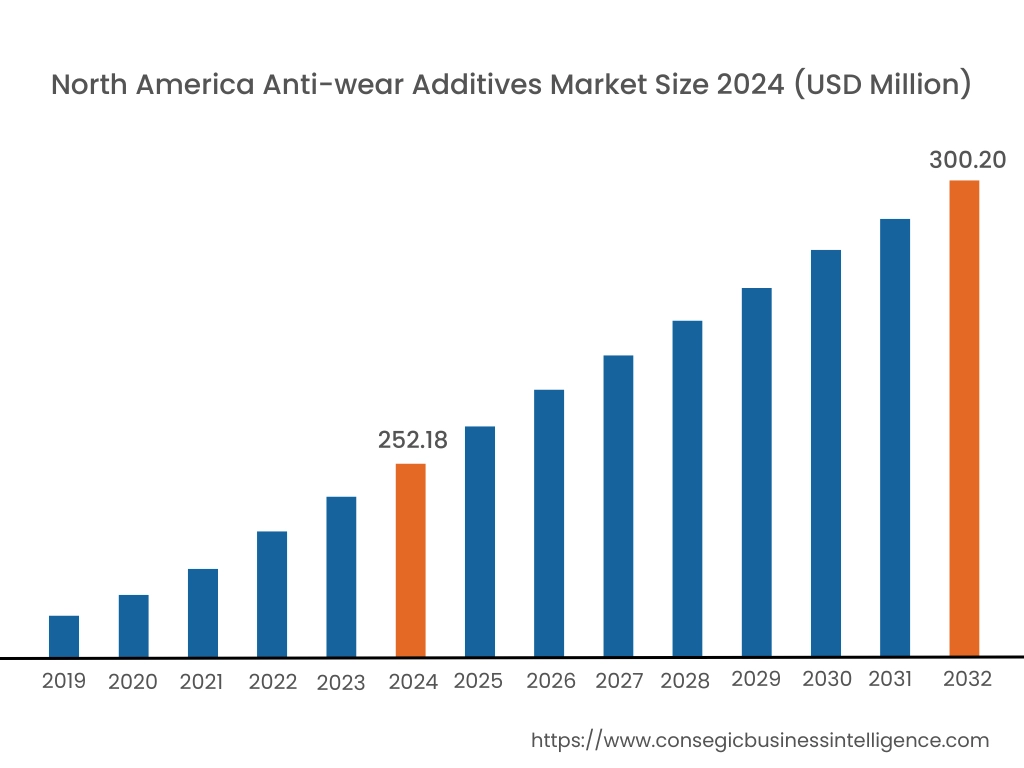

In 2024, North America was valued at USD 252.18 Million and is expected to reach USD 300.20 Million in 2032. In North America, the U.S. accounted for the highest share of 72.50% during the base year of 2024. North America holds a significant share in the anti-wear additives market analysis, driven by its well-established automotive, aerospace, and industrial sectors. The U.S. leads the region with strong trends for global anti-wear additives in engine oils, transmission fluids, and industrial lubricants to enhance equipment longevity and efficiency. The region's focus on advanced machinery in manufacturing and the growing adoption of synthetic lubricants further support the anti-wear additives market growth. Canada contributes through its increasing use of anti-wear additives in heavy machinery for mining and forestry operations. However, stringent environmental regulations on additive formulations, particularly concerning zinc-based compounds, may restrict market growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 2.9% over the forecast period. Asia-Pacific is the fastest-growing region in the anti-wear additives market analysis, fueled by rapid industrialization, urbanization, and expanding automotive and manufacturing sectors in China, India, and Japan. China dominates the market with rising trends for anti-wear additives in automotive lubricants, driven by the country’s massive vehicle production and industrial activities. India’s growing construction, automotive, and agricultural sectors further boost the use of additives in machinery and engine oils. Japan focuses on high-performance additives in advanced automotive and electronics industries. However, fluctuating raw material costs and the presence of low-cost alternatives may hinder market expansion in some areas.

Europe is a prominent market for anti-wear additives, supported by a strong automotive and industrial manufacturing base. Countries like Germany, France, and the UK are key contributors. Germany’s thriving automotive sectors drive significant trends for anti-wear additives in engine and gear oils to improve vehicle efficiency and performance. France emphasizes the use of advanced additives in industrial lubricants for manufacturing processes, while the UK focuses on eco-friendly additives for automotive and aviation sectors, aligning with sustainability goals. However, strict EU regulations regarding environmental concerns and the use of hazardous chemicals may challenge market players.

The Middle East & Africa regional analysis is witnessing steady growth in the anti-wear additives market, primarily driven by the oil & gas, construction, and mining industries. Countries like Saudi Arabia and the UAE are key contributors, adopting anti-wear additives in lubricants to ensure the efficient operation of drilling equipment and heavy machinery. In Africa, South Africa is emerging as a market, leveraging anti-wear additives for mining and industrial machinery applications. However, limited infrastructure and dependence on imports for high-quality additives may restrict broader market growth in the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. As per the analysis Brazil’s expanding automotive and industrial manufacturing sectors drive trends for anti-wear additives in engine oils and industrial lubricants. Mexico’s growing automotive sectors and investments in infrastructure projects further support market expansion. The region is also seeing an increase in agricultural machinery, which uses anti-wear additives for enhanced performance and durability. However, economic instability and inconsistent enforcement of environmental regulations may pose challenges for market players.

Top Key Players and Market Share Insights:

The anti-wear additives market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the anti-wear additives market. Key players in the anti-wear additives industry include -

- Evonik Industries (Germany)

- Tianhe Chemicals Group (China)

- Afton Chemical Corporation (USA)

- Croda International Plc (UK)

- BASF SE (Germany)

- Lubrizol Corporation (USA)

- Infineum International Limited (UK)

- Chevron Oronite Company LLC (USA)

- Vanderbilt Chemicals, LLC (USA)

Recent Industry Developments :

Collaborations:

- In October 2024, Infineum, a UK-based specialty automotive chemicals manufacturer and a joint venture between ExxonMobil and Shell, is expanding its operations in India by establishing a new blending facility. This facility will focus on producing sulfonate and salicylate packages, essential additives for automotive lubricants that provide anti-wear and anti-corrosion properties, crucial for engine protection. The facility is scheduled to commence trial production by mid-2025, with full commercial operations expected in the third quarter of 2025.

Anti-wear Additives Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 926.25 Million |

| CAGR (2025-2032) | 2.5% |

| By Type |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Anti-wear Additives Market by 2032? +

Anti-wear Additives Market size is estimated to reach over USD 926.25 Million by 2032 from a value of USD 760.26 Million in 2024 and is projected to grow by USD 765.72 Million in 2025, growing at a CAGR of 2.5% from 2025 to 2032.

What are the key drivers boosting the growth of the Anti-wear Additives Market? +

The market is driven by increasing demand for high-performance lubricants across emerging industries such as automotive, aerospace, and renewable energy, where wear reduction and operational efficiency are critical.

Which factors are hampering the growth of the Anti-wear Additives Market? +

Environmental concerns and regulatory limitations, particularly on zinc-based additives like ZDDP, hinder market growth due to their toxicity and impact on emissions systems.

What opportunities are emerging for anti-wear additives in new applications? +

Expanding applications in electric vehicles (EVs) and renewable energy systems are creating new opportunities for specialized anti-wear additives to protect bearings, transmissions, and mechanical components under unique operating conditions.