- Summary

- Table Of Content

- Methodology

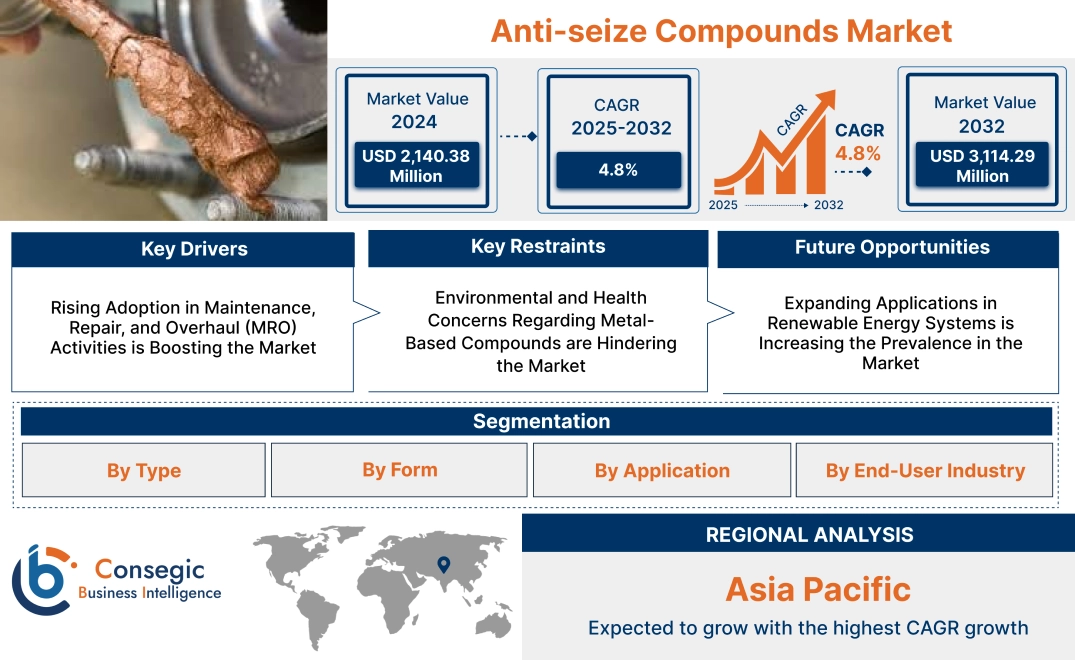

Anti-seize Compounds Market Size:

Anti-seize Compounds Market size is estimated to reach over USD 3,114.29 Million by 2032 from a value of USD 2,140.38 Million in 2024 and is projected to grow by USD 2,204.98 Million in 2025, growing at a CAGR of 4.8% from 2025 to 2032.

Anti-seize Compounds Market Scope & Overview:

The anti-seize compounds are lubricants and protective compounds designed to prevent seizing, galling, and corrosion of threaded connections and moving parts exposed to extreme conditions. These compounds, formulated with solid lubricants such as graphite, copper, aluminum, or molybdenum disulfide, provide a durable barrier that ensures smooth assembly, disassembly, and long-term protection. Key characteristics of these compounds include high-temperature resistance, excellent chemical inertness, and effective performance under high pressure and in corrosive environments. The benefits include reduced maintenance costs, enhanced equipment lifespan, and ease of servicing in challenging operating conditions. Applications span automotive, aerospace, marine, oil and gas, and industrial machinery, where reliable performance and component longevity are critical. End-users include automotive manufacturers, industrial equipment producers, and maintenance service providers, driven by increasing trends for high-performance lubricants, growing industrialization, and advancements in material protection technologies.

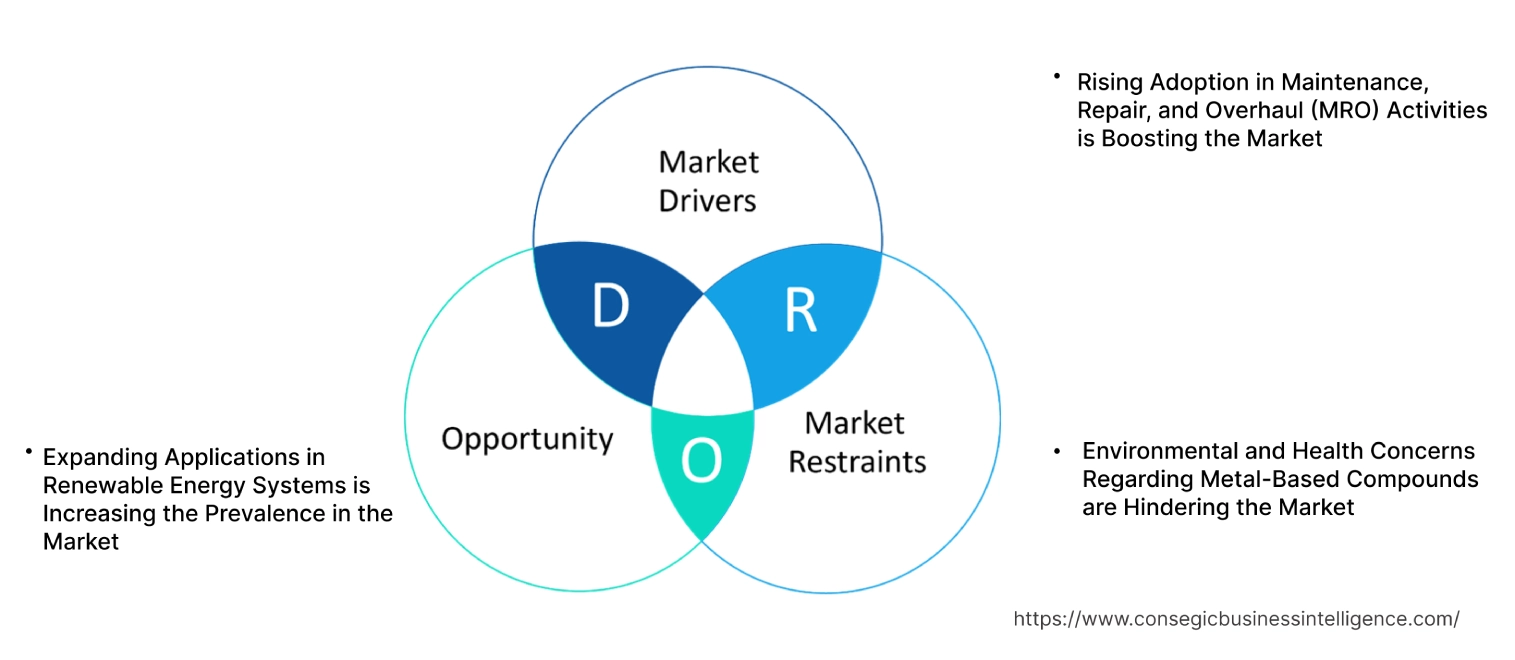

Anti-seize Compounds Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption in Maintenance, Repair, and Overhaul (MRO) Activities is Boosting the Market

Anti-seize compounds are becoming integral to maintenance, repair, and overhaul (MRO) operations across various industries, including automotive, manufacturing, and aerospace. These compounds prevent threaded connections and metal surfaces from galling, corrosion, and seizing, simplifying the assembly and disassembly processes. By ensuring smoother maintenance operations, they help reduce downtime, minimize repair costs, and enhance overall equipment reliability.

Trends in preventive maintenance and equipment longevity highlight the importance of these compounds in extending the lifespan of critical components. Their use in high-pressure and high-temperature environments, such as turbines, engines, and heavy machinery, further underscores their role in efficient MRO practices. Analysis indicates that industries prioritizing operational efficiency and cost-effective maintenance solutions are increasingly adopting these compounds to improve productivity and reduce operational disruptions.

Key Restraints:

Environmental and Health Concerns Regarding Metal-Based Compounds are Hindering the Market

Many traditional anti-seize compounds contain heavy metals like copper, nickel, and lead, which pose environmental and health risks during application and disposal. These concerns are amplified by regulatory frameworks in regions emphasizing environmental compliance and workplace safety. The use of metal-based compounds can lead to contamination during disposal and exposure risks for workers, creating challenges for manufacturers to align with evolving standards.

The push toward sustainability has intensified scrutiny over such compounds, driving the need for safer and eco-friendly alternatives. Manufacturers are under pressure to reformulate their products to reduce toxicity without compromising performance. Trends in regulatory compliance and green manufacturing practices are reshaping the market, with non-metallic and bio-based alternatives gaining traction as viable solutions.

Future Opportunities :

Expanding Applications in Renewable Energy Systems is Increasing the Prevalence in the Market

The renewable energy sector is emerging as a significant market for anti-seize compounds due to the harsh environmental conditions in which renewable energy systems often operate. Wind turbines, solar panel mounting systems, and hydroelectric plant components require reliable protection against corrosion, extreme temperatures, and wear. Anti-seize compounds ensure the durability and efficiency of these components, minimizing the need for frequent maintenance and enhancing system reliability.

Trends in renewable energy expansion and sustainable infrastructure development are creating new anti-seize compounds market opportunities for compounds tailored to meet the unique challenges of these applications. Analysis suggests that manufacturers focusing on renewable energy-specific formulations, such as those offering superior weather resistance and longer-lasting protection, can capitalize on this growing market segment. As clean energy projects continue to rise globally, the role of these compounds in supporting the longevity and reliability of renewable energy systems is expected to expand.

Anti-seize Compounds Market Segmental Analysis :

By Type:

Based on type, the market is segmented into copper-based compounds, nickel-based compounds, aluminum-based compounds, zinc-based compounds, non-metallic compounds, and others.

The copper-based anti-seize compounds segment accounted for the largest revenue share in 2024.

- Copper-based anti-seize compounds are widely used for their excellent conductivity, extreme pressure resistance, and high-temperature tolerance.

- These compounds are extensively applied in industrial equipment, automotive, and construction industries for preventing galling, seizing, and corrosion in threaded connections, gaskets, and bearings.

- Their suitability for a wide range of applications, including high-temperature and high-pressure environments, has driven their dominance in the market.

- Additionally, the increasing opportunities in the adoption of copper-based compounds in heavy machinery and oil & gas equipment further reinforce their market position.

The nickel-based anti-seize compounds segment is anticipated to register the fastest CAGR during the forecast period.

- Nickel-based compounds are preferred for applications in extreme temperature and corrosive environments, such as aerospace, marine, and oil & gas industries.

- These compounds offer superior resistance to oxidation, chemicals, and acids, making them ideal for high-performance applications.

- The growing anti-seize compounds market trends for nickel-based compounds in critical applications, such as turbine assembly and heat exchangers, are driving their rapid anti-seize compounds market growth.

- Furthermore, advancements in formulation technology to enhance performance and environmental compliance are expected to boost the adoption of nickel-based compounds.

By Form:

Based on form, the market is segmented into paste, liquid, and aerosol.

The paste segment accounted for the largest revenue share in 2024.

- Paste anti-seize compounds are widely used due to their ease of application, durability, and versatility.

- These compounds are ideal for threaded connections, bearings, and gaskets in industries such as construction, automotive, and industrial equipment.

- The growing preference for paste forms in heavy-duty applications requiring thick and consistent coatings has driven the dominance of this segment.

- Additionally, the availability of specialized paste formulations tailored for specific environments, such as high temperatures or chemical exposure, further boosts their adoption.

The aerosol segment is anticipated to register the fastest CAGR during the forecast period.

- Aerosol compounds offer convenient application and uniform coverage, making them ideal for hard-to-reach areas and intricate components.

- These compounds are gaining popularity in automotive, aerospace, and industrial equipment maintenance, where precision and ease of use are critical.

- The growing anti-seize compounds market trends for user-friendly and environmentally compliant products, coupled with advancements in aerosol packaging technologies, are driving the rapid advancement of this segment.

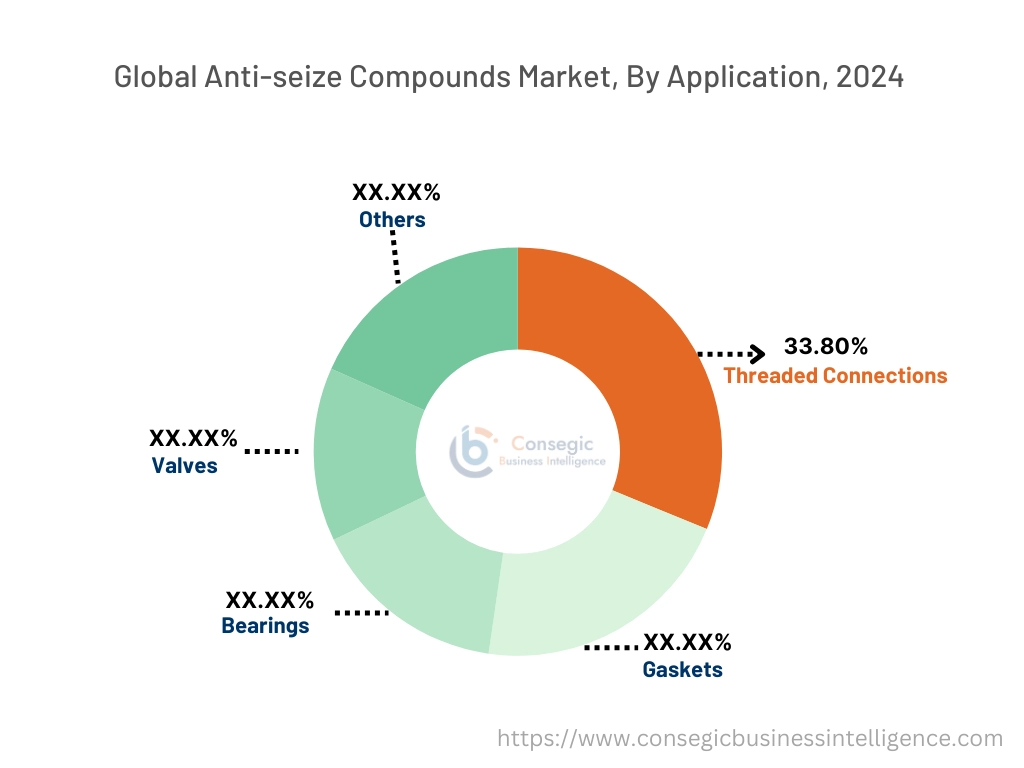

By Application:

Based on application, the market is segmented into threaded connections, gaskets, bearings, valves, and others.

The threaded connections segment accounted for the largest revenue of 33.80% in the anti-seize compounds market share in 2024.

- Threaded connections are a primary application area for anti-seize compounds, as these compounds prevent galling, seizing, and corrosion during assembly and operation.

- Industries such as construction, automotive, and oil & gas rely heavily on the compounds to ensure the durability and reliability of threaded components.

- The increasing adoption of anti-seize compounds for threaded connections in heavy machinery and critical equipment has solidified the dominance of this segment in the market.

The valves segment is anticipated to register the fastest CAGR during the forecast period.

- Valves require compounds to ensure smooth operation, prevent wear and corrosion, and enhance the longevity of components exposed to high pressure and temperature.

- The rising anti-seize compounds market demand for advanced valve systems in industries such as oil & gas, aerospace, and marine is driving the adoption of anti-seize compounds in this application.

- Additionally, the focus on reducing operational downtime and improving equipment efficiency is expected to fuel significant anti-seize compounds market growth in the valves segment.

By End-Use Industr:

Based on end-use, the market is segmented into automotive, aerospace, marine, industrial equipment, construction, oil & gas, and others.

The industrial equipment segment accounted for the largest revenue in anti-seize compounds market share in 2024.

- The industrial equipment sector is a major consumer of anti-seize compounds due to the high demand for maintenance and protection of machinery used in manufacturing, mining, and heavy industries.

- These compounds are critical for ensuring the smooth operation and longevity of components such as bearings, valves, and threaded connections.

- The increasing focus on reducing equipment downtime and improving operational efficiency in industrial processes has driven the dominance of this segment.

The aerospace segment is anticipated to register the fastest CAGR during the forecast period.

- Anti-seize compounds are extensively used in aerospace applications for protecting high-performance components such as turbines, fasteners, and exhaust systems from extreme temperatures, corrosion, and wear.

- The growing production of commercial and military aircraft, coupled with stringent performance and safety standards, has fueled the anti-seize compounds market demand for advancement in this industry.

- Additionally, the adoption of lightweight materials and the focus on enhancing fuel efficiency in aerospace applications are expected to drive significant growth in this segment.

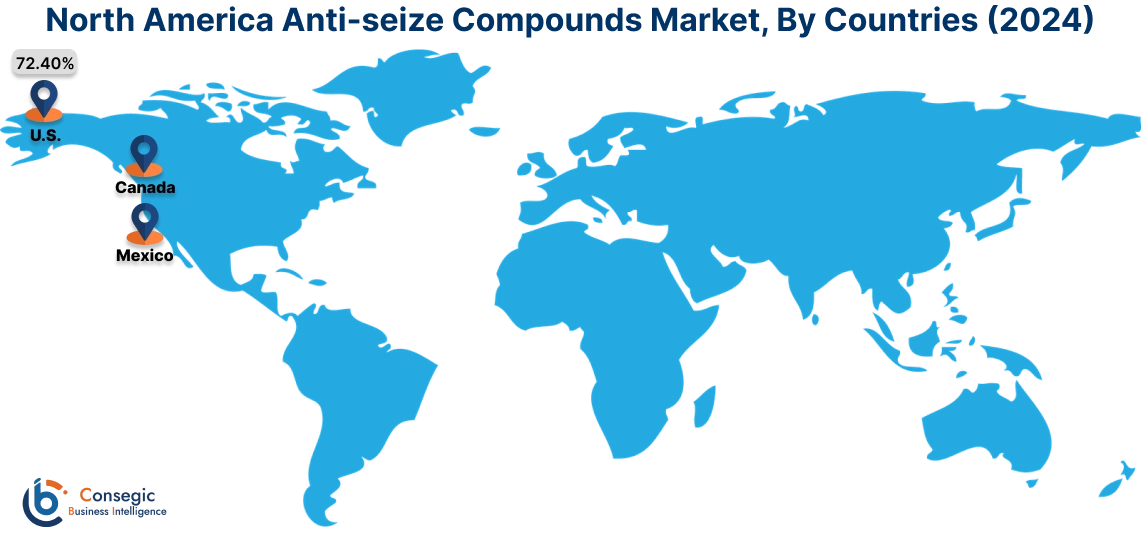

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

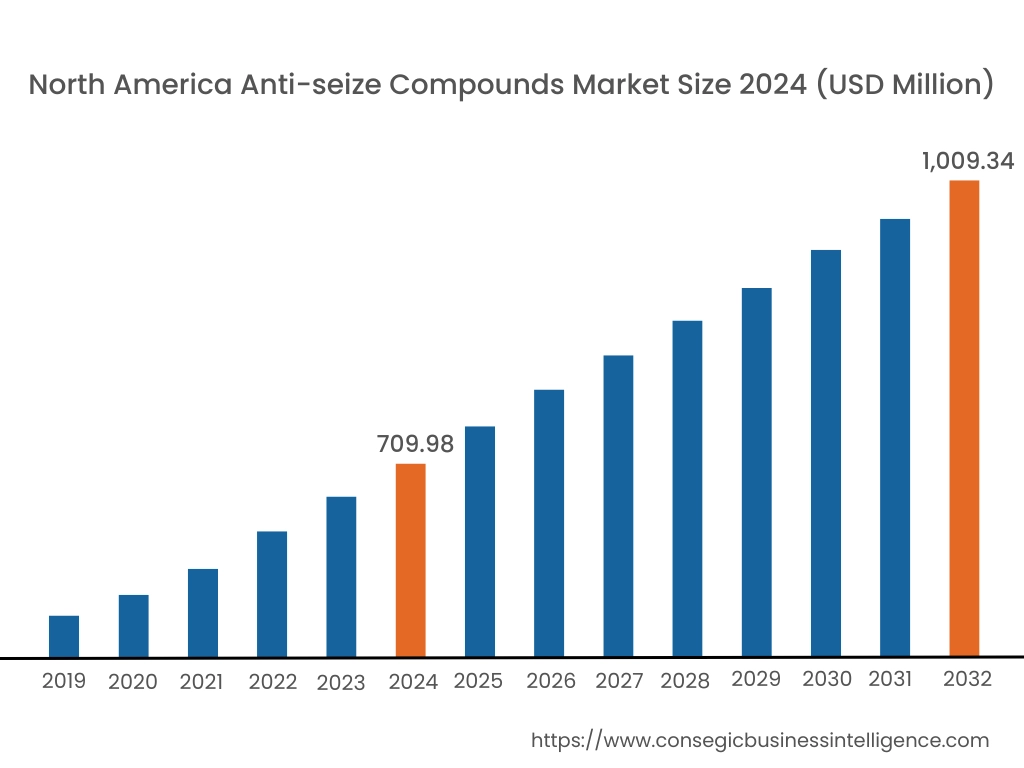

In 2024, North America was valued at USD 709.98 Million and is expected to reach USD 1,009.34 Million in 2032. In North America, the U.S. accounted for the highest share of 72.40% during the base year of 2024. North America holds a significant stake in the anti-seize compounds market analysis, driven by its well-developed industrial, automotive, and aerospace sectors. The U.S. leads the region due to the widespread use of these compounds in high-temperature and high-pressure applications across industries such as manufacturing, oil and gas, and transportation. These compounds are essential for preventing galling, corrosion, and seizing in equipment and machinery. Canada contributes to the market with its expanding oil and gas industry, where anti-seize compounds are critical for enhancing the longevity of tools and equipment. However, the market may face challenges due to stringent environmental regulations regarding certain metal-based compounds.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.2% over the forecast period. The anti-seize compounds market analysis is fueled by rapid industrialization, urbanization, and the expansion of manufacturing and automotive industries in China, India, and Japan. China dominates the market with extensive use of these compounds in automotive production, heavy machinery, and industrial equipment. India’s growing construction, power generation, and transportation sectors further drive the demand for these compounds to reduce equipment wear and downtime. Japan emphasizes high-precision applications in electronics, automotive, and aerospace industries, utilizing anti-seize compounds for their superior performance under extreme conditions. However, price sensitivity in emerging markets and limited awareness about advanced formulations may hinder growth in some areas.

Europe is a prominent market for anti-seize compounds, supported by its strong industrial base and stringent focus on equipment maintenance and efficiency. Countries like Germany, France, and the UK are key contributors. Germany’s robust automotive and manufacturing industries drive trends for anti-seize compounds in machinery and vehicle components. France emphasizes the use of these compounds in aerospace and defense applications, particularly for their high-temperature and corrosion-resistant properties. The UK focuses on marine and industrial applications where harsh environments require advanced lubrication solutions. However, strict EU regulations on chemical usage and environmental impact may pose challenges for manufacturers.

The Middle East & Africa regional analysis is witnessing steady growth in the global anti-seize compounds market, driven by increasing investments in oil and gas, construction, and mining sectors. Countries like Saudi Arabia and the UAE rely heavily on anti-seize compounds for drilling equipment, pipelines, and industrial machinery to enhance operational efficiency and reduce maintenance costs. In Africa, South Africa is a key market, leveraging these compounds in mining and transportation sectors where extreme conditions require durable solutions. However, limited local production capabilities and reliance on imports may restrict broader anti-seize compounds market expansion in the region.

Latin America is an emerging market for anti-seize compounds, with Brazil and Mexico leading the region. Brazil’s expanding industrial and automotive sectors drive the demand for these compounds in machinery, vehicle components, and manufacturing equipment. As per the analysis, Mexico’s growing oil and gas industry and infrastructure projects further support the adoption of anti-seize compounds in applications requiring protection against extreme pressures and temperatures. The region also shows increasing interest in corrosion-resistant formulations for marine and industrial applications. However, economic instability and inconsistent regulatory frameworks may pose challenges to anti-seize compounds market expansion in some countries.

Top Key Players and Market Share Insights:

The anti-seize compounds market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the anti-seize compounds market. Key players in the anti-seize compounds industry include -

- Henkel AG & Co. KGaA (Germany)

- The Dow Chemical Company (USA)

- Bostik (France)

- CSW Industrials, Inc. (USA)

- CRC Industries (USA)

- 3M Company (USA)

- SKF Group (Sweden)

- Rocol (UK)

- FUCHS (Germany)

- DuPont (USA)

Recent Industry Developments :

Product Launches:

- In April 2023, DuPont introduced MOLYKOTE® P-3700 Anti-Seize Paste, a high-purity solid lubricant designed for bolted joints. Effective in applications up to 900°C, providing controlled friction during assembly and ensuring easy disassembly of threaded connections even after prolonged exposure to high temperatures. The absence of hazardous substances eliminates the formation of hexavalent chromium (Cr(VI)) when used on high-chromium alloys at temperatures exceeding 300°C, addressing environmental and health concerns associated with traditional anti-seize compounds.

Anti-seize Compounds Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,114.29 Million |

| CAGR (2025-2032) | 4.8% |

| By Type |

|

| By Form |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the estimated market size of the Anti-Seize Compounds Market by 2032? +

Anti-seize Compounds Market size is estimated to reach over USD 3,114.29 Million by 2032 from a value of USD 2,140.38 Million in 2024 and is projected to grow by USD 2,204.98 Million in 2025, growing at a CAGR of 4.8% from 2025 to 2032.

What are anti-seize compounds? +

Anti-seize compounds are protective lubricants formulated to prevent seizing, galling, and corrosion of threaded connections and moving parts in extreme environments. They are designed to ensure smooth assembly, disassembly, and long-term protection.

What are the primary drivers for the Anti-Seize Compounds Market? +

The market is primarily driven by the rising adoption of anti-seize compounds in maintenance, repair, and overhaul (MRO) operations across various industries. Their ability to enhance equipment reliability, reduce downtime, and minimize maintenance costs has contributed to their growing demand.

What challenges are restraining the growth of the Anti-Seize Compounds Market? +

A significant challenge lies in the environmental and health concerns associated with metal-based compounds, which contain elements like copper and nickel. Regulatory scrutiny and the push for safer alternatives have made compliance with environmental standards more complex for manufacturers.