- Summary

- Table Of Content

- Methodology

Anti-Money Laundering Software Market Scope & Overview:

Anti-money laundering (AML) software is a specialized solution designed to detect, prevent, and report suspicious financial activities that may indicate money laundering or other illicit transactions. These systems provide financial institutions and businesses with tools for transaction monitoring, customer due diligence, compliance management, and risk assessment, ensuring adherence to regulatory requirements.

AML software automates the identification of unusual patterns in financial transactions, enabling organizations to respond swiftly to potential risks.These solutions are equipped with advanced features such as real-time monitoring, data analytics, and automated reporting, facilitating efficient management of compliance workflows. They integrate seamlessly with existing financial systems, allowing for comprehensive data aggregation and analysis.

AML software also includes robust mechanisms for detecting fraudulent activities and managing compliance audits, enhancing operational transparency and security.End-users of AML software include banks, insurance companies, payment processors, and other financial service providers that require reliable tools to combat financial crime and maintain regulatory compliance. This software is a critical component in safeguarding the financial ecosystem and ensuring ethical business practices.

Anti-Money Laundering Software Market Size:

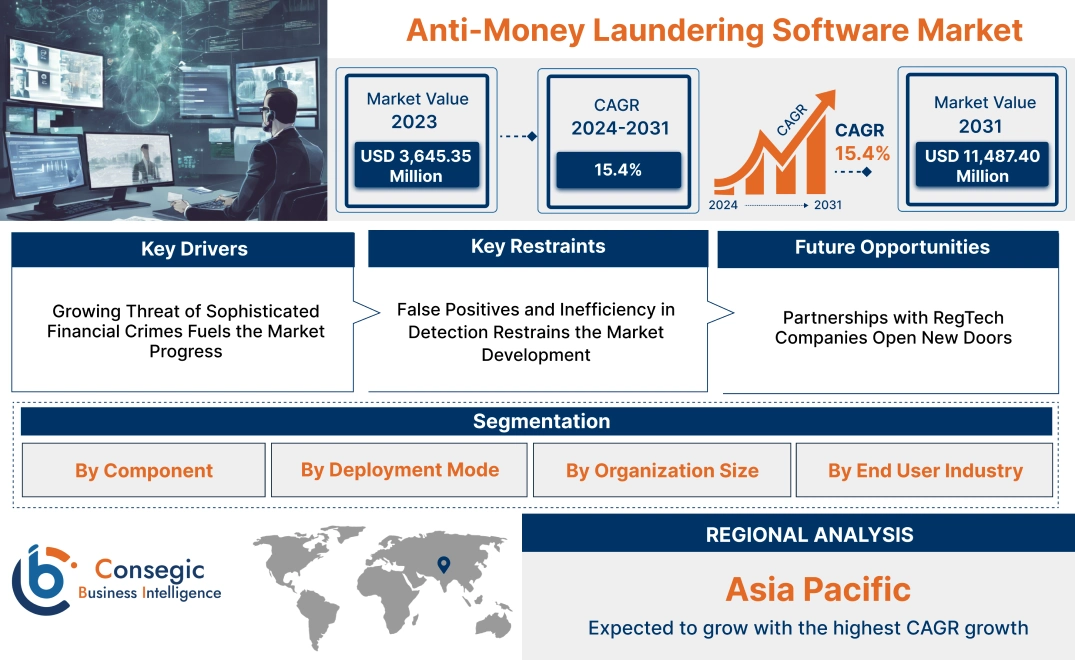

Anti-Money Laundering Software Market size is estimated to reach over USD 11,487.40 Million by 2031 from a value of USD 3,645.35 Million in 2023 and is projected to grow by USD 4,142.79 Million in 2024, growing at a CAGR of 15.4% from 2024 to 2031.

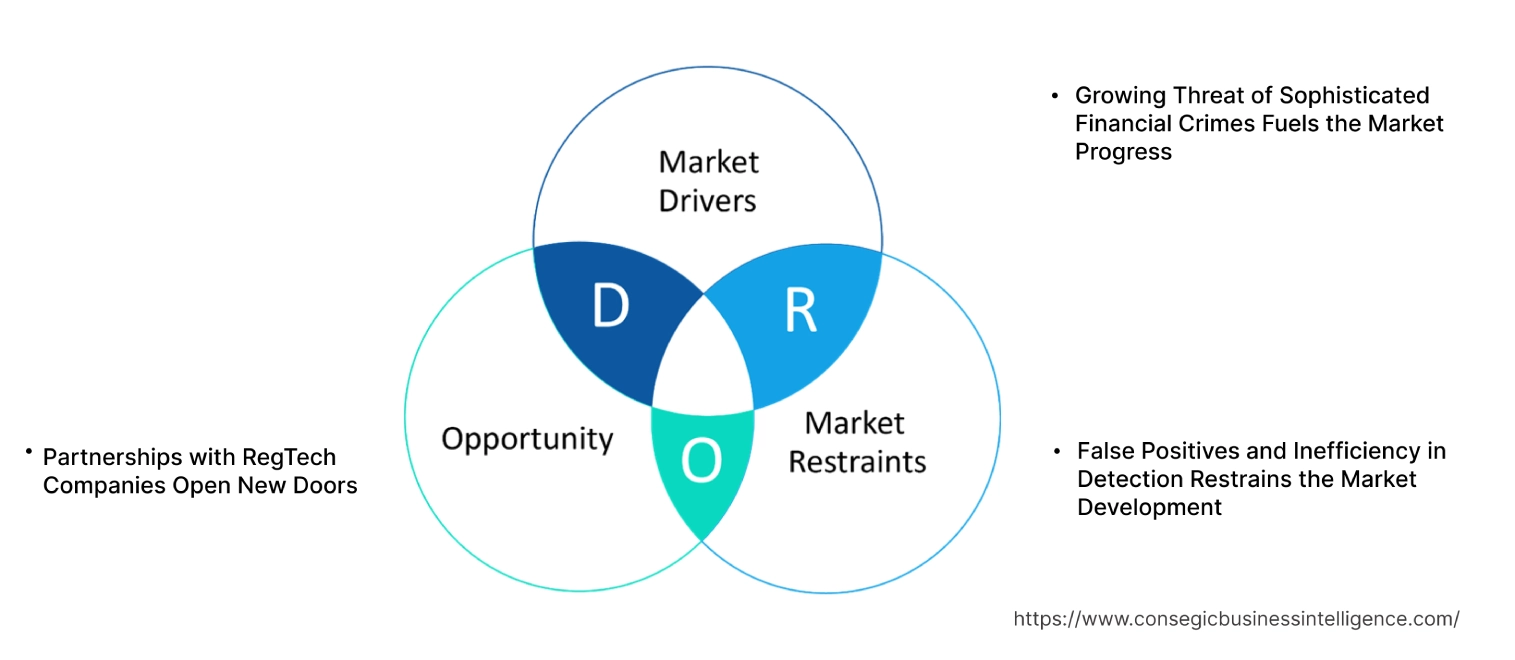

Anti-Money Laundering Software Market Dynamics - (DRO) :

Key Drivers:

Growing Threat of Sophisticated Financial Crimes Fuels the Market Progress

The increasing complexity of financial crimes, including techniques like layering, integration, and cyber-enabled fraud, is driving the demand for advanced detection systems in the financial sector. Criminals leverage sophisticated methods to obscure illicit transactions, making traditional rule-based systems insufficient for effective monitoring.

Advanced solutions powered by artificial intelligence (AI) and machine learning (ML) are becoming critical, as they enable real-time detection of anomalous patterns across vast datasets. These technologies provide dynamic risk assessment, adaptive learning, and predictive analytics, allowing financial institutions to stay ahead of evolving threats.

By automating processes and reducing manual intervention, AI and ML-driven tools enhance operational efficiency and accuracy in identifying suspicious activities. As financial crimes grow more intricate, the adoption of intelligent detection systems is becoming a strategic priority for institutions to safeguard against fraud and maintain compliance with regulatory requirements. Thus, the aforementioned factors lead to the anti-money laundering software market growth.

Key Restraints :

False Positives and Inefficiency in Detection Restrains the Market Development

The issue of false positives remains a significant constraint in compliance systems, particularly in anomaly detection for anti-money laundering (AML) processes. Many existing solutions generate a high volume of alerts for transactions flagged as potentially suspicious, a large percentage of which turn out to be false positives.

This inefficiency not only wastes valuable resources but also overburdens compliance teams, requiring extensive manual review to verify and resolve alerts. The repetitive nature of this task leads to operational delays and increased costs, particularly for institutions managing large transaction volumes.

Additionally, excessive false positives reduce confidence in the system’s accuracy and effectiveness, discouraging further investment in such technologies. The inefficiency hampers the ability of financial institutions to focus on genuine risks, creating compliance gaps that could expose organizations to regulatory scrutiny and financial penalties. Therefore, the above-mentioned factors limit the anti-money laundering software market demand.

Future Opportunities :

Partnerships with RegTech Companies Open New Doors

Partnerships with regulatory technology (RegTech) companies are emerging as a key growth strategy for compliance solution providers. By collaborating with RegTech firms, providers incorporate cutting-edge technologies such as blockchain for secure, tamper-proof transaction monitoring and biometric verification for robust customer authentication.

These integrations not only enhance the functionality of compliance solutions but also improve efficiency in meeting regulatory requirements. Additionally, RegTech partnerships allow providers to offer customized solutions tailored to specific industries, such as banking, insurance, and fintech. This collaborative approach broadens market reach, enabling providers to tap into diverse customer segments.

Furthermore, leveraging RegTech expertise helps address complex challenges in areas like real-time monitoring and cross-border compliance, making solutions more comprehensive and competitive. As regulatory landscapes become increasingly stringent, partnerships with RegTech firms position providers to deliver innovative and scalable compliance solutions, aligning with market trends and customer expectations, further creating significant anti-money laundering software market opportunities.

Top Key Players & Market Share Insights:

The anti-money laundering software market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global anti-money laundering software market. Key players in the anti-money laundering software industry include –

- Accenture (Ireland)

- Oracle Corporation (USA)

- NICE Actimize (USA)

- RiskMS (USA)

- 4xLabs (Singapore)

- BAE Systems (UK)

- Cognizant (USA)

- Fiserv, Inc. (USA)

- SAS Institute, Inc. (USA)

- ACI Worldwide (USA)

Anti-Money Laundering Software Market Segmental Analysis :

By Component:

Based on components, the market is segmented into solutions and services.

The solutions segment accounted for the largest revenue of the total anti-money laundering software market share in 2023.

- Transaction monitoring tools are pivotal for identifying and reporting suspicious financial activities in real time, ensuring compliance with regulatory frameworks.

- Customer identity verification systems streamline KYC processes, minimizing risks associated with fraudulent accounts and enhancing customer trust.

- Compliance management platforms provide robust features for regulatory reporting and audit management, reducing manual effort and ensuring accuracy.

- Thus, the dominance of this segment is attributed to the growing demand for sophisticated software solutions to tackle complex money laundering schemes effectively, leading to anti-money laundering software market expansion.

The services segment is expected to register the fastest CAGR during the forecast period.

- Consulting services assist organizations in tailoring anti-money laundering frameworks to align with unique compliance and operational requirements.

- Integration services enable seamless deployment of software solutions into existing IT infrastructures, ensuring interoperability and scalability.

- Support and maintenance services ensure the continuous performance of software systems, reducing downtime and operational disruptions.

- As per anti-money laundering software market analysis, the segment's progress is driven by the increasing demand for expert guidance and ongoing support to manage regulatory complexities.

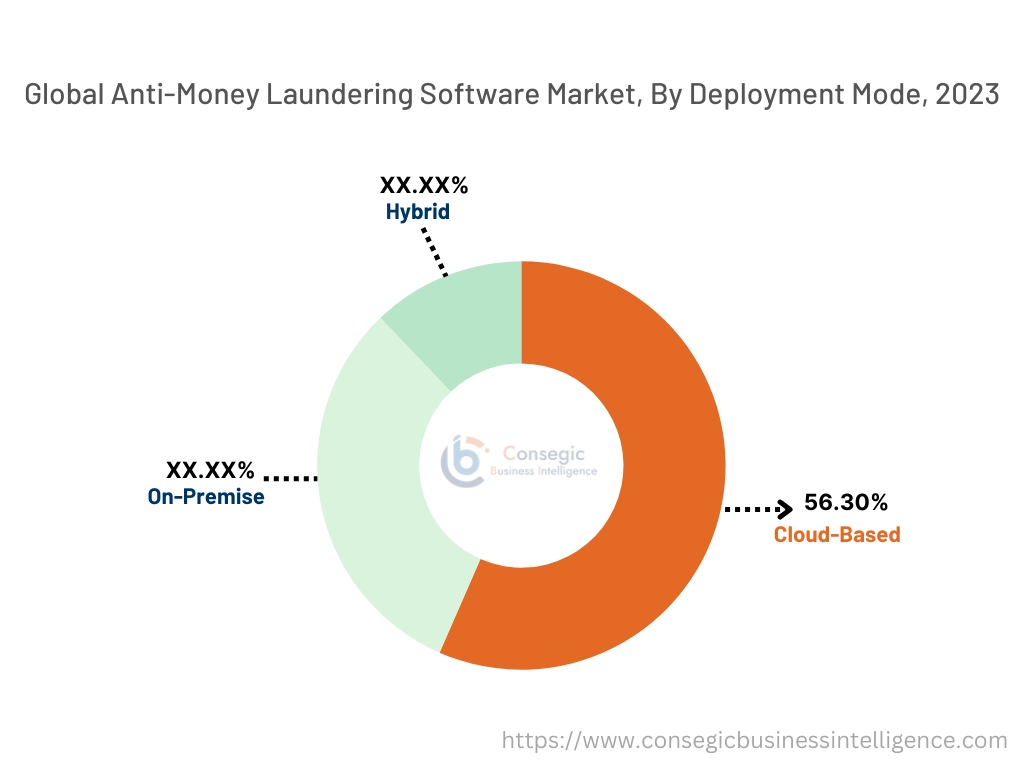

By Deployment Mode:

Based on deployment mode, the market is segmented into on-premise, cloud-based, and hybrid.

The cloud-based segment held the largest revenue of 56.30% of the total anti-money laundering software market share in 2023.

- Cloud-based deployment offers scalability and flexibility, enabling organizations to adapt to evolving compliance needs without significant infrastructure investments.

- The segment is preferred by SMEs and large enterprises alike for its cost-efficiency and ease of implementation.

- Cloud-based platforms leverage advanced data analytics and AI to enhance transaction monitoring and risk assessment capabilities.

- As per anti-money laundering software market trends, the dominance of this segment is supported by the shift toward digital transformation and increasing adoption of cloud technology across industries.

The hybrid segment is expected to register the fastest CAGR during the forecast period.

- Hybrid deployment combines the advantages of on-premise control and cloud flexibility, making it ideal for organizations with stringent security requirements.

- Financial institutions and government agencies often opt for hybrid models to maintain sensitive data on-premise while leveraging cloud analytics.

- This segment’s steady expansion reflects the demand for customizable deployment options that address specific operational and compliance challenges.

- Thus, the advancements in hybrid infrastructure technologies are further driving adoption, particularly in highly regulated industries, which fuels the anti-money laundering software market demand.

By Organization Size:

Based on organization size, the market is segmented into small & medium enterprises (SMEs) and large enterprises.

The large enterprises segment held the largest revenue share in 2023.

- Large enterprises leverage advanced anti-money laundering solutions to manage high transaction volumes and complex compliance requirements.

- These organizations invest heavily in technology to enhance their fraud detection and risk management capabilities.

- The dominance of this segment reflects the critical role of compliance management in mitigating risks associated with extensive financial operations.

- As per the market trends, increased regulatory scrutiny on large financial institutions has driven the adoption of comprehensive anti-money laundering systems, facilitating the anti-money laundering software market growth.

The SME segment is expected to register the fastest CAGR during the forecast period.

- SMEs are increasingly adopting cloud-based anti-money laundering solutions due to their affordability and ease of integration.

- Simplified regulatory compliance solutions designed for smaller organizations are enabling SMEs to improve operational efficiency.

- The growth of this segment is supported by government initiatives and regulatory bodies encouraging compliance in smaller financial institutions.

- SMEs are leveraging AI-driven tools to optimize their compliance processes and reduce manual errors, contributing to anti-money laundering software market expansion.

By End User:

Based on the end-user industry, the market is segmented into BFSI, IT & telecom, government, healthcare, retail, and others.

The BFSI segment accounted for the largest revenue share in 2023.

- Financial institutions rely on robust anti-money laundering software to mitigate risks associated with fraudulent transactions and ensure regulatory compliance.

- Banks and payment service providers invest significantly in advanced transaction monitoring and customer verification systems.

- The dominance of this segment is driven by increased scrutiny from regulatory authorities and the need for real-time risk management.

- As per anti-money laundering software market analysis, the BFSI sector's reliance on digital platforms has further fueled the adoption of advanced compliance technologies.

The government segment is expected to register the fastest CAGR during the forecast period.

- Government agencies use anti-money laundering software to monitor and investigate suspicious financial activities, ensuring national security.

- Public sector organizations deploy these solutions to enhance their audit processes and comply with international regulatory standards.

- The steady growth of this segment is supported by increasing collaboration between governments and financial institutions to combat financial crimes.

- Technological advancements in analytics tools have enabled government agencies to streamline investigations and improve transparency in financial operations, creating new anti-money laundering software market opportunities.

Anti-Money Laundering Software Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 11,487.40 Million |

| CAGR (2024-2031) | 15.4% |

| By Component |

|

| By Deployment Mode |

|

| By Organization Size |

|

| By End User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

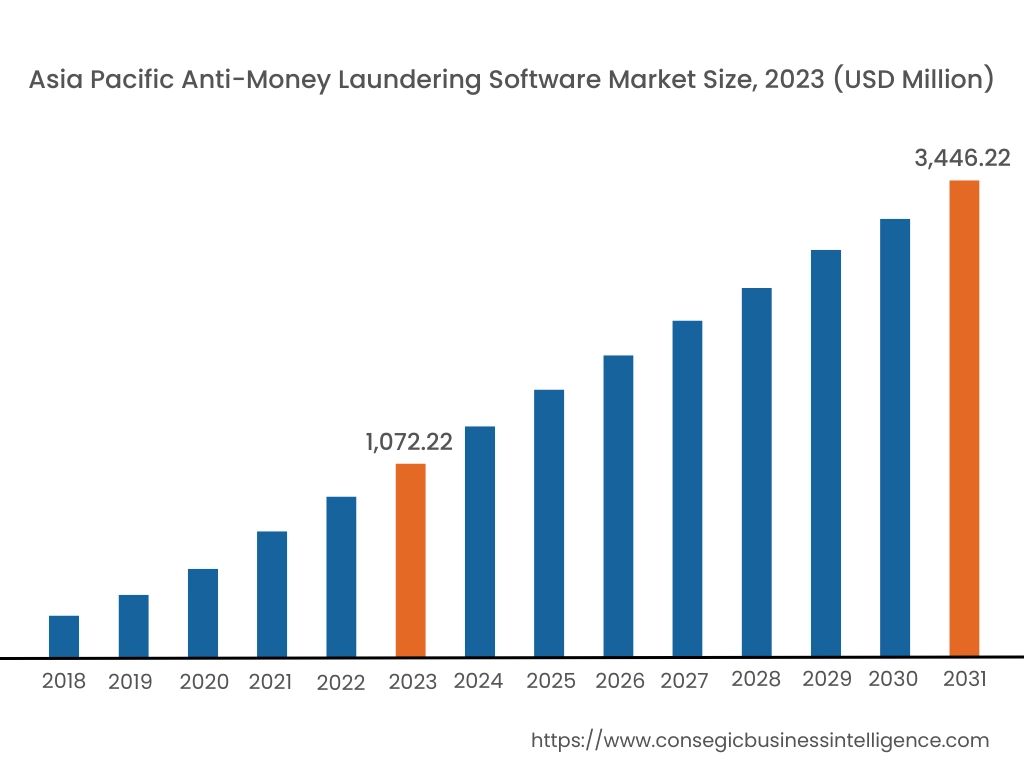

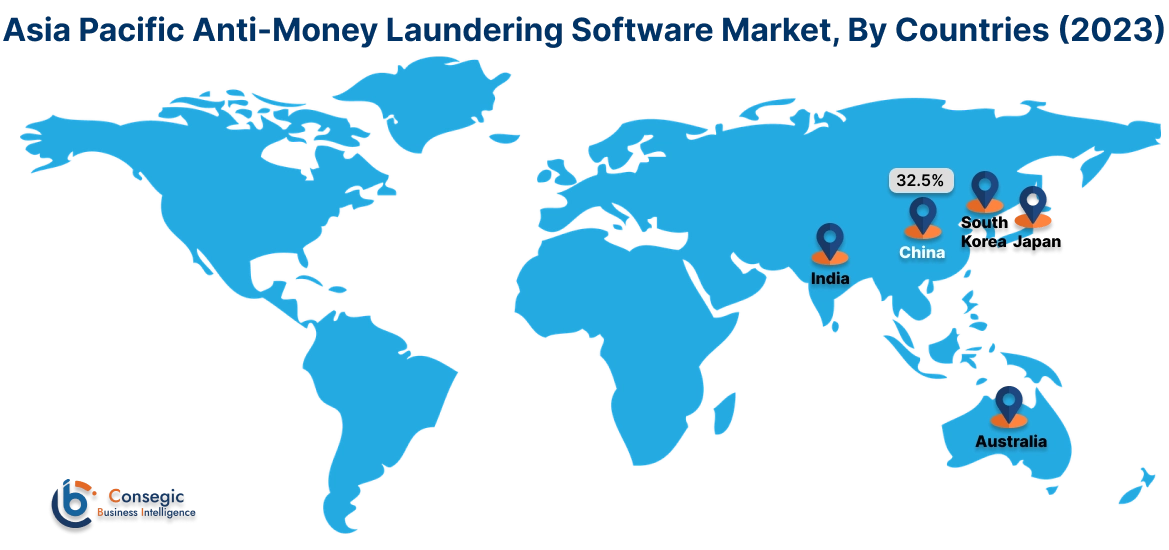

Asia Pacific region was valued at USD 1,072.22 Million in 2023. Moreover, it is projected to grow by USD 1,220.56 Million in 2024 and reach over USD 3,446.22 Million by 2031. Out of these, China accounted for the largest share of 32.5% in 2023. The Asia-Pacific region is experiencing rapid growth in the AML software market, propelled by expanding financial services and increasing regulatory scrutiny in countries such as China, India, and Japan. As per anti-money laundering software market trends, the surge in digital banking and online transactions necessitates robust AML solutions. Trends show a rising adoption of real-time transaction monitoring systems to promptly identify illicit activities.

North America is estimated to reach over USD 3,779.35 Million by 2031 from a value of USD 1,211.68 Million in 2023 and is projected to grow by USD 1,375.86 Million in 2024. This region holds a significant share of the AML software market, driven by stringent regulatory frameworks and a robust financial sector. The United States, in particular, enforces rigorous AML compliance, compelling financial institutions to adopt advanced software solutions. The trend towards integrating artificial intelligence and machine learning into AML systems is prominent, enhancing the detection of suspicious activities.

Europe represents a substantial portion of the global AML software market, with countries like the United Kingdom, Germany, and France leading in adoption. The region's strict regulatory standards, including the EU's Anti-Money Laundering Directives, drive the implementation of comprehensive AML solutions. Analysis indicates a growing trend towards cloud-based AML systems, offering scalability and cost-effectiveness.

The Middle East & Africa region is gradually adopting AML software, particularly in financial hubs like the United Arab Emirates and South Africa. Efforts to align with international AML standards and combat financial crimes are driving this adoption. Analysis reveals an increasing trend towards implementing comprehensive compliance management solutions to meet regulatory requirements.

Latin America is an emerging market for AML software, with Brazil and Mexico being key contributors. The region's growing financial sector and initiatives to strengthen AML regulations are fostering the adoption of software solutions. Trends indicate a focus on customer identity management systems to enhance Know Your Customer (KYC) processes.

Recent Industry Developments:

Investments & Funding:

- In February 2024, Napier AI, a London-based financial crime compliance RegTech firm, secured a £45 million investment from Crestline Investors, Inc., a U.S.-based credit-focused institutional alternative asset manager. This funding aims to accelerate Napier AI's growth in providing AI-powered anti-money laundering and financial crime compliance solutions to financial institutions, payments, and wealth & asset management firms. The investment underscores the increasing demand for advanced compliance technologies amid rising regulatory requirements.

- In January 2024, Sinpex, a Munich-based provider of compliance and anti-money laundering (AML) solutions, has successfully closed a €4 million financing round. The round was co-led by TX Ventures and ACE Ventures, with participation from existing investors EquityPitcher and AI Fund. This funding aims to support Sinpex's growth and prepare for international expansion. The company utilizes AI and natural language processing to automate the collection and verification of compliance data, enhancing efficiency and accuracy in business relationships.

- In January 2023, Sandbar, a New York-based fintech startup specializing in anti-money laundering (AML), fraud, and counter-terrorism risk detection software, has secured $4.8 million in seed funding. This funding aims to enhance Sandbar's product offerings and expand its reach to a broader audience. The company's solutions are designed to help organizations identify suspicious financial behaviors, prioritize alerts, and automate casework, enabling businesses to scale safely.

Partnerships & Collaborations:

- In September 2024, Tech Mahindra partnered with Discai to develop an AI-powered Anti-Money Laundering (AML) solution for global financial institutions. This collaboration combines Tech Mahindra's IT integration expertise with Discai's advanced AI and rule-based AML technology to enhance transaction monitoring and ensure regulatory compliance. The solution focuses on AI-driven and rule-based transaction monitoring, helping financial institutions effectively prevent and detect financial crimes.

Key Questions Answered in the Report

What is the size of the Anti-Money Laundering Software Market? +

Anti-Money Laundering Software Market size is estimated to reach over USD 11,487.40 Million by 2031 from a value of USD 3,645.35 Million in 2023 and is projected to grow by USD 4,142.79 Million in 2024, growing at a CAGR of 15.4% from 2024 to 2031.

What are the key segments in the Anti-Money Laundering Software Market? +

The Anti-Money Laundering Software Market is segmented by component (Solutions and Services), deployment mode (On-Premise, Cloud-Based, Hybrid), organization size (SMEs, Large Enterprises), and end-user industry (BFSI, IT & Telecom, Government, Healthcare, Retail, Others), as well as by region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which region is expected to dominate the Anti-Money Laundering Software Market? +

North America is expected to hold the largest market share in the Anti-Money Laundering Software Market, driven by stringent regulatory frameworks and a robust financial sector. The United States, in particular, has seen significant adoption of advanced AML systems due to rigorous AML compliance enforcement.

Who are the key players in the Anti-Money Laundering Software Market? +

Key players in the Anti-Money Laundering Software Market include Accenture (Ireland), Oracle Corporation (USA), BAE Systems (UK), Cognizant (USA), Fiserv, Inc. (USA), SAS Institute, Inc. (USA), ACI Worldwide (USA), NICE Actimize (USA), RiskMS (USA), and 4xLabs (Singapore).