- Summary

- Table Of Content

- Methodology

Anti-drone Market Size:

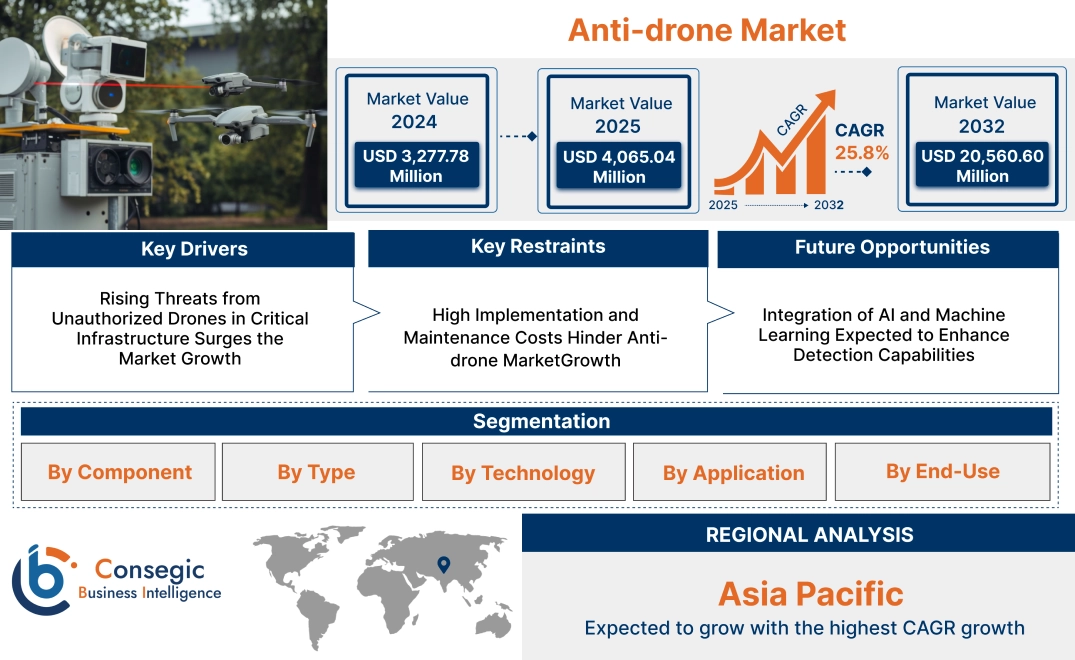

Anti-drone Market size is estimated to reach over USD 20,560.60 Million by 2032 from a value of USD 3,277.78 Million in 2024 and is projected to grow by USD 4,065.04 Million in 2025, growing at a CAGR of 25.8% from 2025 to 2032.

Anti-drone Market Scope & Overview:

Anti-drone technology refers to systems designed to detect, track, and neutralize unauthorized or hostile drones. These technologies include radio frequency (RF) jammers, lasers, and advanced radar systems, offering robust protection against aerial threats.

The key features of these systems include real-time detection, precise tracking, and the ability to disable drones through non-lethal methods. These systems provide enhanced security by preventing drone-related risks, including surveillance, smuggling, and attacks.

Anti-drone technologies find applications in military, defense, law enforcement, and critical infrastructure sectors. They are extensively used at airports, government buildings, and large-scale events to ensure public safety and protect sensitive areas. The benefits include increased security, minimized risk of espionage, and protection from potential drone-based attacks.

Anti-drone Market Dynamics - (DRO) :

Key Drivers:

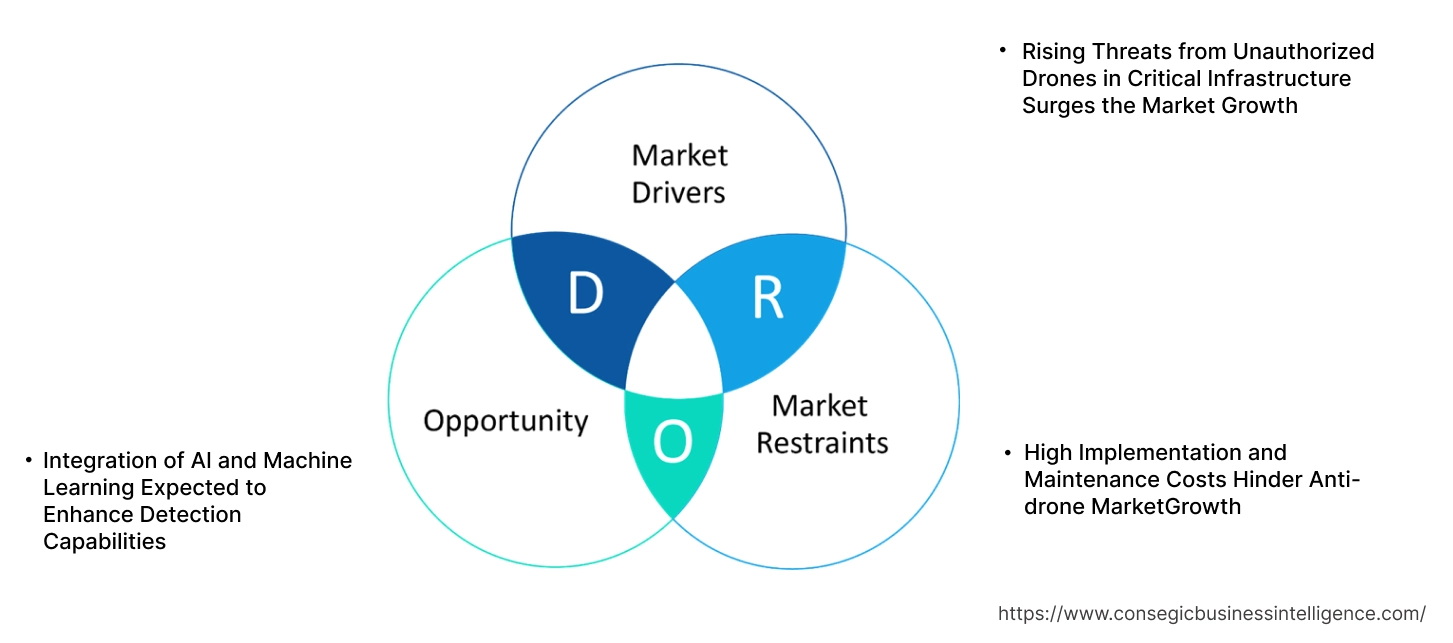

Rising Threats from Unauthorized Drones in Critical Infrastructure Surges the Market Growth

Unauthorized drones pose security risks to critical infrastructure such as power plants, airports, and government buildings. These drones can disrupt operations, conduct unauthorized surveillance, or even carry payloads that threaten public safety. Anti-drone technologies, including radar detection, radio frequency jamming, and drone interception systems, are essential in mitigating these threats. For instance, airports worldwide have faced numerous flight disruptions due to rogue drones entering restricted airspace. Implementing anti-drone measures enhances security and operational continuity. Therefore, increasing threats from unauthorized drones in critical infrastructure drive the anti-drone market trend of solutions.

Key Restraints:

High Implementation and Maintenance Costs Hinder Anti-drone Market Growth

Anti-drone systems require advanced technologies, including radar, radio frequency sensors, and artificial intelligence-based tracking, leading to high acquisition and deployment costs. Additionally, maintenance and operational expenses add financial burdens, especially for small businesses and public entities with limited budgets. Customizing anti-drone solutions to different environments, such as urban or military settings, further increases costs. For instance, deploying anti-drone defenses at international airports requires significant investment in infrastructure and personnel training. These high costs associated with implementation and maintenance restrict anti-drone market expansion, particularly among cost-sensitive sectors.

Future Opportunities :

Integration of AI and Machine Learning Expected to Enhance Detection Capabilities

Artificial intelligence and machine learning are expected to revolutionize anti-drone technology by improving detection accuracy and response times. These technologies will enable systems to differentiate between legitimate and unauthorized drones, reducing false alarms and improving threat assessment. AI-powered anti-drone solutions will also facilitate autonomous response mechanisms, minimizing human intervention. For example, AI-driven radar systems will analyze drone flight patterns to predict potential security threats more efficiently. Therefore, advancements in AI and machine learning will create new anti-drone market opportunities for enhancing anti-drone capabilities and adoption.

Anti-drone Market Segmental Analysis :

By Component:

Based on the component, the Market is segmented into hardware and software.

The hardware segment accounted for the largest revenue in anti-drone market share in 2024 and is anticipated to register the fastest CAGR during the forecast period.

- Hardware includes devices like radar systems, jammers, and other equipment designed to detect, track, and neutralize drones.

- Technological advancements, such as miniaturization of radar systems and the development of advanced jamming technologies, contribute to the anti-drone market trend of the hardware segment.

- Hardware components offer real-time detection and response to drone threats, making them essential for military, defense, and government applications.

- As security concerns increase globally, trend for hardware solutions that provide tangible, immediate responses to unauthorized drone activity is expected to rise.

- The increasing use of drones in illegal activities, such as surveillance, smuggling, or terrorism, necessitates sophisticated anti-drone hardware.

- Therefore, according to the anti-drone market analysis, the hardware segment is expected to maintain dominance in the Market, driven by the growing anti-drone market demand for effective and immediate threat neutralization technologies.

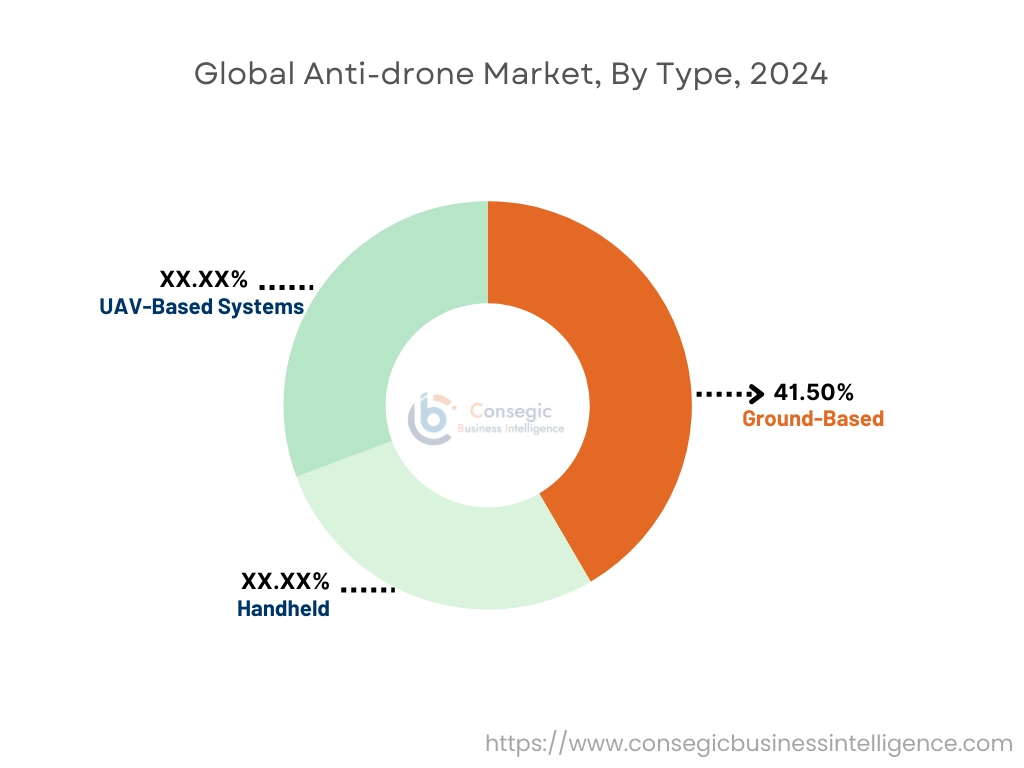

By Type:

Based on the type, the Market is segmented into ground-based, handheld, and UAV-based systems.

The ground-based system accounted for the largest revenue share by 41.50% in 2024.

- Ground-based systems provide comprehensive surveillance and protection over large areas, making them ideal for military and defense installations.

- These systems typically include radar, communication jammers, and anti-drone guns, allowing for efficient and automated drone interdiction.

- With the increasing need for perimeter security in sensitive areas, ground-based systems are increasingly being adopted in government, military, and commercial sectors.

- As these systems offer scalability and can be integrated with existing security infrastructure, they have a broad application range, which boosts their anti-drone market share.

- Therefore, according to the anti-drone market analysis, the versatility of ground-based anti-drone solutions makes them crucial in high-risk locations such as airports, military bases, and government buildings.

The handheld sector is anticipated to register the fastest CAGR during the forecast period.

- Handheld anti-drone systems offer flexibility, allowing security personnel to deploy them in varied environments.

- These systems are typically lightweight and portable, making them ideal for on-the-ground defense and urban security operations.

- Increasing security measures in public spaces, especially concerning drone-related criminal activity, will drive the adoption of handheld systems.

- The growing use of handheld solutions in counter-drone operations at events, public gatherings, and border security will lead to accelerated trend in this subsegment.

- Thus, according to the market analysis, the trend for ground-based systems will continue to dominate, while handheld systems are expected to experience significant growth due to their portability and ease of use in urban environments.

By Technology:

Based on the technology, the Market is segmented into laser systems, electronic systems, and kinetic systems.

The electronic systems sector accounted for the largest revenue share in 2024 and is expected to register the fastest CAGR during the forecast period.

- Electronic systems include communication jammers, GPS jammers, and other systems that interfere with drone signals, rendering them inoperable.

- These systems offer a non-destructive way of neutralizing drone threats by disrupting communication between the drone and its operator.

- Electronic systems are critical for both detection and interdiction, as they are often used to disable drones mid-flight.

- With the growing prevalence of drones in public and military areas, electronic systems are increasingly seen as an efficient solution for preventing drone incursions.

- Therefore, according to the market analysis, the advancement of signal jamming and spoofing technologies enhances the effectiveness of electronic systems, further boosting their adoption in security measures.

By Application:

Based on the application, the Market is segmented into detection and interdiction.

Detection accounted for the largest revenue share in 2024.

- Detection technologies include radar systems, cameras, and acoustic sensors designed to identify drones in restricted airspace.

- With increasing airspace congestion and unauthorized drone operations, the trend for advanced detection systems has grown, especially in military and government sectors.

- Detection systems are often used as the first line of defense, providing early warning of potential drone threats.

- Therefore, according to the market analysis, real-time, 360-degree coverage of high-value areas such as airports, military bases, and government installations is a significant application of detection technologies.

Interdiction is anticipated to register the fastest CAGR during the forecast period.

- Interdiction technologies actively neutralize the threat posed by drones once detected, making them a crucial part of anti-drone systems.

- This segment includes jamming, laser, and kinetic systems designed to physically disable or destroy drones.

- With the increasing risk of drones being used for terrorism, smuggling, or other illicit activities, the need for effective interdiction solutions is becoming more urgent.

- Thus, according to the market analysis, detection solutions will continue to dominate the market, while interdiction technologies are expected to see rapid trend due to the rising need for direct threat neutralization.

By End Use:

Based on end-use, the Market is segmented into military & defense, government, and commercial.

The military & defense sector accounted for the largest revenue share in 2024.

- The military & defense sector is the primary adopter of anti-drone technologies due to the increasing use of drones in warfare and surveillance.

- Drones are used by military adversaries for reconnaissance, surveillance, and even weapon delivery, making these systems essential for security operations.

- Anti-drone technologies are deployed in various defense applications, including border security, base defense, and high-security zones.

- Therefore, according to the market analysis, as drone threats evolve, the military is continuously investing in advanced counter-drone technologies to ensure national security.

The commercial sector is anticipated to experience the fastest growth during the forecast period.

- The commercial sector includes sectors such as aviation, oil & gas, transportation, and agriculture, which are increasingly adopting anti-drone technologies.

- With the rising use of drones for surveillance, delivery, and cargo transport, commercial entities need anti-drone solutions to protect their assets and ensure safety.

- Anti-drone technologies help prevent unauthorized drones from intruding on private properties, secure locations, or sensitive airspace.

- Thus, according to the market analysis, the military & defense sector will remain the largest contributor to the Market, while the commercial sector will see the fastest growth as industries increasingly integrate anti-drone solutions into their operations.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

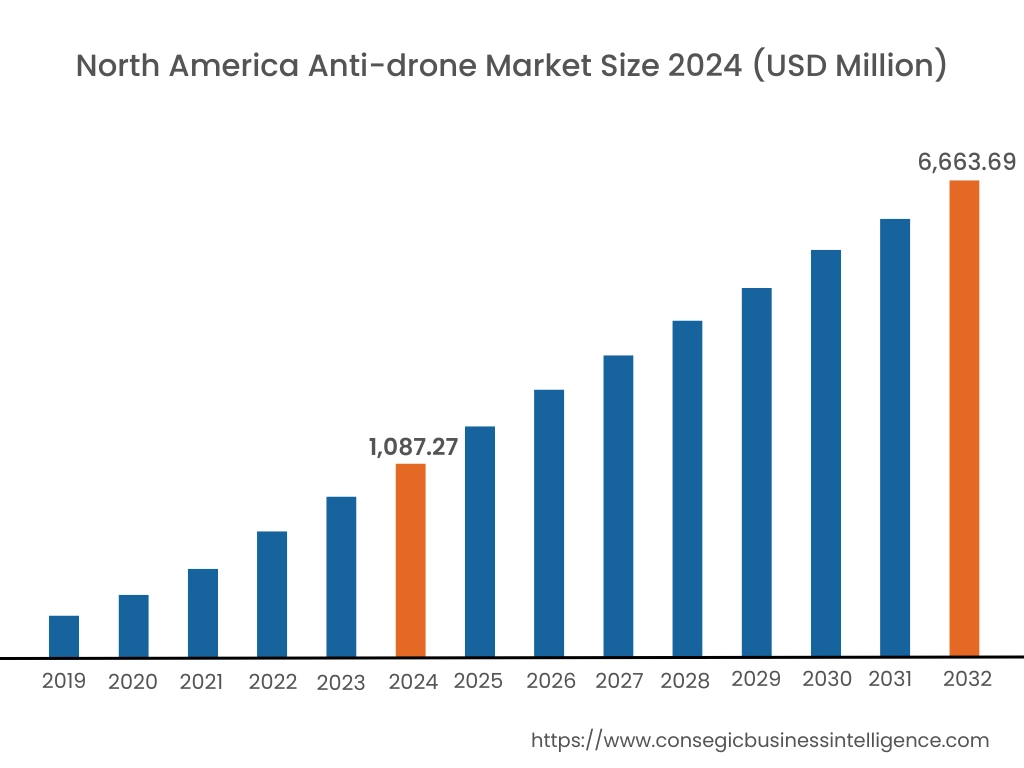

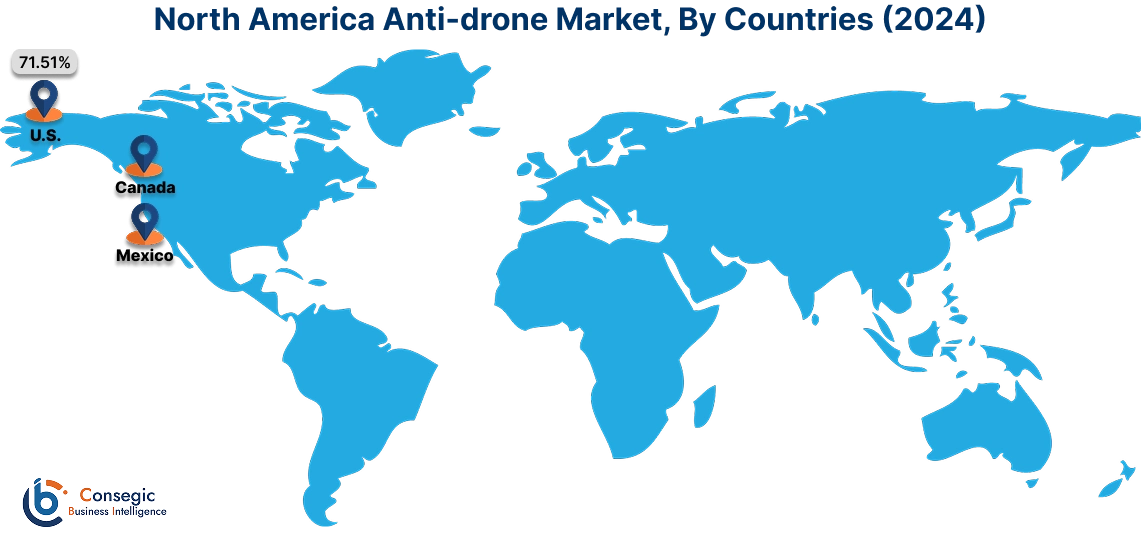

In 2024, North America was valued at USD 1,087.27 Million and is expected to reach USD 6,663.69 Million in 2032. In North America, the U.S. accounted for the highest share of 71.51% during the base year of 2024.

The anti-drone market in North America is robust, led by the United States, which invests heavily in defense and security technologies. Increasing concerns over security threats, including unauthorized drone use in sensitive areas, support the anti-drone market expansion. Both governmental and commercial entities actively adopt anti-drone solutions to safeguard infrastructure, military assets, and public spaces. The region’s advanced technological capabilities, along with strong investments in R&D for drone countermeasures, further enhance market growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 26.3% over the forecast period.

Asia-Pacific holds significant potential in the anti-drone market, driven by the rapid adoption of drone technology across countries like China, India, and Japan. The region experiences heightened concerns over border security, public safety, and critical infrastructure protection, resulting in increasing trend for these systems. Governments in China and India are focusing on enhancing their defense capabilities, leading to investments in anti-drone technologies. Additionally, the region's growing commercial drone market is also contributing to the anti-drone market demand for countermeasures.

In Europe, the anti-drone market is expanding due to the increasing threat of drones in both military and civilian contexts. Countries such as the United Kingdom, France, and Germany have been at the forefront of deploying anti-drone systems to protect critical infrastructure, airports, and military assets. The region’s stringent security regulations and focus on countering illegal drone activities support the demand for these technologies. European countries also invest in collaborative research and development to improve anti-drone solutions.

The Middle East and Africa (MEA) region experiences a rising demand for anti-drone solutions, primarily driven by security concerns in volatile regions. Countries like Saudi Arabia, the UAE, and Israel are increasingly adopting these technologies to protect key infrastructure and military assets from aerial threats. The region's military and defense sectors are major drivers of market growth, with governments investing in sophisticated drone detection and neutralization systems. The growing concern over the use of drones in warfare and terrorism further supports market development in this region.

In Latin America, the anti-drone market is gradually expanding, with key countries like Brazil and Mexico focusing on protecting critical infrastructure from drone threats. Although the market is still in its early stages, security concerns related to unauthorized drones in urban areas, airports, and military sites are increasing the demand for countermeasures. Regional governments are investing in anti-drone technologies, especially in sectors related to defense and public safety, driving growth in the market.

Top Key Players & Market Share Insights:

The global anti-drone market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global anti-drone market. Key players in the Anti-drone industry include-

- Raytheon Technologies Corporation (United States)

- Lockheed Martin Corporation (United States)

- Blighter Surveillance Systems Ltd (United Kingdom)

- SRC, Inc. (United States)

- Liteye Systems, Inc. (United States)

- Thales Group (France)

- Airbus Group SE (Netherlands)

- The Boeing Company (United States)

- Dedrone GmbH (Germany)

- DroneShield Ltd (Australia)

Recent Industry Developments :

Partnerships & Collaborations

- In December 2024, OpenAI partnered with defense-tech startup Anduril Industries to integrate artificial intelligence into the U.S. military's counter-drone systems. This collaboration aims to improve the detection and neutralization of unauthorized drones, marking OpenAI's significant entry into defense applications.

Mergers and Acquisitions

- In December 2024, L3Harris expanded its defense technology offerings by acquiring Aerojet Rocketdyne, a move that strengthens its position in propulsion systems and related technologies pertinent to counter-drone applications.

- In December 2024, BAE Systems acquired Ball Aerospace, enhancing its capabilities in space systems and advanced technologies, which are integral to modern defense strategies, including anti-drone solutions.

- In November 2024, AeroVironment announced an all-stock deal to acquire BlueHalo, a company specializing in drone defense systems and laser communication technologies, valued at approximately $4.1 billion. This strategic move aims to expand AeroVironment's portfolio in response to rising geopolitical tensions.

Anti-drone Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 20,560.60 Million |

| CAGR (2025-2032) | 25.8% |

| By Component |

|

| By Type |

|

| By Technology |

|

| By Application |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Anti-drone Market? +

In 2024, the Anti-drone Market was USD 3,277.78 million.

What will be the potential market valuation for the Anti-drone Market by 2032? +

In 2032, the market size of Anti-drone Market is expected to reach USD 20,560.60 million.

What are the segments covered in the Anti-drone Market report? +

The component, type, application, technology, and end-use are the segments covered in this report.

Who are the major players in the Anti-drone Market? +

Raytheon Technologies Corporation (United States), Lockheed Martin Corporation (United States), Thales Group (France), Airbus Group SE (Netherlands), The Boeing Company (United States), Dedrone GmbH (Germany), DroneShield Ltd (Australia), Blighter Surveillance Systems Ltd (United Kingdom), SRC, Inc. (United States), Liteye Systems, Inc. (United States) are the major players in the Anti-drone market.