- Summary

- Table Of Content

- Methodology

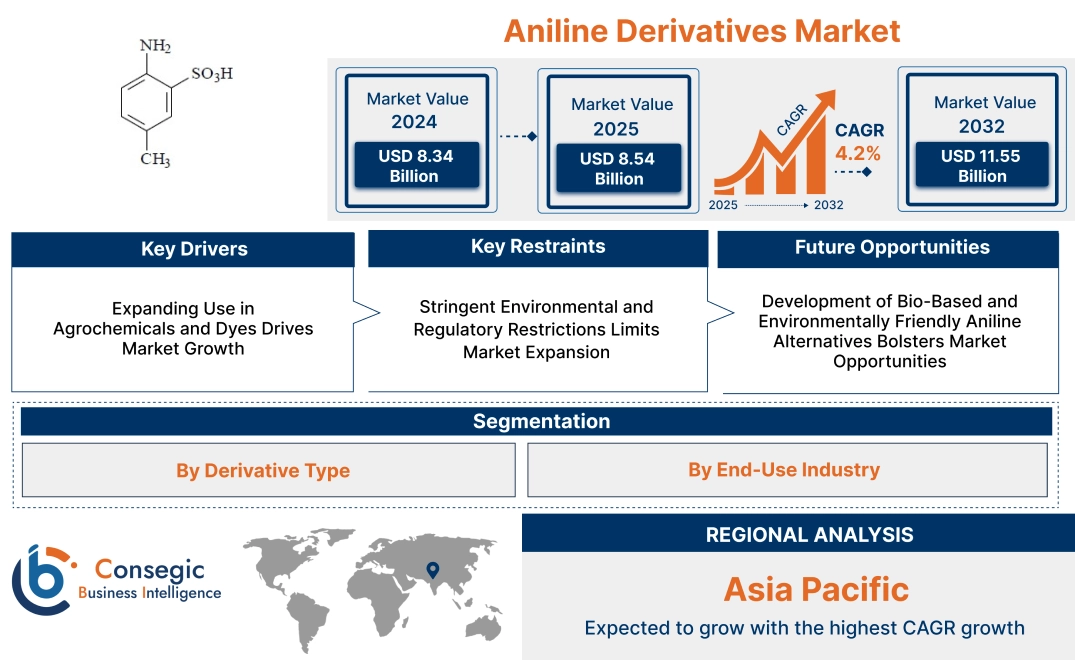

Aniline Derivatives Market Size:

Aniline Derivatives Market size is estimated to reach over USD 11.55 Billion by 2032 from a value of USD 8.34 Billion in 2024 and is projected to grow by USD 8.54 Billion in 2025, growing at a CAGR of 4.2% from 2025 to 2032.

Aniline Derivatives Market Scope & Overview:

Aniline derivatives are organic compounds derived from aniline, known for their role in chemical synthesis across multiple fields. These derivatives exhibit high reactivity, making them essential in the production of dyes, pharmaceuticals, agrochemicals, and rubber processing chemicals. They are typically characterized by an aromatic structure, strong nucleophilic properties, and a slightly pungent odor.

Key characteristics include solubility in organic solvents, stability under controlled conditions, and adaptability to chemical modifications. Their ability to undergo electrophilic substitution reactions makes them suitable for complex formulations in industrial applications. These compounds enhance the performance of coatings, pigments, and specialty chemicals, contributing to improved product durability and functionality.

Chemical manufacturers, pharmaceutical industries, and polymer producers utilize them in various synthesis processes requiring precision and efficiency. Advancements in processing technologies continue to refine their properties, ensuring their effectiveness in specialized formulations across different industrial sectors.

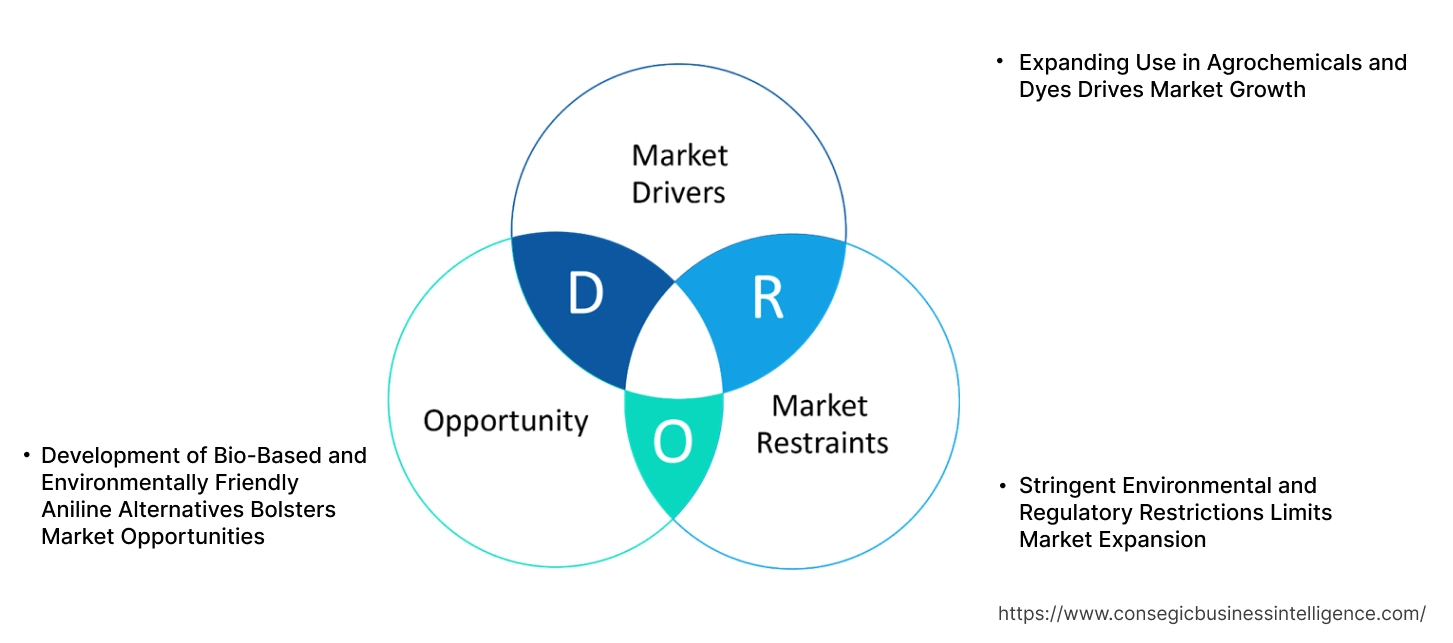

Aniline Derivatives Market Dynamics - (DRO):

Key Drivers:

Expanding Use in Agrochemicals and Dyes Drives Market Growth

In the agricultural sector, aniline derivatives are widely used in the formulation of herbicides, fungicides, and insecticides, improving crop protection and yield. As farming practices modernize and food production scales up, the need for high-performance chemical formulations continues to rise. Additionally, the textile and printing industries rely on aniline-based dyes and pigments for fabric coloring, ink production, and coatings. The increasing consumption of vibrant and long-lasting synthetic dyes in clothing, automotive coatings, and industrial applications is further strengthening market growth. With emerging economies investing in chemical manufacturing and agricultural advancements, the market is witnessing heightened need for efficient and cost-effective aniline-based products. These trends are expected to contribute significantly to aniline derivatives market expansion, reinforcing their role in multiple high-growth industries.

Key Restraints:

Stringent Environmental and Regulatory Restrictions Limits Market Expansion

Regulatory agencies such as EPA, REACH, and other global environmental bodies impose strict guidelines on waste disposal, emissions control, and worker safety, increasing compliance costs for manufacturers. The classification of some aniline-based chemicals as hazardous substances has resulted in limitations on their use in consumer applications, food packaging, and pharmaceuticals. Additionally, governments are encouraging the adoption of low-toxicity and biodegradable alternatives, which affects the demand for conventional formulations. Meeting evolving regulatory standards requires significant investment in green production technologies, pollution control systems, and sustainable sourcing, raising operational expenses. Companies that fail to comply face market restrictions, legal penalties, and reduced competitiveness. Overcoming these challenges through innovation and regulatory adaptation will be crucial for ensuring aniline derivatives market growth in the evolving chemical sector.

Future Opportunities:

Development of Bio-Based and Environmentally Friendly Aniline Alternatives Bolsters Market Opportunities

Manufacturers are investing in renewable feedstocks, green chemistry techniques, and enzymatic synthesis processes to reduce environmental impact and meet regulatory requirements. The growth of biodegradable and low-toxicity formulations is expanding opportunities in industries such as textiles, pharmaceuticals, and specialty coatings, where environmental concerns are a priority. Additionally, government policies supporting low-carbon and circular economy practices are encouraging the adoption of plant-based raw materials for chemical production. Companies focusing on bio-derived intermediates and recyclable aniline alternatives are gaining a competitive advantage in sustainability-driven markets.

- For instance, in February 2024, Covestro opened the world’s first bio-based aniline manufacturing facility that utilizes plant biomass instead of petroleum for production. This marks an important milestone in achieving a circular economy and minimizing the carbon footprint of the plastics sector, in which aniline is significantly used.

As industries continue to shift toward environmentally responsible manufacturing, the expansion of bio-based aniline innovations is expected to create new aniline derivatives market opportunities, reinforcing their role in the next generation of green chemical solutions.

Aniline Derivatives Market Segmental Analysis :

By Derivative Type:

Based on derivative type, the aniline derivatives market is segmented into aniline, methyl-anilines, ethyl-anilines, and others.

The aniline segment held the largest aniline derivatives market share in 2024.

- Aniline is widely used in the production of dyes, rubber processing chemicals, and agricultural products, ensuring its dominance in the market.

- The need for high-purity chemicals is rising, particularly in pharmaceuticals and polymer production.

- Market analysis suggests that manufacturers are focusing on refining aniline processing techniques, ensuring enhanced efficiency and product quality.

- As per aniline derivatives market trends, expanding applications in polyurethane and specialty coatings are further driving growth in this segment.

The methyl-anilines segment is expected to experience the fastest CAGR during the forecast period.

- Methyl-anilines are widely used in the chemical and rubber industries, making them an essential component in various industrial processes.

- The need for methyl-anilines is increasing in the production of agrochemicals, antioxidants, and high-performance coatings.

- Segmental trends analysis suggest that advancements in methyl-aniline-based formulations are improving product stability and efficiency.

- Thus, with ongoing developments in chemical processing and specialty chemicals, this segment is contributing to the aniline derivatives market expansion.

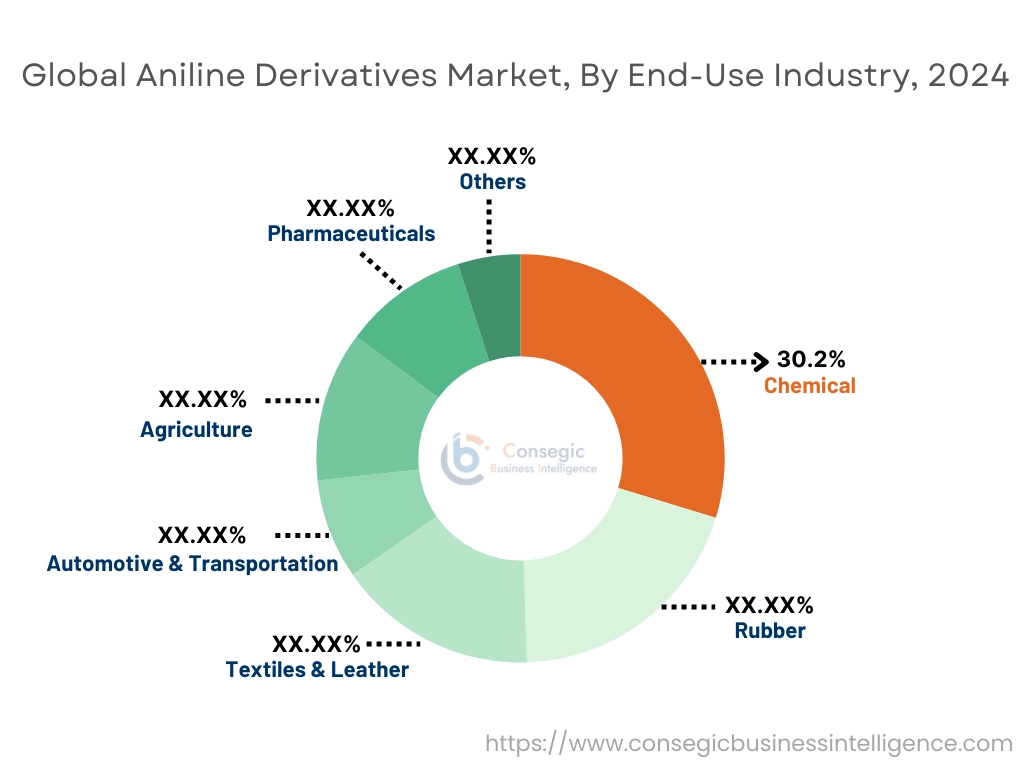

By End-Use Industry:

By end-use industry, the market is segmented into textiles & leather, automotive & transportation, agriculture, pharmaceuticals, chemical, rubber, and others.

The chemical segment held the largest aniline derivatives market share of 30.2% in 2024.

- Aniline derivatives are widely utilized as intermediates in the synthesis of dyes, pigments, solvents, and specialty chemicals that support industrial and consumer formulations.

- The chemical sector benefits from consistent demand for aniline-based compounds including methylene diphenyl diisocyanate (MDI), used in polyurethane production and high-performance coatings.

- Strong industrial output across emerging economies contributes to steady consumption of downstream chemical derivatives.

- According to aniline derivatives market trends, stable regulatory frameworks and global trade of chemical intermediates drive this segment’s leadership.

- Growth in specialty chemicals and advanced intermediates continues to reinforce the segment’s contribution to overall market expansion.

The rubber segment is expected to achieve the fastest CAGR during the forecast period.

- Aniline derivatives such as N-phenyl-1-naphthylamine and other aromatic amines are crucial antioxidants and accelerators in rubber compounding.

- Rising global need for durable and high-performance rubber products, particularly in tires, automotive components, and industrial belts, is fueling adoption.

- Segmental trends indicate increased focus on enhancing rubber aging resistance and performance in extreme conditions.

- Thus, this segment’s acceleration is aligned with global automotive production recovery and infrastructure-related material consumption, supporting long-term aniline derivatives market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

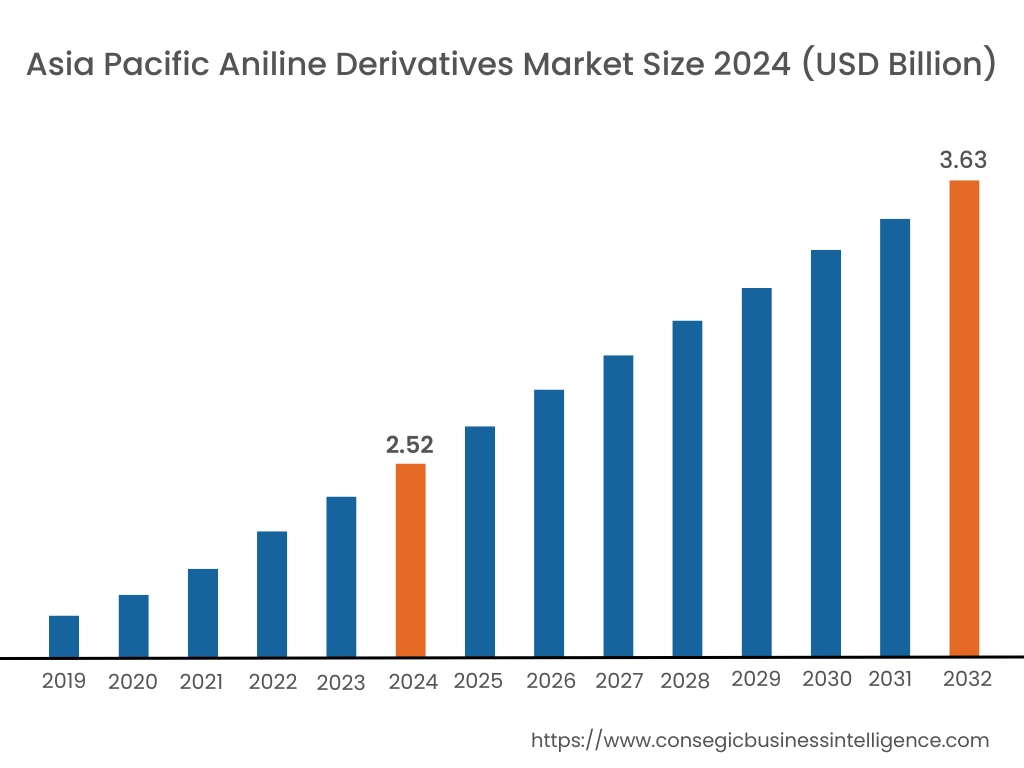

Asia-Pacific region was valued at USD 2.52 Billion in 2024. Moreover, it is projected to grow by USD 2.58 Billion in 2025 and reach over USD 3.63 Billion by 2032. Out of this, China accounted for the maximum revenue share of 45.3%. The Asia-Pacific region is experiencing rapid growth in the aniline derivatives market due to rising industrialization, infrastructure development, and expanding chemical manufacturing capabilities. Countries like China, India, and Japan are leading the market, benefiting from cost-effective production and high domestic consumption. The increasing need for aniline-based compounds in polyurethane production, agrochemicals, and pharmaceuticals contributes significantly to market expansion. Furthermore, government initiatives promoting domestic chemical production and exports create a substantial aniline derivatives market opportunity for both regional and global manufacturers.

North America is estimated to reach over USD 3.24 Billion by 2032 from a value of USD 2.28 Billion in 2024 and is projected to grow by USD 2.34 Billion in 2025. As per aniline derivatives market analysis of North America, the demand for aniline derivatives is largely fueled by the automotive, construction, and pharmaceutical sectors. The region benefits from advanced manufacturing capabilities and a strong regulatory framework ensuring the safe production and application of these chemicals. The increasing focus on sustainable and high-performance materials has led to a shift towards specialty chemicals for coatings, rubber processing, and adhesives. Additionally, research and development efforts are driving innovation, addressing both safety concerns and expanding product applications.

Europe exhibits a well-established aniline derivatives industry, primarily supported by stringent environmental regulations and the region’s focus on sustainable chemical production. Countries such as Germany, France, and the United Kingdom are key players in producing and consuming these derivatives, particularly for dyes, pigments, and agricultural chemicals. The emphasis on eco-friendly alternatives has resulted in a growing interest in bio-based aniline derivatives. The steady demand for specialty chemicals in industrial applications continues to reinforce aniline derivatives market demand.

As per aniline derivatives market analysis, the Latin American market is steadily evolving, with demand stemming from agricultural applications and the production of dyes and coatings. Brazil and Mexico, in particular, are key markets where chemical industries are growing in response to increasing demand for specialty and high-performance materials. The adoption of aniline derivatives in pesticide formulations is crucial for the agricultural sector, which remains a driving force behind the market’s regional expansion. Infrastructure development and industrial growth further contribute to sustained market activity.

The aniline derivatives market demand in the Middle East and Africa is rising due to increasing investments in industrial applications and chemical manufacturing. It is primarily driven by construction, automotive, and oil-based industries that utilize aniline derivatives for coatings, adhesives, and synthetic rubber. While regulatory challenges and market accessibility issues persist, the gradual shift towards diversified industrial sectors supports ongoing analysis and potential future expansion.

Top Key Players & Market Share Insights:

The aniline derivatives market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global aniline derivatives market. Key players in the aniline derivatives industry include -

- Covestro AG (Germany)

- LANXESS (Germany)

- Tosoh Corporation (Japan)

- INEOS Phenol (UK)

- BASF SE (Germany)

- Huntsman International LLC (USA)

- Wanhua Chemical Group Co., Ltd. (China)

- Jilin Connell Chemical Industry Co., Ltd. (China)

- Aarti Industries Ltd (India)

- Mitsubishi Chemical Corporation (Japan)

Aniline Derivatives Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 11.55 Billion |

| CAGR (2025-2032) | 4.2% |

| By Derivative Type |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Aniline Derivatives Market? +

Aniline Derivatives Market size is estimated to reach over USD 11.55 Billion by 2032 from a value of USD 8.34 Billion in 2024 and is projected to grow by USD 8.54 Billion in 2025, growing at a CAGR of 4.2% from 2025 to 2032.

What specific segmentation details are covered in the Aniline Derivatives Market report? +

The Aniline Derivatives market report includes specific segmentation details for derivative type and end-use industry.

Which is the fastest-growing region in the Aniline Derivatives Market? +

Asia Pacific is the fastest-growing region in the Aniline Derivatives market. These trends are encouraged by rising industrialization, infrastructure development, and expanding chemical manufacturing capabilities.

Who are the major players in the Aniline Derivatives Market? +

The key participants in the Aniline Derivatives market are Covestro AG (Germany), LANXESS (Germany), Huntsman International LLC (USA), Wanhua Chemical Group Co., Ltd. (China), Jilin Connell Chemical Industry Co., Ltd. (China), Aarti Industries Ltd (India), Mitsubishi Chemical Corporation (Japan), Tosoh Corporation (Japan), INEOS Phenol (UK) and BASF SE (Germany).