- Summary

- Table Of Content

- Methodology

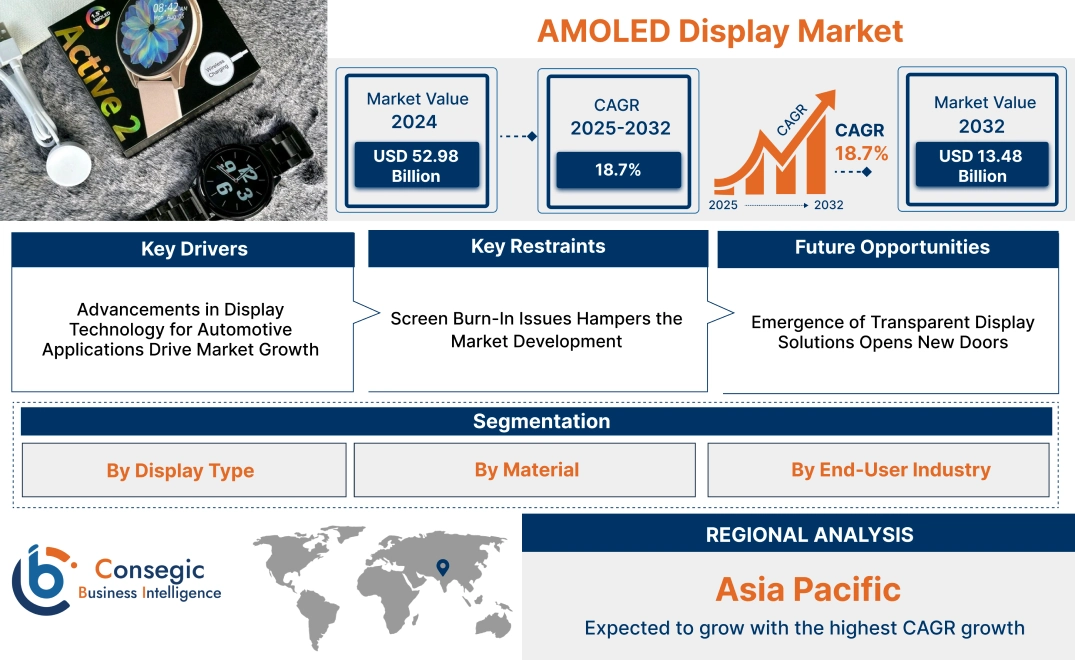

AMOLED Display Market Size:

AMOLED Display Market size is estimated to reach over USD 52.98 Billion by 2032 from a value of USD 13.48 Billion in 2024 and is projected to grow by USD 15.76 Billion in 2025, growing at a CAGR of 18.7% from 2025 to 2032.

AMOLED Display Market Scope & Overview:

An AMOLED (Active Matrix Organic Light Emitting Diode) display is an advanced screen technology known for its high-resolution visuals, vibrant colors, and energy efficiency. These displays utilize organic compounds that emit light when an electric current is applied, eliminating the need for a backlight and enabling thinner and lighter designs. They are widely used in devices such as smartphones, televisions, wearables, and automotive displays.

AMOLED displays are available in various configurations, including flexible and rigid formats, catering to diverse design and application requirements. Their ability to provide deep blacks, wide viewing angles, and fast response times makes them suitable for applications that demand high visual quality and performance. These displays are also engineered to offer longevity and durability, ensuring reliability across different usage scenarios.

End-users of this technology include manufacturers of consumer electronics, automotive systems, and industrial devices seeking premium display solutions to enhance product functionality and user experience. These screens play a crucial role in shaping the visual quality of next-generation devices.

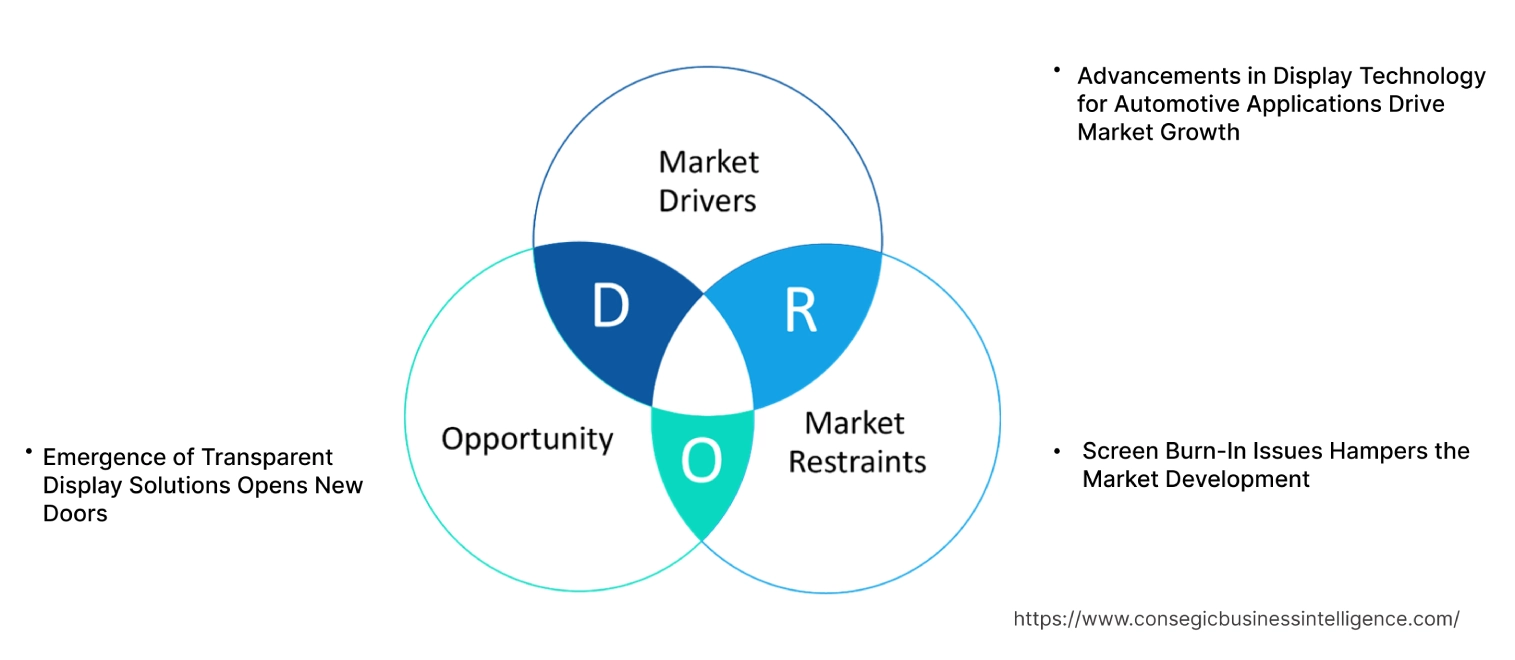

AMOLED Display Market Dynamics - (DRO) :

Key Drivers:

Advancements in Display Technology for Automotive Applications Drive Market Growth

The automotive sector is rapidly integrating advanced display systems to enhance driver experience and safety. AMOLED technology is becoming a preferred choice for infotainment systems, digital dashboards, and heads-up displays due to its superior image quality, vibrant colors, and high contrast ratios. These displays provide clear visibility even under challenging lighting conditions, such as direct sunlight or nighttime driving.

Additionally, the flexibility of AMOLED displays allows for curved and uniquely shaped screens, catering to modern vehicle designs. As automakers increasingly adopt digital interfaces for navigation, entertainment, and vehicle controls, the demand for high-performance displays is rising. This trend aligns with the growing focus on connected vehicles and electric cars, further boosting the adoption of AMOLED technology in the automotive sector. Thus, the aforementioned factors are fueling the AMOLED display market growth.

Key Restraints:

Screen Burn-In Issues Hampers the Market Development

AMOLED displays are susceptible to screen burn-in, a phenomenon where static images left on the screen for extended periods cause permanent damage. This issue arises from the uneven aging of organic materials in the display, resulting in visible "ghost" images or shadows on the screen. Prolonged use of the screen at maximum brightness exacerbates the problem, reducing the display's overall lifespan and visual quality.

Screen burn-in is particularly concerning for devices used to display static content, such as navigation systems or menu screens. These durability concerns limit the adoption of AMOLED technology in applications where prolonged static imagery is common, impacting its suitability in certain industries such as automotive and retail signage. This constraint highlights the need for enhanced material development and usage guidelines to ensure the longevity of these displays. In conclusion, screen burn-in issues are limiting the AMOLED display market demand.

Future Opportunities :

Emergence of Transparent Display Solutions Opens New Doors

Transparent display technology is revolutionizing various industries, offering innovative applications in areas such as smart retail, automotive windshields, and interactive displays. AMOLED technology, with its self-emissive properties and superior color reproduction, is ideally suited for transparent screens, enabling high clarity and vivid visuals without backlighting. In smart retail, transparent displays enhance customer engagement by overlaying digital information on products.

In the automotive sector, these displays are being integrated into windshields to provide heads-up information, improving driver safety and convenience. Additionally, transparent AMOLED screens are finding use in futuristic interactive panels for exhibitions, offices, and home automation. As industries seek cutting-edge solutions for enhanced user experiences, the emergence of transparent displays is creating significant AMOLED display market opportunities.

AMOLED Display Market Segmental Analysis :

By Display Type:

Based on display type, the market is segmented into flexible displays, transparent displays, and 3D displays.

The flexible displays segment held the largest revenue of the total AMOLED display market share in 2024.

- Flexible displays offer superior versatility, enabling innovative designs such as foldable and rollable screens for consumer electronics.

- The dominance of this segment is driven by the widespread adoption of foldable smartphones and wearable devices incorporating flexible display technology.

- These displays are increasingly used in automotive applications for infotainment systems and advanced dashboard designs.

- The analysis of segmental trends depicts that flexible displays are preferred for their lightweight construction, durability, and ability to withstand mechanical stress, making them a popular choice across industries, contributing to the AMOLED display market expansion.

The 3D displays segment is projected to register the fastest CAGR during the forecast period.

- The rising need for immersive visual experiences in gaming, entertainment, and virtual reality applications drives the adoption of 3D displays.

- Advancements in holographic and augmented reality technologies further contribute to the segment's rapid progression.

- 3D displays are increasingly used in healthcare for medical imaging and diagnostics, offering enhanced depth perception and precision.

- As per the AMOLED display market analysis, the segment's growth is supported by innovations in display technologies and increasing investment in AR/VR ecosystems.

By Material:

Based on material, the market is categorized into polymer, glass, and glass substrate.

The polymer segment accounted for the largest revenue of the total AMOLED display market share in 2024.

- Polymer-based AMOLED displays are lightweight, flexible, and highly durable, making them suitable for a wide range of applications.

- Their dominance is attributed to the increasing adoption of polymer displays in foldable smartphones, wearables, and automotive interiors.

- Polymer materials enable the production of ultra-thin and energy-efficient displays, enhancing device portability and battery life.

- As per the AMOLED display market trends, the rising popularity of flexible and rollable displays supports the growth of the polymer segment in the market.

The glass substrate segment is expected to grow at the fastest CAGR during the forecast period.

- Glass substrates are critical for rigid AMOLED displays, widely used in televisions, laptops, and industrial applications.

- The segment's growth is driven by the demand for high-resolution and durable displays offering superior image quality.

- Technological advancements in glass manufacturing, such as the development of ultra-thin and shatterproof glass, enhance its applicability.

- Therefore, the increased adoption of glass substrates in premium consumer electronics contributes to the segment's rapid extension, which further boosts the AMOLED display market growth.

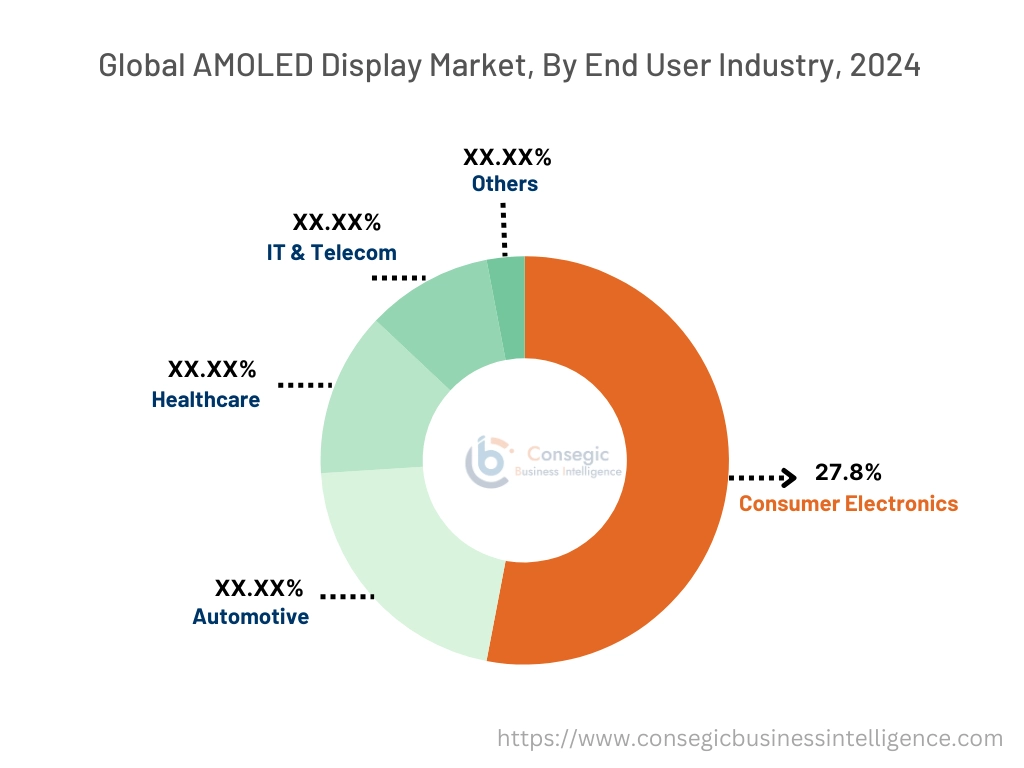

By End User Industry:

Based on the end-user industry, the market is segmented into consumer electronics, automotive, healthcare, IT & telecom, and others.

The consumer electronics segment held the largest revenue of 52.3% share in 2024.

- Consumer electronics dominate the market due to the extensive use of AMOLED displays in smartphones, televisions, and wearable devices.

- The growing preference for high-quality visuals and immersive experiences fuels the demand for these displays in this sector.

- They are widely used in premium consumer electronics for their vibrant colors, higher contrast ratios, and energy efficiency.

- As per the AMOLED display market analysis, the increasing adoption of foldable and flexible displays in consumer electronics supports the segment's dominance.

The automotive segment is projected to grow at the fastest CAGR during the forecast period.

- The rising integration of advanced infotainment systems and digital dashboards drives the demand for AMOLED displays in automotive applications.

- These displays are preferred for their flexibility, enabling innovative designs in next-generation electric and autonomous vehicles.

- The use of transparent displays for heads-up displays (HUDs) and augmented reality features in vehicles supports the segment's expansion.

- The segment's growth is further driven by advancements in AMOLED technology and increasing investment in automotive electronics, creating significant AMOLED display market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

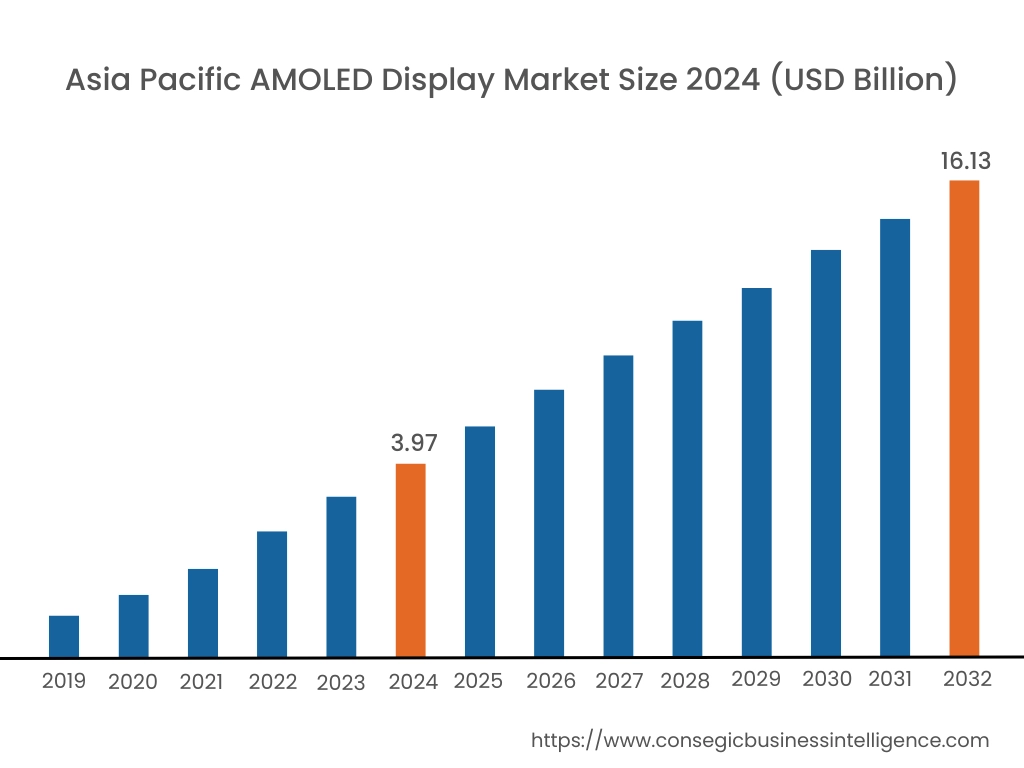

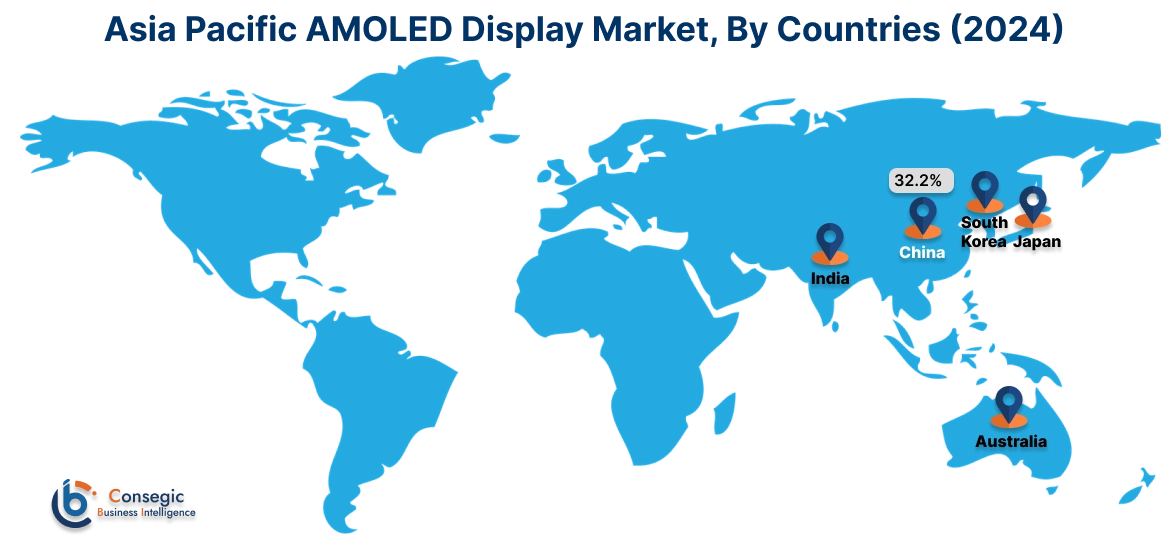

Asia Pacific region was valued at USD 3.97 Billion in 2024. Moreover, it is projected to grow by USD 4.65 Billion in 2025 and reach over USD 16.13 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.2%. The Asia-Pacific region is experiencing rapid development in the AMOLED display market, driven by industrialization and technological advancements in countries such as China, Japan, and South Korea. The enlargement of the consumer electronics sector and the rising need for high-quality displays have intensified the need for advanced display technologies like AMOLED. Government initiatives promoting industrial efficiency further influence AMOLED display market expansion.

North America is estimated to reach over USD 17.17 Billion by 2032 from a value of USD 4.47 Billion in 2024 and is projected to grow by USD 5.22 Billion in 2025. This region holds a substantial share of the AMOLED display market, driven by the increasing adoption of advanced display technologies in consumer electronics, automotive, and healthcare sectors. The United States, in particular, has seen a rise in the implementation of AMOLED displays in smartphones and wearable devices. A notable trend is the integration of flexible and foldable AMOLED screens in next-generation devices, enhancing user experience and device versatility. Analysis indicates that the presence of key market players and continuous technological innovations contribute to the AMOLED display market demand.

Europe represents a significant portion of the global AMOLED display market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on sustainability and energy efficiency has propelled the utilization of eco-friendly display solutions. Analysis indicates a growing trend towards the deployment of AMOLED displays in automotive infotainment systems and industrial applications, offering enhanced visual performance and design flexibility.

The Middle East & Africa region shows a growing interest in advanced display solutions, particularly in the telecommunications and industrial sectors. Countries like the United Arab Emirates and South Africa are investing in modern technologies to enhance data acquisition capabilities and comply with international standards. Analysis suggests an increasing trend towards adopting AMOLED displays to meet the needs of modern imaging applications.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's growing focus on technological modernization and the automotive sector has spurred the adoption of advanced display solutions. As per the AMOLED display market trends, government policies aimed at enhancing technological capabilities influence market trends.

Top Key Players and Market Share Insights:

The AMOLED Display market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global AMOLED Display market. Key players in the AMOLED Display industry include -

- Samsung Display (South Korea)

- LG Display (South Korea)

- AU Optronics (AUO) (Taiwan)

- Japan Display Inc. (JDI) (Japan)

- BOE Technology Group (China)

- Tianma Microelectronics (China)

- Visionox (China)

- EverDisplay Optronics (EDO) (China)

Recent Industry Developments :

Product Launches:

- In September 2024, Samsung launched Galaxy Book5 Pro 360, its first AI-powered 2-in-1 PC in the Galaxy Book5 series. Equipped with Intel Core Ultra processors (Series 2) and the Intel Arc GPU, it offers 47 TOPs NPU and 300+ AI-enhanced features. Key highlights include a Dynamic AMOLED 2X display, all-day battery life, and seamless Galaxy ecosystem integration via Microsoft Phone Link. With advanced productivity tools like Live Translate and Transcript Assist, it redefines mobile computing. Slim, lightweight, and boasting Dolby Atmos speakers, it’s ideal for work and entertainment.

- In September 2024, Xiaomi launched the Xiaomi 14T Series, designed for photography enthusiasts, featuring next-gen Leica optics, AI-powered enhancements, and superior night photography. The flagship Xiaomi 14T Pro boasts a 50MP Leica lens, advanced computational photography, and cinematic video capabilities. Both models offer seamless AI integration, 6.67-inch AMOLED displays, and cutting-edge MediaTek processors.

- In April 2024, Samsung launched Galaxy M55 5G and Galaxy M15 5G, boasting segment-leading features like Super AMOLED Plus displays, powerful processors, and monster batteries. The Galaxy M55 5G offers a 6.7” FHD+ 120Hz display, Snapdragon 7 Gen1 chip, 5000mAh battery, and a 50MP (OIS) camera, while the Galaxy M15 5G features a 6.5” AMOLED display, Dimensity 6100+, 6000mAh battery, and a triple camera setup.

AMOLED Display Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 52.98 Billion |

| CAGR (2025-2032) | 18.7% |

| By Display Type |

|

| By Material |

|

| By End User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the AMOLED Display Market? +

AMOLED Display Market size is estimated to reach over USD 52.98 Billion by 2032 from a value of USD 13.48 Billion in 2024 and is projected to grow by USD 15.76 Billion in 2025, growing at a CAGR of 18.7% from 2025 to 2032.

What are the key segments in the AMOLED Display Market? +

The AMOLED Display Market is segmented by display type (flexible displays, transparent displays, 3D displays), material (polymer, glass, glass substrate), end-user industry (consumer electronics, automotive, healthcare, IT & telecom, others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which display type is expected to dominate the AMOLED Display Market? +

The flexible displays segment held the largest revenue share in 2024 and is expected to continue dominating the market due to the widespread adoption of foldable smartphones, wearables, and automotive applications.

Which segment is projected to grow the fastest in the AMOLED Display Market? +

The 3D displays segment is projected to register the fastest CAGR during the forecast period, driven by the increasing demand for immersive visual experiences in gaming, entertainment, and virtual reality (VR) applications.

Who are the major players in the AMOLED Display Market? +

Key players in the AMOLED Display Market include Samsung Display (South Korea), LG Display (South Korea), BOE Technology Group (China), Tianma Microelectronics (China), Visionox (China), EverDisplay Optronics (EDO) (China), AU Optronics (AUO) (Taiwan), and Japan Display Inc. (JDI) (Japan).