- Summary

- Table Of Content

- Methodology

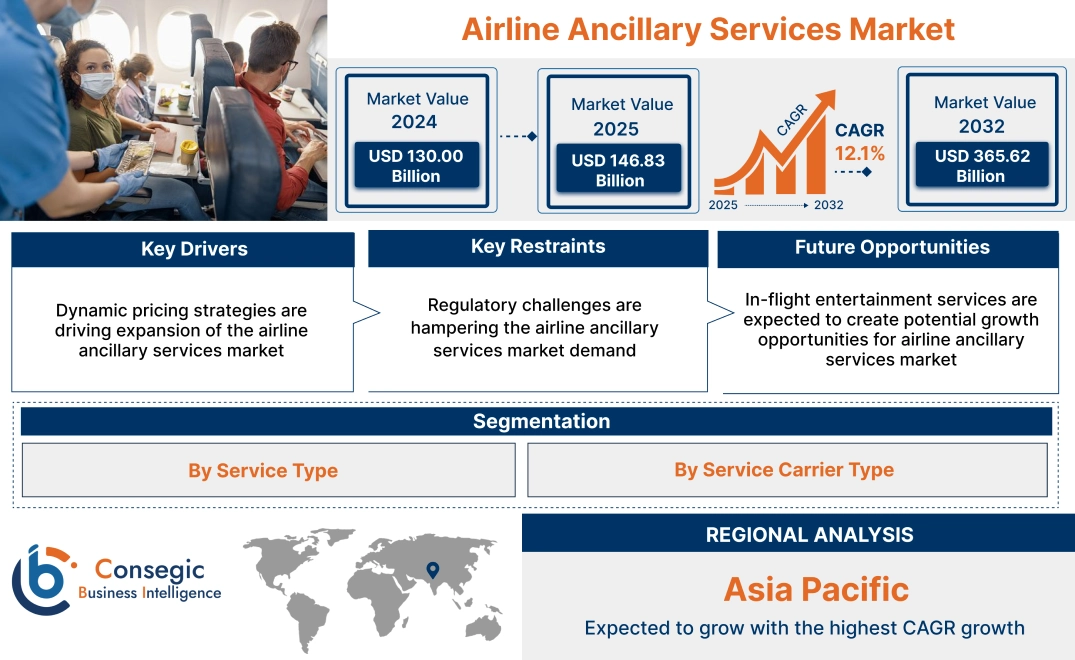

Airline Ancillary Services Market Size:

Airline Ancillary Services Market Size is estimated to reach over USD 365.62 Billion by 2032 from a value of USD 130.00 Billion in 2024 and is projected to grow by USD 146.83 Billion in 2025, growing at a CAGR of 12.1% from 2025 to 2032.

Airline Ancillary Services Market Scope & Overview:

Airline ancillary services encompass supplementary products or services provided by airlines beyond the standard ticket fare. These optional offerings are designed to meet the unique needs, preferences, or convenience of passengers, thereby generating additional revenue for airlines. The common examples of ancillary services include seat selection, additional baggage allowance, priority boarding, in-flight Wi-Fi, meals, entertainment, and travel insurance. Further, as airlines contend with fierce competition and narrow profit margins, ancillary services have gained significance. By extending their revenue sources, airlines can mitigate operating costs and enhance profitability.

Airline Ancillary Services Market Dynamics - (DRO) :

Key Drivers:

Dynamic pricing strategies are driving expansion of the airline ancillary services market

Dynamic pricing strategies for airline ancillary services have emerged as a beneficial trend, transforming how airlines optimize revenue and improve customer satisfaction. Leveraging advanced algorithms and data analytics, airlines can adjust prices for add-on services such as seat upgrades, baggage allowances, and in-flight amenities based on factors like demand, time until departure, and customer preferences. This strategy benefits both airlines and passengers, which fosters customer loyalty and increases ancillary revenue streams. Airlines can maximize revenue by taking advantage of demand fluctuations and offering personalized pricing options. Passengers gain the flexibility to select services that align with their needs and budgets, resulting in a more tailored travel experience.

Moreover, dynamic pricing promotes early bookings, enhances inventory management, and can help minimize overbooking and flight disruptions. It also allows airlines to provide targeted promotions and incentives, fostering customer loyalty and boosting ancillary revenue streams. Overall, dynamic pricing strategies for airline ancillary services create a mutually advantageous situation, driving profitability for airlines in the near future.

- For instance, the incorporation of artificial intelligence (AI) and real-time data collection has elevated dynamic pricing in the airline industry to new levels. AI-driven tools assess real-time data, including search patterns, current bookings, and external influences such as weather or political events. This enables airlines to forecast demand with remarkable precision. Additionally, real-time analytics uncover customer behaviour patterns, enabling airlines to provide personalized pricing tailored to customer preferences and willingness to pay.

Thus, according to the airline ancillary services market analysis, these developments and trends are driving the airline ancillary services market size.

Key Restraints:

Regulatory challenges are hampering the airline ancillary services market demand

Government and regulatory bodies frequently intervene in the airline industry to safeguard consumer interests and promote fair competition. Regulations regarding pricing transparency, baggage fees, and other ancillary services may restrict airlines' capacity to optimize revenue from these offerings. Further, regulations mandating that airlines are solely responsible for compensating or providing care and assistance due to delays fail to tackle the underlying issue of why delays happen. This approach overlooks the market dynamics that would incentivize airlines to find solutions to retain their customers. Additionally, it may lead airlines to cancel flights, resulting in an even more negative experience for passengers. These factors and analysis are hindering the progress of the market trends.

Future Opportunities :

In-flight entertainment services are expected to create potential growth opportunities for airline ancillary services market

In-flight entertainment (IFE) has become a fundamental component of airline ancillary services, indicating a positive trend within the aviation industry. Providing a wide variety of entertainment options during flights improves the overall passenger experience, making journeys more enjoyable and comfortable. This trend demonstrates airlines' dedication to accommodating the evolving preferences of passengers, who increasingly desire personalized and immersive experiences during their flights.

Further, the integration of Wi-Fi connectivity on many flights allows passengers to remain connected to the digital world, promoting productivity, communication, and social engagement throughout their journey. As airlines continue to invest in improving their IFE offerings, they not only distinguish themselves in a competitive market but also cultivate increased passenger satisfaction and loyalty. Ultimately, in-flight entertainment represents a favorable trend that enriches the overall travel experience and contributes to the success of airlines in fulfilling passenger expectations.

- For instance, in December 2024, Air India has extended its wireless in-flight entertainment services to its single-aisle fleet. The service Vista Stream allows airline passengers to stream a diverse range of entertainment content directly to their personal electronic devices, including tablets, laptops, and smartphones. Additionally, it includes a live map for real-time flight tracking and is compatible with Windows, Android, and iOS, providing easy access to entertainment for all throughout the flight.

Thus, based on the above analysis, these factors are driving the airline ancillary services market opportunities.

Airline Ancillary Services Market Segmental Analysis :

By Service Type:

Based on the service type, the market is segmented into baggage fees, airline retail, onboard services, pet transportation services, frequent flyer program services (FFP), travel insurance services, lounge services, paid seats, flight marketing services, pre-paid wi-fi services, disability-related accommodations services, and others.

Trends in the service type:

- Personalization has become a key focus, as airlines customize ancillary offerings to align with individual passenger preferences through advanced data analysis, resulting in targeted upgrades and amenities.

- Airlines are eager to expand their ancillary revenue streams beyond conventional offerings, forming partnerships with third-party vendors for services like car rentals and travel insurance, while also tackling environmental issues through eco-friendly solutions such as carbon offset programs and sustainable inflight products. This ongoing evolution highlights the necessity for airlines to quickly adapt to these trends, not only to improve customer satisfaction but also to create additional revenue prospects.

The baggage fees segment accounted for the largest revenue share in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Airlines strategically design their fee structures, frequently utilizing tiered pricing based on factors such as luggage weight, size, and travel class. These fees play a crucial role in augmenting airlines' ancillary revenue, enabling them to mitigate operational costs and maintain competitive ticket pricing.

- Additionally, ancillary services such as priority baggage handling and excess baggage allowances offer more chances for airlines to cater to the varied needs and preferences of passengers.

- In November 2024, Air India has changed its baggage policy for flights to Europe and the U.K., aligning with international carriers. The new policy introduces fare categories with different baggage allowances. The basic value fare includes one checked bag, while higher tiers provide more baggage and flexibility. Passengers requiring an additional checked-in bag must select a higher fare class, with prices starting around USD 46.63 (INR 4,000) for a one-way trip.

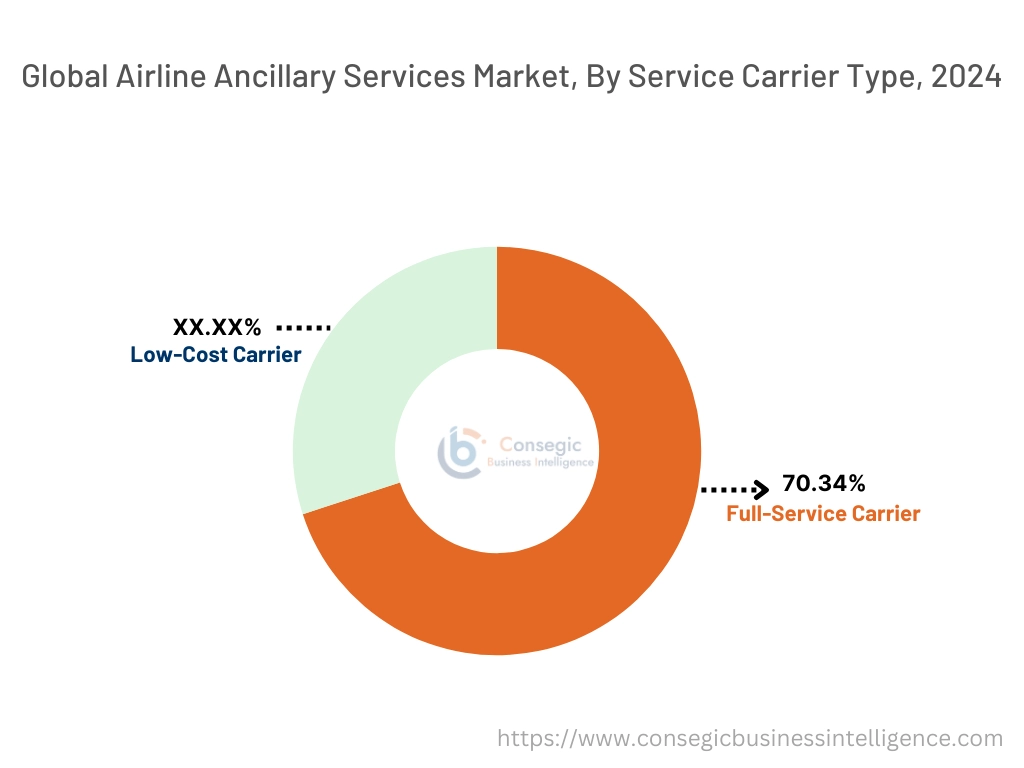

By Service Carrier Type:

Based on the service carrier type, the airline ancillary services market is segmented into full-service carrier and low-cost carrier.

Trends in the service carrier type:

- Technology has been instrumental in the development of ancillary revenue. Online booking platforms and mobile applications facilitate airlines in providing and selling a diverse array of ancillary services directly to passengers.

- Consumers are becoming more price-sensitive and are inclined to pay only for the services they require. This change in consumer behaviour has fostered a conducive environment for the development of ancillary revenue.

Full-service carrier segment accounted for the largest revenue share of 70.34% in the year 2024.

- Full-service carriers are consistently working to improve the customer experience through innovations such as personalized service, upgraded in-flight entertainment, and enhanced dining options.

- There is a growing focus on sustainability, featuring initiatives aimed at reducing carbon emissions, implementing eco-friendly practices, and providing sustainable in-flight amenities.

- Sustainability is increasingly important in the full-service airline segment, driven by environmental concerns, regulatory needs, and shifting consumer preferences.

- Airlines are adopting sustainable practices such as fuel-efficient aircraft and sustainable aviation fuels to set themselves apart in a competitive market.

- In November 2022, Vistara enhanced its daily frequencies to Frankfurt and Paris from Delhi with the Boeing 787-9 aircraft. The airline has publicised plans to operate six flights per week on the Delhi-Frankfurt route and to increase the frequency on the Delhi-Paris route to five times per week.

- These factors, analysis, and developments would further supplement the airline ancillary services market trends during the forecast period.

The low-cost carrier aviation segment is anticipated to register the fastest CAGR during the forecast period.

- Low-cost airlines operate with a lower cost structure compared to traditional carriers. These airlines offer discounted fares to passengers, offsetting revenue losses by charging for additional services such as food, priority boarding, seat selection, and baggage.

- Furthermore, many low-cost carriers maintain a single aircraft type in their fleets, minimizing the training requirements for crew members.

- Point-to-point business model in the airline sector allows airlines to transport passengers directly between specific city pairs, bypassing intermediaries, and hubs. This model aims to minimize travel time, enhance convenience, and often leads to more competitive rates due to decreased operational costs.

- For instance, in June 2023, SkyUp Airlines LLC, a Ukrainian low-cost carrier, has been granted a license by the U.S. Department of Transportation (DoT) to operate foreign air flights of its Boeing 737 with a simplified process.

- These factors and developments would further supplement the airline ancillary services market trends during the forecast period.

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

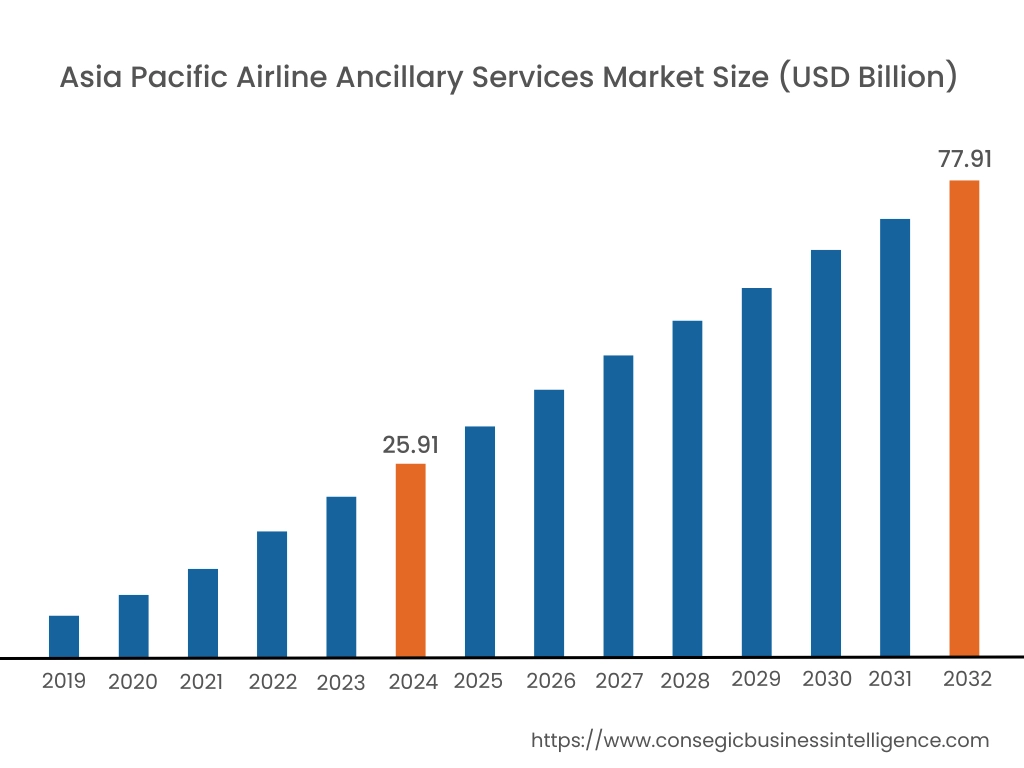

Asia Pacific airline ancillary services market expansion is estimated to reach over USD 77.91 billion by 2032 from a value of USD 25.91 billion in 2024 and is projected to grow by USD 29.43 billion in 2025. Out of this, China airline ancillary services market accounted for the maximum revenue share of 35.56%. The exponential growth of working professionals in developing countries has led to an increase in freight traffic and disposable income. According to the United Nations, the rising number of middle-class travelers, particularly in China and India, is the primary driver of the development in air travel and related services in the region. As the global economy recovers from contractions, the need for air travel continues to rise. This heightened demand has resulted in an increased production of commercial aircraft, significantly boosting various ancillary services such as in-flight shopping, food and beverages, excess luggage, and in-flight Wi-Fi. Further, according to IATA, the number of air passengers reached 4.54 billion in 2019 and in 2023, global air passenger numbers climbed to 95% of pre-pandemic levels, totaling 4.35 billion individuals. The growing passenger numbers worldwide are prompting a need for more exciting and comfortable flight experiences. In-flight catering or culinary services has emerged as a key trend among both full-service and low-cost carriers. These factors are expected to further drive the regional airline ancillary services market share in the coming years.

- For instance, in March 2023, Vistara, a full-service carrier, has launched a daily non-stop service between Mumbai and Dammam, Saudi Arabia. This initiative expands the airline’s international footprint in the Gulf region. The inclusion of Dammam in the airline’s expanding international network aligns with its objective to enhance its presence in the Middle East.

North America airline ancillary services market growth is estimated to reach over USD 140.55 billion by 2032 from a value of USD 50.34 billion in 2024 and is projected to grow by USD 56.83 billion in 2025. Air traffic in the North American region is experiencing continuous development. For instance, IATA reported that while North American airlines' full-year passenger traffic declined by 65.6% in 2020 as compared to 2019, the region still maintained the largest share of global passenger traffic (RPK), accounting for approximately 32.6% of worldwide RPKs. Additionally, the US Bureau of Transportation Statistics indicated that U.S. airlines transported 674 million passengers in 2021, reflecting an 82.5% increase from 2020 (369 million passengers). Furthermore, the regional airlines offer a range of amenities and services to cater to a diverse passenger base. A robust infrastructure is critical for airports to ensure a seamless and efficient experience. Consequently, the regional airports are investing in infrastructure improvements to better meet the anticipated rise in need for airline services. As a result, government investments have also been observed in the region. These factors would further drive the regional airline ancillary services market share during the forecast period.

- For instance, in March 2022, the Government of Canada announced support packages aimed at upgrading the infrastructure at Toronto Pearson International Airport, which includes new funding for essential infrastructure projects. As part of this initiative, the airport is anticipated to receive over USD 99.06 million (CAD 142 million) from Transport Canada's Airport Critical Infrastructure Program.

As per the airline ancillary services market analysis and trends, the airline ancillary services market in Europe is currently experiencing robust development. Europe is one of the most renowned tourist destinations globally, contributing significantly to the growth of the global market. The expansion of major airlines, including Virgin Atlantic, British Airways, and Lufthansa, which are adding new destinations, is expected to further facilitate market development. For instance, in 2021, British Airways announced 13 new routes, 12 originating from London and one from Germany. These new routes will prompt airlines to improve their services, thereby stimulating market growth. Additionally, the expected growth of the Latin America market in the coming years is expected to be driven primarily by an increase in aircraft deliveries and passenger traffic. In 2021, Latin American airlines transported approximately 19.8 million air passengers in Brazil, accounting for nearly 50% of passengers in its other domestic markets. According to Airbus forecasts, the Latin American region will see the delivery of 2,550 new aircraft between 2022 and 2041. These new deliveries will enable commercial airlines operating in Latin America to significantly expand their fleet range, increasing the current number of 1,450 aircraft to 2,850 in the years ahead. Furthermore, The Middle East airline ancillary services industry has shown relatively stable trends in the airline sector over recent years and is expected to experience moderate growth during the forecast period. Despite constrained economic activity, the region has achieved a higher air traffic capacity, leading to increased revenue passenger kilometers. Moreover, favorable travel developments in Saudi Arabia and Oman offer prospects for ancillary service providers.

Top Key Players and Market Share Insights:

The global airline ancillary services market is highly competitive with major players providing casino management solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the airline ancillary services industry includes-

- Deutsche Lufthansa AG (Germany)

- Delta Airlines (U.S.)

- Emirates (UAE)

- Air France (France)

- Dnata (UAE)

- American Airlines (U.S.)

- Alaska Air (U.S.)

- United Airlines (U.S.)

- Southwest Airlines (U.S.)

- Ryanair (Ireland)

Recent Industry Developments :

Partnership:

- In June 2022, Emirates flight catering announced the partnership with Coca-Cola Arena, to provide premium food offerings for every demographic and occasion. With this partnership, Emirates flight catering will provide a comprehensive suite of hospitality and catering services, including logistics, menu development, food production, and service staff for all conferences and events.

Airline Ancillary Services Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 365.62 Billion |

| CAGR (2025-2032) | 12.1% |

| By Service Type |

|

| By Service Carrier Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Airline Ancillary Services market? +

Airline Ancillary Services Market Size is estimated to reach over USD 365.62 Billion by 2032 from a value of USD 130.00 Billion in 2024 and is projected to grow by USD 146.83 Billion in 2025, growing at a CAGR of 12.1%from 2025 to 2032.

Which is the fastest-growing region in the Airline Ancillary Services market? +

Asia-Pacific is the region experiencing the most rapid growth in the market as the regional industry is undergoing a rapid evolution spurred by shifting consumer preferences, technological advancements, and strategic emphasis on revenue diversification.

What specific segmentation details are covered in the Airline Ancillary Services report? +

The airline ancillary services report includes specific segmentation details for service type, service carrier type, and region.

Who are the major players in the Airline Ancillary Services market? +

The key participants in the market are Deutsche Lufthansa AG (Germany), Delta Airlines (U.S.), American Airlines (U.S.), Alaska Air (U.S.), United Airlines (U.S.), Southwest Airlines (U.S.), Ryanair (Ireland), Emirates (UAE), Air France (France), Dnata (UAE), and others.