- Summary

- Table Of Content

- Methodology

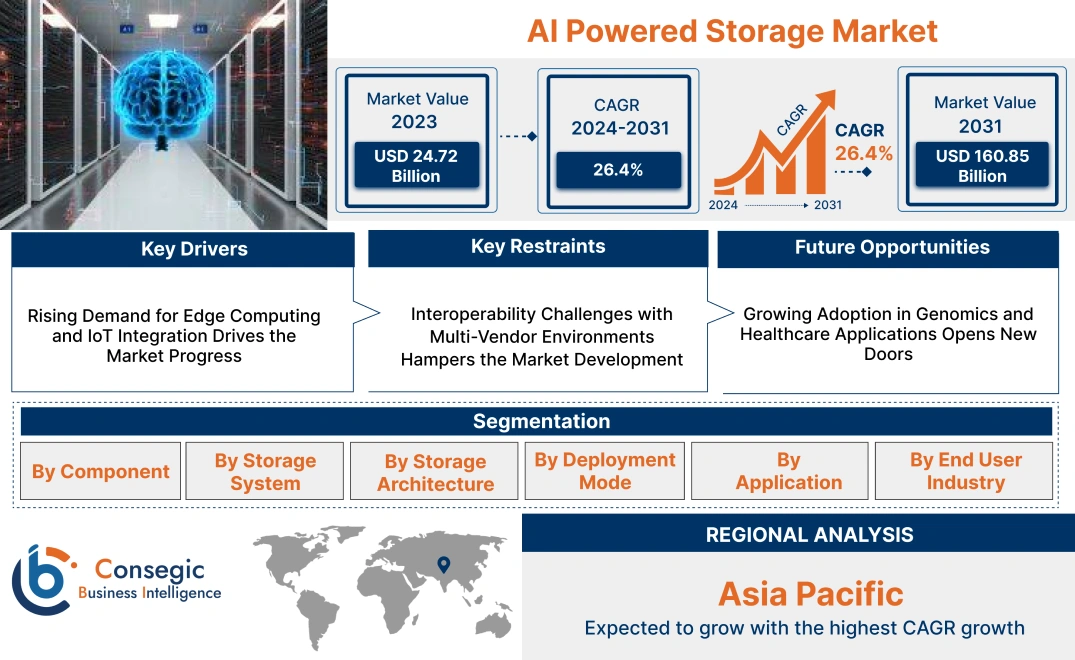

AI Powered Storage Market Size:

AI Powered Storage Market size is estimated to reach over USD 160.85 Billion by 2031 from a value of USD 24.72 Billion in 2023 and is projected to grow by USD 30.80 Billion in 2024, growing at a CAGR of 26.4% from 2024 to 2031.

AI Powered Storage Market Scope & Overview:

AI-powered storage refers to specialized infrastructure designed to support machine learning (ML) and artificial intelligence (AI) workloads by managing and processing vast data volumes with speed and efficiency. These storage systems are equipped with high-performance, scalable options to handle the massive datasets generated by AI applications, ensuring quick data access and seamless processing. They incorporate advanced features like data reduction through deduplication and compression, as well as tiering, to enhance efficiency and minimize costs.

These systems also prioritize robust data security, employing access control measures and encryption to protect sensitive information. Integration with AI frameworks further simplifies data management, providing streamlined access and processing capabilities. This enables organizations to accelerate the development and deployment of AI and ML applications, ensuring optimal performance across diverse use cases.

End-users of AI-powered storage include enterprises in industries such as technology, healthcare, finance, and research, where managing and analyzing large datasets is critical for innovation and operational efficiency. These systems form a foundational element for advancing AI-driven solutions and optimizing data-intensive workloads.

AI Powered Storage MarketDynamics - (DRO) :

Key Drivers:

Rising Demand for Edge Computing and IoT Integration Drives the Market Progress

The rapid growth of edge computing and IoT ecosystems is driving the demand for advanced storage solutions that process and manage data closer to the source. With billions of IoT devices generating massive amounts of data, traditional centralized storage systems face latency and bandwidth limitations. AI-powered storage solutions address these challenges by enabling real-time data management, filtering, and analysis directly at the edge, minimizing the need for continuous data transmission to centralized servers.

This capability is particularly vital for applications like autonomous vehicles, where split-second decision-making is required, as well as smart cities and industrial automation, where seamless connectivity and real-time monitoring are essential. By reducing latency and optimizing bandwidth usage, these intelligent systems enhance operational efficiency and enable IoT-driven innovations. As edge computing adoption grows, AI-driven storage technologies are becoming critical enablers for efficient and scalable data management in decentralized architectures further driving AI powered storage market growth.

Key Restraints :

Interoperability Challenges with Multi-Vendor Environments Hampers the Market Development

Organizations frequently operate storage solutions sourced from multiple vendors, leading to significant interoperability issues when integrating AI-powered systems. Each vendor often employs proprietary protocols, architectures, and interfaces, making it difficult to achieve seamless communication and compatibility across platforms. AI-powered storage solutions must adapt to diverse hardware and software configurations, requiring extensive customization and integration efforts.

This lack of standardization not only increases deployment time but also elevates operational complexity and costs, especially in large-scale environments like data centers or hybrid cloud infrastructures. Furthermore, inconsistencies in data formats and communication protocols hinder the efficiency of real-time analytics and predictive maintenance, limiting the full potential of AI-driven technologies. These interoperability issues create barriers for organizations aiming to modernize their storage infrastructure while maintaining their existing multi-vendor setups, slowing down the AI powered storage market demand.

Future Opportunities :

Growing Adoption in Genomics and Healthcare Applications Opens New Doors

The healthcare sector is witnessing a surge in data-intensive applications such as genomics, medical imaging, and drug discovery, driving the need for efficient storage and retrieval solutions. Genomics research, for instance, generates massive datasets from DNA sequencing, requiring storage systems capable of handling petabytes of data while ensuring quick access for analysis. Similarly, medical imaging technologies like MRI and CT scans demand high-capacity storage solutions for real-time data retrieval and processing.

AI-powered storage systems address these constraints by offering faster data management, enabling healthcare providers to leverage advanced analytics for personalized medicine and improved patient outcomes. In drug discovery, AI-driven storage enhances the ability to process and analyze vast chemical and biological datasets, accelerating research timelines. As healthcare increasingly relies on data-driven decision-making, AI-optimized storage systems present a significant growth opportunity, aligning with the sector's push for innovation and efficiency. Thus, the aforementioned factors drive the AI powered storage market opportunities.

AI Powered Storage Market Segmental Analysis :

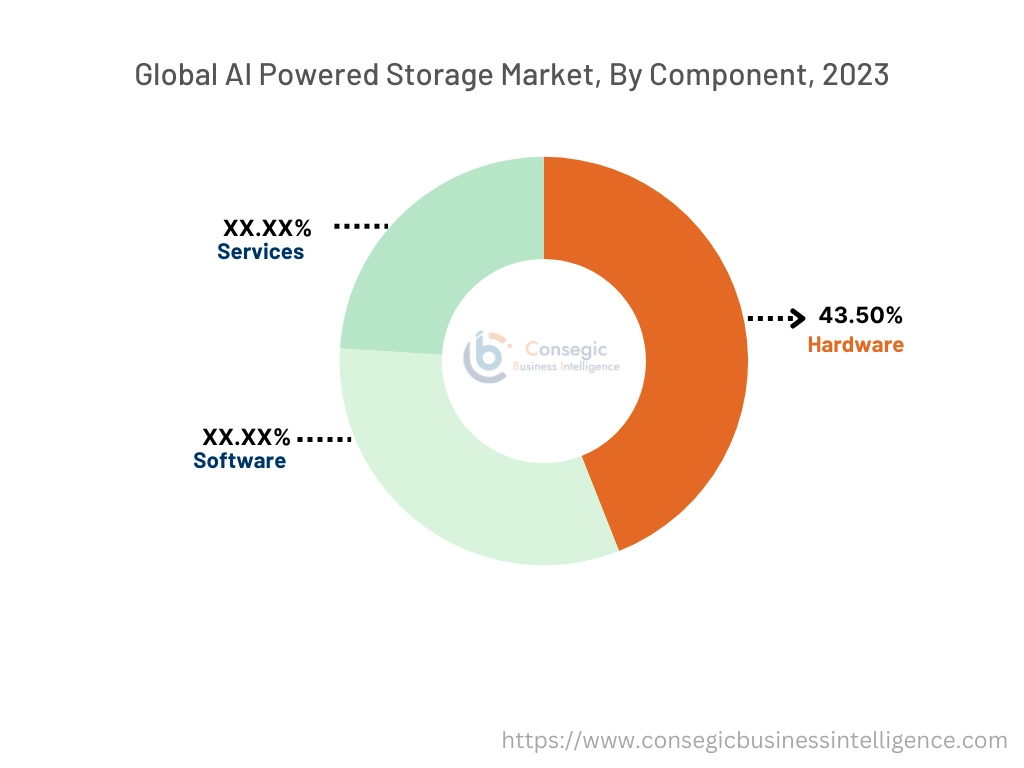

By Component:

Based on the component, the market is segmented into Hardware (Storage Devices, AI Accelerators, Networking Equipment), Software (Storage Management, AI Algorithms), and Services (Consulting, Integration, Support & Maintenance).

The hardware segment held the largest revenue of 43.50% of the total AI powered storage market share in 2023.

- AI-powered storage hardware includes storage devices optimized for speed and AI accelerators that process large datasets efficiently.

- Networking equipment, such as high-speed switches and routers, ensures seamless data transfer and low-latency performance in AI storage infrastructures.

- Advanced storage devices, including NVMe SSDs and persistent memory, are widely adopted for their ability to handle high-speed analytics workloads.

- Innovations in hardware are enhancing storage density, reducing power consumption, and improving overall system efficiency, driving the segment's dominance.

- The prominence of hardware reflects its fundamental role in supporting real-time analytics and predictive decision-making in various industries, fueling the AI powered storage market expansion.

The software segment is expected to grow at the fastest CAGR during the forecast period.

- Software solutions, including storage management tools and AI algorithms, enable intelligent data handling and dynamic workload optimization.

- AI algorithms enhance predictive analytics and real-time processing, allowing enterprises to derive actionable insights from their data.

- Storage management software automates data lifecycle management, including tiering, compression, and deduplication, to maximize efficiency.

- The integration of AI-driven software in cloud environments supports flexible and scalable storage solutions.

- The AI powered storage market trends in automation and digital transformation are driving the adoption of software solutions across industries.

By Storage System:

Based on the storage system, the market is segmented into Direct Attached Storage (DAS), Network Attached Storage (NAS), and Storage Area Network (SAN).

The Storage Area Network segment accounted for the largest revenue of the total AI powered storage market share in 2023.

- SAN systems provide high-speed, low-latency access to data, making them suitable for enterprise-grade applications like big data analytics and disaster recovery.

- They offer scalability and flexibility, allowing businesses to expand storage capacity without disrupting existing operations.

- SAN solutions are particularly favored by industries such as BFSI and healthcare for their robust performance and enhanced data security.

- As per AI powered storage market analysis, the adoption of SAN reflects its capability to handle critical workloads and complex data environments effectively.

The Network attached storage segment is expected to grow at the fastest CAGR during the forecast period.

- NAS systems are widely adopted for file-based storage, offering simplicity and cost-effectiveness for small to medium enterprises.

- The integration of AI-powered features in NAS, such as automated data classification and real-time analytics, is driving adoption.

- NAS solutions are increasingly preferred for collaborative applications, including media production and document management.

- The segment's proliferation is supported by its ability to meet the needs of distributed work environments efficiently, which further encourages the AI powered storage market growth.

By Storage Architecture:

Based on storage architecture, the market is segmented into File Based, Block Storage, and Object Based.

The object-based storage segment held the largest revenue share in 2023.

- Object storage systems are ideal for managing unstructured data, making them suitable for applications like big data analytics and real-time streaming.

- These systems enable scalability and support hybrid cloud environments, ensuring seamless integration with enterprise workflows.

- The adoption of object storage is driven by its ability to handle large datasets with high efficiency and flexibility.

- Industries such as media entertainment and healthcare rely on object storage for high-performance data management, contributing to the AI powered storage market demand.

The file-based storage segment is expected to grow at the fastest CAGR during the forecast period.

- File storage systems are widely used in environments where structured and semi-structured data require efficient organization.

- These systems are gaining traction in industries such as manufacturing and retail, where shared file access is critical for operations.

- File storage solutions are increasingly integrated with cloud platforms, enabling hybrid deployments that enhance flexibility and scalability.

- The growth of this segment reflects its ability to meet the diverse demands of modern enterprises effectively boosting the AI powered storage market expansion.

By Deployment Mode:

Based on deployment mode, the market is segmented into On-Premise, Cloud-Based, and Hybrid.

The cloud-based segment held the largest revenue share in 2023.

- Cloud-based storage offers scalability, cost efficiency, and easy accessibility, making it suitable for dynamic workloads and growing datasets.

- These solutions are widely adopted in industries such as IT & telecom and media, where real-time analytics and large-scale data storage are critical.

- Cloud storage providers are integrating AI capabilities to optimize performance and reduce operational complexity for businesses.

- As per AI powered storage market analysis, the dominance of this segment highlights its role in enabling seamless operations and supporting digital transformation initiatives.

The hybrid segment is expected to grow at the fastest CAGR during the forecast period.

- Hybrid solutions combine the scalability of cloud storage with the control and security of on-premise systems, offering a balanced approach.

- These solutions are particularly favored in industries like BFSI and healthcare, where compliance and data sovereignty are top priorities.

- Hybrid storage systems enable organizations to manage workloads dynamically, optimizing performance and cost efficiency.

- The rapid expansion of this segment is supported by advancements in enterprise modernization and increasing cloud adoption, creating significant AI powered storage market opportunities.

By Application:

Based on application, the market is segmented into Data Analytics, Real-Time Streaming, Backup & Recovery, Predictive Maintenance, and Others.

The data analytics segment accounted for the largest revenue share in 2023.

- AI-powered storage enhances analytics by providing high-speed data access and intelligent data classification.

- These solutions are extensively adopted in industries like BFSI and automotive for deriving actionable insights from large datasets.

- Advanced analytics applications, such as fraud detection and customer behavior analysis, rely on AI-driven storage systems.

- As per AI powered storage market trends, the importance of data analytics in decision-making processes underscores the segment's dominance.

The real-time streaming segment is expected to grow at the fastest CAGR during the forecast period.

- Real-time streaming applications, such as video analytics and live monitoring, require low-latency storage solutions for optimal performance.

- AI-powered storage enables seamless streaming by prioritizing and processing data efficiently.

- The rapid adoption of streaming technologies in media and entertainment supports the enlargement of this segment.

- As per the market analysis, the segment's growth reflects its critical role in enabling real-time insights and enhancing user experiences.

By End-User Industry:

Based on the end-user industry, the market is segmented into IT & Telecom, BFSI, Healthcare, Automotive, Media & Entertainment, and Others.

The IT & telecom segment held the largest revenue share in 2023.

- AI-powered storage is critical for managing the large-scale data generated by 5G networks, IoT devices, and cloud-based services in the IT & telecom sector.

- These systems enable faster data retrieval and support high-performance computing applications, such as AI-driven customer support and fraud detection.

- The segment benefits from the growing trend of digital transformation across telecom providers, requiring robust storage infrastructure for seamless operations.

- AI-powered storage enhances data security and compliance, ensuring the protection of sensitive customer and business data.

- The analysis of segmental trends shows that the dominance of this segment is supported by the increasing reliance on real-time data processing and analytics to optimize network performance and customer experiences.

The automotive segment is expected to grow at the fastest CAGR during the forecast period.

- AI-powered storage solutions are integral to autonomous driving systems, enabling real-time data processing from sensors, cameras, and LiDAR systems.

- These systems are increasingly adopted for vehicle-to-everything (V2X) communication, ensuring seamless interaction between vehicles, infrastructure, and other devices.

- Automotive manufacturers rely on AI-driven storage for predictive maintenance, enhancing vehicle efficiency and reducing operational downtime.

- The segment is fueled by advancements in connected vehicle technology, including in-car entertainment systems and driver assistance features, which require robust storage solutions.

- Therefore, as per market trends the rapid growth of this segment is supported by innovations in electric and autonomous vehicles, driving the need for high-capacity, AI-optimized storage systems.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

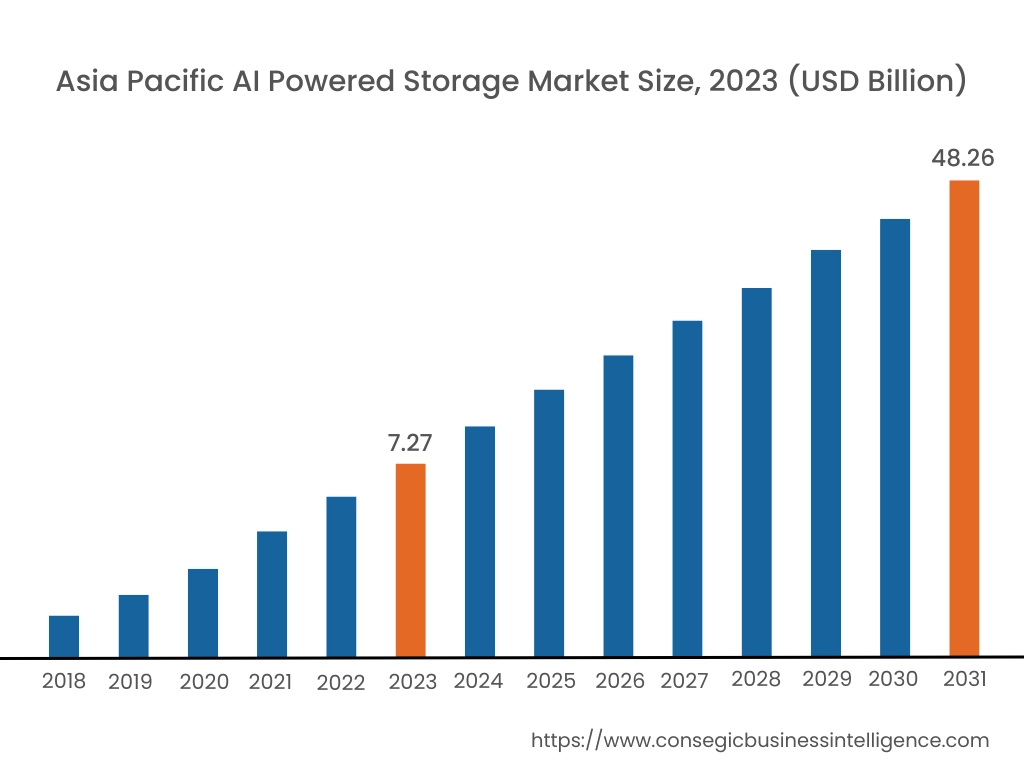

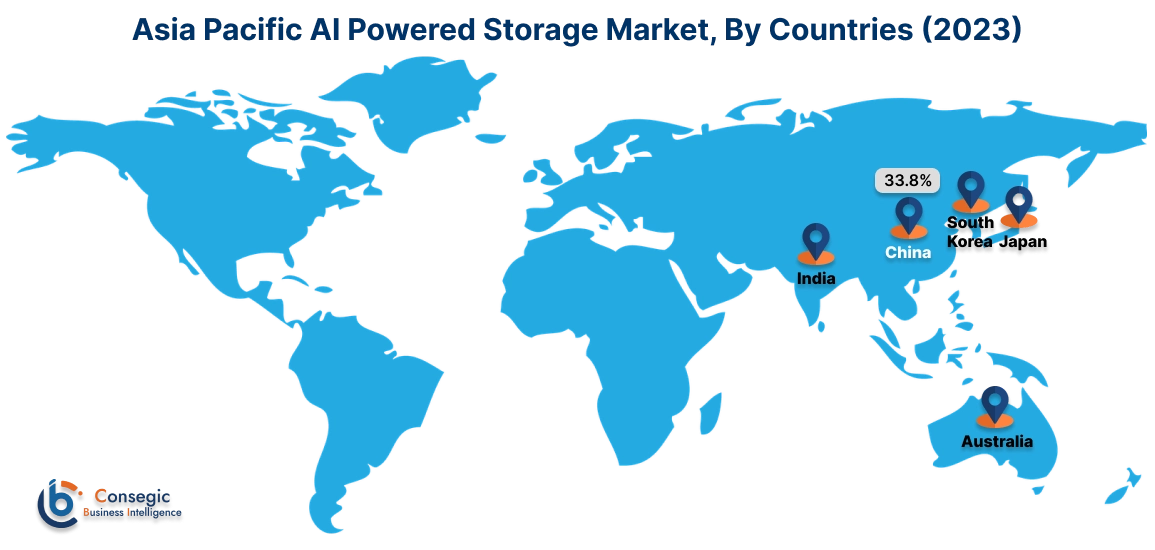

Asia Pacific region was valued at USD 7.27 Billion in 2023. Moreover, it is projected to grow by USD 9.07 Billion in 2024 and reach over USD 48.26 Billion by 2031. Out of these, China accounted for the largest share of 33.8% in 2023. The Asia-Pacific region is emerging as the fastest-growing market for AI-powered storage, with China, Japan, and India at the forefront. This rapid development is fueled by the increasing adoption of IoT devices, and smartphones, and the rise in the adoption of cloud computing services. Government initiatives promoting digital transformation and smart city projects are further influencing market trends. Industries in this region are leveraging AI-powered storage systems to manage the exponential rise in data volumes.

North America is estimated to reach over USD 52.92 Billion by 2031 from a value of USD 8.22 Billion in 2023 and is projected to grow by USD 10.23 Billion in 2024. North America dominates the AI-powered storage market, with a substantial share. The United States leads in adoption due to the rapid integration of AI with storage solutions across various industries, including healthcare, IT, and finance. Enterprises in this region are increasingly investing in advanced technologies to safeguard critical data and enhance operational efficiency. Additionally, the trend of adopting AI-powered systems for predictive analytics and security management is gaining traction.

Europe holds a significant position in the global AI-powered storage market, driven by stringent data privacy regulations such as GDPR and a strong focus on secure data management. Countries like Germany, the United Kingdom, and France are leading in the adoption of advanced storage systems integrated with AI capabilities to improve data processing and compliance. Recent analysis highlights a growing trend of deploying AI-driven storage in sectors such as banking and manufacturing to streamline operations.

The Middle East & Africa region demonstrates steady growth in the adoption of AI-powered storage systems, particularly in sectors like oil & gas, telecommunications, and healthcare. The UAE and Saudi Arabia are leading the market by investing in innovative storage technologies to support digital transformation goals aligned with national agendas like Vision 2030. The growing reliance on AI-driven data management to enhance operational efficiency is shaping market trends in this region.

Latin America represents an emerging market for AI-powered storage, with Brazil and Mexico contributing significantly to the region’s development. The increasing adoption of cloud services, coupled with a growing IT sector, is fostering the deployment of advanced storage systems. Government initiatives to modernize digital infrastructure and support industrial digitization are positively influencing market trends.

Top Key Players & Market Share Insights:

The AI Powered Storage market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global AI Powered Storage market. Key players in the AI Powered Storage industry include –

- Dell Technologies Inc. (USA)

- Hewlett Packard Enterprise (HPE) (USA)

- Cisco Systems, Inc. (USA)

- Tintri, Inc. (USA)

- VAST Data (USA)

- IBM Corporation (USA)

- Pure Storage (USA)

- Western Digital Corporation (USA)

- Seagate Technology Holdings PLC (Ireland)

- NetApp, Inc. (USA)

Recent Industry Developments :

Product Enhancements:

- In October 2024, Dell Technologies introduced innovations to its PowerMax storage platform, enhancing efficiency, cybersecurity, and multi-cloud agility. Powered by advanced AI, the platform now offers intelligent automation for better performance, faster response times, and operational cost reductions. Enhanced cybersecurity features include secure snapshots and ransomware detection, ensuring robust data protection. PowerMax also supports seamless multi-cloud connectivity, enabling businesses to manage data effortlessly across hybrid environments.

Acquisitions & Mergers:

- In January 2024, Wasabi Technologies acquired Curio AI from GrayMeta, including its intellectual property and team, to enhance its cloud storage solutions with AI capabilities. This acquisition aims to integrate AI-powered intelligent storage for the media and entertainment sector, enabling detailed metadata generation for video content.

Partnerships & Collaborations:

- In October 2024, TELUS partnered with Google Cloud and Onix to modernize its data storage infrastructure and accelerate AI-driven innovation. The collaboration focuses on leveraging Google Cloud's services to enhance operational efficiency and drive data insights. Onix, a key Google Cloud partner, will support the transition. The initiative aims to optimize TELUS' customer service, improve decision-making, and foster innovation by deploying AI-powered tools.

AI Powered Storage Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 160.85 Billion |

| CAGR (2024-2031) | 26.4% |

| By Component |

|

| By Storage System |

|

| By Storage Architecture |

|

| By Deployment Mode |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the AI Powered Storage Market? +

AI Powered Storage Market size is estimated to reach over USD 160.85 Billion by 2031 from a value of USD 24.72 Billion in 2023 and is projected to grow by USD 30.80 Billion in 2024, growing at a CAGR of 26.4% from 2024 to 2031.

What are the key segments in the AI Powered Storage Market report? +

The AI Powered Storage Market report includes segmentation by component (Hardware, Software, Services), storage system (Direct Attached Storage, Network Attached Storage, Storage Area Network), storage architecture (File Based, Block Storage, Object Based), deployment mode (On-Premise, Cloud-Based, Hybrid), Application (Data Analytics, Real-Time Streaming, Backup & Recovery, Predictive Maintenance, Others), and end-user industry (IT & Telecom, BFSI, Healthcare, Automotive, Media & Entertainment, Others).

Which segment is expected to grow the fastest in the AI Powered Storage Market? +

The Software segment is expected to grow at the fastest CAGR during the forecast period. Software solutions, including storage management tools and AI algorithms, enable intelligent data handling and real-time processing, driving the adoption of AI-driven storage across various industries.

Who are the major players in the AI Powered Storage Market? +

Key players in the AI Powered Storage Market include Dell Technologies Inc. (USA), Hewlett Packard Enterprise (HPE) (USA), IBM Corporation (USA), Pure Storage (USA), Western Digital Corporation (USA), Seagate Technology Holdings PLC (Ireland), NetApp, Inc. (USA), Cisco Systems, Inc. (USA), Tintri, Inc. (USA), and VAST Data (USA).