- Summary

- Table Of Content

- Methodology

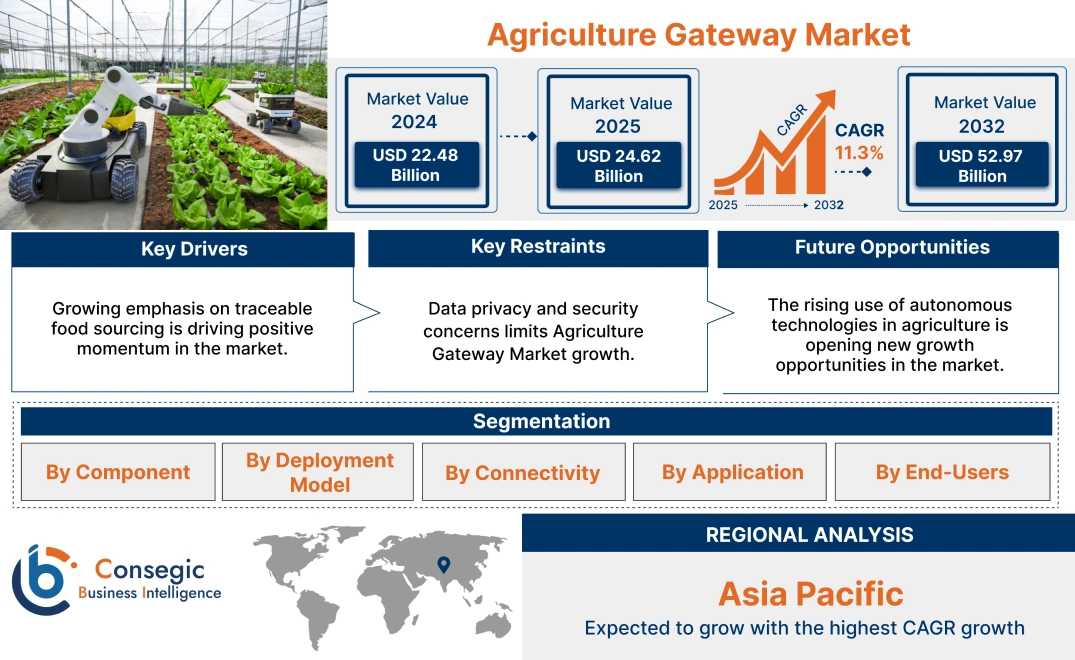

Agriculture Gateway Market Size:

Agriculture Gateway Market size is estimated to reach over USD 52.97 Billion by 2032 from a value of USD 22.48 Billion in 2024 and is projected to grow by USD 24.62 Billion in 2025, growing at a CAGR of 11.3% from 2025 to 2032.

Agriculture Gateway Market Scope & Overview:

An agriculture gateway is a hardware-based communication hub that connects agricultural sensors, edge devices, and control systems with cloud platforms or centralized servers. These gateways act as the primary interface between in-field data sources and remote data processing tools, enabling real-time monitoring, control, and analytics for precision farming systems.

Most gateways support communication through cellular networks, Wi-Fi, or long-range technologies like LoRa and Zigbee. They are designed to receive data from tools like soil moisture sensors, weather monitors, irrigation systems, and machinery trackers. Some models also include built-in processing features, so they can handle basic tasks locally without always needing internet access. These devices are often made with strong materials to perform well in tough outdoor environments.

These devices play a critical role in supporting the interoperability and scalability of digital farming ecosystems. End-users include companies that build smart farming solutions, equipment manufacturers, and large farms looking to connect multiple devices and manage data efficiently.

Agriculture Gateway Market Dynamics - (DRO) :

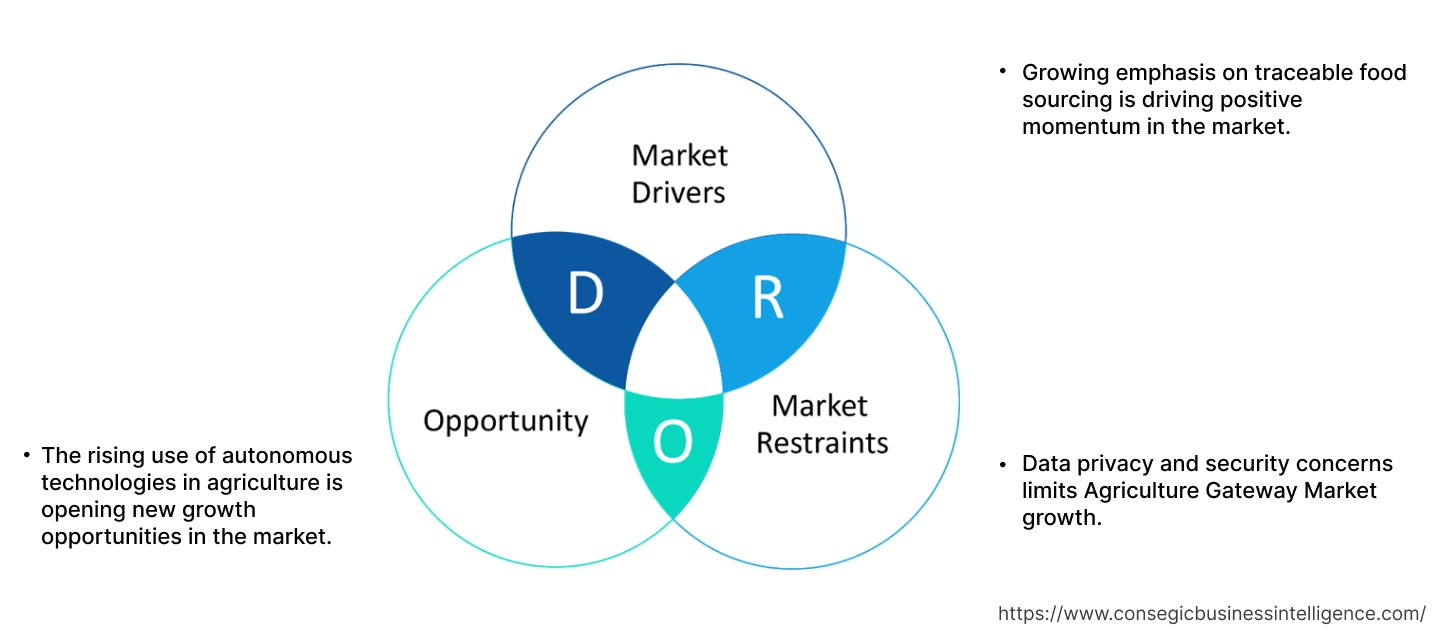

Key Drivers:

Growing emphasis on traceable food sourcing is driving positive momentum in the market.

Consumer awareness around food safety, sustainability, and quality is driving a strong requirement for transparency across the food supply chain. Shoppers increasingly seek clarity on the origin of their food, the methods used in its production, and its journey to their table. Agriculture gateways are instrumental in enabling this level of visibility by integrating data across all stages of food production from planting and harvesting to processing and distribution. These systems provide real-time data transmission that empowers consumers to trace their food's entire lifecycle, fostering trust and enhancing confidence. For producers, this transparency supports compliance with food safety standards, quality assurance protocols, and sustainability regulations. With growing environmental and health-related concerns, the importance of traceability continues to rise, positioning these gateways as essential tools for both farmers and businesses, significantly propelling market progress.

Key Restraints:

Data privacy and security concerns limits Agriculture Gateway Market growth.

These Gateway systems gather large volumes of sensitive data, ranging from crop performance and soil conditions to financial records, making them vulnerable to cyber threats and unauthorized access. The growing risk of data breaches and misuse creates hesitation among farmers and agribusinesses, who may avoid implementing such technologies without guaranteed data protection. Ensuring robust cybersecurity protocols, such as encryption, secure data storage, and compliance with data protection regulations, is essential for gaining trust and encouraging broader adoption. A lack of robust cybersecurity measures undermines user confidence and could result in financial loss or reputational damage. As the market grows, addressing data privacy and security will be crucial for the long-term success and widespread adoption of agricultural technologies. Therefore, the concerns over data privacy and insufficient cybersecurity measures remain key restraining factors limiting the widespread adoption of agriculture gateway systems.

Future Opportunities :

The rising use of autonomous technologies in agriculture is opening new growth opportunities in the market.

The growing autonomous farming systems, including self-driving tractors, drones, and automated harvesters to enhance efficiency and reduce labor dependence, boost the demand for seamless, real-time data exchange. These gateways enable centralized connectivity and ensure continuous data transmission between machines and farm management systems, allowing for precise control, timely decision-making, and coordinated operations. This shift is creating an opportunity for such gateways that can act as the backbone for seamless communication between various smart farming components.

- For instance, in June 2024, Monarch Tractor and Verizon Business, announced a partnership where the autonomous tractors will be connected via Verizon’s network to support more sustainable agriculture practices.

Therefore, as farms move toward greater reliance on automation to boost efficiency, productivity, and labor independence, these gateways are poised to play a central role. This trend opens up strong growth potential for gateway providers, significantly driving the global agriculture gateway market opportunities.

Agriculture Gateway Market Segmental Analysis :

By Component:

Based on Component, the market is categorized into Hardware (Sensors, Actuators, Others), Software (Analytics, Control Systems, Data Management), and Services (Managed, Professional).

The Hardware segment holds the largest revenue of the overall Agriculture Gateway Market share in the year 2024.

- Hardware forms the core of gateway infrastructure, including embedded control units, edge processors, transceivers, and communication modules.

- Sensors integrated into gateway platforms collect soil, weather, and livestock data, while actuators trigger irrigation, feeding, and ventilation actions.

- As IoT adoption accelerates in agriculture, need for low-power, long-range hardware solutions such as LoRa, Zigbee, and NB-IoT continues to rise.

- According to the agriculture gateway market analysis, its physical necessity in all gateway installations, fueling the agriculture gateway market expansion.

The Software segment is expected to grow at the fastest CAGR during the forecast period.

- Software enables data interpretation, device coordination, and decision-making within agricultural gateway networks.

- Analytics engines embedded in gateway software platforms enable predictive modeling, resource optimization, and anomaly detection.

- Data management tools provide real-time dashboards, mobile alerts, and long-term trend analysis, supporting smarter decision-making.

- As per the market analysis, the AI and machine learning embedded into gateway software platforms fuel the global agriculture gateway market growth.

By Deployment Model:

Based on Deployment Model, the market is categorized into cloud-based and on-premises.

The Cloud-Based segment holds the largest revenue of the overall Agriculture Gateway Market share in the year 2024 and is expected to grow at the fastest CAGR during the forecast period.

- Cloud-based deployment offers scalability, remote access, and centralized data integration making it ideal for distributed farming operations.

- Gateways in cloud-based systems support real-time sensor communication, over-the-air updates, and multi-device synchronization without requiring local servers.

- Agribusinesses and large farms are increasingly using cloud platforms to collect, store, and analyze crop, weather, and livestock data from multiple fields or facilities.

- According to the agriculture gateway market analysis, the cost-effectiveness, ease of integration, and compatibility with mobile apps, cloud-based deployments are both the largest and fastest-growing segment, significantly fueling the market growth.

By Connectivity:

Based on Connectivity, the market is categorized into wireless and wired.

The Wireless segment holds the largest revenue share of the overall Agriculture Gateway Market in the year 2024 and is expected to grow at the fastest CAGR during the forecast period.

- Wireless connectivity dominates the market as most modern farms are adopting low-power wide-area networks (LPWAN), cellular IoT, or short-range protocols for real-time communication.

- Wireless gateways support flexible installation and system expansion, particularly important in large or remote agricultural sites where cabling is impractical or cost-prohibitive.

- Technologies such as ZigBee, LoRa, NB-IoT, and Wi-Fi are increasingly integrated into greenhouse control systems, weather-based irrigation, and field asset tracking.

- For instance, in January 2024, Morse Micro and Zetifi announced a strategic partnership at CES 2024, to develop a next-generation remote area connectivity solution tailored for smart IoT farming. The partnership aims to address the connectivity challenges in rural and remote agricultural regions by integrating Morse Micro’s Wi-Fi HaLow technology with Zetifi’s existing rural connectivity solutions.

- Thus, as the advancements in edge computing and remote sensor deployment in agriculture, wireless segment will significantly drive the agriculture gateway market demand.

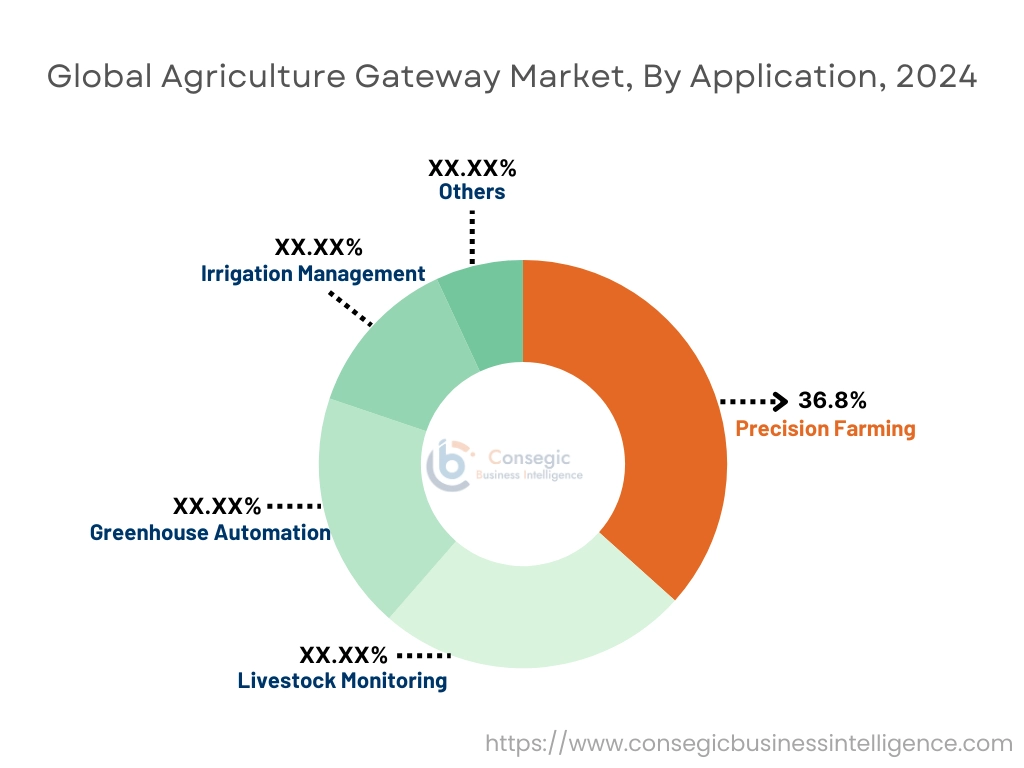

By Application:

Based on Application, the market is categorized into precision farming, livestock monitoring, greenhouse automation, irrigation management, and others.

The Precision Farming segment holds the largest revenue of the overall Agriculture Gateway Market share of 36.8% in the year 2024.

- Precision farming requires high-frequency data exchange from distributed sensors and devices monitoring crop health, nutrient levels, soil moisture, and weather.

- Gateways play a vital role in transmitting this data to analytics platforms and decision support systems in near real-time.

- LoRa and cellular gateways are widely adopted in field crop operations for controlling variable rate equipment and analyzing zone-based productivity.

- For instance, in January 2025, John Deere introduced JDLink Boost, an advanced connectivity solution designed to improve data exchange and remote management capabilities for farming equipment. This enhancement builds upon the existing JDLink system, offering faster, more reliable connectivity to support precision agriculture and smart farming operations.

- Thus, the high demand for precision farming and its growing role in digital agriculture, significantly drives the agriculture gateway market trends.

The Irrigation Management segment is expected to grow at the fastest CAGR during the forecast period.

- Irrigation systems increasingly rely on data from soil moisture sensors, flow meters, and evapotranspiration models to optimize water usage.

- Gateways support remote scheduling, leak detection, and pump automation by bridging sensor networks with centralized irrigation controllers or cloud platforms.

- Solar-powered gateways with built-in GSM or LoRa modules are enabling irrigation automation even in areas with limited infrastructure.

- The rising consumer demand for sustainable irrigation systems and rising irrigation-focused gateway applications is significantly fueling the global agriculture gateway market expansion.

By End-Users:

Based on End-Users, the market is categorized into small & medium farms, large farms, and agribusiness service providers.

The Large Farms segment holds the largest revenue share of the overall Agriculture Gateway Market in the year 2024.

- Large farms typically have multiple operational zones requiring advanced sensor networks, real-time equipment control, and cloud-based analytics, all supported by gateway infrastructure.

- These farms deploy fixed and mobile gateways across irrigation systems, harvesting machines, storage units, and transport vehicles.

- With better access to capital, skilled labor, and in-house IT support, large farms are early adopters of scalable, high-capacity connectivity solutions.

- Thus, the high application scale, complexity, and focus on automation significantly drives the agriculture gateway market trends.

The Small & Medium Farms segment is expected to grow at the fastest CAGR during the forecast period.

- Adoption is accelerating in this segment due to falling costs of IoT-enabled gateways, mobile-first platforms, and plug-and-play solutions tailored to decentralized operations.

- Agritech firms are targeting small-scaled farms with bundled services including gateways, sensors, and advisory apps through subscription or lease models.

- Growing digital literacy and demand for traceability in short food supply chains are encouraging investment in basic connectivity infrastructure of small and medium farms.

- The rising demand for these gateways in small and medium farms and their growing awareness is significantly fueling the global agriculture gateway market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

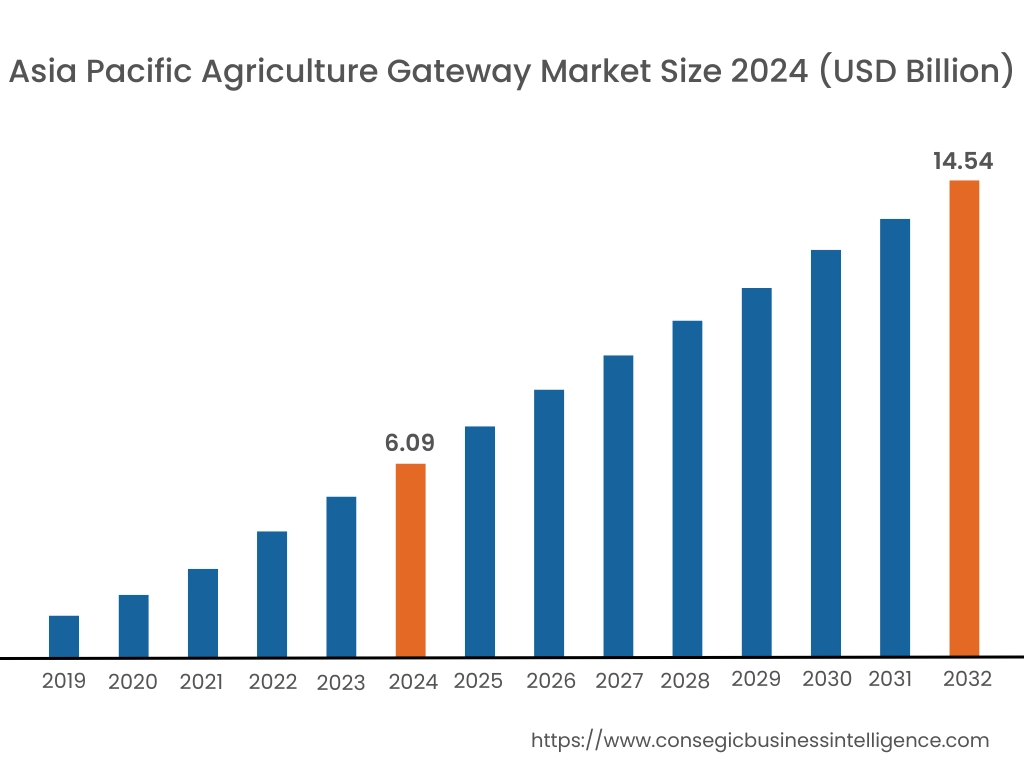

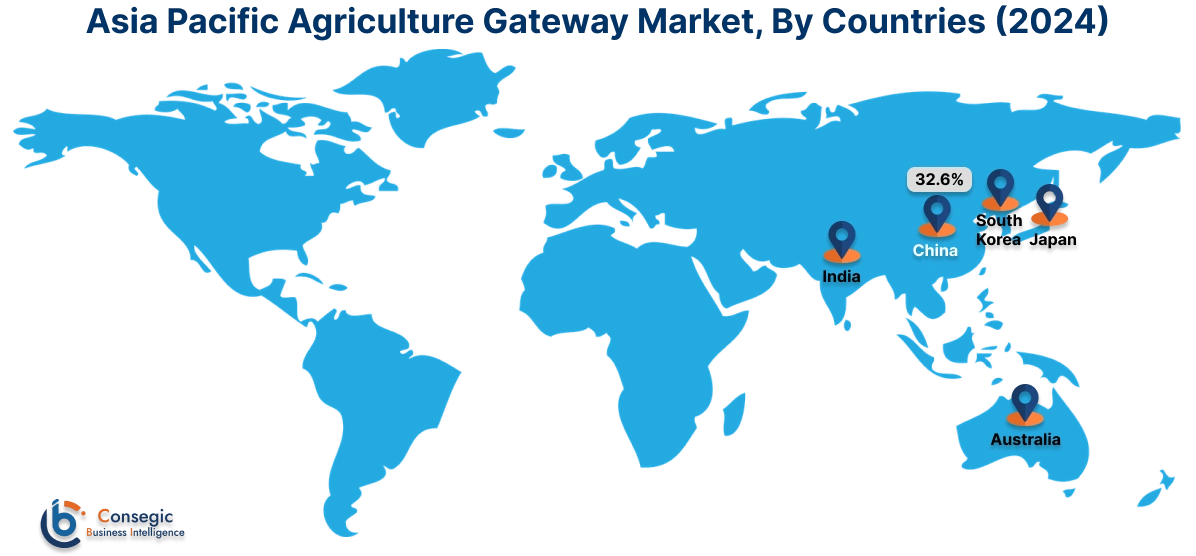

Asia Pacific region was valued at USD 6.09 Billion in 2024. Moreover, it is projected to grow by USD 6.67 Billion in 2025 and reach over USD 14.54 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.6%.

In the Asia-Pacific region, rapid modernization in agriculture is paving the way for the adoption of these gateway systems that seamlessly connect field sensors with centralized analytics. One trend is the development of locally optimized gateway units to handle varied crop and soil conditions, while another trend centers on the use of mobile-compatible platforms to provide remote operational control. In China, large-scale adoption is propelled by the availability of advanced sensor technology, while India leverages cost-effective, locally produced systems. Japan further contributes through precise, high-quality solutions tailored to intensive farming practices.

- For instance, in January 2025, the UP government partnered with Google Cloud to launch the Uttar Pradesh Open Network for Agriculture (UP-ONA), a pioneering AI-powered agri-gateway designed to support farmers with integrated digital solutions. This initiative positions UP-ONA as a transformative gateway model, integrating real-time data, multilingual support, and AI for a transparent, inclusive, and scalable digital farming ecosystem.

Furthermore, analysis of the market showed that proactive government initiatives and active investment in digital agriculture have significantly driven the agriculture gateway market demand.

North America is estimated to reach over USD 17.65 Billion by 2032 from a value of USD 7.47 Billion in 2024 and is projected to grow by USD 8.19 Billion in 2025.

In North America, the shift toward digital agriculture is driving the adoption of advanced gateway systems that connect field sensors and machinery. The integration of IoT capabilities with precision monitoring tools, while another trends centers on the implementation of secure, scalable data aggregation platforms that enable real‑time decision‑making propels market progress. In the United States, technology-focused research and active startup ecosystems are key drivers, whereas in Canada, strong governmental support for rural connectivity plays a critical role. Analysis of the market showed that favorable regulatory policies and robust investments in R&D are steering innovative product development significantly driving the agriculture gateway industry in this region.

Europe exhibits a strong presence in the market due to the increasing trend of digital connectivity to improve operational efficiency and resource management. The adoption of sensor‑integrated gateway systems that provide timely insights into field conditions and the development of interoperable platforms designed to connect various agritech devices boosts market development. In Germany and the United Kingdom, deep-rooted industrial expertise and forward-thinking policies drive the deployment of these systems, whereas in France and Italy, local agritech innovations support a gradual shift toward digital farming. Furthermore, stringent environmental and agricultural regulations promote the use of such technologies, significantly boosting the agriculture gateway market in this region.

Across the Middle East and Africa, traditional agricultural practices are evolving as modern agriculture gateway systems begin to integrate with local farm operations. Trends focusing on the customization of devices that can withstand the region’s challenging climates and ensuring connectivity in remote areas through robust, field‑ready systems are propelling industry development. In the United Arab Emirates, sophisticated systems are being deployed to support high-intensity, resource-efficient farming, whereas in South Africa, efforts are concentrated on bridging technological gaps and improving data connectivity in agriculture, fueling the market growth in this region.

In Latin America, the market is gradually transforming traditional farming methods by introducing digital connectivity solutions. In Brazil, a strong push toward modernization is evident as local innovators work to integrate these systems into extensive agricultural production, while in Argentina, traditional farming is increasingly supplemented by digital solutions that enhance precision and efficiency. Furthermore, the supportive policy frameworks and a rising cultural emphasis on sustainability drives agriculture gateway market growth in this region.

Top Key Players and Market Share Insights:

The Agriculture Gateway Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Agriculture Gateway Market. Key players in the Agriculture Gateway industry include -

- Advantech Co., Ltd. (Taiwan)

- Cisco Systems, Inc. (USA)

- Deere & Company (John Deere) (USA)

- Huawei Technologies Co., Ltd. (China)

- Kerlink (France)

- Libelium Comunicaciones Distribuidas S.L (Spain)

- Trimble Inc. (USA)

- AGCO Corporation (USA)

- Topcon Positioning Systems, Inc. (Japan)

- Ag Leader Technology (USA)

Recent Industry Developments :

Partnerships and Collaborations:

- In February 2025, Topcon Agriculture and Bonsai Robotics have partnered to enhance precision farming for permanent crops such as orchards and vineyards by integrating autonomous navigation with smart implement controls. The collaboration combines Bonsai Robotics’ computer vision and autonomy software with Topcon’s precision machinery systems to enable driverless operations and optimized implement performance.

Agriculture Gateway Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 52.97 Billion |

| CAGR (2025-2032) | 11.3% |

| By Component |

|

| By Deployment Model |

|

| By Connectivity |

|

| By Application |

|

| By End-Users |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Agriculture Gateway Market? +

Agriculture Gateway Market size is estimated to reach over USD 52.97 Billion by 2032 from a value of USD 22.48 Billion in 2024 and is projected to grow by USD 24.62 Billion in 2025, growing at a CAGR of 11.3% from 2025 to 2032.

What specific segments are covered in the Agriculture Gateway Market? +

The Agriculture Gateway Market specific segments for Component, Deployment Model, Connectivity, Application, End-Users and Region.

Which is the fastest-growing region in the Agriculture Gateway Market? +

Asia pacific is the fastest growing region in the Agriculture Gateway Market.

What are the major players in the Agriculture Gateway Market? +

The key players in the Agriculture Gateway Market are Advantech Co., Ltd. (Taiwan), Cisco Systems, Inc. (USA), Deere & Company (John Deere) (USA), Huawei Technologies Co., Ltd. (China), Kerlink (France), Libelium Comunicaciones Distribuidas S.L (Spain), Trimble Inc. (USA), AGCO Corporation (USA), Topcon Positioning Systems, Inc. (Japan), Ag Leader Technology (USA), and others.