- Summary

- Table Of Content

- Methodology

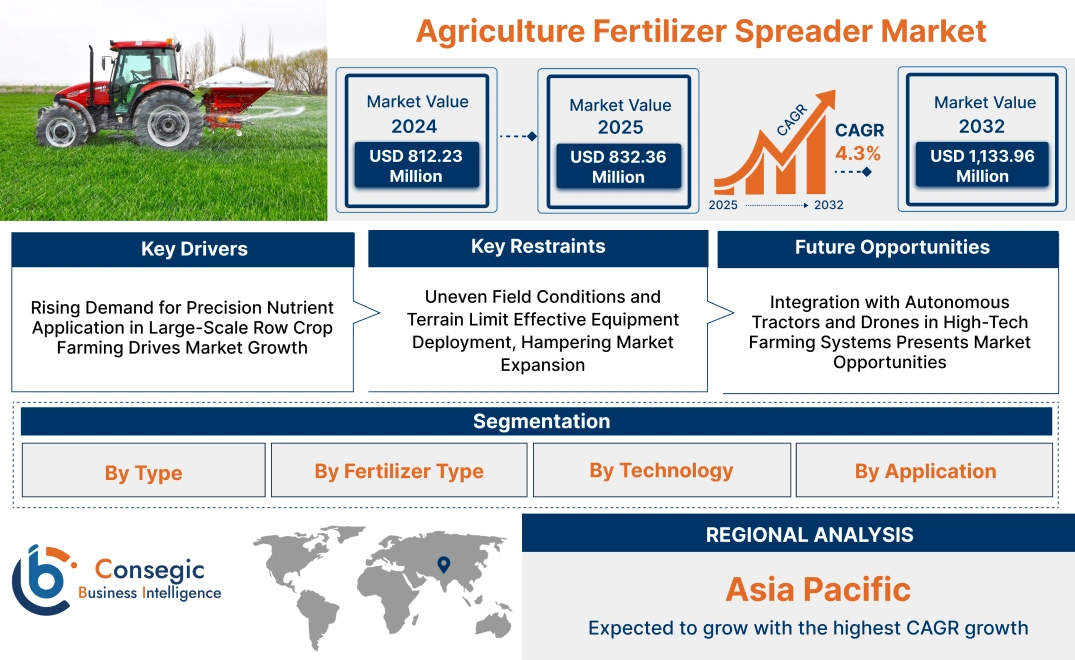

Agriculture Fertilizer Spreader Market Size:

Agriculture Fertilizer Spreader Market size is estimated to reach over USD 1,133.96 Million by 2032 from a value of USD 812.23 Million in 2024 and is projected to grow by USD 832.36 Million in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

Agriculture Fertilizer Spreader Market Scope & Overview:

Agriculture fertilizer spreader is a farm equipment used to spread fertilizers evenly over crop fields, providing balanced nutrient application and maximum soil enrichment. Mounted, trailed, and self-propelled models are available, meeting various farm sizes and operational requirements.

Core features are calibrated dispensing units, variable spread widths, corrosion-proof hoppers, and GPS-guided guidance controls. The machinery dispenses granular, powder, or liquid fertilizers with accuracy, reducing overlap and nutrient loss while maximizing crop yield potential.

Advantages are more precise application accuracy, time-effective operation, and lower manual intervention. Tractor compatibility and compatibility with other towage systems mean seamless integration within farm machinery environments. Site-specific application by fertilizer spreader support improves resource productivity and field production quality. Participation in large-scale farming and precision agriculture operations provides a key means to ensure reliable and controlled nutrition application.

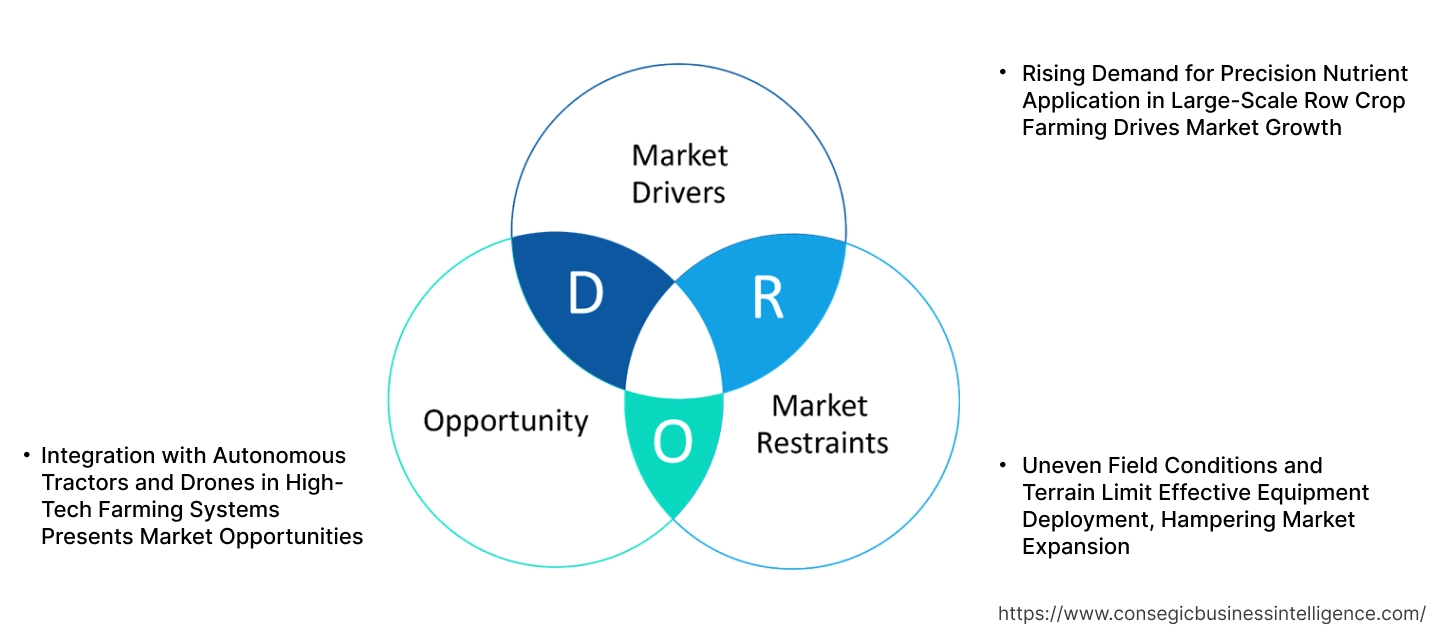

Agriculture Fertilizer Spreader Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Precision Nutrient Application in Large-Scale Row Crop Farming Drives Market Growth

The growing size of commercial row crop farming is propelling the use of fertilizer spreaders that can apply uniform and variable-rate nutrient application. Contemporary agriculture requires precision equipment that minimizes input loss, limits runoff, and optimizes fertilizer utilization with varying soil types and cropping zones. GPS, section control, and real-time sensor feedback enabled spreaders assist in applying the correct amount of nutrients, enhancing yield quality and resource use efficiency. These attributes are a must on big operations farming corn, soybean, wheat, and cotton. Precision farm operations are also being further boosted by increasing environmental compliance requirements and sustainability objectives.

- For instance, in August 2023, the government of Canada invested in the adoption of precision agriculture technology for a local Verner farm under the Adoption Stream of the Agricultural Clean Technology (ACT) Program. This funding enabled the François Delorme farm to purchase fertilizer spreader equipment with variable rate technology, which lowers the use of fertilizer and reduces greenhouse gas emissions.

While farmers will make efficiency, traceability, and return on input investment paramount, the need for sophisticated spreading technology is getting more acute, fueling the extended agriculture fertilizer spreader market expansion.

Key Restraints:

Uneven Field Conditions and Terrain Limit Effective Equipment Deployment, Hampering Market Expansion

In most agricultural areas, field irregularities such as sloping ground, constricted field pieces, and uneven surfaces compromise the effectiveness of mechanized fertilizer application. The conditions decrease the efficacy of calibration and enhance the risk of overlap, missed spots, or non-uniform application. The absence of land grading and field preparation still limits the applicability of high-capacity machines. In these instances, low-tech or manual fertilizer application is still the method of choice despite reduced efficiency. Limited mechanization support infrastructure and inexperienced operators also constrain precision spreader adoption. This is a pertinent challenge in Southeast Asia, East Africa, and hilly agricultural regions. Demand for enhanced productivity does exist, yet physical field limitations continue to constrain equipment performance, hampering the agriculture fertilizer spreader market growth.

Future Opportunities :

Integration with Autonomous Tractors and Drones in High-Tech Farming Systems Presents Market Opportunities

The development of smart agriculture has made new ways to combine fertilizer spreaders with autonomous tractors and aerial drones. These cutting-edge platforms can deliver ultra-accurate input within defined areas as per real-time agronomic data and multispectral imagery. Autonomous spreaders or drone-mounted dispensers can now change application rates based on vegetation indices, soil type, and terrain altitude. This convergence extends nutrient targeting for high-value crops and specialty field conditions. It also facilitates the complete automation of input operations in big and fragmented farms. As the push for labor-free, high-precision systems picks up speed, manufacturers emphasizing robot compatibility and sensor integration are creating strategic benefits.

- For instance, in November 2024, the Drone technology startup Marut Drones received $6.2 million in Series A funding from investment firm Lok Capital to continue running initiatives such as developing advanced agricultural drones, expanding channel partner network and establishing drone agriculture service hubs. This comes after their launch of AG365H, India’s first DGCA Type Certified medium category agricultural drone in October 2024.

These developments echo the larger movement toward automation and data-driven input management—driving agriculture fertilizer spreader market opportunities through both demand and expansion.

Agriculture Fertilizer Spreader Market Segmental Analysis :

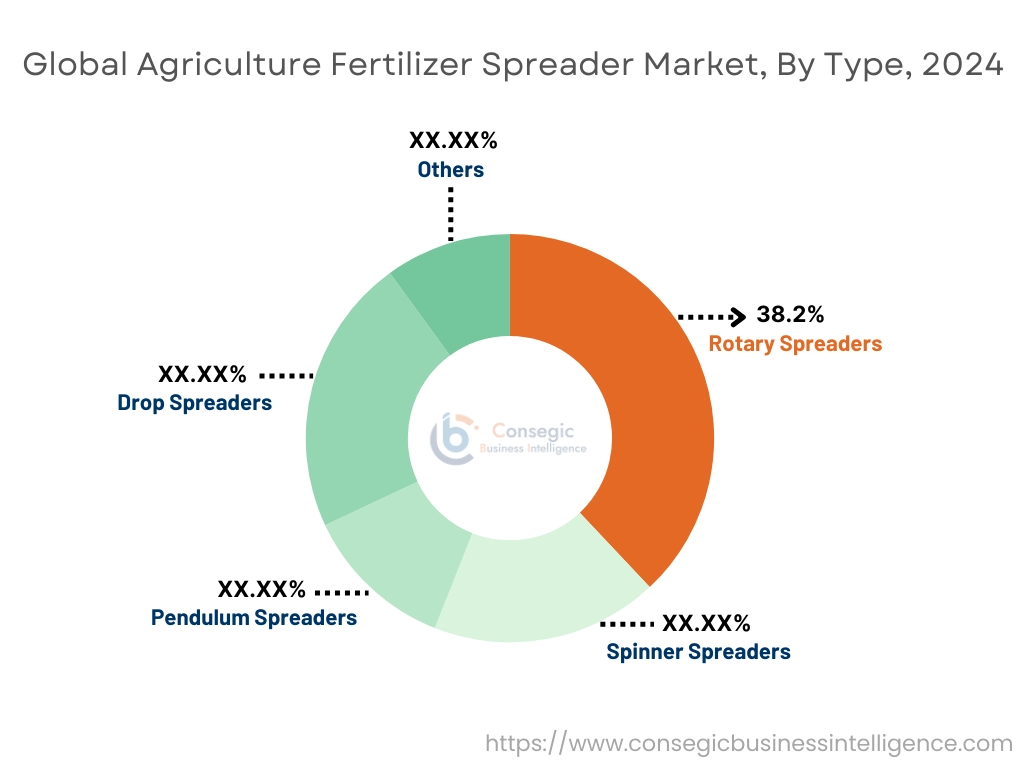

By Type:

Based on type, the market is segmented into drop spreaders, rotary spreaders, spinner spreaders, pendulum spreaders, and others.

The rotary spreaders segment accounted for the largest revenue share of 38.2% in 2024.

- Rotary spreaders are widely adopted due to their ability to uniformly distribute granular fertilizers across wide areas with minimal overlap.

- They are compatible with most dry fertilizers and are valued for their speed and efficiency on large commercial farms.

- Their simple mechanical design reduces maintenance requirements, enhancing usability for small to mid-sized farmers.

- For instance, in October 2024, ICL launched two new spreaders, the AccuPro 360ST and the AccuPro DROP, to expand their agricultural spreader range. The AccuPro 360ST, the latest professional rotary spreader, delivers superior performance and reliability with the integration of the SmartSpread™ system, which ensures uniform and precise application of granular fertilisers.

- As per the agriculture fertilizer spreader market analysis, increasing adoption in open-field row crop farming has contributed to the segment’s dominance.

The spinner spreaders segment is projected to witness the fastest CAGR during the forecast period.

- Spinner spreaders offer adjustable spreading patterns, making them ideal for variable field sizes and fertilizer application rates.

- Their integration with precision agriculture tools allows real-time adjustment of fertilizer flow for enhanced yield optimization.

- Advanced spinner models with twin-disc designs are gaining popularity in commercial agriculture settings.

- For instance, in August 2024, New Leader Manufacturing (NLM) launched a New Leader® nutrient applicator, the NL720 chassis-mounted spinner spreader. It allows fertilizer application at wider widths, higher rates, and faster speeds, maximizing its time in the field and ROI. It is versatile and ensures high productivity alongside a low-maintenance design.

- According to the agriculture fertilizer spreader market trends, growing focus on nutrient management and cost efficiency drives the adoption of high-performance spinner systems.

By Fertilizer Type:

Based on fertilizer type, the market is segmented into dry fertilizers, liquid fertilizers, compost & organic fertilizers, chemical fertilizers, and others.

The dry fertilizers segment accounted for the largest agriculture fertilizer spreader market share in 2024.

- Dry fertilizers are more stable, easier to handle, and suitable for bulk spreading operations across broadacre farms.

- These fertilizers can be precisely applied using mechanical or spinner spreaders, minimizing wastage.

- The affordability and long shelf life of dry formulations support their continued usage across various crop types.

- As per the agriculture fertilizer spreader market analysis, the extensive deployment of nitrogen-based dry fertilizers in row crops reinforces the segment’s leadership.

The compost & organic fertilizers segment is expected to grow at the fastest CAGR during the forecast period.

- Rising adoption of organic farming and regenerative agriculture practices is fueling the use of compost and bio-fertilizers.

- Specialized spreaders with adjustable flow systems are designed to handle the varied texture and density of organic materials.

- Government incentives for sustainable farming and consumer preference for organic produce support segment acceleration.

- According to the agriculture fertilizer spreader market trends, increased awareness of soil health and eco-friendly practices is driving the shift.

By Technology:

Based on technology, the market is segmented into manual, hydraulic, GPS-enabled, and variable rate technology (VRT).

The hydraulic segment held the largest revenue share in 2024.

- Hydraulic fertilizer spreaders are known for their operational reliability, scalability, and ease of integration with tractors and sprayers.

- They offer consistent fertilizer discharge and are suited for medium to large-scale operations across various terrains.

- These systems allow variable speed control, improving application precision and reducing input costs.

- For instance, in February 2024, Stara launched Twister 1500, a hydraulic spreader with twin disks for granulating fertilizer and fine seeds. The fixed rate model is controlled using a smartphone and allows for the variation of the rate manually.

- The segment’s dominance is supported by strong adoption across North America and Europe, where mechanization levels are high.

The variable rate technology (VRT) segment is projected to register the fastest CAGR during the forecast period.

- VRT enables site-specific fertilizer application based on soil fertility data, crop needs, and yield goals, significantly improving efficiency.

- These systems are used in precision farming to reduce environmental impact and maximize fertilizer utilization.

- Adoption is rising among progressive commercial farms that are equipped with advanced GPS and IoT infrastructure.

- Hence, the push toward data-driven and sustainable agriculture is responsible for the agriculture fertilizer spreader market expansion.

By Application:

Based on application, the market is segmented into farm fields, horticulture, commercial agriculture, and others.

The farm fields segment accounted for the largest agriculture fertilizer spreader market share in 2024.

- Fertilizer spreaders are integral to large-scale crop farming operations, particularly for cereals, pulses, and oilseeds.

- Precision application ensures optimal plant growth and soil nutrient balance across extensive field areas.

- Adoption of spinner and rotary spreaders with high-capacity hoppers supports efficient coverage of expansive plots.

- As per the agriculture fertilizer spreader market demand, crop rotation practices and increasing yield targets continue to drive this segment.

The commercial agriculture segment is projected to grow at the fastest CAGR during the forecast period.

- Commercial agribusinesses are investing in high-capacity, GPS-enabled spreaders to ensure consistent and traceable application performance.

- These enterprises emphasize data monitoring and automation to comply with regulatory requirements and maximize return on investment.

- Fertilizer spreaders used in commercial setups are often integrated with autonomous tractors and fleet management systems.

- Thus, professionalized farm operations and contract-based services are boosting commercial segment adoption and driving the agriculture fertilizer spreader market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

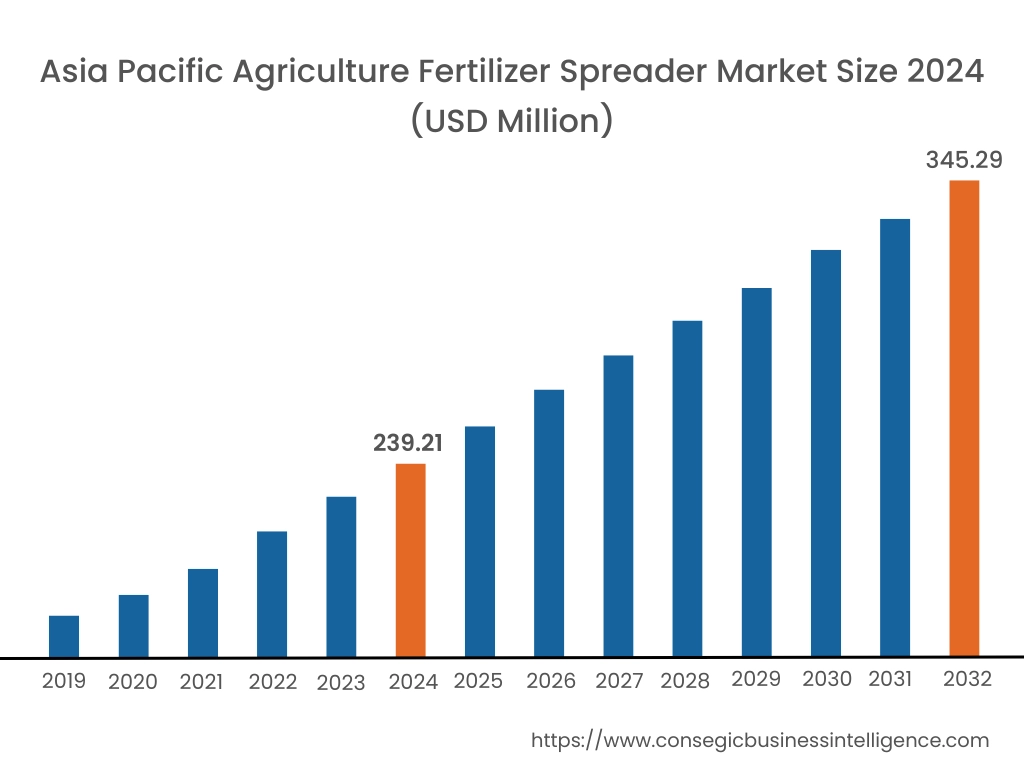

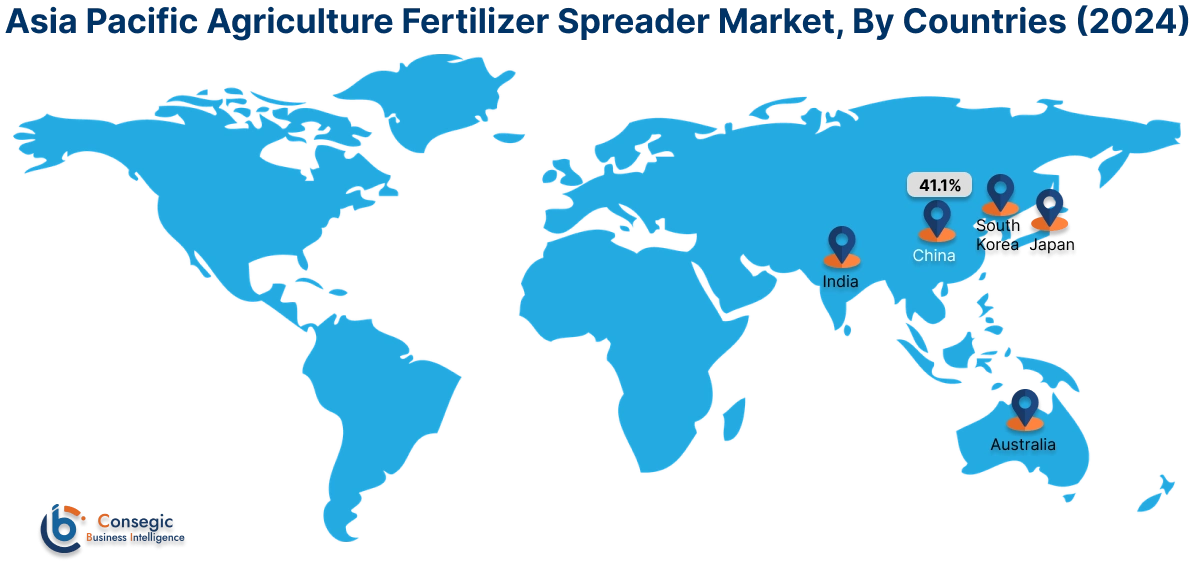

Asia Pacific region was valued at USD 239.21 Million in 2024. Moreover, it is projected to grow by USD 245.83 Million in 2025 and reach over USD 345.29 Million by 2032. Out of this, China accounted for the maximum revenue share of 41.1%. Asia-Pacific accounts for most global consumption, driven by intensive agricultural practices in China, India, Indonesia, and Vietnam. Analysis points to strong agriculture fertilizer spreader market demand in the region, boosted by the rising need for complex fertilizers, DAP, and urea for the cultivation of cereal crops and intense cropping. Government subsidies, land expansion, and food security programs are supporting growth. Yet overuse and nutrient imbalance concerns are compelling policymakers to encourage balanced fertilization practices and integrated soil fertility management. The development of local fertilizer production and distribution infrastructure further enhances access, while growing awareness of crop-specific nutrition is driving demand for tailored nutrient solutions.

North America is estimated to reach over USD 367.52 Million by 2032 from a value of USD 269.42 Million in 2024 and is projected to grow by USD 275.57 Million in 2025. North America holds a dominant position in the agriculture fertilizer spreader industry, with the United States and Canada demonstrating steady uptake of nitrogen-based and blended fertilizers to facilitate high-yielding crop production. Market analysis indicates a strong focus on precision agriculture and site-specific nutrient management, which is driving demand for value-added products like slow-release and stabilized products. Moreover, the move towards regenerative agriculture and sustainable soil health practices is driving integration of organic and bio-based inputs. Regulatory focus on nitrogen runoff and phosphate use is driving new fertilizer technologies to address environmental compliance and crop-specific performance optimization.

Europe represents a regulation-driven agriculture fertilizer spreader market, where environmental constraints, nutrient management directives, and decarbonization policies dictate fertilizer use patterns. Regions such as Germany, France, and the Netherlands are leading the implementation of eco-efficient fertilizer options. Market trends indicate a rising trend towards specialty fertilizers, blends of micronutrients, and foliar application that fit EU nutrient pollution levels. Adoption of digital farming platforms to track input use and maximize yields is underpinning precision delivery and less frequent applications. The European fertilizer market opportunity for agriculture is providing sustainable products that reconcile yield potential with environmental protection objectives.

Latin America is stepping up as a strong agriculture fertilizer spreader market propelled by the growing cultivation of soybeans, maize, and sugarcane in Brazil, Argentina, and Paraguay. According to market study, the sector shows immense priority towards increasing crop productivity and land fertility by potash and phosphoric fertilizer inputs. Regional expansion is based on technological improvement of mechanized agricultural practices and amicable trade flows for import fertilizer. There is growing adoption of high efficiency fertilizers and blended products adapted to local agronomic conditions. In addition, export crop sustainability certifications are promoting precision application and the use of environmentally friendly inputs.

The Middle East and Africa offer a combination of opportunities and challenges, with great growth potential in sub-Saharan areas and certain North African nations. Market research indicates increasing fertilizer use in Egypt, South Africa, Nigeria, and Kenya, with governments and NGOs supporting input availability and farmer training schemes. Dry soils and irregular rainfall patterns are driving the demand for water-soluble and controlled-release products. This region's agriculture fertilizer sector is also seeing a shift towards organic and locally sourced inputs on the back of increasing environmental pressures and scarce foreign exchange availability for importation.

Top Key Players and Market Share Insights:

The agriculture fertilizer spreader market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global agriculture fertilizer spreader market. Key players in the agriculture fertilizer spreader industry include -

- KUHN Group (France)

- RAUCH Landmaschinenfabrik GmbH (Germany)

- Teagle Machinery Ltd. (United Kingdom)

- Maschio Gaspardo S.p.A. (Italy)

- Agrex S.p.A. (Italy)

- Amazone H. Dreyer GmbH & Co. KG (Germany)

- Sulky-Burel (France)

- Kverneland Group (Norway)

- Bredal A/S (Denmark)

- Bogballe A/S (Denmark)

Recent Industry Developments :

Acquisitions:

- In April 2024, the agricultural machinery manufacturer AMAZONE acquired the Brazilian fertilizer spreader specialist MP AGRO. This collaboration enables the combination of both companies’ strengths to deliver better products and services to clients and introduce the technology to AMAZONE in Brazil. This decision also aims to raise the accuracy levels and sustainability in fertilizer application to new standards.

Agriculture Fertilizer Spreader Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,133.96 Million |

| CAGR (2025-2032) | 4.3% |

| By Type |

|

| By Fertilizer Type |

|

| By Technology |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Agriculture Fertilizer Spreader Market? +

Agriculture Fertilizer Spreader Market size is estimated to reach over USD 1,133.96 Million by 2032 from a value of USD 812.23 Million in 2024 and is projected to grow by USD 832.36 Million in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

What specific segmentation details are covered in the Agriculture Fertilizer Spreader Market report? +

The Agriculture Fertilizer Spreader market report includes specific segmentation details for type, fertilizer type, technology and application.

What are the applications in the Agriculture Fertilizer Spreader Market? +

The applications in the Agriculture Fertilizer Spreader Market are farm fields, horticulture, commercial agriculture and others.

Who are the major players in the Agriculture Fertilizer Spreader Market? +

The key participants in the Agriculture Fertilizer Spreader market are KUHN Group (France), RAUCH Landmaschinenfabrik GmbH (Germany), Amazone H. Dreyer GmbH & Co. KG (Germany), Sulky-Burel (France), Kverneland Group (Norway), Bredal A/S (Denmark), Bogballe A/S (Denmark), Teagle Machinery Ltd. (United Kingdom), Maschio Gaspardo S.p.A. (Italy) and Agrex S.p.A. (Italy).