- Summary

- Table Of Content

- Methodology

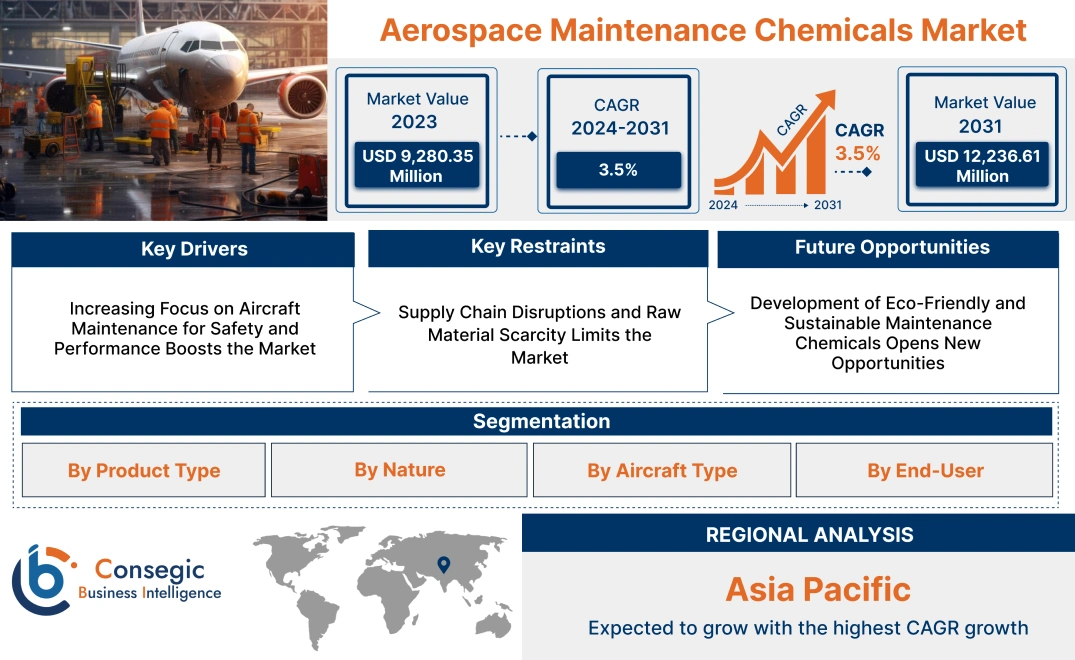

Aerospace Maintenance Chemicals Market Size:

Aerospace Maintenance Chemicals Market size is estimated to reach over USD 12,236.61 Million by 2031 from a value of USD 9,280.35 Million in 2023 and is projected to grow by USD 9,441.46 Million in 2024, growing at a CAGR of 3.5% from 2024 to 2031.

Aerospace Maintenance Chemicals Market Scope & Overview:

The aerospace maintenance chemicals are the chemicals designed to ensure the safety, efficiency, and longevity of aircraft through cleaning, maintenance, and repair processes. These chemicals include cleaning agents, degreasers, de-icing fluids, corrosion inhibitors, and specialty lubricants, essential for maintaining aircraft performance and adhering to stringent regulatory standards. Key characteristics of this market include high efficacy, compatibility with various aircraft materials, and compliance with safety and environmental regulations. The benefits include enhanced operational efficiency, extended aircraft life, reduced downtime, and improved safety during operations. Applications span aircraft cleaning, engine maintenance, corrosion prevention, and surface treatments. End-users include commercial airlines, defense organizations, and maintenance, repair, and overhaul (MRO) service providers, driven by the growing aviation industry, rising air passenger traffic, and the increasing focus on preventive maintenance and operational safety.

Aerospace Maintenance Chemicals Market Dynamics - (DRO) :

Key Drivers:

Increasing Focus on Aircraft Maintenance for Safety and Performance Boosts the Market

The aerospace sector prioritizes rigorous maintenance to ensure aircraft safety, reliability, and operational efficiency. Maintenance chemicals, including cleaners, lubricants, degreasers, and corrosion inhibitors, are essential for preserving performance and extending the lifespan of critical components. These chemicals help address issues such as wear, corrosion, and contamination, which can compromise aircraft functionality if left unchecked.

Trends in global air traffic expansion and stricter aviation safety regulations are driving the adoption of advanced maintenance protocols. The increasing frequency of maintenance, repair, and overhaul (MRO) activities, particularly in commercial aviation, underscores the importance of high-performance maintenance chemicals. The analysis highlights that as airlines focus on enhancing safety standards and minimizing operational downtime, the use of specialized maintenance chemicals will continue to play a central role in meeting industry requirements.

Key Restraints :

Supply Chain Disruptions and Raw Material Scarcity Limits the Market

The production of aerospace maintenance chemicals relies on a stable supply of high-quality raw materials, including solvents, surfactants, and specialty additives. However, supply chain disruptions caused by geopolitical tensions, natural disasters, or global pandemics have led to raw material shortages and price volatility. These challenges not only increase production costs but also impact the timely availability of maintenance chemicals, creating bottlenecks in the market.

Furthermore, the reliance on specific raw materials sourced from limited suppliers exacerbates these issues, particularly during periods of high market uncertainty. For MRO operators and manufacturers, ensuring a consistent supply of maintenance chemicals requires proactive supply chain management and diversification strategies. Trends in reshoring and localized production are emerging as potential solutions to mitigate the risks associated with raw material scarcity.

Future Opportunities :

Development of Eco-Friendly and Sustainable Maintenance Chemicals Opens New Opportunities

The aerospace sector's growing commitment to sustainability is driving innovation in eco-friendly maintenance chemicals. Manufacturers are increasingly developing formulations that minimize environmental impact, such as biodegradable cleaners, non-toxic corrosion inhibitors, and low-VOC degreasers. These chemicals meet regulatory requirements while aligning with trends in green aviation, which prioritize reducing carbon footprints and adopting sustainable practices.

Advancements in chemical engineering have enabled the production of high-performance eco-friendly alternatives that match or exceed the efficacy of traditional chemicals. For example, water-based formulations and plant-derived ingredients are being incorporated into cleaning and protective solutions, offering safer and more environmentally responsible options. As sustainability becomes a key focus in the aerospace sector, the adoption of eco-friendly maintenance chemicals is poised to gain momentum, creating aerospace maintenance chemicals market opportunities for manufacturers to lead the market in innovation and environmental stewardship.

Aerospace Maintenance Chemicals Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into cleaners, degreasers, paint removers, specialty solvents, lubricants, and others.

The cleaners segment accounted for the largest revenue in the aerospace maintenance chemicals market share in 2023.

- Cleaners are critical in aerospace maintenance as they ensure the removal of dirt, grease, and contaminants from aircraft surfaces and components.

- Their application extends across various areas, including exterior cleaning, cabin cleaning, and engine maintenance, making them indispensable for maintaining aerodynamic efficiency and safety standards.

- The increasing frequency of aircraft cleaning cycles due to the aerospace maintenance chemicals market growth in global air traffic and heightened hygiene standards, especially post-pandemic, drives the trends for cleaners.

- Cleaners dominate the market due to their critical role in maintaining aircraft performance and safety, supported by stringent hygiene and maintenance protocols.

The lubricants segment is anticipated to register the fastest CAGR during the forecast period.

- Lubricants are essential for reducing friction and wear in aircraft components, including engines, landing gear, and control systems.

- Advanced synthetic lubricants are increasingly adopted to enhance performance and extend the operational life of components.

- The growing trends for high-performance lubricants tailored to meet the requirements of next-generation aircraft and increasing fleet sizes are key growth drivers for this segment.

- Lubricants are expected to grow rapidly, driven by the analysis of increasing adoption of advanced synthetic solutions and expanding worldwide aircraft fleets.

By Nature:

Based on nature, the market is segmented into organic and inorganic chemicals.

The organic segment accounted for the largest revenue in the aerospace maintenance chemicals market share in 2023.

- Organic aerospace maintenance chemicals are gaining traction due to their eco-friendly and biodegradable nature.

- These chemicals are used extensively in cleaning and degreasing applications to meet regulatory standards aimed at reducing environmental impact.

- The rising preference for green chemicals and increasing opportunities and regulatory scrutiny regarding the use of toxic substances in maintenance operations are driving the growth of the organic segment.

- Organic chemicals dominate the market due to their environmental benefits and growing adoption in compliance with stringent regulatory standards.

The inorganic segment is anticipated to register steady growth during the forecast period.

- Inorganic chemicals, including strong solvents and degreasers, are widely used for heavy-duty maintenance applications such as paint removal and engine cleaning.

- These chemicals are preferred for their effectiveness in handling tough contaminants and deposits.

- Despite growing concerns over environmental impact, advancements in safer formulations are expected to sustain demand for inorganic chemicals in specific applications.

- Thus, inorganic chemicals continue to grow steadily, driven by the analysis of their effectiveness in heavy-duty maintenance and ongoing innovations in safer formulations.

By Aircraft Type:

Based on aircraft type, the market is segmented into commercial aircraft, single-engine piston, military aircraft, business aircraft, and others.

The commercial aircraft segment accounted for the largest revenue share in 2023.

- Commercial aircraft require frequent maintenance cycles, including line, base, and engine maintenance, making them the largest consumers of maintenance chemicals.

- The rapid recovery of worldwide air travel post-pandemic, coupled with fleet expansions and increasing demand for fuel-efficient next-generation aircraft, supports this segment’s dominance.

- Airlines’ focus on enhancing operational efficiency further drives the demand for maintenance chemicals in this category.

- Commercial aircraft lead the market due to their large fleet sizes, frequent maintenance needs, and growing adoption of next-generation aircraft.

The military aircraft segment is anticipated to register steady growth during the forecast period.

- Military aircraft require rigorous maintenance to ensure operational readiness and performance in challenging environments.

- Specialized maintenance chemicals are used to address the unique requirements of military-grade components and systems.

- The rising defense budgets globally and increasing procurement of advanced fighter jets and UAVs are key drivers for this segment.

- Military aircraft continue to grow steadily, driven by increasing defense budgets and the adoption of advanced military aviation technologies.

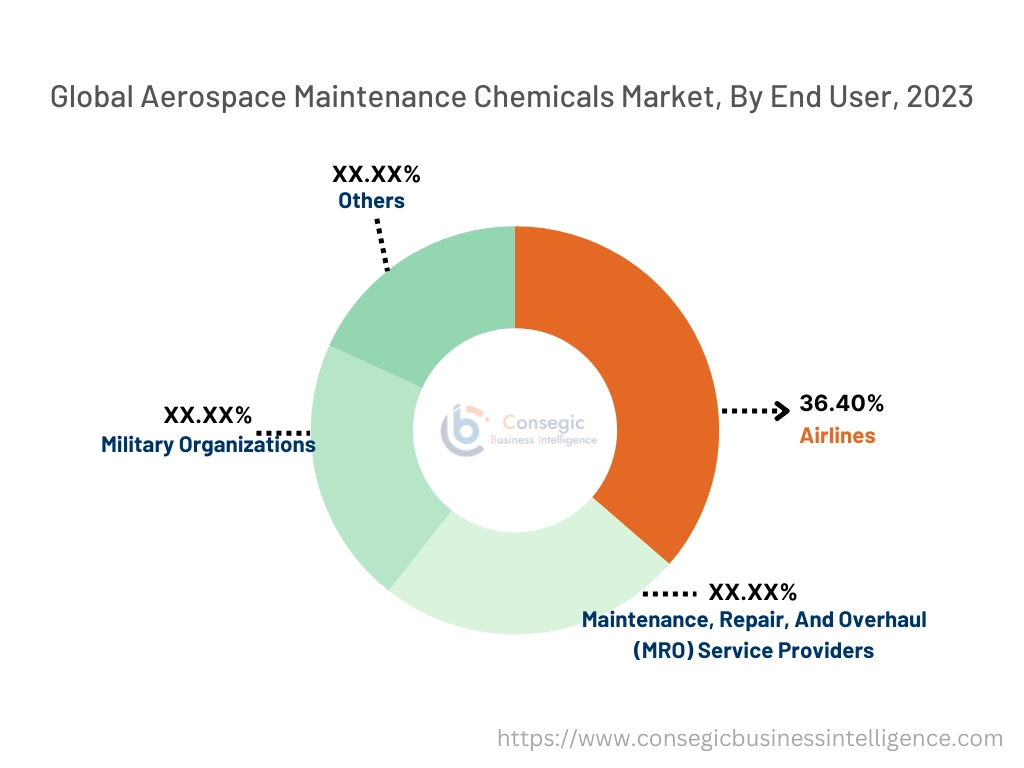

By End-Use Industry:

Based on end-users, the market is segmented into airlines, maintenance, repair, and overhaul (MRO) service providers, military organizations, and others.

The airline segment accounted for the largest revenue of 36.40% share in 2023.

- Airlines are the primary consumers of aerospace maintenance chemicals as they handle the regular upkeep of their fleets to ensure operational efficiency and passenger safety.

- The aerospace maintenance chemicals market growth of worldwide air traffic, coupled with fleet expansions and increasing regulatory compliance requirements, drives the aerospace maintenance chemicals market trends for maintenance chemicals in this segment.

- Airlines’ growing focus on sustainability and the use of eco-friendly chemicals further supports growth.

- Airlines dominate the market due to their responsibility for fleet maintenance, supported by expanding fleets and rising regulatory compliance needs.

The MRO service providers segment is anticipated to register the fastest CAGR during the forecast period.

- Maintenance, Repair, and Overhaul (MRO) service providers play a crucial role in maintaining aircraft for airlines, business aviation, and military organizations.

- The increasing outsourcing of maintenance operations by airlines to specialized MRO providers is driving aerospace maintenance chemicals market trends for maintenance chemicals in this segment.

- Additionally, the growing complexity of modern aircraft and engines, requiring specialized chemicals, further boosts this segment’s growth.

- MRO service providers are expected to grow rapidly, driven by the increasing outsourcing of maintenance activities and the demand for specialized solutions for advanced aircraft.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

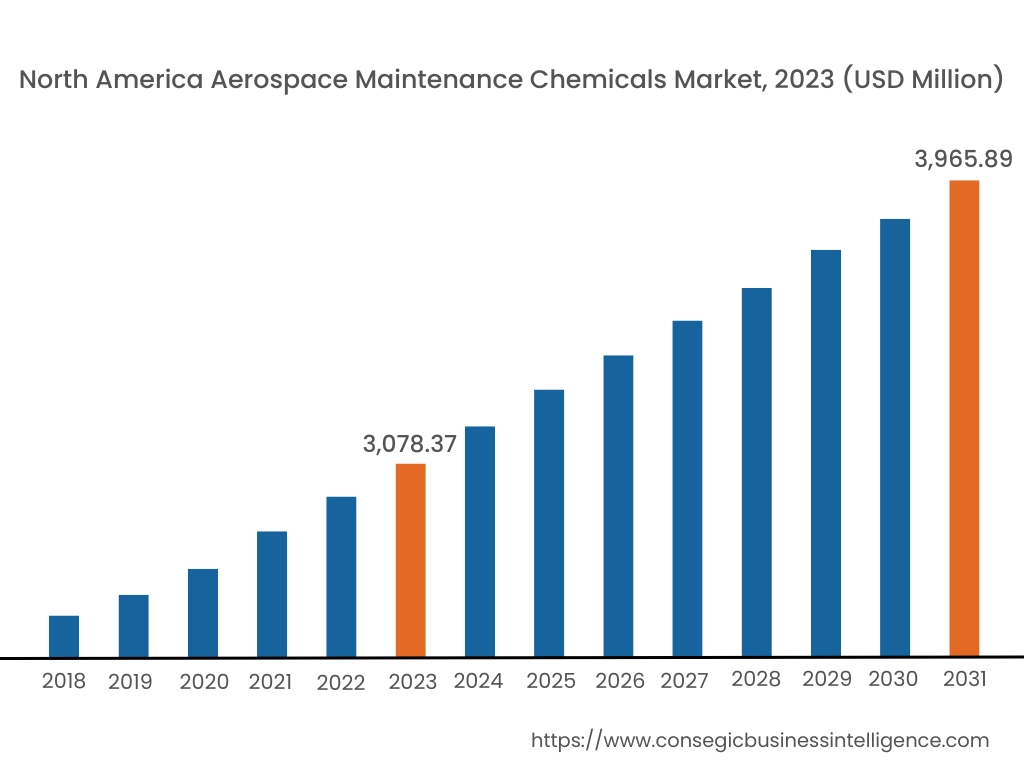

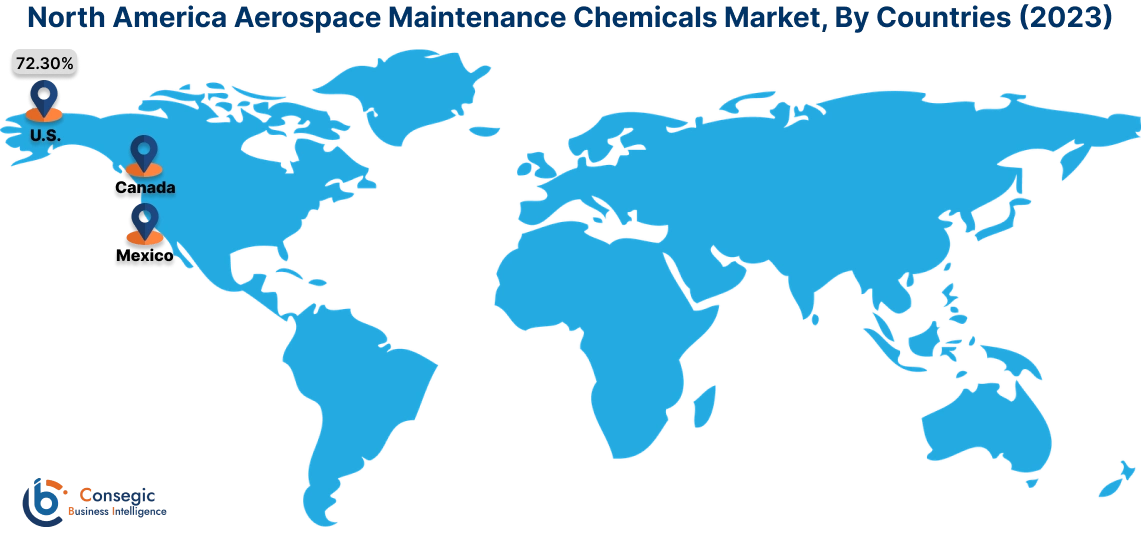

In 2023, North America was valued at USD 3,078.37 Million and is expected to reach USD 3,965.89 Million in 2031. In North America, the U.S. accounted for the highest share of 72.30% during the base year of 2023. North America holds a significant stake in the aerospace maintenance chemicals market analysis, driven by the strong presence of major airlines, aerospace manufacturers, and MRO (Maintenance, Repair, and Overhaul) service providers. The U.S. leads the region with high aerospace maintenance chemicals market demand for cleaning, degreasing, and anti-corrosion chemicals due to the large commercial and defense aircraft fleets. Canada contributes through its growing MRO sector, focusing on advanced maintenance solutions for regional and international airlines. However, stringent environmental regulations on chemical usage, particularly for volatile organic compounds (VOCs), may pose challenges for manufacturers in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 3.9% over the forecast period. Asia-Pacific is the fastest-growing region in the aerospace maintenance chemicals market analysis, fueled by the rapid expansion of commercial aviation, increasing air passenger traffic, and rising defense budgets in China, India, and Japan. China leads the region with significant investments in MRO facilities and a growing market surge for cleaning and anti-corrosion chemicals to maintain its expanding aircraft fleet. India’s growing aviation sector, supported by government initiatives, drives the use of maintenance chemicals in regional airlines and defense aviation. Japan focuses on advanced maintenance technologies and high-performance chemicals for its well-established aerospace sector. However, cost sensitivity in emerging markets and environmental concerns may pose challenges.

Europe is a prominent aerospace maintenance chemicals market demand, supported by the presence of leading aircraft manufacturers, extensive MRO operations, and stringent safety and maintenance regulations. Countries like Germany, France, and the UK are key contributors. Germany’s advanced aerospace industry emphasizes the use of high-performance maintenance chemicals for cleaning and surface treatment. France, home to major aircraft manufacturers, relies heavily on specialized chemicals for maintenance to ensure compliance with strict EU aviation standards. The UK focuses on sustainable and eco-friendly maintenance chemicals, aligning with environmental goals. However, regulatory complexities and high costs of compliance may impact growth.

The Middle East & Africa regions analysis is witnessing steady growth in the market, driven by the increasing presence of regional and international airlines and investments in MRO facilities. The UAE and Saudi Arabia are key contributors, with significant trends for cleaning and surface treatment chemicals to support large commercial fleets and defense aircraft. In Africa, South Africa is emerging as a market with a growing adoption of aerospace maintenance chemicals in regional airlines and military aviation. However, limited local production capabilities and reliance on imported chemicals may hinder broader market development in the region.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s aerospace sector, supported by its role in manufacturing regional aircraft, drives the trends for maintenance chemicals in cleaning and surface protection. Mexico’s growing MRO sector, catering to international airlines and aerospace companies, supports the use of high-performance chemicals for maintenance and repair operations. However, economic instability and inconsistent regulatory frameworks may pose challenges for aerospace maintenance chemicals market expansion across the region.

Top Key Players and Market Share Insights:

The Aerospace Maintenance Chemicals market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global aerospace maintenance chemicals market. Key players in the aerospace maintenance chemicals industry include -

- Exxon Mobil Corporation (U.S.)

- Royal Dutch Shell plc (Netherlands)

- Eastman Chemical Company (U.S.)

- ALMADION International (U.A.E.)

- JACO INDUSTRIALS INC. (U.S.)

- The Dow Chemical Company (U.S.)

- Arrow Solutions (U.K.)

- Callington Haven Pty Ltd. (Australia)

- Florida Chemical (U.S.)

- Nuvite Chemical Compounds (U.S.)

Recent Industry Developments :

- In June 2024, com launched a dedicated marketplace for aviation chemicals and consumables, streamlining procurement for the aerospace maintenance sector. This platform connects buyers with a global network of reputable suppliers, offering a comprehensive catalog of aviation-grade chemicals essential for aircraft maintenance and operations. Advanced search functions allow users to filter products by type, grade, quantity, and location, enhancing efficiency in sourcing materials like cleaning agents, corrosion inhibitors, and sealants. This development simplifies the procurement process, fostering connections between businesses and suppliers within the aviation sector.

Aerospace Maintenance Chemicals Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 12,236.61 Million |

| CAGR (2024-2031) | 3.5% |

| By Product Type |

|

| By Nature |

|

| By Aircraft Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Aerospace Maintenance Chemicals Market by 2031? +

Aerospace Maintenance Chemicals Market size is estimated to reach over USD 12,236.61 Million by 2031 from a value of USD 9,280.35 Million in 2023 and is projected to grow by USD 9,441.46 Million in 2024, growing at a CAGR of 3.5% from 2024 to 2031.

What drives the demand for aerospace maintenance chemicals? +

The increasing focus on aircraft maintenance for safety, operational efficiency, and compliance with stringent regulatory standards drives the demand. Chemicals such as cleaners, lubricants, and corrosion inhibitors play a vital role in maintaining aircraft performance and safety.

Which product type dominates the Aerospace Maintenance Chemicals Market? +

The cleaners segment holds the largest revenue share due to their essential role in removing dirt, grease, and contaminants from aircraft surfaces and components, ensuring aerodynamic efficiency and safety.

What are the major challenges faced by the Aerospace Maintenance Chemicals Market? +

Supply chain disruptions, raw material scarcity, and price volatility are significant challenges. Dependence on specific raw materials and stringent environmental regulations further complicate production and availability.