- Summary

- Table Of Content

- Methodology

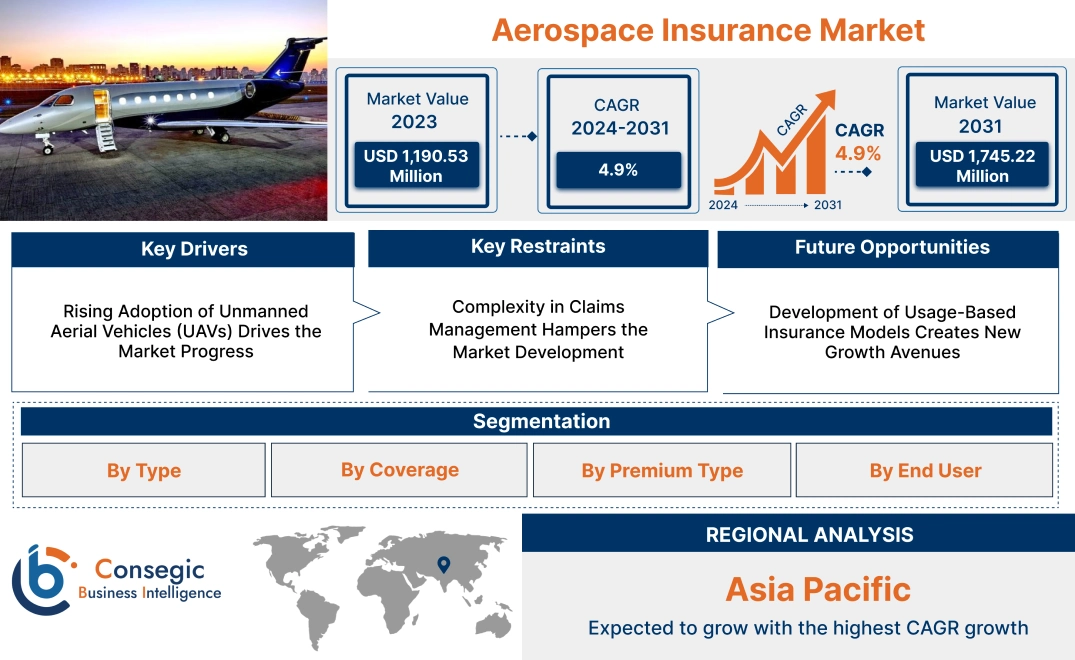

Aerospace Insurance Market Size:

Aerospace Insurance Market size is estimated to reach over USD 1,745.22 Million by 2031 from a value of USD 1,190.53 Million in 2023 and is projected to grow by USD 1,227.63 Million in 2024, growing at a CAGR of 4.90% from 2024 to 2031.

Aerospace Insurance Market Scope & Overview:

Aerospace insurance provides specialized coverage for risks associated with the aviation and aerospace industries. This includes protection for aircraft, airports, manufacturers, and other associated operations against potential liabilities, damages, and financial losses. Aerospace insurance policies typically cover areas such as physical damage to aircraft, third-party liability, passenger liability, and coverage for ground operations, ensuring comprehensive protection for industry stakeholders.

These insurance solutions are tailored to meet the unique demands of the aerospace sector, accounting for factors such as high operational costs, regulatory compliance, and the inherent risks of aviation activities. Policies also extend to include coverage for satellite launches, space exploration activities, and unmanned aerial systems, reflecting the evolving nature of the industry. Advanced risk assessment tools and actuarial models are used to design these policies, ensuring that they align with the specific requirements of clients.

End-users of aerospace insurance include airlines, aircraft manufacturers, maintenance and repair operators (MROs), airport authorities, and space exploration organizations. These solutions are critical in mitigating financial risks and ensuring the stability of operations in a high-stakes industry.

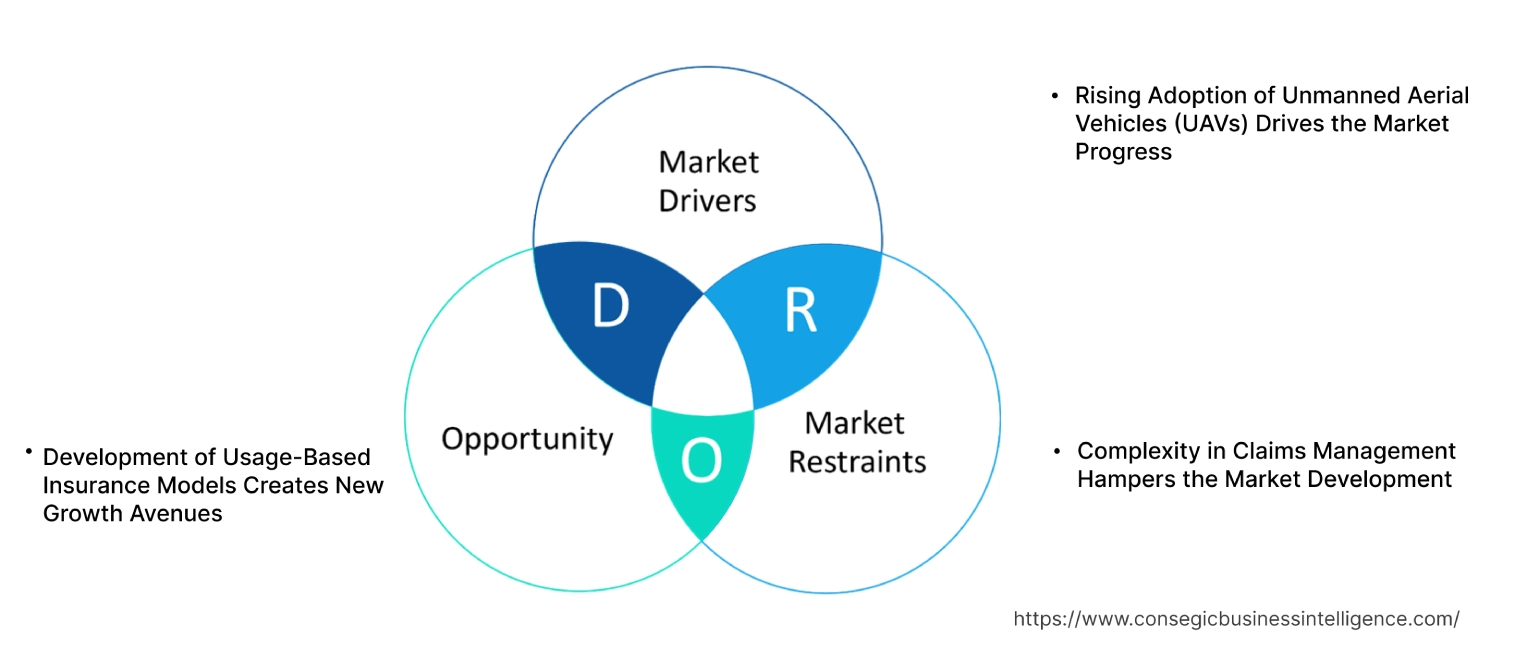

Aerospace Insurance Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of Unmanned Aerial Vehicles (UAVs) Drives the Market Progress

The rapid growth in the use of UAVs, or drones, across various sectors is driving significant demand for specialized insurance solutions. Industries such as agriculture, logistics, and surveillance increasingly rely on drones for operations like crop monitoring, package delivery, and security. These applications introduce unique risks, including airspace navigation challenges, potential collisions, payload damage, and operational failures.

The insurance sector is evolving to address these needs by offering customized policies that cover third-party liability, equipment damage, and regulatory compliance. In defense, drones used for reconnaissance and combat operations require comprehensive risk coverage tailored to their high-value systems. Similarly, recreational drone usage, growing in popularity, has also created a demand for affordable and accessible insurance products. As UAV adoption continues to expand, particularly with advancements in autonomous capabilities, the market for tailored drone insurance solutions drives the aerospace insurance market growth.

Key Restraints :

Complexity in Claims Management Hampers the Market Development

Claims management in aerospace insurance is inherently challenging due to the high-value assets and intricate nature of aviation-related incidents. Investigations often require collaboration among multiple stakeholders, including operators, manufacturers, regulators, and insurers, leading to extended timelines for claim resolution. Factors such as determining liability, assessing damage to costly assets like aircraft, and complying with aviation-specific regulations further complicate the process.

Additionally, the need for precise documentation and analysis of incidents, such as crashes or mid-air collisions, increases the time and effort required for settlement. This complexity not only delays compensation but also affects customer confidence in the system. Businesses and operators, particularly smaller entities with limited cash flow, hesitate to invest in aerospace insurance due to concerns over prolonged claims handling, limiting the aerospace insurance market demand.

Future Opportunities :

Development of Usage-Based Insurance Models Creates New Growth Avenues

Usage-based insurance (UBI) models are transforming the aerospace insurance sector by offering more flexible and cost-effective solutions tailored to specific operational needs. Unlike traditional models, UBI calculates premiums based on actual flight hours, operational data, or usage metrics, aligning costs with the scale and frequency of operations. This innovative approach particularly benefits smaller operators, charter services, and drone operators who do not require comprehensive, full-coverage policies year-round.

By leveraging advanced technologies such as IoT and telematics, insurers monitor real-time data on flight activity, maintenance schedules, and environmental factors, ensuring precise risk assessment and pricing. This customization reduces financial strain on smaller businesses while improving transparency and trust between insurers and clients. As aerospace operations diversify, particularly with the growth of UAVs and regional air transport, UBI models are expected to gain significant adoption, creating new aerospace insurance market opportunities.

Aerospace Insurance Market Segmental Analysis :

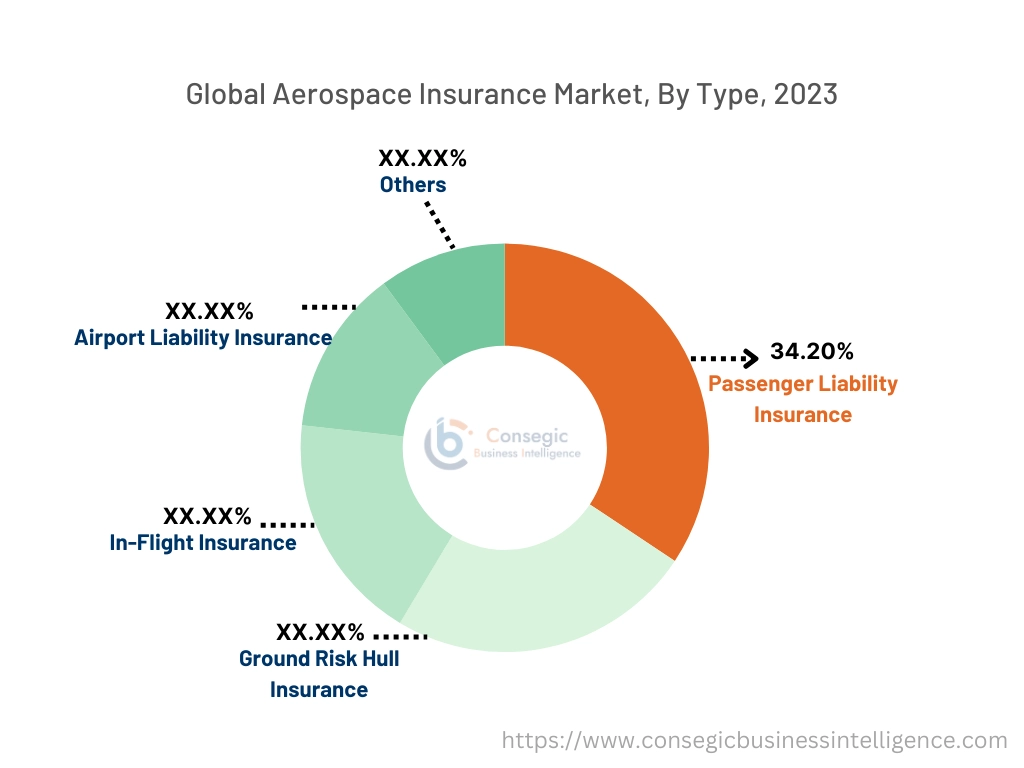

By Type:

Based on type, the market is segmented into passenger liability insurance, ground risk hull insurance, in-flight insurance, airport liability insurance, and others.

The Passenger liability insurance segment accounted for the largest revenue of 34.20% in 2023.

- This type of insurance ensures financial coverage for airlines against claims arising from passenger injuries, fatalities, or property damage during flights.

- The increasing global air travel volume has elevated the importance of passenger liability insurance for airline operators to mitigate financial risks.

- Regulatory requirements mandating liability insurance coverage for commercial aviation operators further drive its dominance in the segment.

- Its adoption is essential for maintaining compliance and safeguarding operational integrity in the aviation sector, which further drives the aerospace insurance market expansion.

The Ground risk hull insurance segment is expected to grow at the fastest CAGR during the forecast period.

- It offers coverage for damages incurred by aircraft while on the ground, including during maintenance, refueling, or parked operations.

- Airports and maintenance operators increasingly opt for ground risk hull insurance to minimize financial exposure during unforeseen incidents.

- As per the aerospace insurance market analysis, the rapid growth of this segment is supported by the proliferation of airport operations and increasing investments in ground-handling infrastructure.

By Coverage:

Based on coverage, the market is segmented into comprehensive coverage, third-party liability coverage, crew member coverage, and cargo liability coverage.

The Comprehensive coverage segment held the largest revenue of the total aerospace insurance market share in 2023.

- It provides end-to-end protection against a wide range of risks, including damages to aircraft, crew, passengers, and third parties.

- Airlines and fleet operators prefer comprehensive coverage to streamline risk management under a single insurance policy.

- Its widespread adoption reflects the need for broad financial protection in an increasingly complex aviation environment.

- As per aerospace insurance market trends, comprehensive policies are favored by commercial and private aviation operators aiming to optimize their insurance portfolios.

The Cargo liability coverage segment is expected to grow at the fastest CAGR during the forecast period.

- This coverage safeguards operators against damages or loss of goods during air transportation.

- The rise in air freight volume, fueled by the expansion of global e-commerce, contributes significantly to the growth of this segment.

- Logistics companies and airlines prioritize cargo liability coverage to meet contractual obligations and ensure customer satisfaction.

- As per the market trends the rapid adoption of this segment is supported by increasing reliance on air freight for high-value and time-sensitive shipments, contributing to the aerospace insurance market growth.

By End User:

Based on end-users, the market is segmented into aircraft operators, aircraft manufacturers, and aircraft lessors.

The Aircraft operators segment accounted for the largest revenue share in 2023.

- Operators, including commercial airlines and private charter companies, rely heavily on aerospace insurance to mitigate operational risks.

- Comprehensive policies provide protection against liabilities, damages, and third-party claims, ensuring financial stability for operators.

- The dominance of this segment reflects the scale and diversity of operations handled by aircraft operators globally.

- Their significant contribution to market revenue is supported by increasing air travel demand and expanding fleet sizes, encouraging the aerospace insurance market expansion.

The Aircraft lessors segment is expected to grow at the fastest CAGR during the forecast period.

- Insurance for leased aircraft ensures compliance with leasing agreements and protects lessors from financial losses.

- The growing popularity of aircraft leasing, particularly among low-cost carriers, boosts the demand for lessor-specific insurance solutions.

- Increasing leasing activity in emerging markets supports the rapid progress of this segment.

- Therefore, as per the aerospace insurance market trends, lessors benefit from customized policies designed to cover risks associated with fleet leasing and maintenance.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

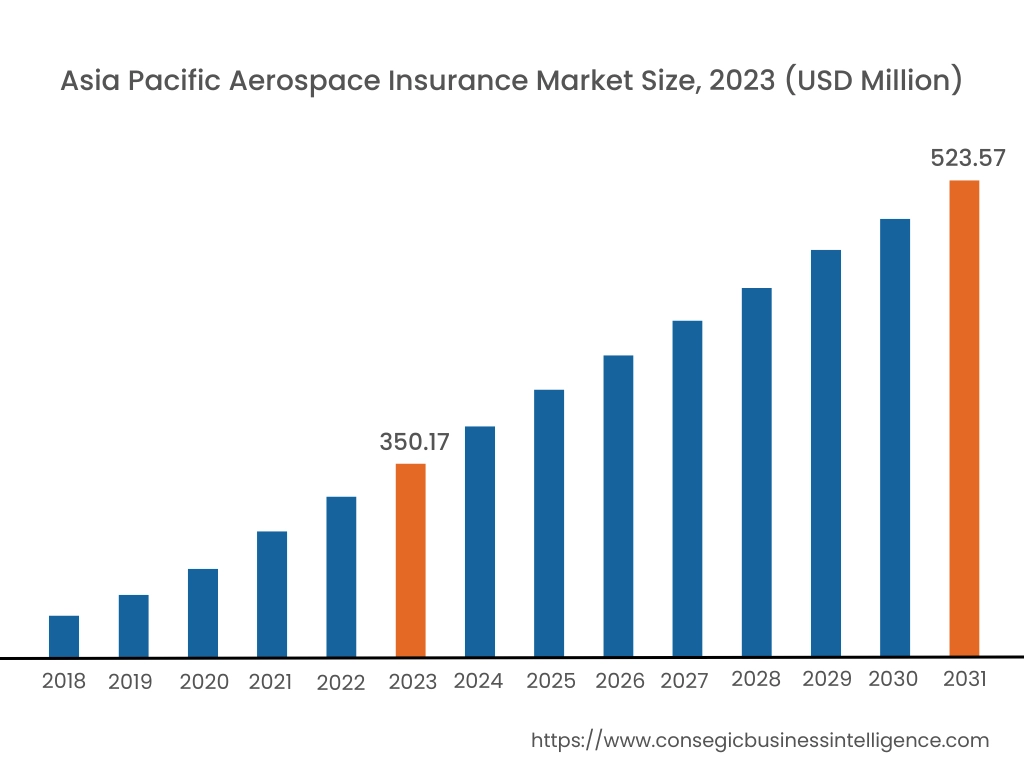

Asia Pacific region was valued at USD 350.17 Million in 2023. Moreover, it is projected to grow by USD 361.69 Million in 2024 and reach over USD 523.57 Million by 2031. Out of these, China accounted for the largest share of 23.4% in 2023. The Asia-Pacific region is experiencing rapid development in the aerospace insurance market, propelled by increasing air travel demand and significant investments in aviation infrastructure. Countries such as China, India, and Japan are expanding their commercial fleets and developing new airports, leading to a heightened need for comprehensive insurance coverage. Market analysis reveals a trend towards adopting digital platforms for policy distribution and customer engagement, catering to a tech-savvy clientele.

North America is estimated to reach over USD 574.18 Million by 2031 from a value of USD 395.72 Million in 2023 and is projected to grow by USD 407.71 Million in 2024. This region holds a significant share of the aerospace insurance market, driven by a robust aviation sector and a comprehensive regulatory framework. The United States, in particular, has a well-established aerospace sector, encompassing commercial airlines, private aviation, and defense operations. The trend towards integrating advanced technologies, such as artificial intelligence and data analytics, into insurance processes is notable, aiming to enhance risk assessment and streamline claims management, creating significant aerospace insurance market opportunities.

Europe represents a substantial portion of the global aerospace insurance market, with countries like the United Kingdom, France, and Germany leading in aviation activities. The region's stringent safety regulations and emphasis on environmental sustainability influence insurance underwriting practices. Recent analysis indicates a growing trend towards offering specialized insurance products tailored to the needs of low-cost carriers and regional airlines.

The Middle East & Africa region shows a growing interest in aerospace insurance, particularly due to the extension of national carriers and investments in aviation infrastructure. The Gulf states, including the United Arab Emirates and Qatar, are enhancing their aviation capabilities, necessitating sophisticated insurance products. Trends indicate a focus on risk management services that address geopolitical risks and operational hazards unique to the region.

Latin America is an emerging market for aerospace insurance, with Brazil and Mexico being key contributors. The region's growing aviation sector, driven by rising passenger traffic and cargo operations, underscores the need for tailored insurance solutions. Analysis suggests a trend towards collaborative efforts between insurers and aviation companies to develop products that address regional operational risks and regulatory requirements.

Top Key Players & Market Share Insights:

The aerospace insurance market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global aerospace insurance market. Key players in the aerospace insurance industry include –

- AIG Aerospace (USA)

- Global Aerospace (UK)

- Berkshire Hathaway (USA)

- Zurich Insurance Group (Switzerland)

- Munich Re (Germany)

- Hiscox (Bermuda)

- Tokio Marine HCC (USA)

- Allianz Global Corporate & Specialty (AGCS) (Germany)

- Chubb Limited (Switzerland)

- Lloyd's of London (UK)

Recent Industry Developments:

Product Launch:

- In December 2024, Worldlink Specialty, LLC launched a digital portal streamlining aviation insurance access. The platform, debuting in mid-November, offers quick quotes, policy binding, and products like Helipad General Liability and Non-Owned UAV Liability. Designed for efficiency, it ensures flexible, high-quality coverage, backed by A-rated financial partners, meeting the evolving needs of brokers and aviation clients.

Aerospace Insurance Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 1,745.22 Million |

| CAGR (2024-2031) | 4.9% |

| By Type |

|

| By Coverage |

|

| By Premium Type |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Aerospace Insurance Market? +

Aerospace Insurance Market size is estimated to reach over USD 1,745.22 Million by 2031 from a value of USD 1,190.53 Million in 2023 and is projected to grow by USD 1,227.63 Million in 2024, growing at a CAGR of 4.90% from 2024 to 2031.

What are the key segments in the Aerospace Insurance Market? +

The Aerospace Insurance Market is segmented by type (Passenger Liability Insurance, Ground Risk Hull Insurance, In-Flight Insurance, Airport Liability Insurance, Others), coverage (Comprehensive Coverage, Third-Party Liability Coverage, Crew Member Coverage, Cargo Liability Coverage, Others), premium type (Flat Premium, Pay-As-You-Go Premium, Hour Flown Premium), end-user (Aircraft Operators, Aircraft Manufacturers, Aircraft Lessors), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Aerospace Insurance Market? +

The Ground Risk Hull Insurance segment is expected to grow at the fastest CAGR during the forecast period. This is due to the increasing adoption of this coverage by airports and maintenance operators to reduce financial exposure during unforeseen incidents and operational disruptions.

Who are the major players in the Aerospace Insurance Market? +

Key players in the Aerospace Insurance Market include AIG Aerospace (USA), Global Aerospace (UK), Hiscox (Bermuda), Tokio Marine HCC (USA), Allianz Global Corporate & Specialty (AGCS) (Germany), Chubb Limited (Switzerland), Lloyd's of London (UK), Berkshire Hathaway (USA), Zurich Insurance Group (Switzerland), and Munich Re (Germany).