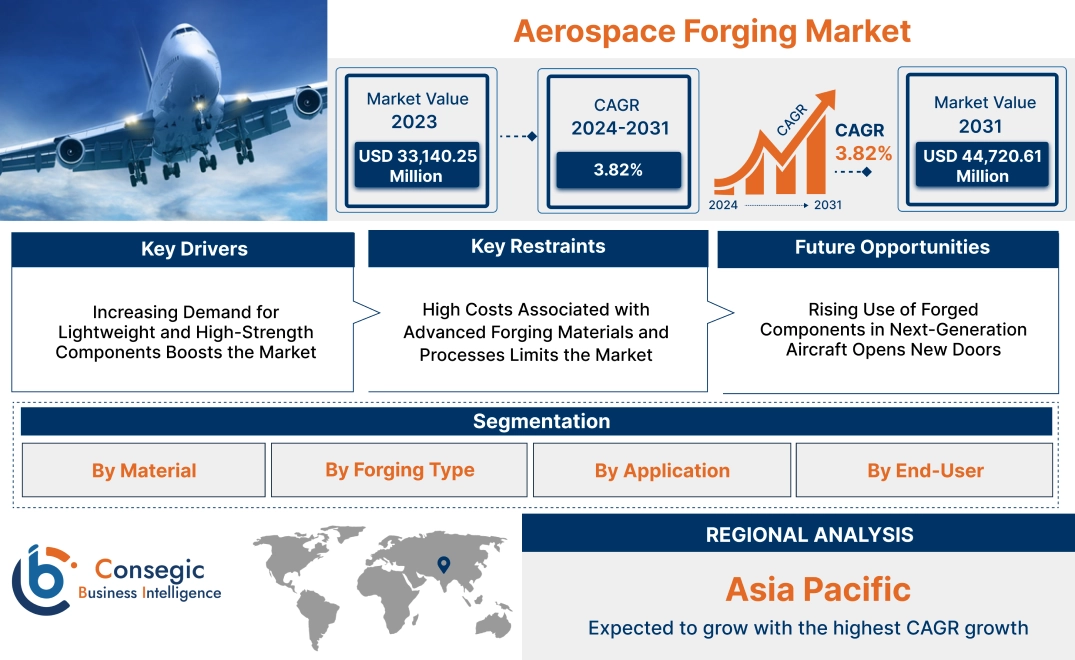

Aerospace Forging Market Size:

The Aerospace Forging Market size is estimated to reach over USD 44,720.61 Million by 2031 from a value of USD 33,140.25 Million in 2023 and is projected to grow by USD 33,814.99 Million in 2024, growing at a CAGR of 3.82% from 2024 to 2031.

Aerospace Forging Market Scope & Overview:

Aerospace forging is the method of producing high-strength components for aerospace applications using forging processes, which involve shaping metal under high pressure. Forged components are essential in the aerospace industry due to their superior mechanical properties, such as enhanced strength, durability, and resistance to fatigue and extreme conditions. Key characteristics of the market include precise dimensional accuracy, the ability to process high-performance alloys like titanium and aluminum, and superior grain structure in the forged parts. The benefits include improved reliability, reduced material wastage, and compatibility with lightweight and high-stress components. Applications span engine components, landing gear, structural parts, and airframe assemblies. End-users include aircraft manufacturers, maintenance repair and overhaul (MRO) providers, and defense contractors, driven by increasing aerospace forging market demand for fuel-efficient aircraft, advancements in forging technologies, and the growing adoption of lightweight materials to improve performance and reduce emissions.

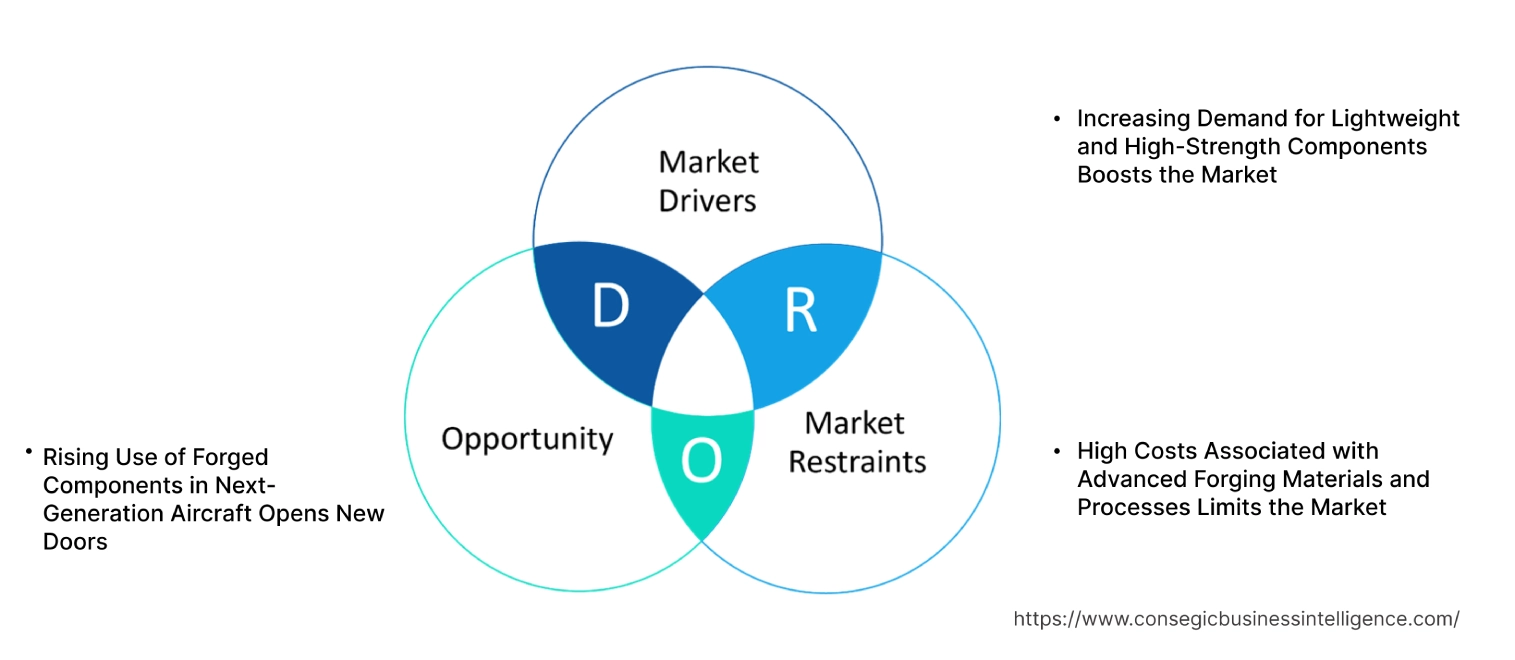

Aerospace Forging Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Lightweight and High-Strength Components Boosts the Market

The aerospace sector is increasingly focused on reducing fuel consumption and emissions, driving the need for lightweight yet durable components. Forged parts, known for their superior strength-to-weight ratio, are essential in achieving these objectives. Materials such as titanium and aluminum alloys are widely used in forging to produce critical aerospace components, including turbine blades, landing gear, and structural supports. These components must withstand extreme operational conditions, including high temperatures and mechanical stress, making forging a preferred manufacturing process for high-performance parts.

Trends in material science and advanced forging techniques are enabling the production of even lighter and stronger components, aligning with the sector's goals for operational efficiency and environmental compliance. The analysis highlights that as aerospace manufacturers prioritize fuel efficiency and enhanced safety, the adoption of forged components continues to gain traction across both commercial and military sectors.

Key Restraints :

High Costs Associated with Advanced Forging Materials and Processes Limits the Market

The production of aerospace-grade forged components is inherently cost-intensive, driven by the use of high-value materials such as titanium and nickel alloys. These materials, while offering exceptional performance, require specialized processing and precision equipment, significantly increasing manufacturing expenses. Furthermore, the energy-intensive nature of forging processes, combined with the need for skilled labor, adds to operational costs, making it challenging for smaller manufacturers to compete in the market.

The rising costs of raw materials due to supply chain constraints and geopolitical factors further exacerbate this issue. Manufacturers must also invest in quality assurance and testing to meet the stringent safety and certification standards of the aerospace sectors, adding complexity and financial burden. Addressing these challenges requires innovations in cost-efficient forging techniques and material utilization to enhance affordability without compromising performance.

Future Opportunities :

Rising Use of Forged Components in Next-Generation Aircraft Opens New Doors

The development of next-generation aircraft, including electric and hybrid-electric models, is creating significant aerospace forging market opportunities. These aircraft require components that are not only lightweight but also capable of withstanding the demands of advanced propulsion systems and high-stress environments. Forged parts, with their exceptional mechanical properties, are critical in ensuring the structural integrity and performance of these innovative aircraft designs.

Trends in sustainable aviation are also driving the use of forged components in engines, wings, and fuselage structures, where weight reduction directly contributes to energy efficiency. Advanced forging techniques, such as isothermal forging and near-net-shape manufacturing, are enabling the production of complex geometries with reduced material waste, aligning with the sector's focus on eco-friendly and cost-effective solutions. The analysis suggests that as the aviation sector continues to evolve, the role of forged components will become even more prominent in meeting its technological and environmental objectives.

Aerospace Forging Market Segmental Analysis :

By Material:

Based on material, the market is segmented into titanium alloys, nickel alloys, aluminum alloys, stainless steel, and others.

The titanium alloys segment accounted for the largest revenue share in 2023.

- Titanium alloys are highly preferred in aerospace forging due to their excellent strength-to-weight ratio, corrosion resistance, and ability to withstand high temperatures.

- These properties make titanium alloys ideal for critical aircraft components such as engine parts, landing gear, and airframes.

- The development of lightweight materials to improve fuel efficiency and reduce emissions in modern aircraft is further driving the adoption of titanium alloys in aerospace applications.

- Titanium alloys dominate the market due to their superior mechanical properties and widespread use in high-performance aerospace components.

The nickel alloys segment is anticipated to register the fastest CAGR during the forecast period.

- Nickel alloys are increasingly used in aerospace forging, particularly for engine components that require exceptional resistance to heat and pressure.

- The growing surge for advanced jet engines and the production of next-generation military and commercial aircraft are driving the growth of this segment.

- Additionally, advancements in alloy manufacturing techniques are further enhancing the performance of nickel alloys.

- Nickel alloys are expected to grow rapidly, driven by their critical role in advanced engine components and high-temperature applications.

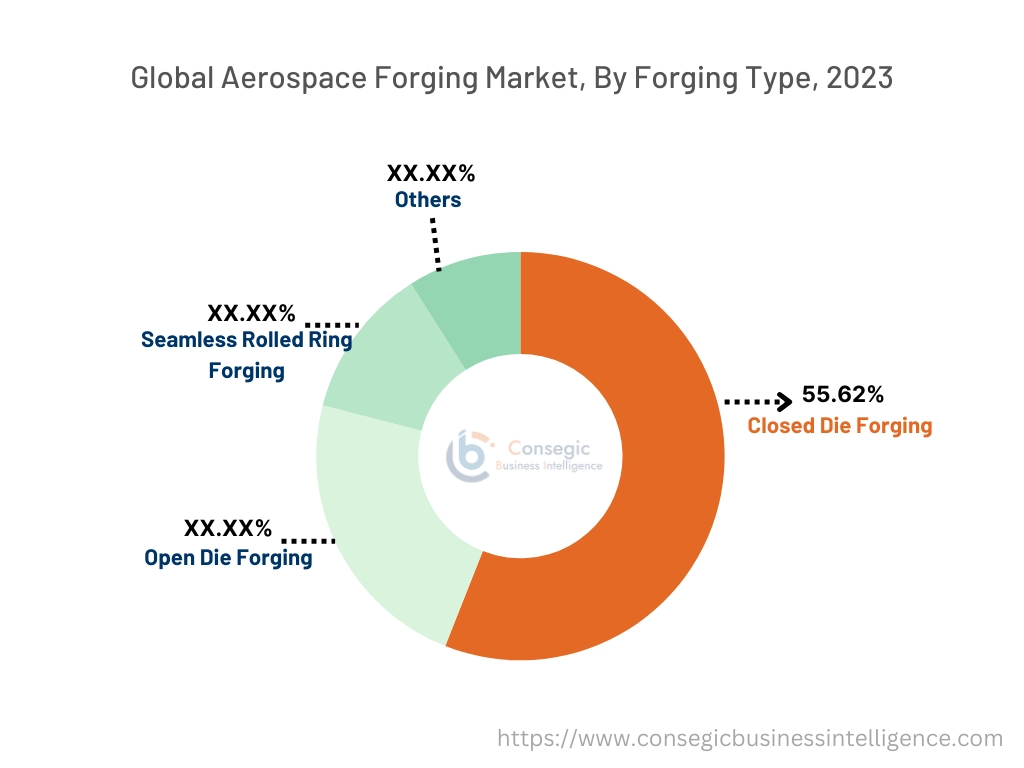

By Forging Type:

Based on forging type, the market is segmented into closed die forging, open die forging, seamless rolled ring forging, and others.

The closed die forging segment accounted for the largest revenue of 55.62% in the aerospace forging market share in 2023.

- Closed die forging is the most widely used forging process in aerospace manufacturing due to its ability to produce complex, high-strength components with minimal material wastage.

- This process is extensively applied in the production of engine parts, structural components, and landing gear.

- The trends for precision and durability in aerospace manufacturing support the dominance of this segment.

- Closed die forging leads the market due to its precision, material efficiency, and extensive use in manufacturing critical aerospace components.

The seamless rolled ring forging segment is anticipated to register the fastest CAGR during the forecast period.

- Seamless rolled ring forging is gaining traction for producing high-strength, durable components such as turbine rings and jet engine casings.

- This process ensures superior structural integrity, making it suitable for high-stress applications in the aerospace sector.

- The increasing aerospace forging market opportunities adoption of advanced jet engines and the need for reliable components are driving the growth of this segment.

- Seamless rolled ring forging is expected to grow rapidly due to its critical role in high-stress aerospace applications, particularly in advanced jet engines.

By Application:

Based on application, the market is segmented into aircraft structure, engine components, landing gear, and others.

The engine components segment accounted for the largest revenue share in 2023.

- Engine components are the most critical and high-value parts in aerospace due to their complex designs and the need to withstand extreme temperatures and pressures.

- Forged parts such as turbine disks, shafts, and casings are essential for ensuring engine performance and reliability.

- The increasing production of fuel-efficient and high-performance jet engines is driving the aerospace forging market trends for forged engine components.

- Engine components dominate the market due to their critical role in aircraft performance and the rising trends for advanced jet engines.

The landing gear segment is anticipated to register steady growth during the forecast period.

- Landing gear components require exceptional strength and durability to support the weight of the aircraft during takeoff and landing.

- Forging is the preferred manufacturing process for landing gear due to its ability to produce robust and reliable parts.

- The surge in global air traffic and the increasing production of commercial and military aircraft support steady demand for forged landing gear components.

- Landing gear continues to grow steadily, driven by the need for durable and high-strength components in commercial and military aircraft.

By End-User:

Based on end-user, the market is segmented into commercial aviation, military aviation, business & general aviation, and others.

The commercial aviation segment accounted for the largest revenue in the aerospace forging market share in 2023.

- The commercial aviation sector is the largest consumer of aerospace forgings due to the size of its global fleet and the frequency of maintenance and component replacement cycles.

- The growing trends for passenger and cargo aircraft, coupled with fleet modernization efforts, are driving the demand for forged components in this segment.

- Additionally, the recovery of air travel and the production of next-generation aircraft are further supporting growth.

- Commercial aviation dominates the market due to the rising trends for aircraft components and ongoing fleet expansions globally.

The military aviation segment is anticipated to register steady growth during the forecast period.

- Military aviation relies heavily on forged components for fighter jets, transport aircraft, and unmanned aerial vehicles (UAVs).

- The increasing defense budgets of several countries and the growing aerospace forging market trends for advanced military aircraft and UAVs are driving aerospace forging market growth in this segment.

- Forged components’ ability to withstand extreme conditions and ensure operational readiness makes them indispensable in military aviation.

- Military aviation continues to grow steadily, driven by increasing defense budgets and the adoption of advanced military aircraft and UAVs.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

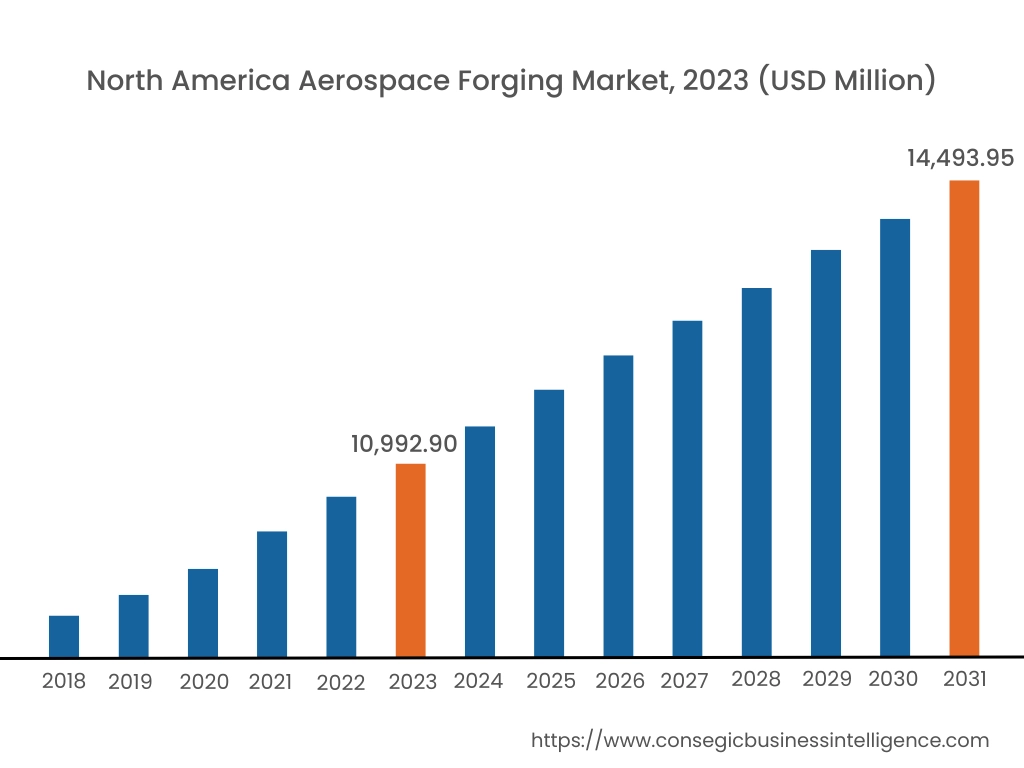

In 2023, North America was valued at USD 10,992.90 Million and is expected to reach USD 14,493.95 Million in 2031. In North America, the U.S. accounted for the highest share of 74.80% during the base year of 2023. North America dominates the aerospace forging market analysis, driven by the presence of leading aerospace manufacturers and a robust supply chain network. The U.S. leads the region, with extensive adoption of forging technologies to produce lightweight and high-strength components for aircraft. The market is bolstered by increasing trends for next-generation aircraft and high investments in military aviation. Canada contributes through its growing aerospace industry, focusing on forging solutions for landing gear, engine components, and structural parts. However, challenges such as fluctuating raw material prices and environmental regulations on metalworking processes may impact the region’s growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.3% over the forecast period. Asia-Pacific is the fastest-growing region in the aerospace forging market analysis, fueled by increasing aircraft production, growing air travel demand, and expanding defense budgets in China, India, and Japan. China leads the market with its focus on domestic aircraft manufacturing and the development of high-strength forged components for both commercial and military aviation. India is witnessing aerospace forging market growth due to government initiatives such as “Make in India,” encouraging local manufacturing of aerospace components. Japan’s advanced material science and focus on high-precision forging for engines and structural parts further boost the market. However, limited infrastructure for high-end forging technologies in some parts of the region may hinder growth.

Europe is a significant market, supported by the analysis and advanced manufacturing capabilities and strong aerospace forging market demand from commercial and military aviation sectors. Countries like Germany, France, and the UK are key contributors. Germany’s expertise in precision engineering drives the adoption of forging for critical aerospace components. France, home to major aircraft manufacturers, uses forging extensively in the production of airframes and engines. The UK emphasizes forging technologies in military aircraft and defense applications. However, high energy costs and stringent EU environmental regulations on forging processes pose challenges for manufacturers in the region.

The Middle East & Africa regions analysis portrays steady growth in the market, driven by increasing investments in aviation and defense sectors. Countries like Saudi Arabia and the UAE are key contributors, leveraging forging technologies for maintenance, repair, and manufacturing of aerospace components to support growing fleets. In Africa, South Africa is emerging as a market, focusing on the production of forged components for regional airlines and military applications. However, limited local production capabilities and reliance on imports for advanced forging technologies and materials may restrict aerospace forging market expansion.

Latin America is an emerging market for aerospace forging, with Brazil and Mexico leading the region. Brazil’s growing aerospace industry, driven by its strong presence in commercial and regional aircraft manufacturing, supports the adoption of forging for structural and engine components. As per the regional analysis, Mexico’s expanding aerospace manufacturing sector, particularly in producing forged parts for export to North America and Europe, enhances the market. However, economic instability and limited access to advanced forging facilities may pose challenges to broader adoption in the region.

Top Key Players and Market Share Insights:

The Aerospace Forging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global aerospace forging market. Key players in the aerospace forging industry include –

- Arconic Corporation (U.S.)

- Precision Castparts Corp. (U.S.)

- ELLWOOD Group Inc. (U.S.)

- Mettis Aerospace Ltd. (U.K.)

- Fountaintown Forge Inc. (U.S.)

- Bharat Forge Limited (India)

- VSMPO-AVISMA Corporation (Russia)

- ATI Inc. (U.S.)

- Larsen & Toubro Limited (India)

- Scot Forge Company (U.S.)

Recent Industry Developments :

Product Launches:

- In November 2024, the University of Strathclyde’s Advanced Forming Research Centre (AFRC) introduced the FutureForge platform, an industrial-scale isothermal testing facility. This platform accelerates the development of next-generation materials and process technologies, enabling the production of high-performance components that can withstand elevated temperatures, thereby enhancing jet engine efficiency and reducing fuel consumption.

Aerospace Forging Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 44,720.61 Million |

| CAGR (2024-2031) | 3.82% |

| By Material |

|

| By Forging Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Aerospace Forging Market by 2031? +

Aerospace Forging Market size is estimated to reach over USD 44,720.61 Million by 2031 from a value of USD 33,140.25 Million in 2023 and is projected to grow by USD 33,814.99 Million in 2024, growing at a CAGR of 3.82% from 2024 to 2031.

What drives the demand for forged components in the aerospace industry? +

The increasing need for lightweight, high-strength components to improve fuel efficiency and reduce emissions drives the demand for forged components in the aerospace industry. Materials like titanium and nickel alloys are extensively used due to their superior mechanical properties.

Which material segment dominates the Aerospace Forging Market? +

The titanium alloys segment holds the largest revenue share due to its excellent strength-to-weight ratio, corrosion resistance, and ability to withstand high temperatures, making it ideal for critical aerospace components.

What are the major challenges faced by the Aerospace Forging Market? +

High costs associated with advanced forging materials such as titanium and nickel alloys, along with energy-intensive processes and stringent quality standards, pose challenges for manufacturers.