- Summary

- Table Of Content

- Methodology

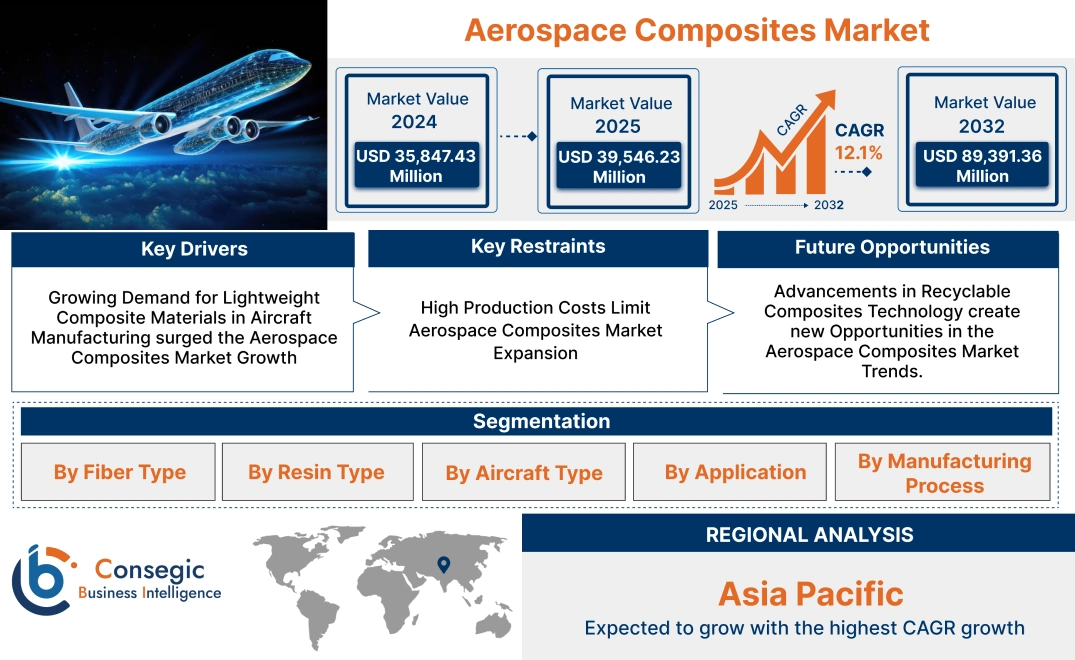

Aerospace Composites Market Size:

The Aerospace Composites Market size is estimated to reach over USD 89,391.36 Million by 2032 from a value of USD 35,847.43 Million in 2024 and is projected to grow by USD 39,546.23 Million in 2025, growing at a CAGR of 12.1% from 2025 to 2032.

Aerospace Composites Market Scope & Overview:

Aerospace composites are materials engineered to enhance aircraft performance, offering superior strength-to-weight ratios and resistance to fatigue and corrosion. These composites feature lightweight properties, high durability, and excellent thermal stability, making them ideal for improving fuel efficiency and extending aircraft lifespans.

Key benefits include reduced fuel consumption, increased payload capacity, and enhanced structural integrity. These composites are widely applied in commercial aircraft, military jets, and spacecraft, addressing critical requirements for safety and performance. End-use industries include commercial aviation, defense, and space exploration, where advanced composite materials are essential for manufacturing reliable, high-performance airframes and components.

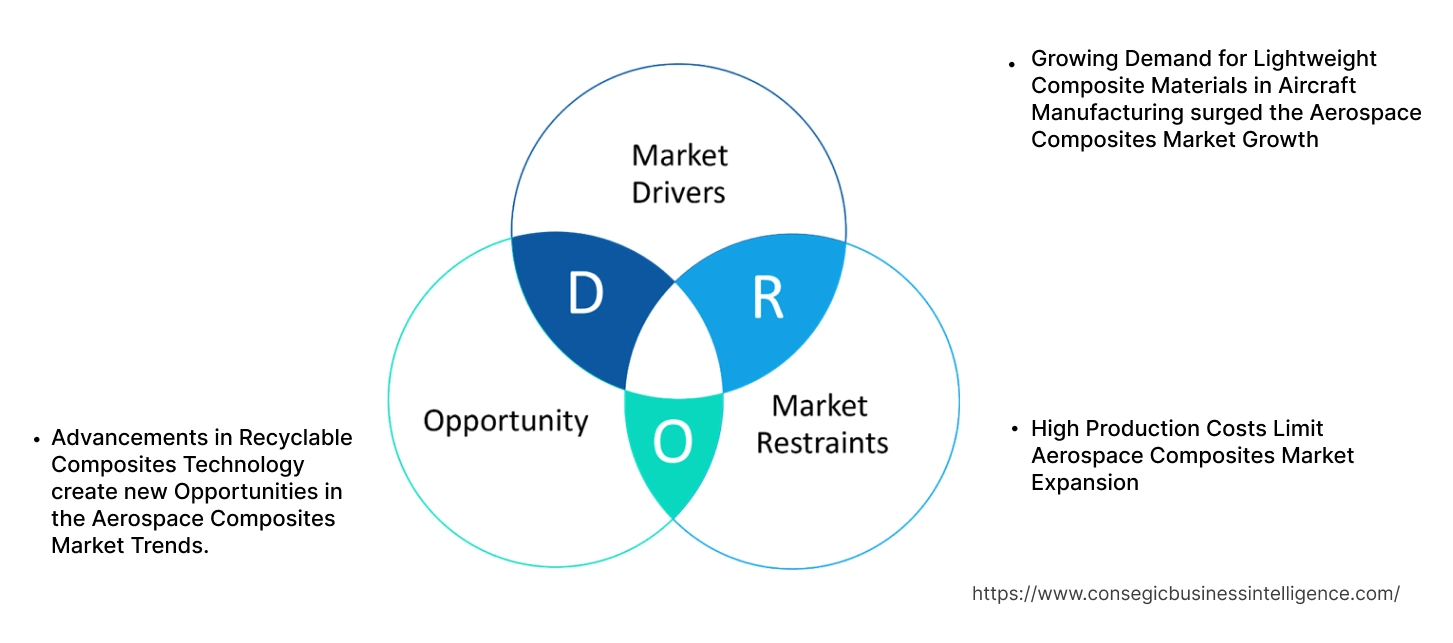

Aerospace Composites Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for Lightweight Composite Materials in Aircraft Manufacturing surged the Aerospace Composites Market Growth

The aerospace industry increasingly relies on lightweight composite materials to enhance fuel efficiency and reduce operational costs. Carbon fiber-reinforced composites, for instance, provide high strength-to-weight ratios, making them ideal for commercial aircraft structures. In recent years, Boeing incorporated these composites extensively in its 787 Dreamliner, resulting in significant weight reductions and improved fuel efficiency. As airlines prioritize fuel-efficient aircraft, the adoption of these composites for lightweight construction is expected to expand. Therefore, the increased aerospace composites market demand for lightweight materials in aircraft manufacturing is driving the market trends.

Key Restraints:

High Production Costs Limit Aerospace Composites Market Expansion

The manufacturing of aerospace composites, especially carbon fiber composites, involves high production costs due to complex processes and specialized equipment. These costs significantly impact the affordability of composite-based components, posing challenges for small aircraft manufacturers and budget-conscious airlines. Additionally, factors like the cost of raw materials and precision fabrication requirements further raise expenses. Consequently, the high costs associated with composite production constrain aerospace composites market growth, particularly in price-sensitive regions and smaller aerospace firms.

Future Opportunities :

Advancements in Recyclable Composites Technology create new Opportunities in the Aerospace Composites Market Trends.

The future development of recyclable composites presents promising aerospace composites market opportunities for the aerospace sector. Researchers are exploring sustainable materials and manufacturing techniques that allow composites to be reused without compromising strength or durability. For instance, initiatives aimed at producing recyclable carbon fiber composites are underway, which makes these composites more environmentally sustainable and economically viable. Thus, according to aerospace composites market analysis, the emergence of recyclable composites is expected to drive future aerospace composites market expansion as environmental regulations tighten, providing a sustainable solution for the aerospace industry.

Aerospace Composites Market Segmental Analysis :

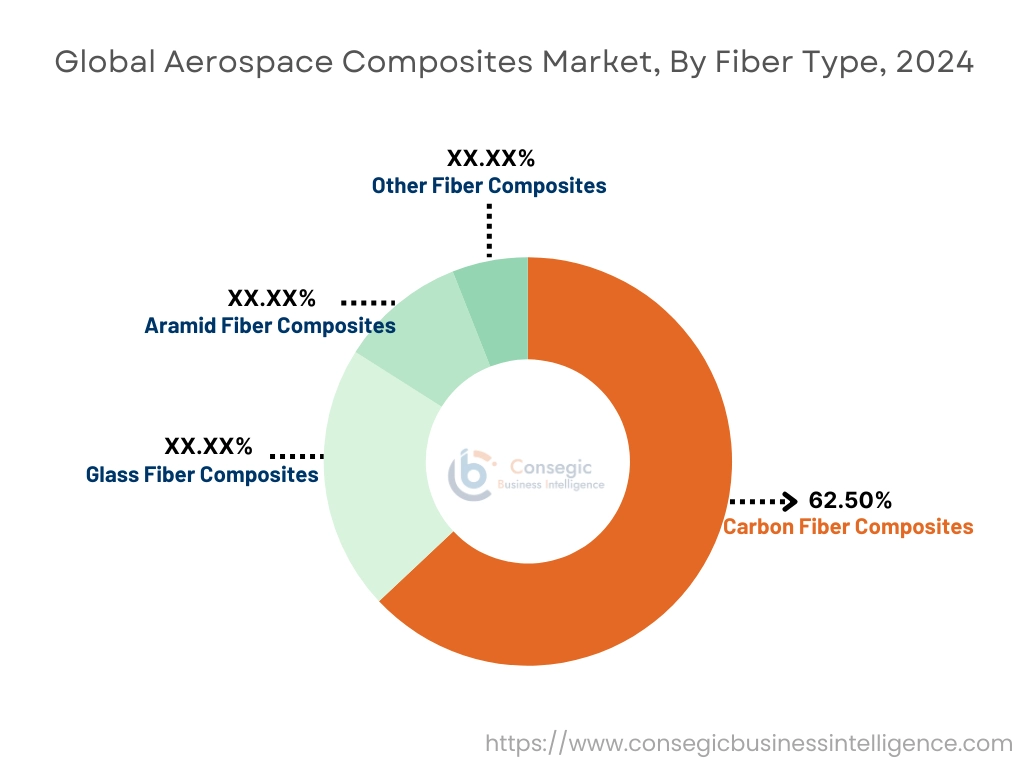

By Fibre Type:

Based on fiber type, the market is segmented into carbon fiber composites, glass fiber composites, aramid fiber composites, and other fiber composites.

The carbon fiber composites segment accounted for the largest revenue share of 62.50% in 2024.

- Carbon fiber composites are highly sought after for their lightweight properties combined with superior strength, reducing aircraft weight and improving fuel efficiency.

- They exhibit exceptional resistance to corrosion and fatigue, making them ideal for critical structural components in both commercial and military aircraft.

- Their use extends to applications such as wings, fuselage sections, and tail assemblies, which require high structural integrity.

- The segment’s growing trend is propelled by increasing production of next-generation aircraft and stringent emissions standards globally.

- Thus, market analysis suggests the dominance of carbon fiber composites stems from their unmatched strength-to-weight ratio and extensive adoption across commercial aviation and defense sectors.

The aramid fiber composites segment is anticipated to register the fastest CAGR during the forecast period.

- Aramid fiber composites are well-known for their impact resistance, flame retardancy, and lightweight nature, contributing to enhanced safety standards.

- These fibers are predominantly utilized in aircraft interiors, ballistic-grade protective materials, and rotorcraft applications.

- The rising aerospace composites market demand for materials that meet stringent safety and durability requirements in military and civil aviation drives their rapid adoption.

- Innovation in processing techniques has further boosted their efficiency and broadened their scope in aerospace applications.

- Therefore, according to the aerospace composites market analysis, the aramid fiber composites segment’s trending growth is fueled by its safety benefits and increasing integration in military and interior aviation components.

By Resin Type:

Based on resin type, the market is categorized into epoxy, phenolic, polyester, thermoplastic, ceramic, and other resins.

The epoxy resin segment accounted for the largest revenue in the market in 2024.

- Epoxy resins are known for their excellent adhesion, thermal resistance, and chemical stability, making them suitable for structural and protective components.

- They are widely used in manufacturing fuselage, wings, and load-bearing elements, ensuring enhanced performance and longevity.

- Their ability to maintain structural integrity under extreme conditions contributes significantly to aircraft safety and efficiency.

- The segment benefits from advancements in epoxy formulations that enable lighter and more durable composite components.

- The extensive adoption of epoxy resins in high-stress aerospace applications highlights their critical role in ensuring aircraft durability and efficiency.

The thermoplastic resin segment is projected to attain the fastest CAGR growth over the forecast period.

- Thermoplastics offer recyclability, high impact resistance, and adaptability, making them ideal for lightweight, high-volume production.

- They are increasingly used in non-load-bearing components, seating, and secondary structures, enhancing sustainability in aerospace manufacturing.

- The segment's current trend is driven by the rising aerospace composites market opportunities for rapid processing times and complex shapes in advanced aircraft design.

- Innovations in thermoplastic composites enable cost-efficient production without compromising performance.

- Therefore, the analysis of market trends shows that thermoplastic resins are gaining prominence for their eco-friendly properties and efficient production processes, aligning with the sector’s evolving priorities.

By Aircraft Type:

By aircraft type, the market is segmented into commercial aircraft, military aircraft, helicopters, spacecraft, and business jets & general aviation.

Commercial aircraft accounted for the largest revenue in the market in 2024.

- The rising requirement for air travel, especially in emerging markets, has driven the production of lightweight, fuel-efficient commercial aircraft.

- Composites in commercial aviation are primarily used to enhance fuel efficiency, reduce emissions, and lower operational costs.

- Applications include fuselage panels, wing spars, and other load-bearing components essential for structural stability.

- The ongoing replacement of aging aircraft fleets globally further supports the trending growth of this segment.

- Thus, market analysis shows that the commercial aircraft segment's growing trend reflects the increasing reliance on composites to meet efficiency, cost, and environmental standards in aviation.

The spacecraft segment is expected to register the fastest CAGR during the forecast period.

- The expansion of private space ventures and growing investments in government-led space exploration are driving need for lightweight, heat-resistant composite materials.

- Composites improve spacecraft payload capacity, durability, and resistance to the harsh space environment.

- Their application includes structural components, propulsion systems, and thermal shields, ensuring mission success and longevity.

- The need for advanced materials capable of supporting reusable spacecraft designs also boosts growth.

- Therefore, the spacecraft segment’s rapid growth is aligned with increased investments in space exploration and the requirement for innovative materials enhancing mission capabilities.

By Application:

Based on application, the market is segmented into interior, exterior, structural components, engine components, and other applications.

The structural components segment held the largest revenue share in the aerospace composites market share in 2024.

- Composites in structural components improve load-bearing capacity and overall aircraft performance while reducing material fatigue and weight.

- Applications include primary structures like wings, fuselage, and tail assemblies, where weight reduction is critical.

- The adoption of composite structures in military aircraft ensures enhanced stealth and performance.

- Increased production of composite-intensive aircraft models further strengthens the dominance of this segment.

- Thus, structural components drive the market due to their central role in enhancing aircraft design, performance, and efficiency.

The engine components segment is anticipated to register the fastest CAGR during the forecast period.

- Engine components made from composites offer exceptional thermal resistance and reduced weight, improving overall fuel efficiency.

- These materials are extensively used in fan blades, casings, and ducts, where high-stress resistance is essential.

- Innovations in composite technology have enabled higher durability and performance in extreme engine conditions.

- The segment benefits from the growing need for advanced propulsion systems in commercial and defense aviation.

- Therefore, the rapid adoption of composites in engine components reflects their critical role in advancing fuel-efficient, high-performance propulsion systems.

By Manufacturing Process:

Based on the manufacturing process, the market includes filament winding, layup, resin transfer molding, injection molding, and other manufacturing processes.

The layup process accounted for the largest revenue share in the aerospace composites market share in 2024.

- The layup process enables precise fiber placement, ensuring optimized strength-to-weight ratios for large aircraft components.

- This process is widely used in manufacturing critical parts like wings, fuselage panels, and stabilizers.

- Its adaptability to both manual and automated production enhances versatility across different aerospace applications.

- The growing demand for complex composite structures further drives reliance on the layup process.

- Thus, the layup process remains dominant due to its effectiveness in producing large, precise, and high-strength aerospace components.

The resin transfer molding process is projected to witness the fastest CAGR during the forecast period.

- Resin transfer molding ensures efficient production of complex composite parts with consistent quality and minimal waste.

- This process is well-suited for high-volume production, reducing costs while maintaining material integrity.

- Applications include interior components, brackets, and panels where precision and durability are critical.

- Increasing demand for cost-effective, lightweight solutions in aerospace drives the adoption of this process.

- Therefore, analysis suggests, that resin transfer molding is rapidly gaining exposure as a preferred process for producing high-quality, cost-effective aerospace composite components.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

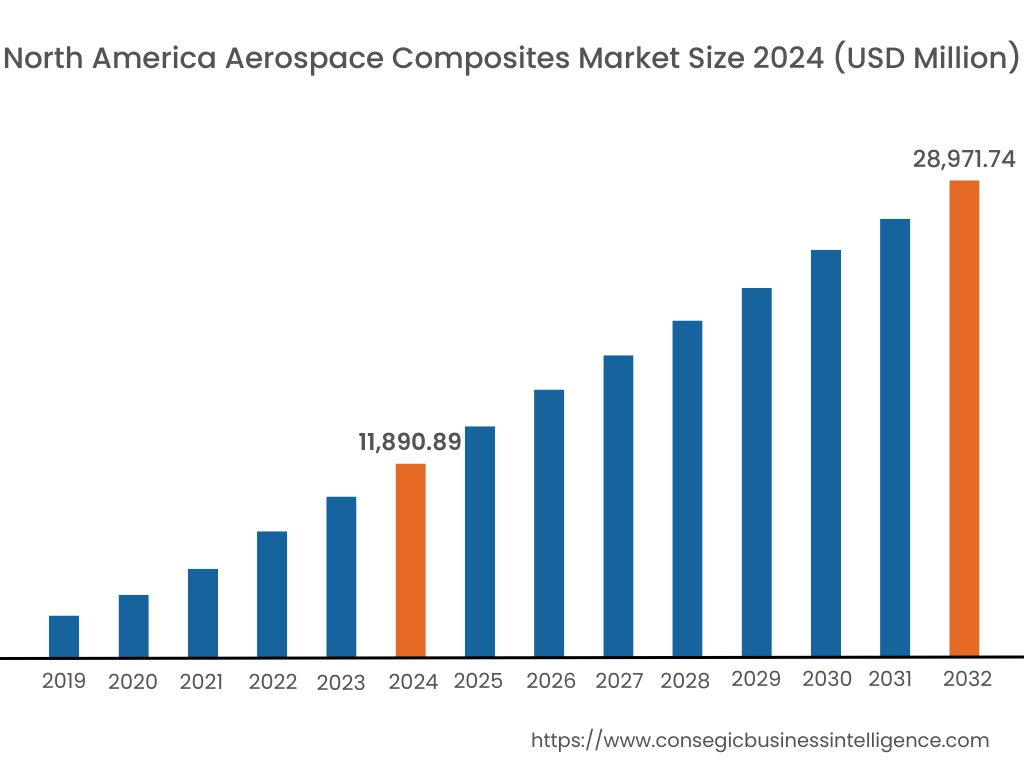

In 2024, North America was valued at USD 11,890.89 Million and is expected to reach USD 28,971.74 Million in 2032. In North America, the U.S. accounted for the highest share of 73.70% during the base year of 2024. The market in North America benefits from a strong presence of aerospace manufacturers and high defense spending. The United States is a leading user of advanced composite materials, particularly in military aircraft and commercial aviation. The rising demand for fuel-efficient aircraft contributes to the increased adoption of lightweight composite materials. Research initiatives focused on enhancing material durability and strength further support market advancement in North America.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 12.6% over the forecast period. In Asia-Pacific, the market is expanding due to rapid growth in the aviation sector and rising passenger traffic. Countries like China, Japan, and India are actively investing in aerospace production and modernization, promoting the use of composites for weight reduction. Government support for the domestic industry, especially in China, fosters regional market development. Additionally, local partnerships with global suppliers are boosting the availability of high-performance composite materials.

Europe's market benefits from the presence of major aircraft manufacturers, particularly in France and Germany. The region prioritizes eco-friendly aerospace innovations, leading to the adoption of sustainable composite materials in aircraft production. The European Union's focus on reducing emissions in the aviation industry supports investments in lightweight composites. Additionally, collaborative efforts with research institutions strengthen regional advancements in material technology.

In the Middle East and Africa, the market is influenced by rising investments in aviation infrastructure and defense. Countries like the UAE and Saudi Arabia are expanding their commercial aviation and military capabilities, creating demand for high-strength composite materials. Initiatives to develop domestic aerospace production support market activity, though reliance on imports for advanced materials remains high in this region.

Latin America's market shows steady rise, particularly in Brazil and Mexico, where aerospace manufacturing is gradually expanding. Regional partnerships with international aerospace firms promote the use of advanced composite materials. Government initiatives supporting the domestic aerospace sector also contribute to market activity. However, economic constraints and limited local manufacturing capabilities pose challenges for broader adoption.

Top Key Players & Market Share Insights:

The global aerospace composites market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the aerospace composites market. Key players in the aerospace composites industry include-

- Hexcel Corporation (United States)

- Toray Industries, Inc. (Japan)

- Spirit AeroSystems Holdings, Inc. (United States)

- BASF SE (Germany)

- Gurit Holding AG (Switzerland)

- Solvay S.A. (Belgium)

- Teijin Limited (Japan)

- SGL Carbon SE (Germany)

- Mitsubishi Chemical Holdings Corporation (Japan)

- DuPont de Nemours, Inc. (United States)

Recent Industry Developments :

Mergers and Acquisitions:

- In January 2024, Boeing expanded its presence in Southeast Asia by acquiring Aerospace Composites Malaysia Sdn Bhd from Hexcel Corporation. This move strengthens Boeing's capabilities in the region.

- In May 2024, GracoRoberts acquired Pacific Coast Composites to enhance its product offerings and streamline lead times in the aerospace industry.

Aerospace Composites Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 89,391.036 Million |

| CAGR (2025-2032) | 12.1% |

| By Fiber Type |

|

| By Resin Type |

|

| By Aircraft Type |

|

| By Application |

|

| By Manufacturing Process |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Aerospace Composites Market? +

In 2024, the Aerospace Composites Market was USD 35,847.43 million.

What will be the potential market valuation for the Aerospace Composites Market by 2032? +

In 2032, the market size of the Aerospace Composites Market is expected to reach USD 89,391.36 million.

What are the segments covered in the Aerospace Composites Market report? +

The fiber types, resin types, aircraft types, applications, and manufacturing processes are the segments covered in this report.

Who are the major players in the Aerospace Composites Market? +

Hexcel Corporation (United States), Toray Industries, Inc. (Japan), Solvay S.A. (Belgium), Teijin Limited (Japan), SGL Carbon SE (Germany), Mitsubishi Chemical Holdings Corporation (Japan), DuPont de Nemours, Inc. (United States), Spirit AeroSystems Holdings, Inc. (United States), BASF SE (Germany), Gurit Holding AG (Switzerland) are the major players in the Aerospace Composites market.