- Summary

- Table Of Content

- Methodology

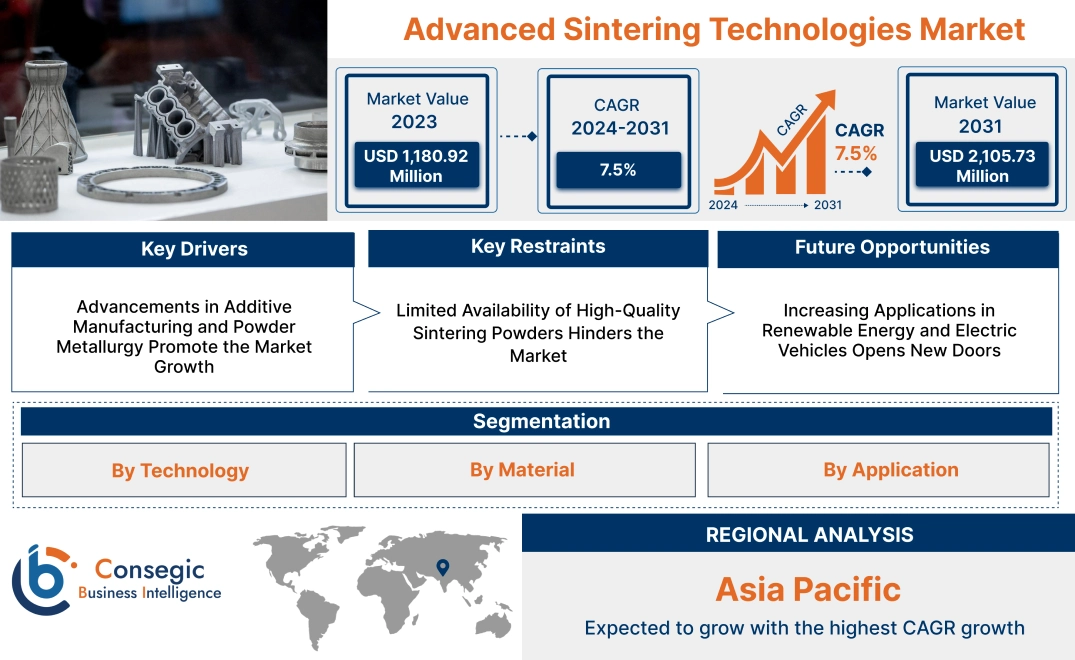

Advanced Sintering Technologies Market Size:

Advanced Sintering Technologies Market size is estimated to reach over USD 2,105.73 Million by 2031 from a value of USD 1,180.92 Million in 2023 and is projected to grow by USD 1,248.42 Million in 2024, growing at a CAGR of 7.5% from 2024 to 2031.

Advanced Sintering Technologies Market Scope & Overview:

Advanced sintering technologies refer to innovative processes that consolidate powder materials into dense, high-performance components without reaching their melting point. These methods employ precise temperature control, optimized pressure conditions, and controlled atmospheres to achieve uniform microstructures and improved mechanical properties. They enable manufacturers to reduce energy consumption, enhance dimensional accuracy, and produce complex shapes with minimal post-processing. Applications span multiple industries, including automotive, aerospace, electronics, medical devices, and cutting tools, where improved strength, durability, and wear resistance are essential. The market focuses on supporting sustainability, cost efficiency, and reliability, aligning with stringent quality standards and environmental regulations. Ongoing research and development activities emphasize new material systems, shorter processing times, and digital integration, allowing broader implementation across value chains. As global demand for advanced materials and precision components rises, advanced sintering technologies remain integral in evolving manufacturing ecosystems.

Advanced Sintering Technologies Market Dynamics - (DRO) :

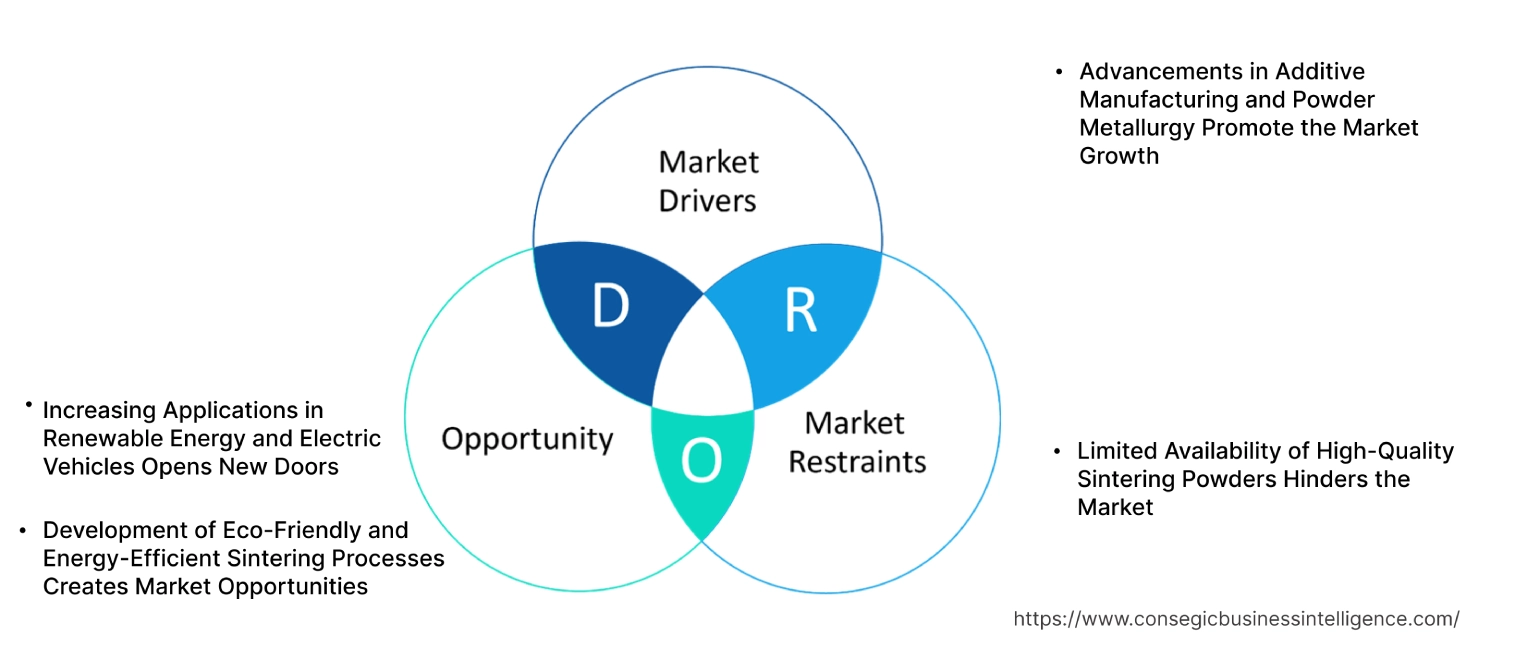

Key Drivers:

Advancements in Additive Manufacturing and Powder Metallurgy Promote the Market Growth

The integration of advanced sintering technologies with additive manufacturing and powder metallurgy is revolutionizing the production of complex, high-precision components. These techniques enable manufacturers to design and produce parts with intricate geometries and enhanced material properties, which were previously unattainable using traditional methods. Processes like spark plasma sintering (SPS) and hot isostatic pressing (HIP) allow faster production cycles, superior density, and improved mechanical performance, making them essential for industries such as aerospace, automotive, and healthcare.

Trends in lightweight materials and rapid prototyping are further driving the adoption of sintering technologies. For instance, the use of sintered components in 3D printing allows the creation of customized parts tailored to specific applications, aligning with industry analysis that emphasizes efficiency and precision. As industries continue to adopt digital manufacturing workflows, the synergy between sintering technologies and additive manufacturing is expected to enhance innovation and competitiveness.

Key Restraints :

Limited Availability of High-Quality Sintering Powders Hinders the Market

The production of high-performance sintered components relies heavily on the availability of uniform, high-quality powders, which are critical for achieving desired material properties. However, the limited supply of these powders poses a significant challenge for manufacturers. Variations in powder quality can lead to inconsistencies in the sintering process, affecting the structural integrity and functionality of the final products.

Additionally, the high costs associated with sourcing and processing sintering powders, coupled with supply chain disruptions, further constrain the scalability of advanced sintering technologies. This issue is particularly pronounced in emerging markets, where access to specialized raw materials remains limited. Addressing these challenges requires innovations in powder production and the development of alternative materials to ensure consistent quality and cost-efficiency.

Future Opportunities :

Increasing Applications in Renewable Energy and Electric Vehicles Opens New Doors

The renewable energy and electric vehicle (EV) sectors are emerging as significant opportunities for advanced sintering technologies. Components such as battery electrodes, fuel cell membranes, and high-performance magnets, which are essential for these industries, benefit from the enhanced properties provided by sintering processes. Sintered parts offer superior thermal and mechanical stability, making them ideal for applications that require reliability and durability in extreme conditions.

Trends in clean energy solutions and electrification highlight the growing importance of advanced sintering technologies in supporting sustainable innovations. For instance, the production of lightweight, energy-efficient components for EVs relies on sintering techniques to achieve precise material properties and design flexibility. As the focus on renewable energy intensifies globally, sintering technologies are poised to play a crucial role in advancing green technologies and infrastructure.

Development of Eco-Friendly and Energy-Efficient Sintering Processes Creates Market Opportunities

The need for sustainable manufacturing practices has spurred innovations in eco-friendly and energy-efficient sintering technologies. Techniques such as low-temperature sintering and advanced heating systems reduce energy consumption and minimize emissions, aligning with global trends favoring environmentally responsible production methods. These advancements not only address environmental concerns but also lower operational costs, making sintering technologies more accessible to a wider range of industries.

Eco-friendly sintering processes also enable compliance with stricter environmental regulations, positioning manufacturers as leaders in sustainable practices. Analysis of sector trends suggests that adopting green sintering technologies will enhance the competitive edge of manufacturers, particularly in sectors like automotive, electronics, and healthcare, where sustainability is becoming a key priority. As industries move toward a circular economy, eco-friendly sintering processes offer a pathway to achieving both environmental and economic goals.

Advanced Sintering Technologies Market Segmental Analysis :

By Technology:

Based on technology, the market is segmented into spark plasma sintering (SPS), microwave sintering, pressureless sintering, hot isostatic pressing (HIP), and others.

The spark plasma sintering (SPS) segment accounted for the largest revenue advanced sintering technologies market share in 2023.

- Spark plasma sintering (SPS) is widely adopted for its ability to produce high-density materials with enhanced mechanical and thermal properties in a significantly shorter timeframe.

- SPS technology is extensively used in aerospace, defense, and electronics industries due to its precision and effectiveness in processing advanced ceramics, metals, and composites.

- Additionally, SPS allows the sintering of materials at lower temperatures, minimizing grain growth and enhancing the final product’s performance.

- The growing demand for high-performance materials in critical applications drives the dominance of this segment.

- SPS leads the market due to its efficiency, precision, and widespread use in producing high-performance materials for the aerospace, defense, and electronics industries.

The microwave sintering segment is anticipated to register the fastest CAGR during the forecast period.

- Microwave sintering is gaining popularity due to its energy efficiency and ability to provide uniform heating, resulting in superior material properties.

- This technology is particularly suited for processing ceramics and composites, making it ideal for applications in healthcare, electronics, and energy sectors.

- The increasing focus on sustainable manufacturing practices and the need to reduce energy consumption in industrial processes are key drivers for the growth of microwave sintering.

- Microwave sintering is expected to grow rapidly due to its energy efficiency, sustainability, and increasing adoption in advanced material processing.

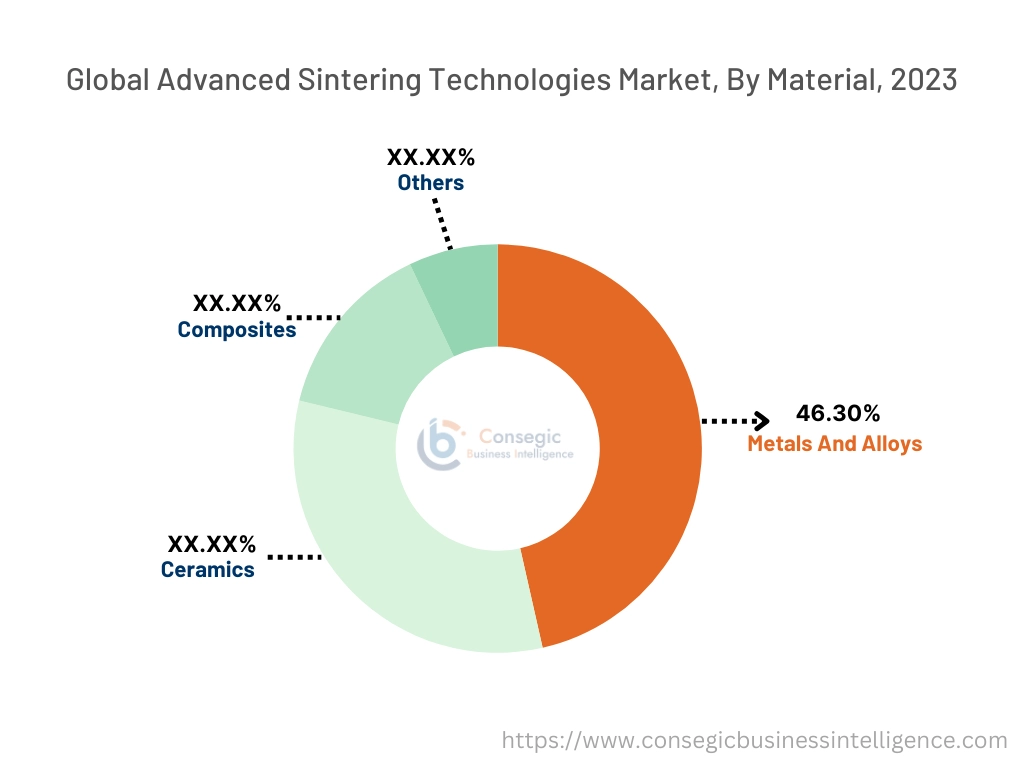

By Material:

Based on material, the market is segmented into metals and alloys, ceramics, composites, and others.

The metals and alloys segment accounted for the largest revenue of 46.30% in advanced sintering technologies market share in 2023.

- Metals and alloys are the most commonly sintered materials due to their extensive use in automotive, aerospace, and industrial applications.

- Sintered metals and alloys offer excellent mechanical strength, thermal stability, and wear resistance, making them essential for manufacturing components such as gears, engine parts, and electronic connectors.

- The increasing surge for lightweight and durable materials in the automotive and aerospace industries further supports the growth of this segment.

- Metals and alloys dominate the advanced sintering technologies market trends, driven by their versatility and extensive use in producing high-performance components for automotive and aerospace applications.

The ceramics segment is anticipated to register the fastest CAGR during the forecast period.

- Ceramics are increasingly used in advanced applications due to their superior hardness, corrosion resistance, and thermal stability.

- The growing advanced sintering technologies market demand for advanced ceramics in electronics, medical devices, and renewable energy systems is driving the growth of this segment.

- Innovations in sintering technologies, such as SPS and microwave sintering, are further propelling the adoption of ceramics in complex and high-precision applications.

- Ceramics analysis is expected to grow rapidly, driven by increasing development for advanced applications in electronics, healthcare, and renewable energy sectors.

By Application:

Based on application, the market is segmented into automotive, aerospace and defense, electronics, healthcare, energy, and others.

The aerospace and defense segment accounted for the largest revenue share in 2023.

- The aerospace and defense sectors rely heavily on advanced sintering technologies to produce lightweight, high-strength components that can withstand extreme conditions.

- Sintered materials, including advanced ceramics and alloys, are used in manufacturing turbine blades, heat shields, and structural components.

- The increasing opportunities for fuel-efficient aircraft and advancements in defense technologies trends drive the dominance of this segment.

- Aerospace and defense dominate the market due to the critical need for high-performance materials in fuel-efficient and advanced defense systems.

The electronics segment is anticipated to register the fastest CAGR during the forecast period.

- Advanced sintering technologies are extensively used in the electronics sector for producing components such as capacitors, semiconductors, and resistors.

- The growing trend of miniaturization in electronic devices and the increasing demand for high-performance materials with superior electrical properties are key drivers for this segment.

- Additionally, the rapid growth of the semiconductor industry and consumer electronics market further propels the adoption of sintering technologies in this sector.

- Electronics are expected to grow rapidly, driven by increasing advanced sintering technologies market opportunities for miniaturized and high-performance components in semiconductors and consumer electronics.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

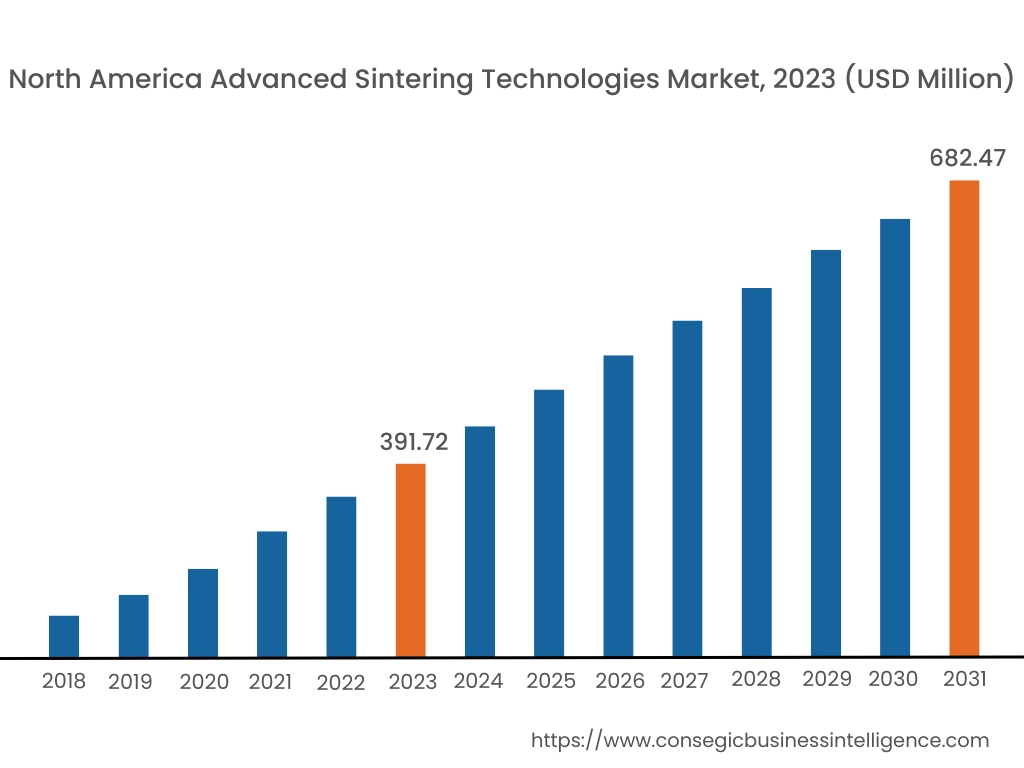

In 2023, North America was valued at USD 391.72 Million and is expected to reach USD 682.47 Million in 2031. In North America, the U.S. accounted for the highest share of 74.80% during the base year of 2023. North America holds a significant share in the advanced sintering technologies market analysis, driven by its well-developed automotive, aerospace, and defense industries. The U.S. leads the region with increasing adoption of advanced sintering techniques such as spark plasma sintering (SPS) and hot isostatic pressing (HIP) for manufacturing high-performance materials. These technologies are widely used in producing lightweight components for aircraft and automotive applications. Canada contributes through advancements in powder metallurgy and sintering processes for electronics and industrial equipment. However, high costs associated with advanced sintering equipment and materials may limit adoption in smaller industries.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.9% over the forecast period. Asia-Pacific is the largest and fastest-growing region in the advanced sintering technologies market expansion, fueled by the trends of rapid industrialization, urbanization, and expansion of the electronics and automotive industries in China, Japan, and South Korea. China leads the market with extensive use of advanced sintering in automotive parts, electronics, and industrial machinery. Japan’s focus on high-precision components for electronics and medical devices drives the adoption of sintering technologies like SPS and microwave sintering. South Korea emphasizes the use of sintering in semiconductor manufacturing and renewable energy applications. However, high initial investment costs and limited technical expertise in some regions may impact the adoption of advanced sintering technologies.

Europe is a key market for advanced sintering technologies, supported by strong demand from the automotive, electronics, and energy sectors. Countries like Germany, France, and the UK are major contributors. Germany’s automotive and industrial manufacturing sectors drive the use of sintering technologies for producing high-strength and wear-resistant components. France focuses on advanced sintering for aerospace and nuclear applications, while the UK is leveraging these technologies in renewable energy systems and precision electronics. However, compliance with stringent environmental regulations and high energy consumption in sintering processes may pose challenges for manufacturers.

The Middle East & Africa region is witnessing steady growth in the advanced sintering technologies market analysis, driven by increasing investments in industrial and energy sectors. Saudi Arabia and the UAE are adopting advanced sintering processes for manufacturing components used in oil and gas, aerospace, and defense applications. In Africa, South Africa is an emerging market, leveraging sintering technologies in mining equipment and industrial machinery. However, limited local production capabilities and dependence on imports for advanced sintering equipment and materials may restrict market expansion in certain areas.

Latin America is an emerging market for advanced sintering technologies, with Brazil and Mexico leading the region. Brazil’s growing automotive and aerospace sectors drive the adoption of sintering technologies for producing lightweight and durable components. Mexico, with its expanding electronics and manufacturing industries, uses sintering processes to produce high-performance parts for export markets. The region is also exploring the application of advanced sintering in renewable energy systems and industrial tools. However, economic instability and limited infrastructure for high-end manufacturing may pose challenges to broader adoption.

Top Key Players and Market Share Insights:

The Advanced Sintering Technologies market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Advanced Sintering Technologies market. Key players in the Advanced Sintering Technologies industry include -

- ALD Vacuum Technologies (Germany)

- Linn High Therm (Germany)

- Shanghai Gehang Vacuum Technology Co. (China)

- Nabertherm GmbH (Germany)

- Carbolite Gero Ltd. (UK)

- Sumitomo Heavy Industries Ltd. (Japan)

- BTU International (USA)

- FCT Systeme (Germany)

- EOS GmbH (Germany)

- ChinaSavvy (China)

Recent Industry Developments :

- In October 2024, 3Dnatives and Desktop Metal introduced the PureSinter Furnace, a debit and sintering vacuum furnace designed to address common challenges in powder metal sintering, such as contamination and high maintenance costs. The PureSinter Furnace offers high-temperature capabilities of up to 1,420°C and rapid cooling for faster sintering cycles, aiming to enhance efficiency and reduce operational costs in both additive and traditional manufacturing processes.

Advanced Sintering Technologies Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 2,105.73 Million |

| CAGR (2024-2031) | 7.5% |

| By Technology |

|

| By Material |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size of the Advanced Sintering Technologies Market by 2031? +

Advanced Sintering Technologies Market size is estimated to reach over USD 2,105.73 Million by 2031 from a value of USD 1,180.92 Million in 2023 and is projected to grow by USD 1,248.42 Million in 2024, growing at a CAGR of 7.5% from 2024 to 2031.

What drives the demand for advanced sintering technologies in the automotive and aerospace industries? +

The increasing need for lightweight, high-strength components with superior thermal and wear resistance drives the adoption of advanced sintering technologies in the automotive and aerospace sectors. These technologies enhance material properties and improve component performance.

Which material segment dominates the Advanced Sintering Technologies Market? +

The metals and alloys segment holds the largest revenue share due to its extensive use in automotive, aerospace, and industrial applications. Their mechanical strength and versatility make them indispensable in producing high-performance components.

What are the major challenges faced by the Advanced Sintering Technologies Market? +

High costs associated with advanced sintering equipment, materials, and energy-intensive processes are significant challenges. Additionally, limited technical expertise in some regions can hinder adoption.

Which application segment contributes the most to the market? +

The aerospace and defense segment dominates the market, leveraging advanced sintering technologies to produce lightweight, high-strength components such as turbine blades and heat shields for fuel-efficient aircraft and advanced defense systems.