- Summary

- Table Of Content

- Methodology

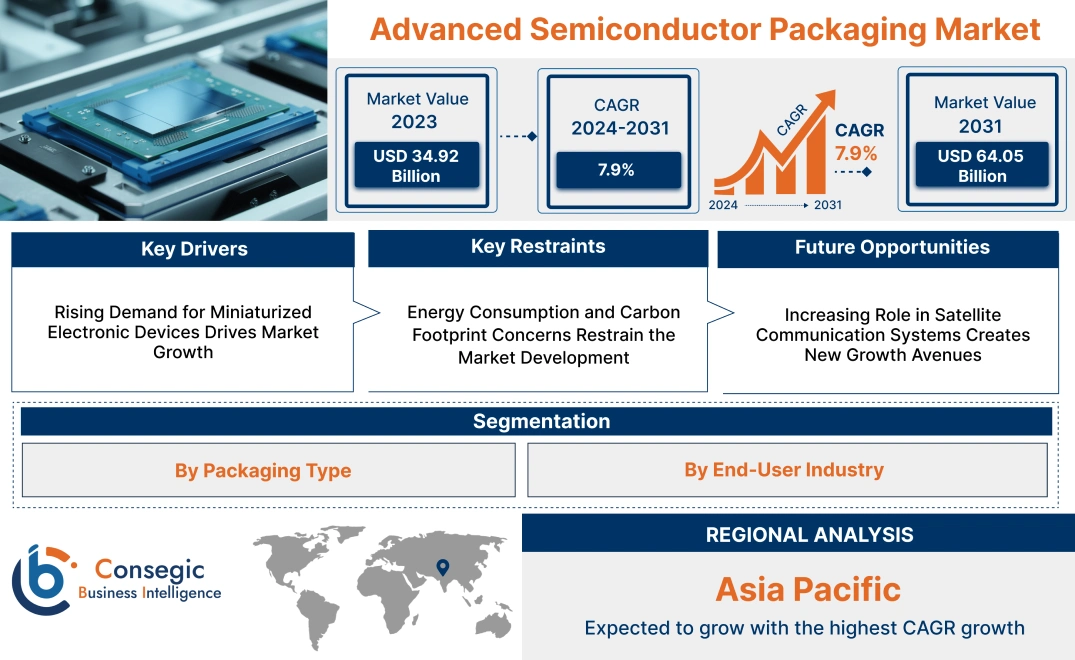

Advanced Semiconductor Packaging Market Size:

Advanced Semiconductor Packaging Market size is estimated to reach over USD 64.05 Billion by 2031 from a value of USD 34.92 Billion in 2023 and is projected to grow by USD 37.05 Billion in 2024, growing at a CAGR of 7.9% from 2024 to 2031.

Advanced Semiconductor Packaging Market Scope & Overview:

Advanced semiconductor packaging is a modern approach to enclosing semiconductor devices, improving their performance, functionality, and integration. Techniques like 2.5D packaging, 3D packaging, fan-out packaging, and system-in-package (SiP) are used to meet the growing needs of complex applications. These solutions focus on providing better electrical connections, managing heat effectively, and saving space, making them ideal for high-performance and compact devices.

This technology is widely used in industries such as electronics, telecommunications, automotive, and industrial automation, ensuring reliable and efficient operation. It supports higher chip densities, better heat management, and improved signal quality, meeting the needs of fast and energy-efficient devices. Advanced materials and connection methods also make these solutions compatible with new chip designs.

End-users, including semiconductor manufacturers, electronics companies, and IoT device developers, depend on advanced packaging to improve device performance and support next-generation technologies. This packaging approach plays a key role in enabling innovation and advancing technology across various industries.

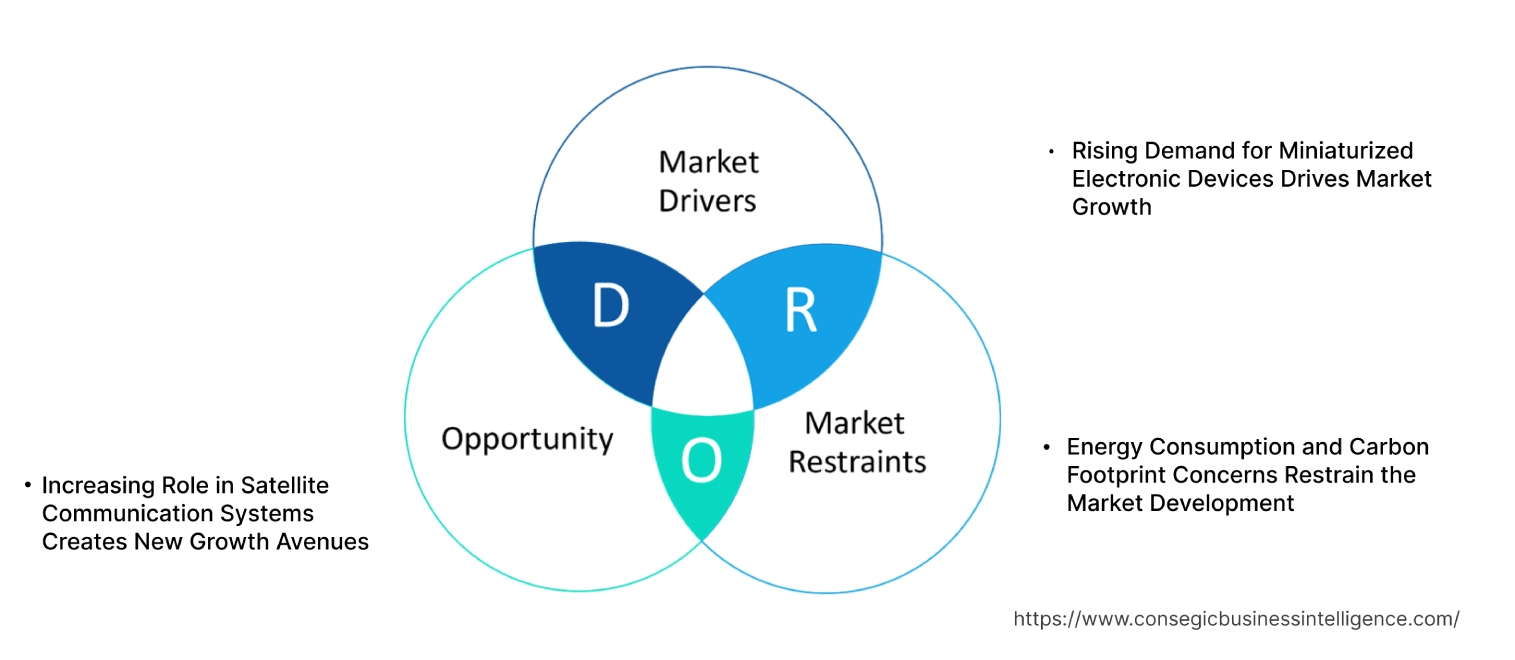

Advanced Semiconductor Packaging MarketDynamics - (DRO) :

Key Drivers:

Rising Demand for Miniaturized Electronic Devices Drives Market Growth

The growing adoption of miniaturized electronic devices, including wearables, IoT sensors, and compact consumer electronics, is significantly driving the need for advanced packaging solutions. These devices demand high performance, energy efficiency, and multifunctionality within smaller form factors, making traditional packaging methods insufficient. Advanced packaging technologies, such as system-in-package (SiP) and wafer-level packaging, enable the integration of multiple components, including processors, memory, and sensors, into a single compact package.

This integration not only reduces the size of the devices but also enhances their reliability and performance, meeting the stringent requirements of miniaturized designs. Industries such as healthcare, where portable medical devices are increasingly used, and consumer electronics, where portability and aesthetics are key, are fueling this need. As trends in device miniaturization and smart connectivity expand, advanced packaging has become a critical enabler for innovation in next-generation electronics, driving advanced semiconductor packaging market growth across various sectors.

Key Restraints :

Energy Consumption and Carbon Footprint Concerns Restrain the Market Development

Semiconductor packaging processes, such as lithography, etching, and bonding, are highly energy-intensive, contributing significantly to operational costs and environmental impact. The extensive use of power during these processes raises concerns about carbon emissions, particularly as industries increasingly face regulatory pressures and sustainability targets. Meeting these requirements often requires manufacturers to adopt eco-friendly practices, such as using renewable energy sources, optimizing production workflows, and investing in energy-efficient equipment.

However, these sustainability measures come with higher upfront costs, adding financial burdens for manufacturers, especially smaller players. Additionally, transitioning to greener operations may involve disruptions to existing workflows, further complicating scalability. This dual constraint of maintaining cost-efficiency while adhering to stringent environmental regulations creates barriers for manufacturers, slowing the adoption of advanced packaging technologies in an increasingly eco-conscious market. Balancing these demands remains a critical restraint for the sector, hampering advanced semiconductor packaging market demand.

Future Opportunities :

Increasing Role in Satellite Communication Systems Creates New Growth Avenues

Advanced semiconductor packaging solutions are playing an increasingly vital role in satellite communication systems, where performance, reliability, and durability under extreme environmental conditions are non-negotiable. Satellites, especially low-earth orbit (LEO) constellations, require components that withstand intense vibrations during launch, extreme temperature fluctuations in space, and high radiation levels. Advanced packaging techniques, such as hermetic sealing and radiation-hardened designs, ensure that semiconductor components meet these rigorous requirements.

The global push for satellite-based internet services, including initiatives like Starlink and OneWeb, is driving demand for reliable and efficient packaging solutions. These constellations rely on compact and high-performance semiconductors for signal processing, data transmission, and power management. Advanced packaging not only enhances the functionality of these systems but also supports lightweight designs crucial for space applications. As per the market trends analysis, as the satellite communication networks expand, robust semiconductor packaging solutions tailored for space will experience significant advanced semiconductor packaging market opportunities.

Advanced Semiconductor Packaging Market Segmental Analysis :

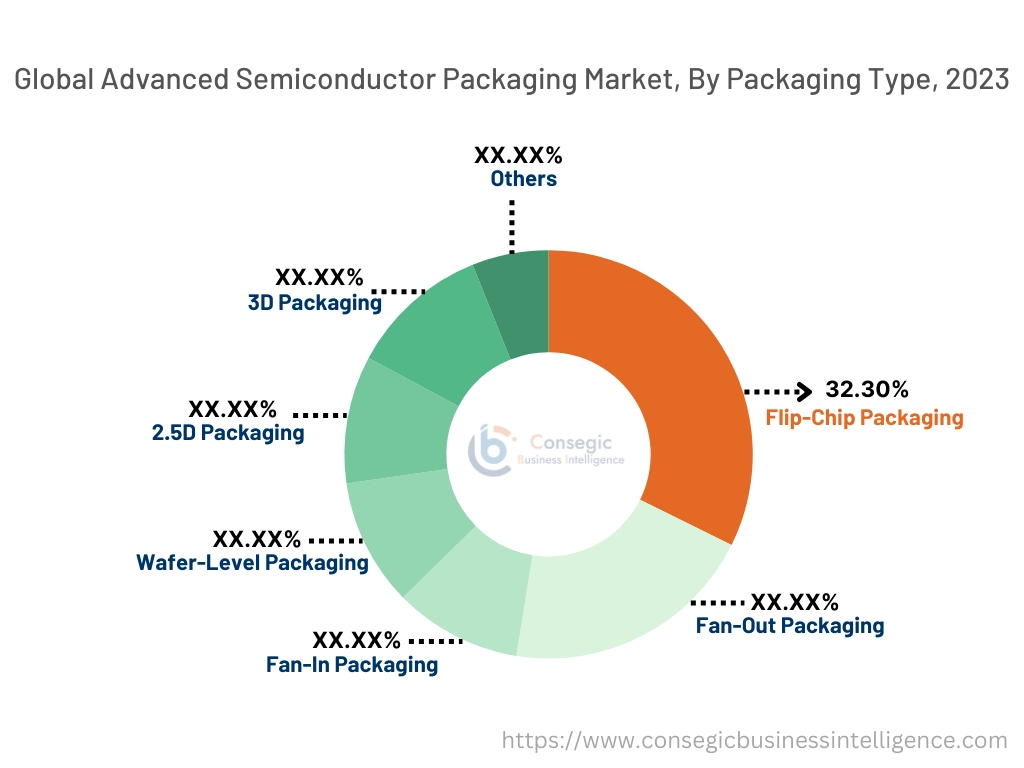

By Packaging Type:

Based on packaging type, the market is segmented into Flip-Chip Packaging, Fan-Out Packaging, Fan-In Packaging, Wafer-Level Packaging, 2.5D Packaging, 3D Packaging, and Others.

The flip-chip packaging segment held the largest revenue of 32.30% of the total advanced semiconductor packaging market share in 2023.

- Flip-chip technology offers superior electrical and thermal performance by enabling direct die-to-substrate connections, ensuring high reliability for advanced applications.

- Widely utilized in processors, GPUs, and memory modules, this packaging type supports high-performance applications across electronics and telecommunications.

- The growth in adoption of flip-chip packaging is driven by increasing complexity in semiconductor designs, especially in consumer electronics and automotive sectors.

- As per advanced semiconductor packaging market analysis, continuous advancements in flip-chip materials and techniques, such as copper pillars and underfill compounds, are further enhancing its performance and adoption.

The 3D packaging segment is expected to grow at the fastest CAGR during the forecast period.

- 3D packaging facilitates vertical stacking of chips, improving integration density while reducing power consumption, making it suitable for data-intensive applications.

- Industries like IT & telecom and data centers are increasingly adopting 3D packaging for enhanced performance and compact device designs.

- Through-Silicon Via (TSV) technology plays a key role in enabling efficient interconnectivity, which is critical for high-performance computing systems.

- The segmental trends analysis shows the increasing investments in advanced packaging technologies to cater to high-performance computing and artificial intelligence needs, fueling the advanced semiconductor packaging market expansion.

By End-User Industry:

Based on the end-user industry, the market is segmented into Electronics & Semiconductors, Automotive, Healthcare, IT & Telecom, Aerospace & Defense, and Others.

The electronics & semiconductors segment accounted for the largest revenue of the total advanced semiconductor packaging market share in 2023.

- Advanced semiconductor packaging is critical for enabling miniaturization in consumer devices such as smartphones, tablets, and wearables.

- Packaging solutions like wafer-level and flip-chip packaging are widely used in memory modules and processors to achieve high thermal efficiency and power performance.

- The growth in the need for compact and high-performance devices is driving the integration of advanced packaging technologies in consumer electronics.

- As per advanced semiconductor packaging market trends, the dominance of this segment reflects the increasing importance of packaging in enhancing the functionality and efficiency of modern electronic devices.

The IT & telecom segment is expected to grow at the fastest CAGR during the forecast period.

- Advanced packaging technologies, including fan-out and 3D packaging, are essential for enabling high-speed data processing and low latency in telecommunications equipment.

- The ongoing rollout of 5G networks is driving the adoption of semiconductor packaging solutions that support higher data rates and advanced network capabilities.

- Packaging solutions in this segment are focused on improving the performance and scalability of data centers and networking infrastructure.

- The analysis of segmental trends depicts that increasing investments in telecommunication systems and the rising reliance on high-performance computing platforms are driving advanced semiconductor packaging market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

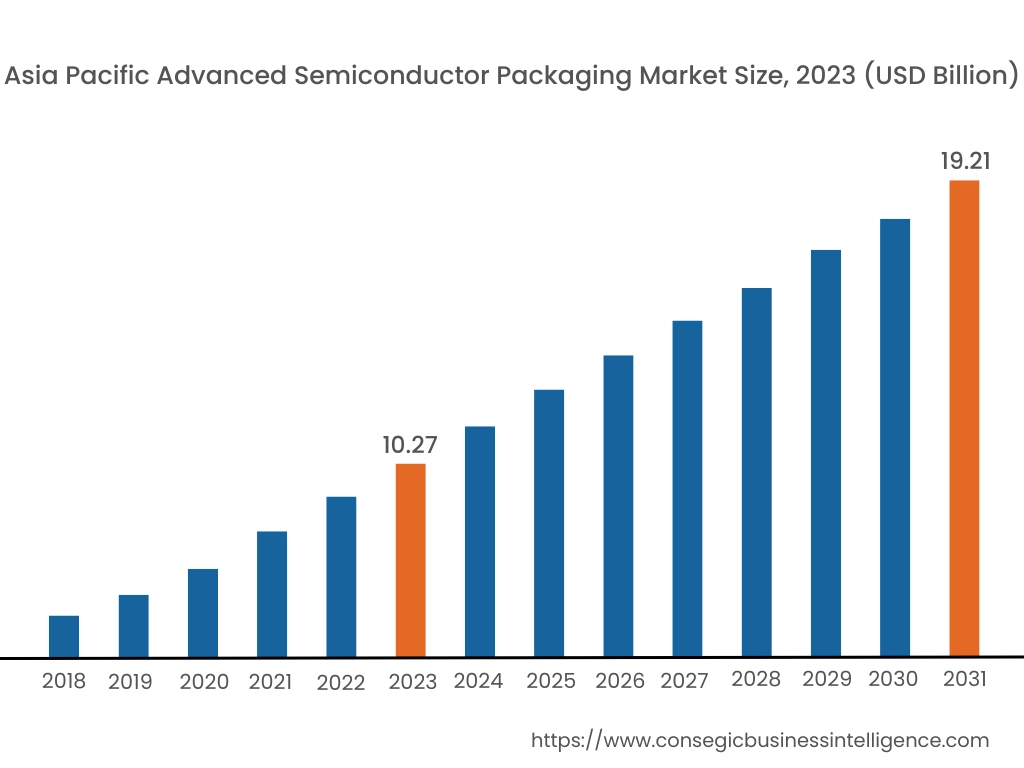

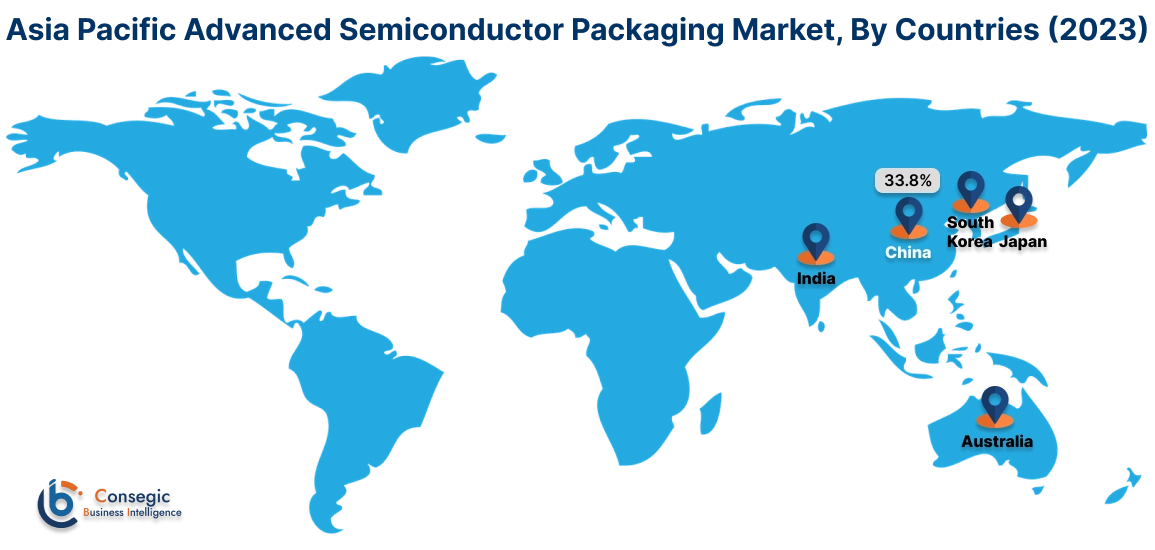

Asia Pacific region was valued at USD 10.27 Billion in 2023. Moreover, it is projected to grow by USD 10.92 Billion in 2024 and reach over USD 19.21 Billion by 2031. Out of these, China accounted for the largest share of 33.8% in 2023. The Asia-Pacific region is experiencing rapid growth in the advanced semiconductor packaging market, propelled by industrialization and technological advancements in countries like China, Japan, and South Korea. The region has become a global hub for electronics manufacturing, where advanced packaging technologies are extensively used to meet the increasing need for consumer electronics and automotive applications. Government initiatives promoting industrial automation and smart manufacturing further influence advanced semiconductor packaging market demand.

North America is estimated to reach over USD 21.07 Billion by 2031 from a value of USD 11.61 Billion in 2023 and is projected to grow by USD 12.30 Billion in 2024. As per advanced semiconductor packaging market analysis, this region stands as a significant player, driven by the robust need for high-performance computing and data centers. The United States, in particular, has seen substantial investments in semiconductor packaging technologies to support innovations in artificial intelligence (AI), 5G, and Internet of Things (IoT) applications.

Europe holds a substantial share of the global advanced semiconductor packaging market, with countries like Germany, France, and the United Kingdom leading in technological advancements. The region's strong manufacturing base, particularly in the automotive and aerospace sectors, drives the adoption of advanced packaging solutions. The advanced semiconductor packaging market trends indicate a growing trend toward integrating advanced packaging technologies to enhance device performance and miniaturization.

The Middle East & Africa region shows a growing interest in advanced semiconductor packaging, particularly in the telecommunications and automotive sectors. Countries like the United Arab Emirates and Saudi Arabia are investing in advanced technologies to support their economic diversification efforts. The analysis suggests an increasing trend towards adopting advanced packaging solutions to enhance the performance and reliability of electronic devices further boosting advanced semiconductor packaging market expansion.

Latin America is an emerging market for advanced semiconductor packaging, with Brazil and Mexico being key contributors. The region's expanding automotive and manufacturing sectors are adopting advanced packaging technologies to improve the performance and efficiency of electronic components. Government policies aimed at industrial modernization and technological innovation create significant advanced semiconductor packaging market opportunities.

Top Key Players & Market Share Insights:

The Advanced Semiconductor Packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Advanced Semiconductor Packaging market. Key players in the Advanced Semiconductor Packaging industry include –

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Advanced Semiconductor Engineering, Inc. (ASE Group) (Taiwan)

- Amkor Technology, Inc. (USA)

- Intel Corporation (USA)

- Samsung Electronics Co., Ltd. (South Korea)

- JCET Group Co., Ltd. (China)

- Siliconware Precision Industries Co., Ltd. (SPIL) (Taiwan)

- Powertech Technology Inc. (PTI) (Taiwan)

- STATS ChipPAC Ltd. (Singapore)

- Unimicron Technology Corporation (Taiwan)

Recent Industry Developments :

Product Launches:

- In In October 2024, KLA introduced a comprehensive portfolio of process control and enabling solutions for IC substrate manufacturing, supporting the growing demand for advanced semiconductor packaging. The portfolio includes Corus and Serena direct imaging platforms, as well as Lumina inspection and metrology systems, designed to improve accuracy, yield, and efficiency in IC substrate production. These innovations cater to high-performance applications by enabling advanced packaging methods, heterogeneous integration, and improved interconnect density, with a focus on next-gen materials like glass.

Partnerships & Collaborations:

- In September 2023, Scrona AG and Electroninks announced a collaboration to develop advanced semiconductor packaging solutions. Scrona, known for its MEMS-based electrohydrodynamic (EHD) multi-nozzle printheads, will partner with Electroninks, a leader in metal-organic decomposition (MOD) inks. The partnership focuses on optimizing the use of Electroninks' materials with Scrona’s technology for applications like RDL repair and fine-line metallization. Joint R&D efforts will take place in Scrona’s Zürich lab and a Taiwan center. This collaboration aims to accelerate innovations in device miniaturization and semiconductor packaging.

Investments & Funding:

- In November 2024, The Biden-Harris Administration announced up to $300 Billion in funding to support U.S. semiconductor packaging under the CHIPS for America program. This initiative aims to enhance the nation's semiconductor supply chain, focusing on the advanced packaging industry, crucial for high-performance chips. The funding will boost innovation in packaging technologies, strengthening the U.S. position in the global semiconductor market. This initiative also supports workforce development and aims to build a more resilient, competitive domestic semiconductor industry.

Advanced Semiconductor Packaging Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 64.05 Billion |

| CAGR (2024-2031) | 7.9% |

| By Packaging Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Advanced Semiconductor Packaging Market? +

Advanced Semiconductor Packaging Market size is estimated to reach over USD 64.05 Billion by 2031 from a value of USD 34.92 Billion in 2023 and is projected to grow by USD 37.05 Billion in 2024, growing at a CAGR of 7.9% from 2024 to 2031.

What specific segmentation details are covered in the Advanced Semiconductor Packaging Market report? +

The Advanced Semiconductor Packaging Market report includes segmentation details by packaging type (Flip-Chip Packaging, Fan-Out Packaging, Fan-In Packaging, Wafer-Level Packaging, 2.5D Packaging, 3D Packaging, Others), end-user industry (Electronics & Semiconductors, Automotive, Healthcare, IT & Telecom, Aerospace & Defense, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Advanced Semiconductor Packaging Market? +

The 3D Packaging segment is expected to grow at the fastest CAGR during the forecast period. This packaging technique allows for vertical stacking of chips, improving integration density while reducing power consumption, and is increasingly adopted in industries like IT & telecom and data centers for data-intensive applications.

Who are the major players in the Advanced Semiconductor Packaging Market? +

The major players in the Advanced Semiconductor Packaging Market include Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan), Advanced Semiconductor Engineering, Inc. (ASE Group) (Taiwan), Amkor Technology, Inc. (USA), Intel Corporation (USA), Samsung Electronics Co., Ltd. (South Korea), JCET Group Co., Ltd. (China), Siliconware Precision Industries Co., Ltd. (SPIL) (Taiwan), Powertech Technology Inc. (PTI) (Taiwan), STATS ChipPAC Ltd. (Singapore), and Unimicron Technology Corporation (Taiwan).