- Summary

- Table Of Content

- Methodology

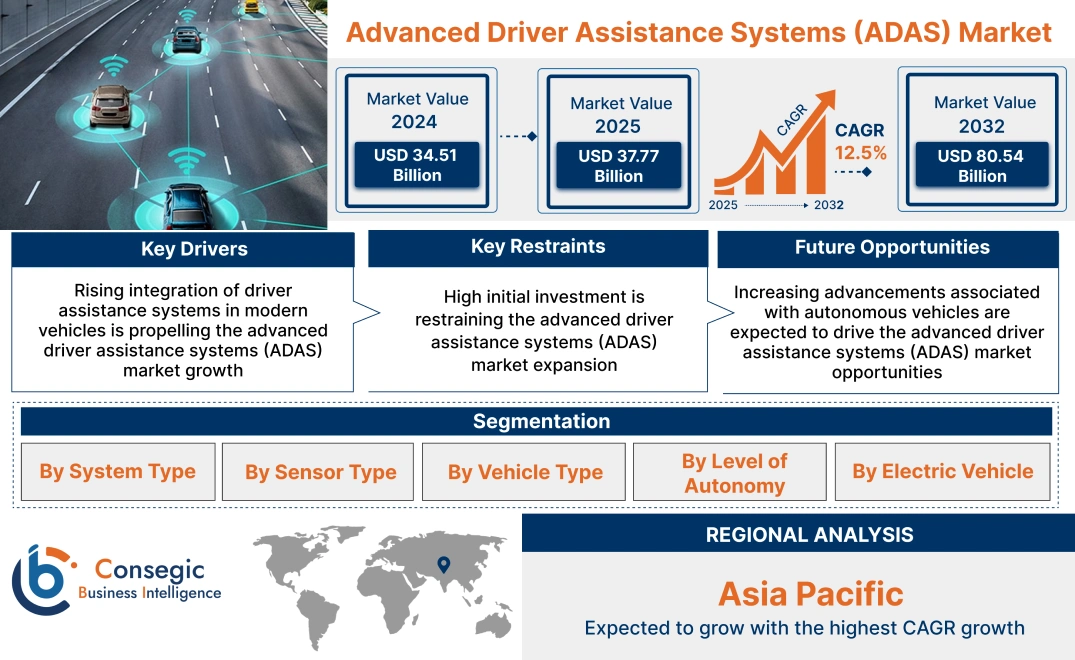

Advanced Driver Assistance Systems (ADAS) Market Size:

Advanced Driver Assistance Systems (ADAS) Market size is estimated to reach over USD 80.54 Billion by 2032 from a value of USD 34.51 Billion in 2024 and is projected to grow by USD 37.77 Billion in 2025, growing at a CAGR of 12.5% from 2025 to 2032.

Advanced Driver Assistance Systems (ADAS) Market Scope & Overview:

Advanced driver assistance systems (ADAS) refer to electronic technologies used in vehicles for assisting drivers in safe operations of automobiles while improving vehicle safety and driving experience. ADAS primarily uses sensors and cameras to assist the driver with routine operations such as assistance in parking, pedestrian detection, lane departure warning, blind-spot detection, and others. Moreover, the integration of ADAS in vehicles offer several benefits such as improved safety, enhanced driving experience, reduced traffic accidents, and others. The above benefits of advanced driver assistance systems (ADAS) are primary determinants for increasing its utilization in passenger cars and commercial vehicles.

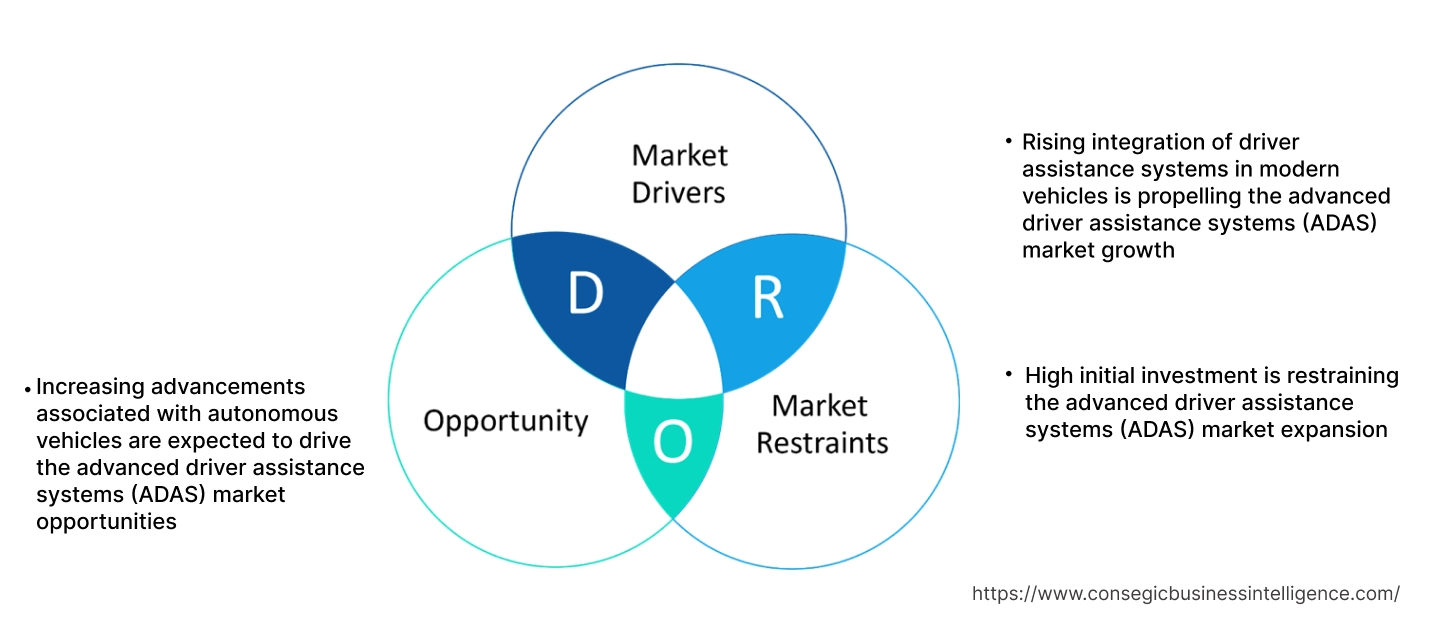

Advanced Driver Assistance Systems (ADAS) Market Dynamics - (DRO) :

Key Drivers:

Rising integration of driver assistance systems in modern vehicles is propelling the advanced driver assistance systems (ADAS) market growth

Advanced driver-assistance systems are primarily integrated in modern vehicles for assisting drivers with safe operation of a vehicle. Advanced driver-assistance system utilizes automated technology involving sensors and cameras for detecting nearby obstacles or driver errors, and responding accordingly to avoid an accident. Moreover, the integration of advanced driver assistance systems in modern vehicles facilitate several vehicle functionalities such as adaptive cruise control, intelligent park assistance, rollover stability control, lane departure warning, blind spot detection, and automatic emergency braking among others. Additionally, governments worldwide are introducing favorable initiatives and regulations for installation of ADAS in modern vehicles, which is further driving the market.

- For instance, in April 2022, Honda Cars India Limited launched its new hybrid electric vehicle, Honda City eHEV. The Honda City eHEV is integrated with ADAS technology that provides an enhanced driving experience. The ADAS system enables several features such as adaptive cruise control, lane keep assist, road departure warning, auto high beam control, and collision mitigation braking system.

Therefore, as per the analysis, the rising integration of driver assistance system in modern vehicles is proliferating the advanced driver assistance systems (ADAS) market size.

Key Restraints:

High initial investment is restraining the advanced driver assistance systems (ADAS) market expansion

High initial investment associated with the integration of advanced driver assistance systems is among the primary factors restraining the market. The upfront costs associated with manufacturing advanced driver assistance systems including costs of hardware components, software, and others along with integration of systems into vehicles can be significantly high, which may cause financial barriers, particularly for smaller businesses or businesses operating on tighter budgets.

Additionally, advanced driver assistance systems may require frequent maintenance or repair, which can be more challenging for non-technical individuals or small-scale businesses. Advanced driver assistance systems often require the attention of specialized technicians to fix them, which could lead to increased costs and vehicle downtime. Hence, high initial investments associated with the deployment of driver assistance systems are restraining the advanced driver assistance systems (ADAS) market.

Future Opportunities :

Increasing advancements associated with autonomous vehicles are expected to drive the advanced driver assistance systems (ADAS) market opportunities

Autonomous vehicles are gaining significant popularity since recent years, attributing to its ability to facilitate safer commuting, enhance driving experience, and improve traffic flow among others. Moreover, advanced driver-assistance system plays a critical role modern autonomous vehicle in assisting drivers with safe operation of the vehicle. The integration of ADAS in autonomous vehicles assist in avoiding collisions, offer adaptive cruise control, assist in lane centering, alert lane departure, provide navigational assistance, automate lighting, and offer several other features. As a result, the increasing advancements associated with autonomous vehicles are providing lucrative aspects for market development.

- For instance, in July 2023, Volkswagen Group commenced its first autonomous vehicle test program in Austin, United States. The program includes the rollout of a batch of 10 all-electric Buzz vehicles integrated with an autonomous driving technology platform. Volkswagen Group also intends to increase its test fleet in Austin and expand its testing operations to four more cities in the U.S. Additionally, the company plans to launch its autonomous driving vehicles in Austin by 2026.

Hence, as per the analysis, the increasing advancements associated with autonomous vehicles are projected to increase the integration of ADAS in autonomous vehicles. The above factors are expected to boost the advanced driver assistance systems (ADAS) market opportunities during the forecast period.

Advanced Driver Assistance Systems (ADAS) Market Segmental Analysis :

By System Type:

Based on system type, the market is segmented into tire pressure monitoring system (TPMS), road sign recognition (RSR), night vision system (NVS), lane departure warning (LDW), intelligent park assist (IPA), forward collision warning (FCW), driver monitoring system (DMS), cross traffic alert (CTA), blind spot detection (BSD), automatic emergency braking (AEB), adaptive front light (AFL), adaptive cruise control (ACC), and others.

Trends in the system type:

- Rising advancements associated with blind spot detection system for reducing the risk of accidents during lane changes by monitoring the dangerous blind spot area and improving vehicle safety.

- There is a rising trend towards the integration of adaptive cruise control system in modern vehicles to facilitate improved speed control, lower chances of collisions, and improved comfort while driving among others.

The adaptive cruise control (ACC) segment accounted for a significant revenue in the overall market in 2024.

- Adaptive cruise control refers to a type of advanced driver-assistance system for road vehicles that is capable of automatically adjusting the vehicle's speed to maintain a safe distance from vehicles ahead.

- Adaptive cruise control enables users to relax while driving, particularly on highways, by automatically adjusting the car’s speed by matching the speed of the vehicles in front.

- Moreover, ACC offers several benefits such as improved speed control, lower chances of collisions, improved comfort while driving, and others.

- For instance, Robert Bosch offers adaptive cruise control (ACC) solutions in its product offerings. The ACC solutions is designed for integration in passenger cars.

- According to the advanced driver assistance systems (ADAS) market analysis, rising advancements associated with adaptive cruise control (ACC) solutions are driving the advanced driver assistance systems (ADAS) market size.

The blind spot detection (BSD) segment is anticipated to register a substantial CAGR growth during the forecast period.

- A blind spot detection system includes a vehicle-based sensor device that is capable of detecting other vehicles to the side and rear of the driver. The warning may be audible, visual, vibrating, or tactile.

- Moreover, blind spot detection system helps in reducing the risk of accidents during lane changes by monitoring the dangerous blind spot area.

- For instance, in October 2023, Sensata Technologies launched its new PreView Sentry 79 model of take-off and reverse blind spot monitoring radar. The blind spot monitoring radar is developed to set a new standard for blind spot detection and collision avoidance in the automotive sector.

- Therefore, increasing advancements associated with automotive blind spot detection solutions are anticipated to propel the market during the forecast period.

By Sensor Type:

Based on sensor type, the market is segmented into ultrasonic sensors, radar sensors, LiDAR, laser sensors, infrared (IR) sensors, and image sensors.

Trends in the sensor type:

- Rising integration of image sensors in advanced driver-assistance systems for applications such as object detection, lane departure warning, and pedestrian recognition among others.

- Increasing advancements associated with radar sensors for facilitating ADAS functionalities such as adaptive cruise control, automatic emergency braking, cross-traffic alert, and blind spot monitoring among others.

The image sensors segment accounted for a substantial revenue share in the total advanced driver assistance systems (ADAS) market share in 2024.

- Image sensors are primarily used in the automotive industry for enhanced driving assistance, car safety, and driving comfort.

- Image sensors are mainly integrated in advanced driver-assistance systems for applications such as object detection, lane departure warning, and pedestrian recognition among others.

- Moreover, image sensors are a vital part of advanced driver assistance system as it provides high-resolution pictures that computer vision algorithms interpret and prevent crashes by utilizing these algorithms for identification of individuals, obstructions, and other vehicles on the route.

- For instance, in October 2024, OMNIVISION launched its new OX12A10 model of CMOS image sensor. The new sensor improves automotive safety by providing enhanced resolution and image quality and it is ideal for use in vision cameras for advanced driver assistance systems (ADAS) and autonomous driving applications among others.

- Therefore, the rising innovations related to image sensors for use in ADAS applications are driving the market.

Radar sensors segment is anticipated to register significant CAGR growth during the forecast period.

- Radar sensors utilize radio waves for detecting vehicles and objects. Radar sensor calculates the speed and direction of detected objects, which enables ADAS systems to provide safety alerts and take control of driving functions.

- Moreover, radar sensors are used in advanced driver-assistance system for applications involving adaptive cruise control, automatic emergency braking, cross-traffic alert, and blind spot monitoring among others.

- For instance, in September 2023, Valeo and Mobileye announced a new partnership for delivering imaging radars for facilitating next-generation advanced driver assist and automated driving features.

- Thus, the increasing developments associated with radar sensors for ADAS applications are anticipated to boost the market during the forecast period.

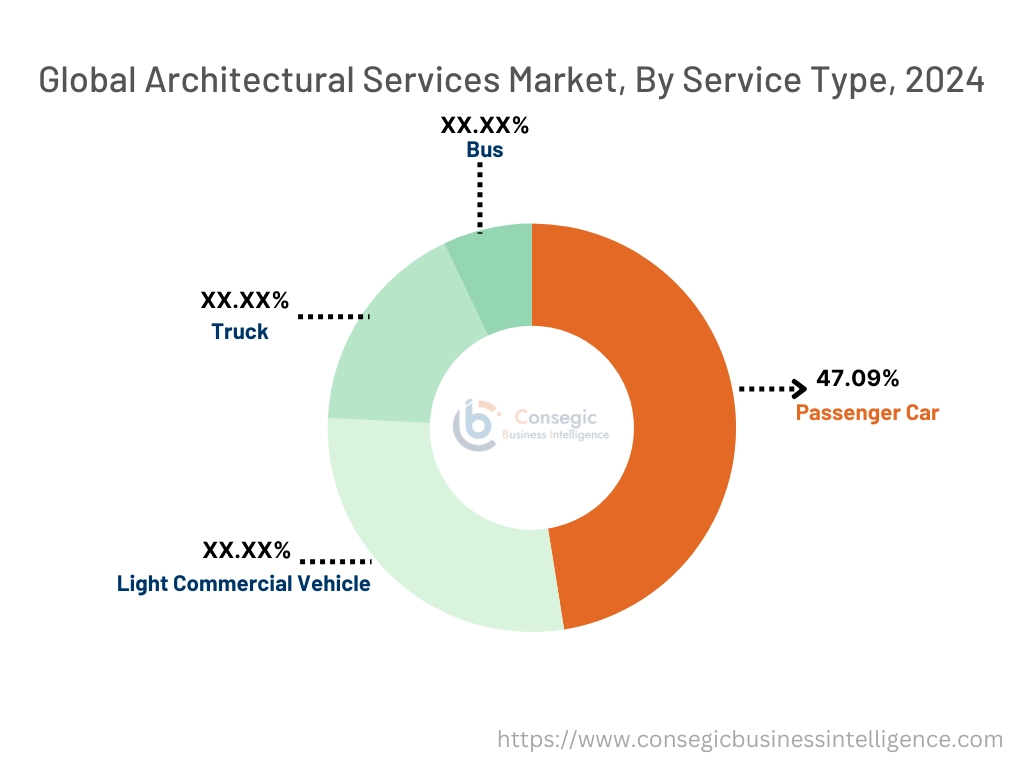

By Vehicle Type:

Based on the vehicle type, the market is segmented into passenger car, light commercial vehicle, truck, and bus.

Trends in the vehicle type:

- Factors including the rising disposable income, growing popularity of luxury cars, and progressions in autonomous driving systems are key aspects propelling the passenger cars segment.

- Factors including the rising sales of heavy-duty vehicles, growing investments in commercial vehicles, and increasing need for economical modes of transportation and logistics are primary determinants for driving the commercial vehicles segment.

Passenger cars segment accounted for the largest revenue share of 47.09% in the total market share in 2024, and it is anticipated to register substantial CAGR growth during the forecast period.

- Advanced driver-assistance systems are primarily integrated in passenger cars for assisting drivers with safe operation of a vehicle.

- Moreover, the integration of advanced driver assistance systems in passenger cars facilitate several vehicle functionalities such as adaptive cruise control, intelligent park assistance, rollover stability control, lane departure warning, blind spot detection, and automatic emergency braking among others.

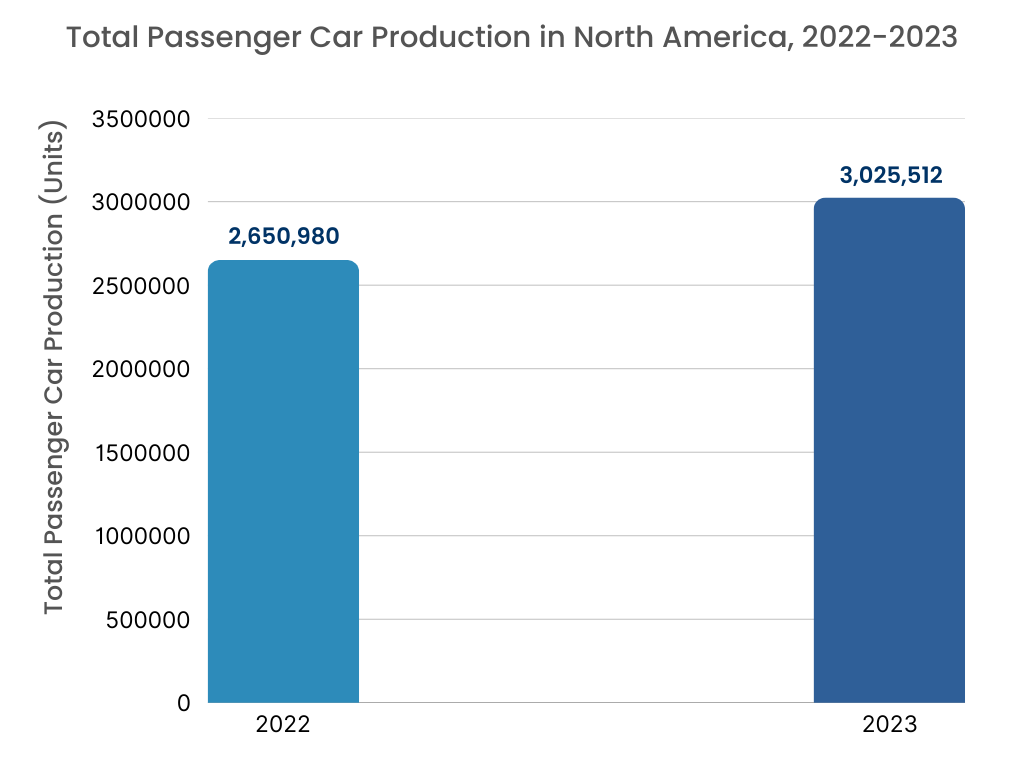

- For instance, according to the International Organization of Motor Vehicle Manufacturers, the total passenger car production in Europe reached up to 15,449,729 units in 2023, representing an increase of nearly 13% from 13,727,841 units in 2022.

- According to the analysis, the rising production of passenger cars is propelling the advanced driver assistance systems (ADAS) market trends.

By Level of Autonomy:

Based on level of autonomy, the market is segmented into L1, L2, L3, L4, and L5.

Trends in the level of autonomy:

- Increasing trend in adoption of L2 advanced driver-assistance system for facilitating partial driving automation.

- Rising technological advancements associated with L5 advanced driver-assistance system for facilitating complete automation of vehicles.

L2 segment accounted for the largest revenue in the overall advanced driver assistance systems (ADAS) market share in 2024, and it is anticipated to register substantial CAGR growth during the forecast period.

- Vehicles equipped with level 2 (L2) ADAS is capable of managing numerous driving tasks, including braking, acceleration, and steering, but still require the driver’s attention and vigilance.

- L2 ADAS enables multiple functionalities to work in unison, such as allowing for adaptive cruise control and lane centering features to operate simultaneously.

- Moreover, L2 ADAS facilitates significant advancement by integrating multiple automated capabilities to enhance driving safety and efficiency.

- For instance, Tesla Inc. offers Tesla Autopilot, which is an advanced driver-assistance system that facilitates partial vehicle automation (Level 2 automation).

- Therefore, increasing developments related to level 2 advanced driver-assistance system are driving the advanced driver assistance systems (ADAS) market trends.

By Electric Vehicle:

Based on electric vehicle, the market is segmented into plug-in hybrid electric vehicle (PHEV), hybrid electric vehicles (HEV), fuel cell electric vehicle (FCEV), and battery electric vehicles (BEV).

Trends in the electric vehicle:

- Factors including the prevalence of net zero emissions target in multiple regions worldwide and rising need for eco-friendly and sustainable automobiles are key aspects driving the battery electric vehicles (BEV) segment.

- Rising advancements associated with hydrogen fuel cell electric vehicles are driving the FCEV segment.

Battery electric vehicles (BEV) segment accounted for the largest revenue in the market in 2024, and it is anticipated to register fastest CAGR growth during the forecast period.

- Battery electric vehicles refer to a type of electric vehicle integrated with only rechargeable batteries.

- BEVs utilize motor controllers and electric motors instead of internal combustion engines for propulsion. The energy required to run battery electric vehicles comes from the battery pack which is recharged from the grid.

- Moreover, battery electric vehicles are zero-emissions vehicles that do not generate any harmful emissions or air pollution hazards as compared to traditional gasoline-powered vehicles.

- For instance, according to the International Energy Agency, the total sales of battery electric vehicles (BEVs) in China reached 5.4 million units in 2023, demonstrating a substantial increase of 22.7% in comparison to 4.4 million units in 2022.

- Therefore, the rising adoption of battery electric vehicles is anticipated to boost the advanced driver assistance systems (ADAS) market growth during the forecast period.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

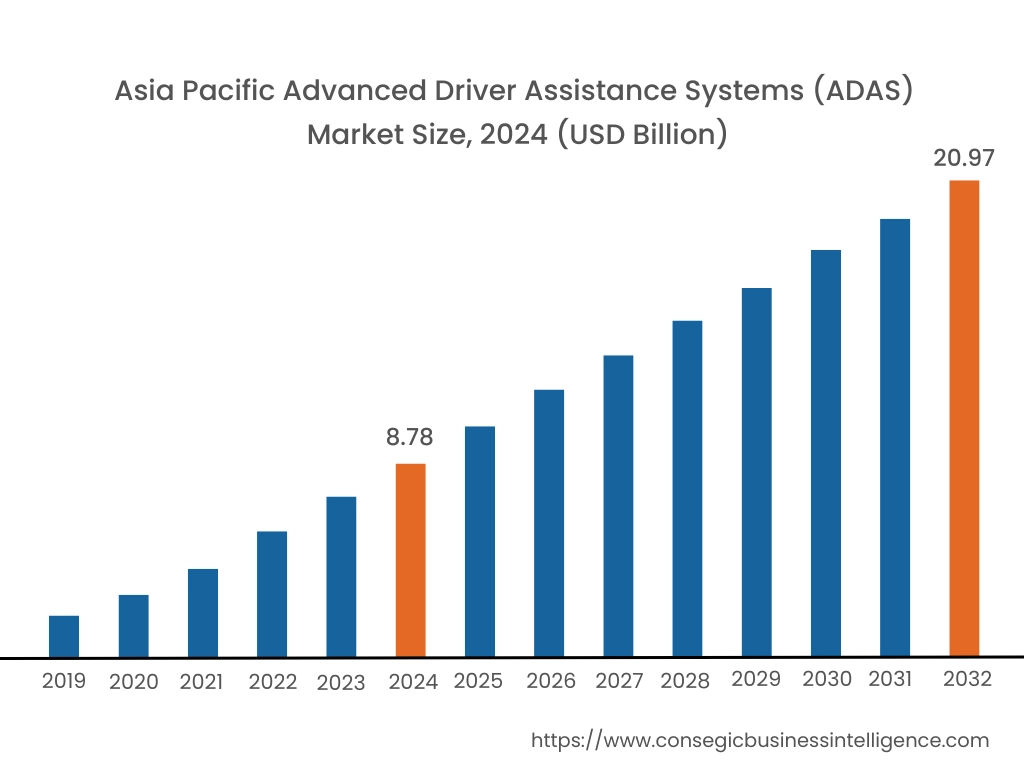

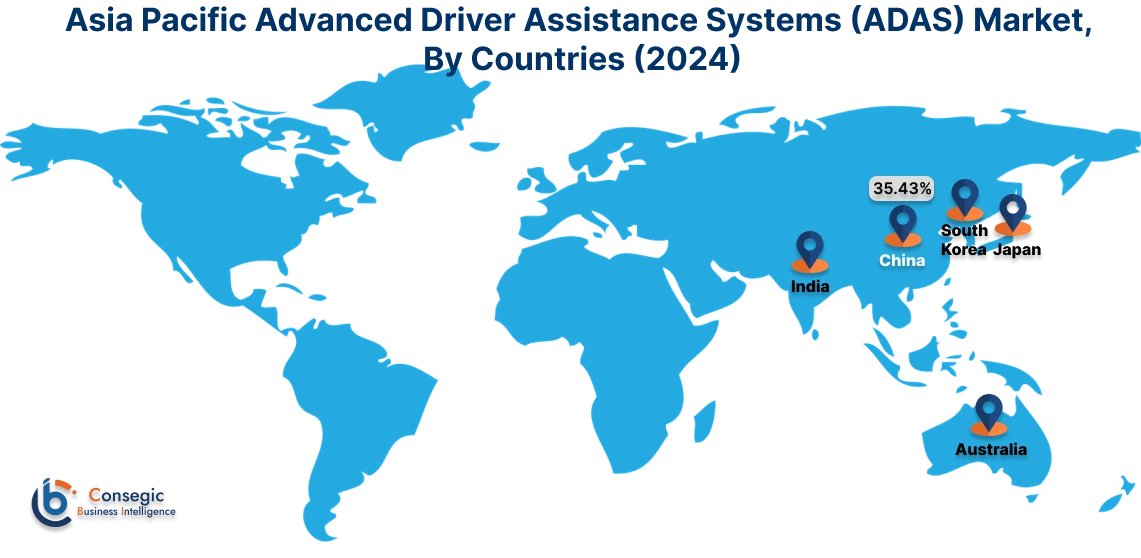

Asia Pacific region was valued at USD 8.78 Billion in 2024. Moreover, it is projected to grow by USD 9.62 Billion in 2025 and reach over USD 20.97 Billion by 2032. Out of this, China accounted for the maximum revenue share of 35.43%. As per the advanced driver assistance systems (ADAS) market analysis, the adoption of driver assistance systems in the Asia-Pacific region is primarily driven by increasing government investments in automotive sector, rising automobile production, and increasing adoption of electric vehicles. Additionally, the rising advancements associated with passenger cars and increasing integration of advanced driver assistance system (ADAS) in modern vehicles are further accelerating the advanced driver assistance systems (ADAS) market expansion.

- For instance, according to the Society of Indian Automobile Manufacturers (SIAM), the total production of passenger cars in India reached 49,01,844 units during FY 2023-24, representing an incline of 7% in comparison to 45,87,116 units during FY 2022-23. The above factors are further propelling the market demand in the Asia-Pacific region.

North America is estimated to reach over USD 29.00 Billion by 2032 from a value of USD 12.51 Billion in 2024 and is projected to grow by USD 13.68 Billion in 2025. In North America, the growth of advanced driver assistance systems (ADAS) industry is driven by rising production of automobiles and increasing adoption of electric vehicles (EVs) in the region. Similarly, rising advancements associated with autonomous vehicles are further contributing to the advanced driver assistance systems (ADAS) market demand.

- For instance, in October 2024, Tesla introduced the Cybercab, the company’s robotaxi, and also announced plans to commence autonomous driving of its Model 3 and Model Y cars in Texas and California states in the U.S in 2025. The above factors are projected to boost the market demand in North America during the forecast period.

Additionally, the regional analysis depicts that the increasing vehicle production, advent of electro mobility, and favorable government measures for integration of advanced driver assistance system in modern vehicles are propelling the advanced driver assistance systems (ADAS) market demand in Europe. Furthermore, as per the market analysis, the market demand in Latin America, Middle East, and African regions is expected to grow at a considerable rate due to factors such as growing automotive sector and increasing investments in electric vehicles among others.

Top Key Players and Market Share Insights:

The global advanced driver assistance systems (ADAS) market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the advanced driver assistance systems (ADAS) market. Key players in the advanced driver assistance systems (ADAS) industry include-

- ZF Friedrichshafen AG (Germany)

- Veoneer (Sweden)

- Valeo (France)

- Texas Instruments (U.S)

- Robert Bosch GmbH (Germany)

- Renesas Electronics Corporation (Japan)

- Infineon Technologies AG (Germany)

- Hyundai Mobis (South Korea)

- Hitachi Astemo, Ltd (Japan)

- Hella GmbH & Co. KGaA (Germany)

- Denso (Japan)

- Continental AG (Germany)

- Aptiv (Ireland)

- NVIDIA (U.S)

- Nidec Corporation (Japan)

- Magna International (Canada)

Collaborations and Partnerships:

- In December 2024, JOYNEXT, in collaboration with Autobrains, developed ADAS (advanced driver assistance systems) technologies that are particularly customized to fulfil the needs of manufacturers of small and compact vehicles. The ADAS solution integrates AI-based perception software with control software in a compact module.

- In September 2023, Valeo and Mobileye announced a new partnership for delivering imaging radars for facilitating next-generation advanced driver assist and automated driving features.

Advanced Driver Assistance Systems (ADAS) Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 80.54 Billion |

| CAGR (2025-2032) | 12.5% |

| By System Type |

|

| By Sensor Type |

|

| By Vehicle Type |

|

| By Level of Autonomy |

|

| By Electric Vehicle |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the advanced driver assistance systems (ADAS) market? +

The advanced driver assistance systems (ADAS) market was valued at USD 34.51 Billion in 2024 and is projected to grow to USD 80.54 Billion by 2032.

Which is the fastest-growing region in the advanced driver assistance systems (ADAS) market? +

Asia-Pacific is the region experiencing the most rapid growth in the advanced driver assistance systems (ADAS) market.

What specific segmentation details are covered in the advanced driver assistance systems (ADAS) report? +

The advanced driver assistance systems (ADAS) report includes specific segmentation details for system type, sensor type, vehicle type, level of autonomy, electric vehicle, and region.

Who are the major players in the advanced driver assistance systems (ADAS) market? +

The key participants in the advanced driver assistance systems (ADAS) market are ZF Friedrichshafen AG (Germany), Veoneer (Sweden), Valeo (France), Texas Instruments (U.S), Robert Bosch GmbH (Germany), Renesas Electronics Corporation (Japan), Infineon Technologies AG (Germany), Hyundai Mobis (South Korea), Hitachi Astemo, Ltd (Japan), Hella GmbH & Co. KGaA (Germany), Denso (Japan), Continental AG (Germany), Aptiv (Ireland), NVIDIA (U.S), Nidec Corporation (Japan), Magna International (Canada), and others.